If you have been reading about federal finances lately, you rightly might assume that the federal government either is, or is about to be bankrupt. The message depends on three facts:

- The speaker or writer does not want to spend money on a particular project and/or

- The speaker or writer is ignorant about federal finances and/or

- The speaker or writer assumes you are ignorant or don’t care.

In many case, all of the above.

The simple fact is that is it functionally impossible for the U.S. federal government to run short of money, become insolvent and/or be unable to pay any debt, no matter how large, even without collecting a single penny in taxes.

Being Monetarily Sovereign, the government has the unlimited ability to create U.S. dollars simply by:

- Voting, then

- Touching computer keys, then

- Spending.

Those three easy steps require no income from any source — not from taxes, fines, tariffs or even the laughably sad “Gifts to Reduce the Public Debt” program (Yes, that’s a real thing.)

Why does the federal government collect taxes?

–To control the economy by taxing what it wants to discourage and by giving tax breaks to what it wants to reward and

–To assure demand for the U.S. dollar by requiring that taxes be paid in dollars.

State and local taxes fund state and local spending, but federal taxes do not fund federal spending.

Here is what the government thinks about funding the military:

Drones, missiles, battleships: What’s in Trump’s $1.5 trillion defense spending ask

By Anna Mulrine Grobe Staff writer, April 29, 2026, 5:00 a.m. ET

The Trump administration is hoping to spend $1.5 trillion on defense next year. That’s roughly 42% more than the United States, by far the world’s most expensive military, spends now.

That’s also getting close to 5% of U.S. gross domestic product. The last time the defense budget was significantly higher as a percentage of gross domestic product was during the Reagan administration’s Cold War military buildup in the mid-1980s, when it reached nearly 7%, or during the Vietnam War, when it was more than 9%.

While the huge budget increase plan aims to make good on President Donald Trump’s campaign pledge to rebuild America’s military, it also represents a big shift in national spending priorities.

It’s a pace that potentially diverts billions of dollars from education, healthcare, and other initiatives while adding roughly $5.8 trillion to the national debt over the next decade.

If the government wished, it could spend an additional trillion or ten trillion on the military, while not “diverting” any money from education, healthcare, etc. and not collecting any taxes at all.

It simply could, as we mentioned, vote, touch computer keys, and spend. That is how Monetarily Sovereign nations always function.

However, the current government wants to cut benefits to the people, because cutting those benefits widens the income/wealth/power gap between the rich and the rest.

The wealthiest 2% already get all the healthcare they want and have no need for social benefits.

It’s the remaining 98% who depend on Medicare, Medicaid, Social Security, and other types of financial assistance. Not receiving these benefits makes them relatively poorer, which makes the rich richer.

In the proposed U.S. military budget for the fiscal year 2027, the Army and Navy would each see their budgets grow by a quarter, while the Air Force would get a 34% boost. The Defense Department’s newest branch of service, the Space Force, stands to see its budget more than doubled to about $71 billion.

Even think tanks that describe themselves as hawkish, such as the Foundation for Defense of Democracies, called the administration’s proposed U.S. military budget for the fiscal year 2027 “extraordinary.”

With a bigger budget than the next nine countries combined, the U.S. already has the most expensive armed forces in the world. In terms of sheer active personnel numbers, America ranks third behind China and India, according to the Peterson Foundation.

Worth noting: The cost of the conflict with Iran is not factored into the current defense request. That will take more money – an additional $1 trillion, by some estimates.

But America’s current war is clearly influencing both public and private investments, in everything from more drones (and defenses against them) to more missiles and Navy ships.

Private investment in the military and defense sectors has surged recently, namely in defense tech and startups. In the first quarter of this year, defense startups backed by venture capital raised $468 million, a 180% increase from the same period in 2025.

There is no shortage of funds for the military, which is important to America’s security, while health, food, housing, education, etc. are not important — at least from the right-wing perspective.

This brings us to the needless and endless efforts to prevent the non-existent threat of federal insolvency:

Social Security benefit cuts are coming — and President Trump shoulders some of the blame

Story by Rich Duprey

Markets and policy headlines have offered up a familiar pattern lately: long-term risks get discussed loudly, then quietly kicked a few years down the road. Social Security is the clearest example of that dynamic. The system still pays full benefits today, but the math underneath it is shifting in a way that investors — and retirees — can’t ignore forever.

So here’s the real question behind today’s headline: benefit cuts are coming, and could be as soon as six years away, yet it’s just as much political shorthand for a much slower-moving problem.

But let’s unpack what the data actually says.

Social Security trust funds face depletion in the early 2030s (around 2033), after which payroll taxes would only cover approximately 77% of scheduled benefits, requiring Congress to choose between raising the payroll tax to ~15%, reducing benefits by 20-25%, raising the wage cap, or increasing retirement age.

The author promulgates the disinformation that the federal government must raise taxes and/or cut benefits. Neither is necessary.

The third –the real— option is for the federal government simply to create the dollars to fund these programs.

But that would shrink the income, wealth, and power gap between the rich and everyone else—the last thing any Republican administration wants to see happen.

The delayed policy response to Social Security’s structural funding gap—where fewer workers per retiree (2.7 in 2025 dropping to 2.3 by 2035) cannot sustain current benefit levels—creates market risk through reduced consumer spending, as retirees account for roughly 19% of total U.S. consumption.

The mistaken belief is that the FICA payroll tax directly funds Social Security. It doesn’t. This idea was introduced by President Roosevelt as a way to discourage Congress from cutting Social Security, using a psychological “I-paid-for-it, so-I-deserve-it” approach.

He even threw in a so-called “trust fund” that was nothing more than an accounting entry, not a genuine trust fund. The idea was to make Social Security look like a private sector insurance annuity.

Unfortunately, it hasn’t worked out, as benefits are being reduced under the “You didn’t pay enough” excuse. It’s like an insurance company saying, “We have to cut your benefits because we didn’t get enough new customers to cover you.” Instead of bolstering Social Security, FICA restricts benefits that the federal government could otherwise provide.

Social Security is not a traditional investment fund. It’s a pay-as-you-go system where today’s workers fund today’s retirees through payroll taxes.

Not exactly. The government still pays for SS benefits, but it limits those payments to what FICA collects, and to compound the lie, it unnecessarily collects taxes on the payments.

Payroll tax rate: 12.4% of wages (split employer/employee); Workers per retiree: ~2.7 in 2025; Projected workers per retiree by 2035: ~2.3. That shrinking ratio is the core pressure point. Fewer workers are supporting more retirees, and that imbalance compounds every year.

You also are supposed to believe that you only pay half of FICA and your employer pays the other half. The truth is that you pay the whole thing, because your employer includes the cost of FICA when figuring what salaries the company can afford.

Finally, notice that the highest salaried employees pay the lowest percentage of their salaries in FICA, and that the very wealthiest earners’ income is not FICA-taxed at all. The money they receive from capital gains and interest is not subject to FICA.

Surprisingly, the system still runs a surplus on paper for parts of the cycle — but that surplus is shrinking fast. The 2025 Trustees Report estimates the combined trust funds will be depleted in the early 2030s, most commonly cited around 2033 for the Old-Age and Survivors Insurance fund.

As we said earlier, they are fake trust funds, created to deceive. Keep in mind that there is no Military Trust Fund to be “depleted.” That would be unthinkable. But cutting Social Security and Medicare is just fine.

That’s the first misconception to clear up: there is no “benefit cut date.” There is a trust fund exhaustion estimate, after which automatic reductions apply under current law.

The clock is ticking toward a 23% automatic benefit cut. It’s not just a retirement crisis—it’s a looming shock to the entire U.S. consumer market. © 24/7 Wall St.

What “Cuts in Six Years” Actually Means

Trust fund depletion timeline (early 2030s); Political delay window (mid-to-late 2020s); Here’s what happens mechanically, based on SSA rules:

After depletion, payroll taxes continue. But they only cover about 77% of scheduled benefits. The gap becomes an automatic reduction unless Congress acts. That’s another way of saying benefits don’t disappear, but they are statutorily reduced if no new funding is added.

Congress easily could act. For instance, it simply could vote to add a few trillion dollars to the “trust fund.” No new taxes would be needed. Congress continually votes to add dollars to various programs, without changing tax laws.

The Congressional Budget Office (2026 Long-Term Outlook) estimates that closing the financial gap would require one of the following:

Policy Option Estimated Impact: Raise payroll tax rate to ~15% Fully closes gap

Raise wage cap (currently $184,500) :Covers ~60% of shortfall

Reduce benefits across the board: 20%–25% reduction

Gradual retirement age increase: Partial long-term fix

The CBO “forgot” one possibility: Add several trillion dollars to the trust fund: The financial gap disappears.

In short, the “six-year warning” is really about when lawmakers must act to avoid automatic reductions later in the 2030s.

The Trump Factor — and the Tax Policy Wildcard

Now to the politically sensitive part of the headline.

During President Donald Trump’s administration and subsequent policy proposals tied to his fiscal agenda, several tax relief measures aimed at seniors and middle-income workers have been discussed in legislative drafts often referred to by supporters as part of a broader “big, beautiful bill” framework.

One frequently cited feature the temporary tax relief for seniors from 2025–2028, structured as deductions or credits designed to reduce taxable income, contained in Trump’s “One Big, Beautiful Bill.”

Here’s where the Social Security linkage comes in:

Social Security is funded primarily through payroll taxes. Certain tax cuts and exemptions reduce taxable wage or income bases. That can indirectly reduce inflows to the trust fund. According to analysis from the Congressional Budget Office, broad-based senior tax relief measures would reduce federal revenue by tens of billions of dollars over a multi-year window.

The Monetarily Sovereign federal government neither needs nor uses tax income for anything. It creates all the dollars it needs and uses. Who says so? These experts say so.

That doesn’t “raid” Social Security in a direct sense. But it does affect the broader fiscal environment the program depends on.

In plain English: If you reduce revenue elsewhere while Social Security already runs a structural gap, you make the fix slightly harder — not impossible, but tighter.

Of course, there is no need for a Monetarily Sovereign government to suffer from reduced revenue. It creates its own revenue.

Granted, supporters of the policy argue the offset comes from broader growth effects and targeted relief for retirees facing higher living costs. That said, the SSA’s own projections do not assume offsetting growth large enough to materially change the depletion timeline.

Again, this all relies on the false claim that FICA funds Social Security.

So the debate isn’t about intent. It’s about arithmetic.

The Real Market-Relevant Risk: Policy Compression

Investors often miss this point because Social Security isn’t a traded asset — but it still affects macro conditions. Why? Because if lawmakers delay action too long, the eventual fix becomes more abrupt. That usually means:

Faster payroll tax increases; More sudden benefit formula changes; Or larger one-time fiscal adjustments

And those ripple into consumer spending.

According to the Bureau of Economic Analysis, households 65+ account for roughly account for roughly 20% of total consumption, meaning any benefit reduction would hit demand directly.

But if the government funds increased benefits, demand would be increased, thereby increasing Gross Domestic Product. The entire economy would benefit.

That’s not theoretical — it feeds into retail, healthcare, and consumer staples earnings.

Key Takeaway

When all is said and done, Social Security is not “collapsing” in six years. It is moving toward a point where lawmakers must choose between higher taxes, lower benefits, or both.

Or, they could choose federal funding, which would grow the economy at no cost to anyone.

Regardless of how headlines frame it, the math doesn’t negotiate.

As my old math instructor used to say, “Figures don’t lie, but liars figure. And there are 535 members of Congress, plus the President, who are lying to you about Social Security and Medicare finances.

The federal government should eliminate FICA and pay for SS and Medicare — for everyone.

Rodger Malcolm Mitchell

Twitter: @rodgermitchell

Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell;

MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell;

……………………………………………………………………..

A Government’s Sole Purpose is to Improve and Protect The People’s Lives.

MONETARY SOVEREIGNTY

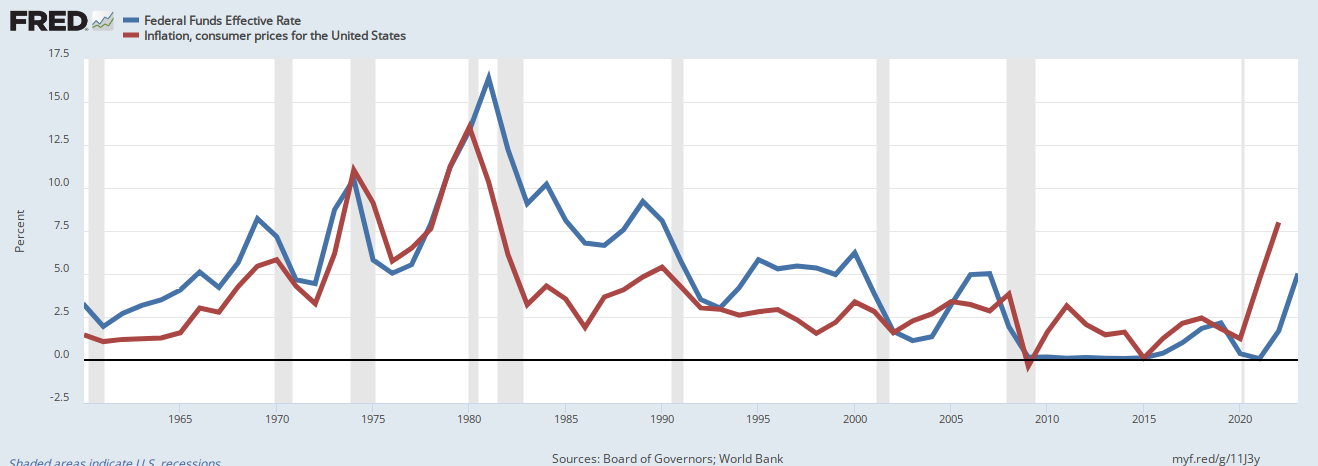

Another strange comment from the Fed: “Although food and energy make up an important part of the budget for most households–and policymakers ultimately seek to stabilize overall consumer prices–core inflation measures that leave out items with volatile prices can be useful in assessing inflation trends.”

Really? Look at this graph and see if you can see why so-called “core inflation” is useful.

Another strange comment from the Fed: “Although food and energy make up an important part of the budget for most households–and policymakers ultimately seek to stabilize overall consumer prices–core inflation measures that leave out items with volatile prices can be useful in assessing inflation trends.”

Really? Look at this graph and see if you can see why so-called “core inflation” is useful.

Why, if the federal government has infinite money, are these expenses not covered, and why are there deductibles and added costs to complete coverages?

You have been told, falsely, that the federal government is like state/local governments, business, you and me, in being monetarily non-sovereign. You have been told falsely, that the federal government spends taxpayers’ dollars and can run short of dollars.

You have been told, falsely, that to provide benefits, the federal government must levy taxes and spend taxpayers’ money.

It’s all a lie.

Why, if the federal government has infinite money, are these expenses not covered, and why are there deductibles and added costs to complete coverages?

You have been told, falsely, that the federal government is like state/local governments, business, you and me, in being monetarily non-sovereign. You have been told falsely, that the federal government spends taxpayers’ dollars and can run short of dollars.

You have been told, falsely, that to provide benefits, the federal government must levy taxes and spend taxpayers’ money.

It’s all a lie.

The graph demonstrates the Fed’s failed attempts to fight inflation (

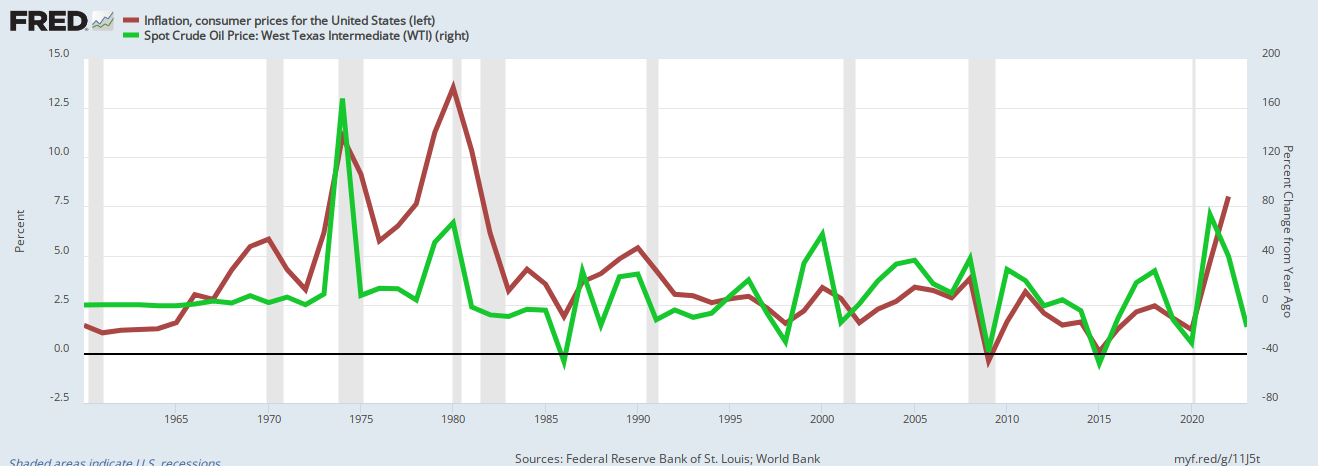

The graph demonstrates the Fed’s failed attempts to fight inflation ( Oil prices (

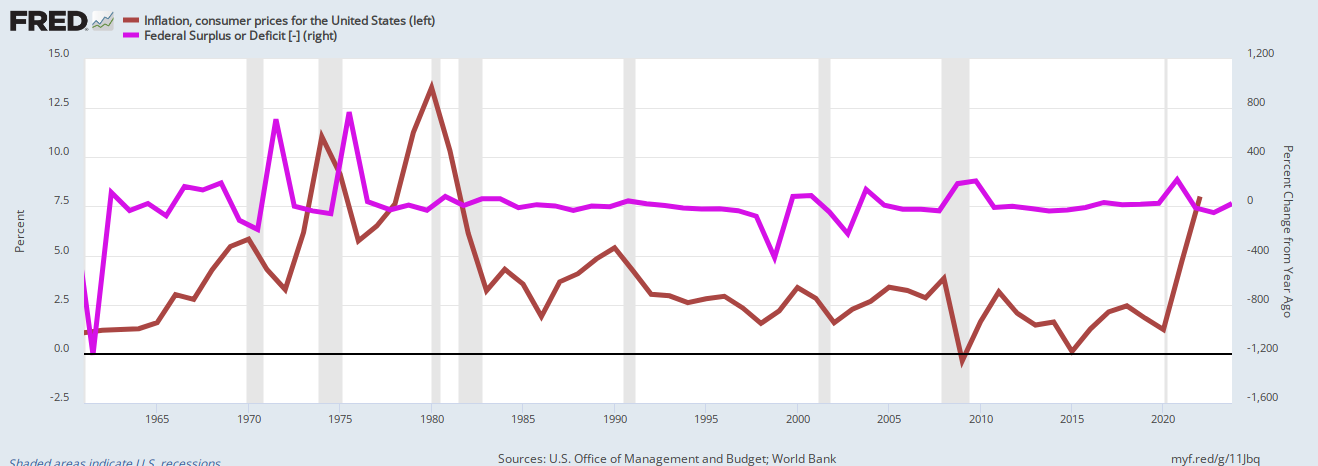

Oil prices ( Changes in federal deficit spending (

Changes in federal deficit spending (