The nation’s leading supplier of federal debt lies, the Committee for a Responsible Federal Budget, has released its latest salvo of utter nonsense:

Here are a few of their baseless claims:

1. The Deficit Could Hit $1 Trillion This Year and $2 Trillion Within a Decade

Although deficits decreased from Fiscal Year (FY) 2011 to FY 2015, they’ve been rising ever since.We now expect deficits to return to nearly $1 trillion this fiscal year (2019) and stay above that level indefinitely.

In fact, if lawmakers extend the costly tax cuts and spending increases indefinitely, deficits will be more than $2 trillion by 2028.

Although the above claims themselves are not baseless, the implication that somehow increases in the federal deficit are bad — that is baseless.

An increasing deficit merely means that the federal government pumps more dollars into the economy that it removes. That is a good thing. It is what grows the economy.

In fact, the opposite of deficits — i.e. surpluses — have been the cause of every depression in U.S. history.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

A growing economy requires a growing supply of money. Austerity (i.e. reduced deficit spending) invariably leads to recessions and depressions.

2. The Long-Term Debt Outlook is Terrifying

This fall, CRFB released its own 75-year budget outlook, which projected an unsustainable fiscal outlook.Under current law, debt will rise from 78 percent of Gross Domestic Product (GDP) in 2018 to 160 percent by 2050 and nearly 360 percent by 2093. Under the Alternative Fiscal Scenario, debt will exceed 600 percent of GDP by 2093.

Why is the high debt/GDP ratio “unsustainable”? It isn’t.

There is no relationship between federal debt and GDP. The debt is not serviced by GDP, nor is it serviced with taxes, exports, or any other form of income.

The federal government is Monetarily Sovereign. It has the unlimited ability to service any amount of debt. It never can run short of dollars.

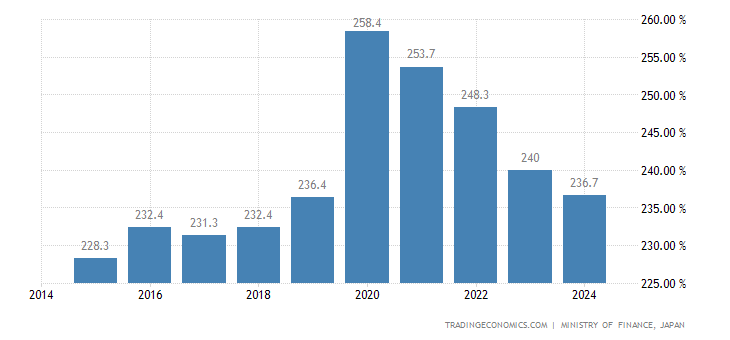

Japan, for example, carries a debt/GDP ratio exceeding 250%, and no one claims this debt is “unsustainable.” See graph, below.

3. “Debt-Financed Laws” Offered a Temporary Stimulus

While the economy has grown by about 3 percent over the past year, our analysis Can America Sustain the Recent Economic Boost? showed that the growth rate would likely return to 2 percent per year.As we illustrated, near-term growth was largely driven by one-time stimulus and other effects from the Tax Cuts and Jobs Act (TCJA), the 2018 Bipartisan Budget Act, and other deficit-financed legislation.

Unfortunately, the economic boost from these laws will be temporary – but the debt will be permanent.

The CRFB admits that economic growth is driven by deficit stimuli.

They also admit that continuing economic growth requires continuing deficit stimuli, which our Monetarily Sovereign government has the infinite ability to provide.

The U.S. government never unintentionally can run short of U.S. dollars. Never. Even if the federal government collected zero taxes, it could continue spending, forever.

So, exactly what is the problem? The CRFB never says.

4. Rapid Economic Growth is Unlikely to Last

In the analysis of America’s recent economic boost, we showed that nearly all forecasters agree that current rapid rates of economic growth are unlikely to last.For example, the Congressional Budget Office (CBO) projects that the economy will grow by 3 percent in 2018 and 2.8 percent in 2019, but then grow by between 1.6 and 1.9 percent per year for the remainder of the decade.

A primary factor in predicting economic growth is federal debt growth. Debt growth creates the dollars that stimulate economic growth.

5. Deficits Shouldn’t Rise When the Economy is This Strong

Typically, a strong economy is paired with low deficits (or even surpluses) – both because strong economic performance produces more revenue and because it creates the economic space for deficit reduction.Yet despite the economy performing at or even above its potential, deficits are widening.

In a recent analysis of deficits and the economy, we showed that the deficit has never been this high when the economy was this strong. 2018 and 2019 are extremely abnormal in that we are running high and rising deficits despite low unemployment, no significant output gap, no recession, and strong economic growth.

The above is a lie of Trumpian proportions. Rising deficits make the economy strong by adding dollars to the economy.

Reduced deficit growth leads to recessions, which are cured by increased deficit growth:

And as you have seen, federal surpluses do not create strong economies. Quite the opposite. Federal surpluses create depressions.

It is true that economic growth brings in higher taxes, but that does not create “economic space for deficit reduction.”

The term “economic space for deficit reduction” is gobbledegook. As long as there are deficits, they always can be reduced, so long as one wishes to experience recessions and depressions.

6. Policymakers are Responsible for More than Half of This Year’s Deficit

This year, the deficit will approach $1 trillion – and policymakers have no one to blame but themselves.We estimate that 55 percent of this year’s projected deficit is the result of deficit-financed legislation enacted since 2015.

Recent spending hikes and tax cuts will cost $540 billion this year. Had these laws been offset or not enacted, the deficit would be $440 billion rather than $981 billion, as CBO projects.

Said more accurately, “Policymakers are Responsible for More than Half of This Year’s Economic Growth, simply because deficits create the dollars necessary for economic growth.”

7. Recent Tax and Spending Bills Both Cost Trillions, If Extended

The Tax Cuts and Jobs Act of 2017 and the Bipartisan Budget Act of 2018 both added tremendously to the national debt.And while the tax cuts will cost significantly more ($1.9 trillion versus $435 billion) over ten years, that is largely an artifact of the most of the tax cuts enacted for eight years, while the spending boost was a two-year deal.

We found that if lawmakers extend both laws indefinitely, the tax cuts will cost about $2.7 trillion over a decade while the spending bill will cost $2.4 trillion. That’s $5 trillion of additional debt that this country simply cannot afford.

The CRFT prays that you not understand Monetary Sovereignty, otherwise you would know that:

- A Monetarily Sovereign government neither needs nor uses tax dollars. It creates dollars by the very act of paying creditors. A Monetarily Sovereign government cannot run short of its own sovereign currency, even if it collects zero taxes.

- Federal debt actually is the total of deposits into T-security accounts. The government does not touch the dollars in these accounts. When the accounts mature, those dollars (plus interest) are returned to the depositors. This not a burden on the government or on taxpayers.

- Tax cuts do not “cost.” They do not “cost” you, me, or anyone else in the economy. They only “cost” the federal government, which uniquely has the unlimited ability to create dollars. Tax cuts benefit the entire economy, and tax cuts for the lower income groups help narrow the Gap between the rich and the rest.

8. Revenue Has Dropped, Not Risen

While some have claimed that revenue grew over the past year . . . we estimated that actual revenue fell by 3.6 percent between tax year 2017 and tax year 2018. Revenue fell by 5.4 percent after inflation, and by 8.1 percent relative to GDP.

Said more accurately, . . . “we estimated that 3.6 fewer dollars were taken from the economy between tax year 2017 and tax year 2018.”

Taking fewer dollars out of the economy helps the economy grow, and the government has no need for those dollars.

And now we come to the real reason why the CRFB exists, why it devotes all its resources to promulgating the “Big Lie”: The Committee for a Responsible Federal Budget is paid by the rich to convince you that your federal benefits should be reduced.

9. Entitlements and Interest Explain Long-Term Debt Growth

While near-term deficits are largely self-imposed, medium- and long-term debt growth are driven primarily by growing costs of Social Security, federal health spending, and interest on the debt. Indeed, these three categories of spending are responsible for over four-fifths of all nominal spending growth over the next decade alone.

Yes, nothing irritates the rich more than you receiving money. This irritation is “Gap Psychology,” the human desire to widen the Gap below you on any economic or social measure, and to narrow the Gap above you.

Gap Psychology drives the appeal of expensive jewelry, cars, homes, and designer clothing. Gap Psychology drives the resentment some have for anti-poverty aids like food stamps and college preferences, as well as immigration.

10. Social Security is Hurdling Toward Insolvency

Social Security costs continue to grow faster than dedicated revenue, and its trust fund is running out.CBO projected that just 13 years from now – when today’s 54-year-olds reach the normal retirement age and today’s youngest retirees turn 75 – the Social Security trust fund will be depleted.

The Trustees project insolvency in 16 years, when today’s 51-year-olds reach the normal retirement age and today’s youngest retirees turn 78. At that point, the law calls for a deep automatic across-the-board cut in benefits.

It is a perfect example of the “Big Lie.”

The federal government cannot run short of dollars, and because the federal government cannot run short of dollars, no agency of the federal government can run short of dollars unless that is what the federal government wants.

The rich run the federal government. The rich want you to believe Medicare and Social Security and Medicaid and every other government program that benefits the not-rich must cut spending.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Alan Greenspan: “Central banks can issue currency, a non-interest-bearing claim on the government, effectively without limit. A government cannot become insolvent with respect to obligations in its own currency.”

St. Louis Federal Reserve: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e.,unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.

There is no “Social Security trust fund.” It is a bookkeeping fiction. The federal government could, if the rich wished, supply unlimited funds to support Social Security and Medicare for every man, woman, and child, of all ages, forever.

11. Rising Health Costs Are Driving Up the Debt

Health care spending is rising even faster than Social Security spending – both as a result of population aging and rising per-person health care costs.In our analysis of health spending and the federal budget, we found that If health spending were held constant at today’s level, debt would stabilize around 90 percent of GDP; if it had been held constant in 2010, debt would peak in about a decade and return to today’s level by 2040.

Said more accurately, “If only you people would spend more out of your own pockets on health care, and take less from the government, the federal debt would be lower, the economy would decline and the Gap between you and the rich would widen.”

12. Tax Expenditures Remain Costly

While Social Security, Medicare, and Medicaid are the fastest growing federal programs, tax breaks remain costly.According to the Joint Committee on Taxation, income tax expenditures will cost about $1.5 trillion per year in lost revenue.

While one goal of tax reform was to dramatically shrink the size and number of these tax breaks, the Tax Cuts and Jobs Act actually only eliminated one significant tax expenditure, and it did little to reduce the overall cost of tax preferences.

In the misleading world of the Committee for a Responsible Federal Budget, the words “Tax Expenditures” are not expenditures at all. They are economic savings.

Those are the dollars not taken from your pockets. Those are the growth dollars that remain in the economy.

Then after telling us that Social Security, Medicare, Medicaid and other benefits to you should be cut, the CRFB suddenly expresses false concern for your future generations:

13. Policymakers are Prioritizing the Past Over the Future

Instead of leaving future generations better off, we’re leaving them with a stack of large bills.Interest payments on the debt are expected to exceed federal spending on children by 2020 and all federal support for children (including tax expenditures and spending) by 2021.

That means we’ll soon be spending more financing the consumption of past generations than investing in our future.

All lies. Future generations will not pay for future federal deficit and debt, any more than current generations pay for current deficits and debt.

Who pays? The government pays for its deficits by creating dollars from thin air, just as it has done ever since it created the very first dollar, way back in the 1780s.

Federal taxes do not fund federal spending. All tax dollars are destroyed upon receipt, and brand-new dollars are created, ad hoc, each time the government pays a creditor.

If interest payments exceed federal support for children, the government could solve that “problem” simply by spending more on children.

Meanwhile, federal interest payments add growth dollars to the economy.

And finally, we come to the biggest whopper of them all:

14. Reducing Debt Would Increase the Size of the Economy

One consequence of a rising national debt is that it crowds out productive investment, which in turn slows income growth.The corollary is that lower debt can actually boost income growth.

CBO estimates that if debt were reduced to its historic average of about 41 percent of GDP by 2048, per-capita GNP (a rough parallel for average income) would be about $6,000 (6.5 percent) higher than under current law.

Simply holding debt at current levels would boost income per person by $4,000 per year in 2048.

This is so laughably wrong, that one wonders how anyone with an IQ above 50 could possibly believe it.

Federal debt, by law and not by necessity, results from federal deficits. Federal deficits are economic surpluses. When the government runs a deficit, the economy runs a surplus — more money enters the economy than leaves it.

It takes a peculiar sort of illogic to claim that adding dollars to the economy “crowds out productive investment, which slows income growth.”

In short, the CRFB and its rich patrons want you to believe that cutting your federal benefits and/or increasing your federal taxes actually increases your income.

If the people who wrote this nonsense actually believe it, they are woefully ignorant of basic economics, and if they don’t believe it, they are shameless liars.

Take your pick.

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

The single most important problems in economics involve the excessive income/wealth/power Gaps between the have-mores and the have-less.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps:

Ten Steps To Prosperity:

1. Eliminate FICA2. Federally funded medicare — parts a, b & d, plus long-term care — for everyone

3. Provide a monthly economic bonus to every man, woman and child in America (similar to social security for all)

4. Free education (including post-grad) for everyone

5. Salary for attending school

6. Eliminate federal taxes on business

7. Increase the standard income tax deduction, annually.

8. Tax the very rich (the “.1%) more, with higher progressive tax rates on all forms of income.

9. Federal ownership of all banks

10. Increase federal spending on the myriad initiatives that benefit America’s 99.9%

The Ten Steps will grow the economy, and narrow the income/wealth/power Gap between the rich and you.

MONETARY SOVEREIGNTY

Impervious aren’t they! I suggest a trick question should be a sole response to these people. It is not really a trick question but it should cut the waffle;

“Can you please define what is the deficit, how it comes about?”

I would give them a 1% chance of getting it right. Every time I have asked what is it, I get only silence, but I haven’t tried the people you mostly quote.

LikeLike

In short, they don’t know what they are talking about; but if they did, they automatically would have to understand Monetary Sovereignty as a possible solution. It’s 2019, and we are in the grip of the Dark Ages.

LikeLike

These are not stupid people. They are paid not to “know.”

LikeLike

I’d really like to live long enough to see how/when this arcane, 180 degree flipped economic thinking is going to right itself in the nick of time.

If money isn’t what we think it is (physically scarce), but what MS says it is (legally abundant), then what’s with the idea of a federal budget? Why not just electronically appropriate credit according to need via bank accounts? For example, federal employees/National Parks need x dollars to go on operating. Bingo. They get xdollars. And so on down each line item.

LikeLiked by 1 person

The real purpose of a budget is to direct and control the economy rather than to limit overall spending. Money is not scarce to the federal government, which cannot unintentionally run short of its own sovereign currency, the U.S. dollar.

LikeLiked by 1 person