The sole purpose of government is to improve and protect the lives of the people.

We give the government our money, our time, and some of our freedom, expecting in return safety, stability, opportunity, and a better life. But when a government focuses more on protecting itself than its people, it has failed.

Government is not an end. It is a tool. Tools must serve the maker. A tool that primarily serves itself is broken.

When I owned several businesses, I went to bed each night asking myself four questions:

- What can go wrong?

- How do we prevent it?

- How do we fix it if it happens?

- What can we do better?

That is exactly how our political leaders should run our nation. Unfortunately, the current leadership asks these questions:

- What’s in it for me?

- How can I stay in power?

- How can I get away with it?

- How can I do harm to my political enemies?

What Can Go Wrong? Every economic problem falls into one of three categories:

-

- Demand Failure–People don’t have enough income, so spending collapses, and the economy falls into recession

- Supply Failure–Not enough goods, i.e. shortages, which lead to inflation and recession

- Structural Failure–The system itself breaks down, leading to inequality, stagnation, social instability

Monetary Sovereignty: There are two repeated, false objections to the federal spending that benefits the people.

I. The “who will pay?” objection. The federal government, uniquely being Monetarily Sovereign, has the unlimited ability to create U.S. dollars at the touch of a computer key. (See: Monetary Sovereignty: Who says so?)

Our Monetarily Sovereign federal government does not need or use taxes to pay its obligations. The government pays all its bills the same way:

- Congress votes

- The President approves

- The Treasury creates the money at the touch of a computer key

Thus, with just those three steps, the federal government can fund any program of any size, without collecting a penny in taxes.

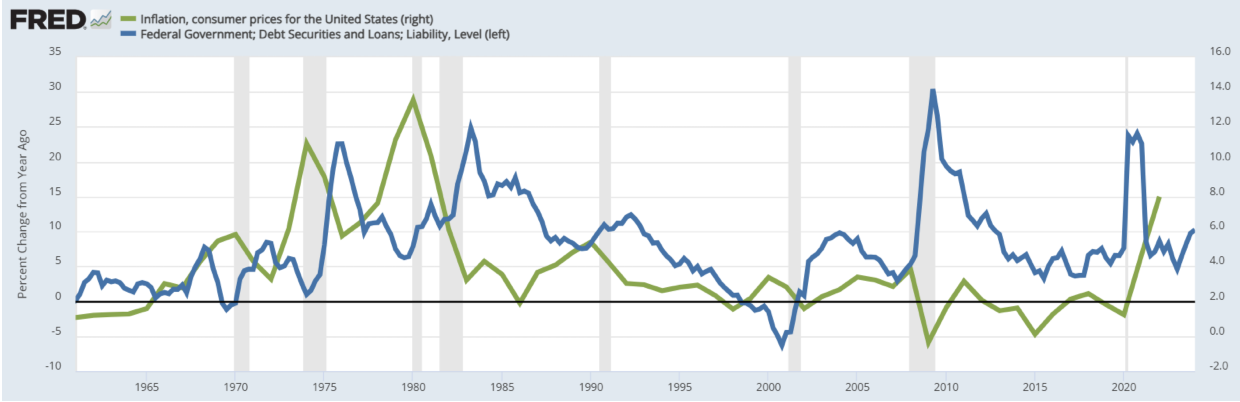

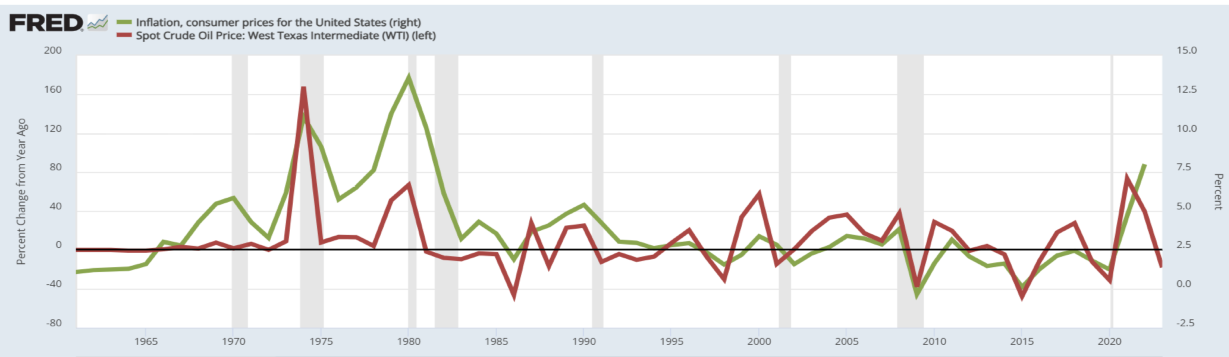

II. The “but that will cause inflation” objection. Federal spending is not a primary cause of inflation. (See: The inflation myths debunked. It’s never “money-printing.” It’s always shortages.)

In fact, inflations are prevented and cured by government spending that addresses shortages. Reduced spending in the face of inflation does nothing to solve the primary problem — shortages — and can exacerbate the problem by causing more shortages.

That is why austerity, aka “belt tightening,” fails as a solution to any economic problem. It is popular among the elite, however, because it tends to widen the income/wealth gap between the rich and the rest.

State and local taxes pay for state and local government expenses, but federal taxes do not fund federal spending. That is the difference between monetary non-sovereignty and Monetary Sovereignty. The states (and business and individuals) primarily are money users, while the federal government primarily is a money creator.

So, why does the federal government collect taxes? Two reasons:

- To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward.

- To assure demand for the U.S. dollar by requiring that taxes be paid in dollars

Federal spending is not funded by federal taxing.

Here are some steps to Prevent and Cure Common Economic Problems While Improving and Protecting the Lives of the People

I. Eliminate the FICA tax. FICA pays for nothing. Neither FICA nor trust funds (See: “The Phony Trust Fund Controversy“) support federal spending. Ending the FICA tax would:

- Increase take-home pay for workers in the lower 95% income bracket

- Reduce employment costs for businesses

- Increase job availability

- Narrow the income/wealth gap between the rich and the rest

- Add billions of growth dollars to the economy

II. Fund Medicare for All. Provide free, comprehensive, no deductible health care insurance for every man, woman, and child in America. Employer-based healthcare traps workers, and creates job lock, fear-based employment inefficiency.

Universal healthcare would:

- Improve health and health care in America

- Allow for labor movement based on economic need rather than medical need

- Increase American longevity

- Increase productivity by reducing the number of sick workers and sick days off

- Add growth dollars to the economy (Gross Domestic Product =Federal Spending + Non-federal Spending + Net Exports

Related programs would:

- Pay schools to educate more medical professionals and workers — doctors, nurses, ancillary workers

- Fund the construction and profitability of more hospitals and rehabilitation centers, especially in rural areas

- Fund the research and development of pharmaceuticals and medical devices.

III. Fund Social Security for All, regardless of age or income. Income security is not charity. SS for all would:

- Help prevent poverty and reduce the need for other welfare services

- Narrow the gap between the rich and the rest

- Benefit business by increasing the demand for products and services

- Add growth dollars to the economy

IV Fund Grades K-16 + Advanced Education for All Who Want It. This would:

- Help increase worker productivity

- Increase scientific advances

- Help make America more competitive vs. other nations

Some intelligent students can’t even afford free college because their families need them as workers, so we suggest:

-

Funding salaries for college students to assure America makes use of its best minds.

V Fund All Forms of Science Education, Research, & Development. R&D is future supply. Without it there would have been no innovation, no growth, no leadership, and America would have fallen behind, becoming more dependent on others.

VI Fund Infrastructure: Roads, bridges, rail, ports, airports, power grids, water systems, local mobility systems.

VII Fund Renewable Energy: This includes R&D and infrastructure for:

- Electric vehicles and charging stations of all kinds — Trains, cars, trucks, boats, planes, people movers, busses,

- Batteries

- Solar panels

- Nuclear

- Geothermal

- Wind

- Hydro

- Wave

VIII Fund Advanced Food Production

- Farming Methods Education, R&D

- Develop more productive, weather and insect resistant, nourishing crops that require less water and fertilizer

- Advanced planting, harvesting, storage, shipping, and delivery methods

IX Fund Affordable Housing

- R&D to reduce the costs of housing (building materials, methods, and locations)

- Tax breaks for home ownership and renting

- Fund trade schools for carpenters, electricians, roofers, etc.

- Fund R&D for alternative building materials.

X Financially support State and Local Governments. Every state, county, city, and local government faces its own unique challenges they know best, along with issues similar to those of others. However, they all share the common struggle of having limited funds to tackle these problems.

- Fund inter-government educational schools and meetings so government representatives can compare notes on problem solving

- Fund the execution of solutions to those problems

- Pay each state a per capita annual award to be used for any specified public purpose.

IN SUMMARY

The federal government, having unlimited access to funds., is best at paying for things, which it can do infinitely. The federal government also is good at addressing inter-state problems that might be intractable for individual states.

By contrast, state and local governments may understand local problems best, but often finds solutions unaffordable.

The recommendation is to combine the strengths of the federal government (paying, mediating interstate problems) with what state and local governments do best (understand local needs and solutions).

The proper combination of federal and state/local strengths and understanding will grow and enrich America while improving and protecting the lives of the people.

Rodger Malcolm Mitchell

Twitter: @rodgermitchell

Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell;

MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell;

……………………………………………………………………..

A Government’s Sole Purpose is to Improve and Protect The People’s Lives.

MONETARY SOVEREIGNTY