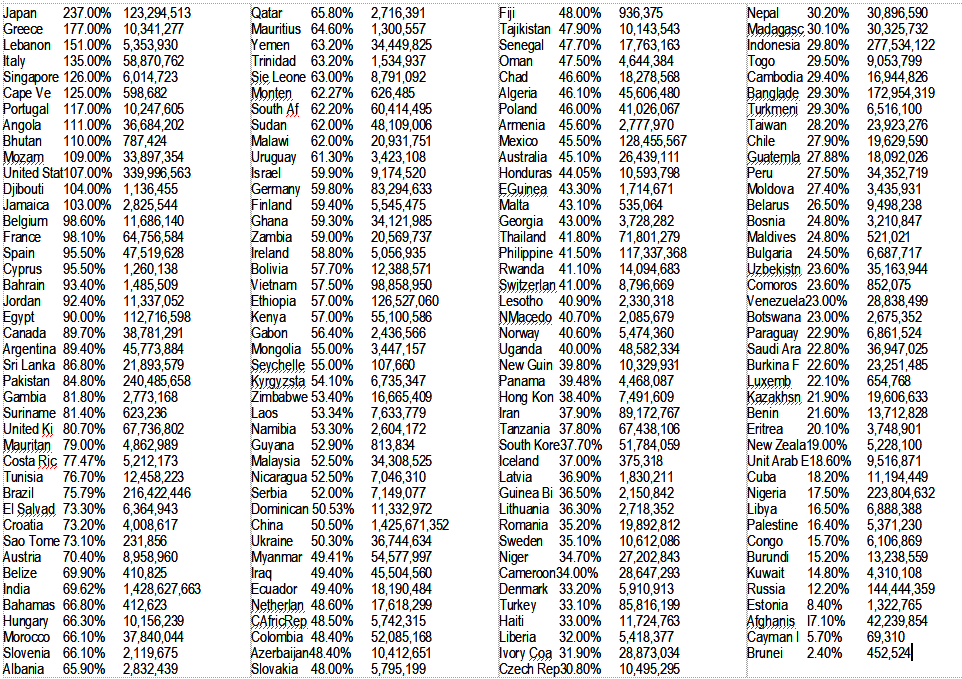

Gross Domestic Product (GDP) is one measure of size, but it is not a measure of health. There is no relationship between the health of an economy and the Debt/GDP ratio. Heather Hennerich’s claim that “GDP serves as a measure of an economy’s overall size and health” simply is false. In fact, the Debt/GDP ratio signifies nothing, nothing at all. Yes, it’s a fraction that is quoted all the time by people who should know better. But you might as well quote an apples/Apple phones comparison. Debt is a cumulative measure of federal government deficits since the beginning of time. GDP is a one year measure of an entire nation’s spending. If you want a similar comparison try the total amount of water a city has wasted vs. the amount of orange juice the mayor drank, yesterday. Call it the “waste/OJ” ratio, and claim it means something. Skim the following list of Debt/GDP ratios, and see if you can find any relationship between the Debt/GDP ratio, the population of the nation, and what you know about the health of its economy. Begin with the fact that wealthy, powerful Japan and weak, impoverished Greece are 1,2 on the list. The United States falls right between Mozambique and Djbouti on the list. Russia has one of the lowest ratios, indicating the “health” of its economy.Debt-to-GDP Ratio: How High Is Too High? It Depends October 07, 2020, By Heather Hennerich

How much federal debt is too much? Is there a tipping point at which it becomes a big problem for a country?

One way to gauge the size of a country’s national debt is to compare it with the size of its economy—the ratio of debt to GDP. (GDP serves as a measure of an economy’s overall size and health, measuring the total market value of all of a country’s goods and services produced in a given year.)

NATION — DEBT/GDP RATIO — POPULATION

This wrongly assumes that federal (Monetarily Sovereign) finances are like personal (monetarily non-sovereign) finances. The federal government does not “finance” its debt. (Here the word “finance” seems to mean pay it off or perhaps pay interest on it.) The so-called “debt” is nothing more than deposits into privately owned, Treasury Security accounts. We say “privately owned” because the federal government never touches those dollars. As a depositor, you alone decide when to take dollars out or leave them in (following certain initial rules). The dollars are yours when you deposit them and when you retrieve them. That’s why they are not a “loan.” If they were a loan, the borrower would control them. But there is no borrower. The federal government never borrows dollars. These accounts are similar to safe deposit boxes into which you place your valuables. Just as the bank never touches those valuables, the federal government, being Monetarily Sovereign, never needs to touch your deposited money. To pay off the so-called “debt” the government merely returns your dollars to you, the depositor. As for the “resources at hand,” we assume this means that in some mysterious way, the government supposedly uses GDP or perhaps Lake Michigan, to pay off T-securities. No one knows how that works. It’s all gibberish and nonsensical.The U.S. federal debt-to-GDP ratio was 107% late last year, and it went up to nearly 136% in the second quarter of 2020 with the passage of a coronavirus relief package.

By comparison, Japan’s ratio at the end of 2019 was higher: about 200%, according to data from the Bank of Japan and Japan’s Ministry of Foreign Affairs and calculations by St. Louis Fed Economist Miguel Faria-e-Castro.

By comparing the total federal debt to the size of a country’s economy, we can see how that government can use the resources at hand to finance the debt, according to Your Guide to America’s Finances from the U.S. Department of Treasury.

Monetarily non-sovereign governments (state, local, euro) use taxes to fund spending. But Monetarily Sovereign governments (US, Canada, Japan, Australia, et al) do not use taxes to fund spending. A huge difference Faria-e-Castro seems not to understand. (And he’s an economist for the St. Louis Fed!!) Monetarily Sovereign governments use taxes to direct their economies by taxing what they want to discourage and giving tax breaks to what they want to encourage. There is scant similarity between federal finances and state/local government finances. Those who do not understand the difference should not be writing for the Federal Reserve. While state/local governments rely on tax income, the federal government could continue spending, forever, with no tax income at all.In his research, Faria-e-Castro explores big questions about the economy, so we asked him about this issue last year.

Deficit spending means that a government is choosing not to raise taxes today to pay for that spending but is choosing to wait until tomorrow, Faria-e-Castro said.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Then we come to this bit of misinformation, that applies to state/local governments, but not to the federal government:The federal government doesn’t borrow dollars. Why would it, given its infinite ability to create new dollars?When federal spending exceeds revenue, the difference is a deficit. The government mostly borrows money to make up the difference.

Greenspan understood Monetary Sovereignty. Too bad he didn’t make his knowledge clear so we no longer would have ridiculous laws mandating a “debt ceiling.” Now, again, the nation is paralyzed by the useless debt ceiling while the GOP demands spending cuts though they have no idea what they want to cut. (They don’t have the courage to admit they really would like to cut Social Security and Medicare, so as to help the rich become richer.)Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

By law, the federal government accepts deposits into T-security accounts equal to the accumulation of federal deficits. This is a point of confusion, because people mistakenly are led to believe that the deposits pay for the deficits. They don’t. The deposits pay for nothing. The purpose of deposits (i.e. T-securities) is to provide a safe place to store dollars, which stabilizes the dollar.The total national debt is an accumulation of federal deficits over time, minus any repayments of debt, among other factors.

This is entirely wrong. You never have endured a “fiscal burden” for previous deficits. The government pays for all its deficits by creating new dollars from thin air. This is not a burden on anyone, not on you and not on the government. The “fiscal burden” myth, promulgated through the decades, is a result of ignorance about Monetary Sovereignty.A big consequence of deficit spending is that the fiscal burden shifts from one generation to the next, Faria-e-Castro said.

It’s only divisive for those who are ignorant about federal finances. “The next generation” doesn’t pay for back debt. The taxes paid by every generation see the same fate: All federal taxes are destroyed upon receipt. Tax dollars are paid from what is known as “the M2 money supply measure.” The moment they are received by the Treasury, they cease to be part of any money supply measure. In short, they are destroyed.That’s fine if a country’s economy is growing, because you know that the next generation will, on average, be better off than the current one, and likely able to pay a little more in taxes to decrease the debt, Faria-e-Castro said.

But if a country’s economy is slowing and economic growth rates are lower than they used to be, “this starts becoming a more divisive issue.”

Here, Faria-e-Castro displays remarkable ignorance of national finance because he doesn’t differentiate between Monetarily Sovereign governments and monetarily non-sovereign governments. The monetarily non-sovereign governments borrow money because they have no sovereign currency.Say the government of “Country X” borrows money to cover its deficits, Faria-e-Castro said. Investors—many of them international—buy that debt and then want to be repaid.

“One day, the president of Country X can just organize a press conference and just tell people, ‘OK. We’re not paying,’” Faria-e-Castro said. “That’s an outright hard default.”

But countries that take that action will have trouble borrowing again. Lenders will be less willing to lend to them and will charge higher interest rates.

Astoundingly, that is precisely what does not happen, and the evidence is there for all to see. Whether one views federal debt as “Federal Debt Held by The Public” (first graph below) or as “Federal Debt as a Percent of Gross Domestic Product” (2nd graph below), there is no relationship between federal debt and inflation.“The president of Country X can call the governor of the central bank and say, ‘OK, you have to print money to pay for this debt,’” Faria-e-Castro said.

In a country where the central bank is not an independent authority, the central bank can be pressured more easily by politicians to start printing money to pay for the country’s debt, he said.

But the flow of new money will invariably lead to high inflation in that country. That erases the value of the debt—a “soft default”—but it also typically kicks off hyperinflation, Faria-e-Castro said.

He thinks the difference between countries has to do with a “strong, central bank.” Poppycock. The central bank of a Monetarily Sovereign nation is strong because Monetary Sovereignty makes it strong. It has the unlimited ability to create its nation’s sovereign currency. Monetarily non-sovereign nations also have central banks. Sadly, these banks are weak because they do not have the unlimited ability to create sovereign currency: They have no sovereign currency to create.Hyperinflation is excessive inflation, with very rapid and out of control general price increases. Economists usually consider monthly inflation rates of above 50% as hyperinflation episodes, as noted in a 2018 On the Economy blog post.

Faria-e-Castro explained, countries that are not politically stable and don’t have independent central banks are not going to have very credible institutions. As a consequence, they can’t borrow easily: Investors won’t be willing to lend them that much for fear of future default.

But the debt of countries with strong institutions and independent central banks—like the U.S. and Japan—doesn’t present the same risks, Faria-e-Castro said.

First, the Bank of Japan “prints” (creates) yen all the time. No “pressure” needed. It’s a normal, daily process. And second, those yen do not pay for the country’s debt. They pay for the country’s purchases. Like the U.S., the Japanese government does not borrow to pay for anything. It creates yen to pay for everything.Few believe, for example, that the Japanese government will ever pressure the Bank of Japan to actually “print” money to pay for the country’s debt, Faria-e-Castro said.

There’s that phony Debt/GDP ratio, again. The U.S. doesn’t borrow. It issues Treasury bills, notes, and bonds, and if not enough are issued to satisfy the law, the Federal Reserve Bank simply buys the rest.“As a consequence, these countries can typically sustain very high levels of debt to GDP,” he said. “Because people really believe that they will be repaid, so they can keep lending.”

No, the Fed determines short-term interest rates by fiat. And that meaningless Debt/GDP ratio is infinitely sustainable.The strength of institutions also affects interest rates on the debt, which is another factor in determining the sustainability of high debt-to-GDP ratios.

When he talks about the “cost of borrowing,” he mistakenly believes government T-securities represent borrowing. They don’t. They represent deposits. These deposits are paid off, not with taxes but by returning the dollars that are in the accounts. And whether interest rates are high or low is irrelevant to a Monetarily Sovereign nation having the infinite ability to create the currency to pay interest.If a country has strong institutions, interest rates on the debt will be low, which means the cost of borrowing will be low, Faria-e-Castro said.

It’s not obvious because Faria-e-Castro is confusing federal financing with private financing. He doesn’t understand the difference between Monetary Sovereignty and monetary non-sovereignty. And he’s speaking for the Federal Reserve!? Yikes! He falls in line with the current mistaken belief that fighting inflations requires the pain of recession that cuts in federal spending beget. That is the kind of leadership that destroys nations. Rodger Malcolm Mitchell Monetary Sovereignty Twitter: @rodgermitchell Search #monetarysovereignty Facebook: Rodger Malcolm MitchellBecause the institutional strength and riskiness of countries varies, there’s no rule of thumb for how high a debt-to-GDP ratio can be before it poses a risk to a country’s economy.

“At the end of the day, it all boils down to strong and independent institutions,” Faria-e-Castro said.

“A lot of economists try to study this. There’s no single measure that we can come up with… Measuring institutional strength is not obvious.”

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

Remind me again: How much of our federal government’s ‘debt’ is in a currency other than our own US Dollar?

LikeLike

0

Deposits in T-bills, T-bonds, and T-notes must be made in U.S. dollars.

LikeLike

If someone owns their own debt are they still in debt? https://wolfstreet.com/2021/04/06/bank-of-canada-holdings-government-of-canada-bonds-rise-to-40-percent-total-outstanding-fed-a-saint-in-comparison-taper-on-table/ The fools to the north used to have Yen debt on their books that someone convinced them they had to offer in the early nineties [all retired now]. https://www.bankofcanada.ca/rates/banking-and-financial-statistics/bonds-outstanding-by-currency-of-payments-and-issuers-formerly-k8/#graph

LikeLike