Now that Senator Sinema has signed on, the Inflation Reduction Act will pass by the scant majority of 51 to 50, including the Vice President’s vote.

Sinema had opposed closing the so-called carried interest tax loophole. Carried interest is treated as a long-term capital gain. Because it’s taxed at a lower rate than ordinary income, private equity, venture capital, and hedge fund operators benefit.

Presumably, she is in bed with those people.

Giving these over-paid number pushers an extra benefit is an anathema to anyone who wants the Gap between the rich and the rest narrowed. So, on that basis, the loophole should be closed.

But it is a federal tax, and federal tax dollars do not fund anything — they are destroyed upon receipt. So whatever reduces federal taxes (i.e., leaves more money in the private sector) benefits the economy.

The dollars you use to pay federal taxes are part of the M2 money supply measure. When those dollars reach the U.S. Treasury, they cease to be part of any money supply measure. Those dollars are destroyed.

When the government spends, it creates new dollars, ad hoc.

Because the Monetarily Sovereign Treasury has the infinite ability to create dollars, there is no answer to the question, “How much money does the Treasury have?” Thus, no measure includes Treasury dollars.

So, there is good and bad in that loophole, but on balance, including the loophole is good because it benefits the entire private sector.

If the Committee for a Responsible Federal Budget’s numbers are correct, and federal deficits are reduced by $305 billion, that would be recessionary.

Reducing deficit growth causes recessions (vertical gray bars) which are cured by increased deficit growth.

Even worse than deficit growth reduction is debt reduction. That leads to depressions:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. A recession began 2001.

The CRFB predicts the federal debt would be reduced by nearly $2 trillion.

This means the federal government will take $2 trillion from the private sector (aka “the economy”) and destroy those dollars.

The most popular measure of an economy is Gross Domestic Product (GDP). It measures the total spending by the federal government everyone else in America, plus the net dollars flowing in from across our borders.

Mathematically, for GDP to grow, the private sector must have more dollars. A growing economy requires a growing supply of dollars; when the dollar supply shrinks, GDP shrinks. Simple arithmetic.

When GDP shrinks for two or more months, we call that a “recession,” and if the recession is exceptionally severe, we call it a “depression.”

[Depressions are often defined as recessions lasting longer than three years or resulting in a drop in annual GDP of at least 10 percent.]

The CRFB predicts a depression, though you wouldn’t know it from the tone of their article.

The Congressional Budget Office (CBO) just released its score of the Inflation Reduction Act (IRA) of 2022, legislation which would use Fiscal Year (FY) 2022 reconciliation instructions to raise revenue; lower prescription drug costs; fund new energy, climate, and health care provisions; and reduce the budget deficits.

Mixed bag:

Raising revenue is bad. That means “take more dollars from the private sector.” The federal government neither needs nor uses the dollars, while the private sector does both, need and use.

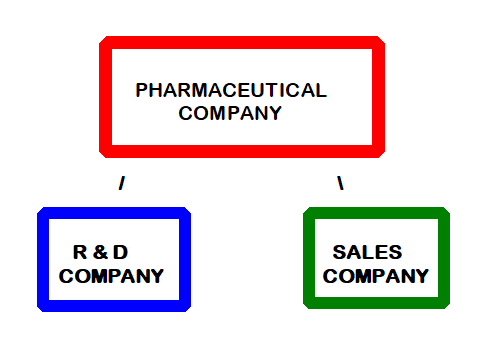

Lowering prescription drug costs would be good if it meant the government was going to pay. Unfortunately, it means the pharmaceutical companies will pay. Dollars will be shifted around in the private sector, and fewer will be available for research and development.

Fund new energy is good if “new energy” will mean “renewable” and “non-polluting.”

The climate and healthcare provisions seem good, depending on how they are implemented. One good thing, the Affordable Care Act will be strengthened financially.

“Reduce the budget deficits” is bad, bad, bad.

Unfortunately, getting the bill through the reconciliation process was legally and politically necessary. But reducing deficits does not reduce inflation.

Inflation is caused by shortages of crucial goods and services, most often oil and food. The only part of the Act that comes even close to reducing inflation is the “fund new energy” part, and again, we’ll have to see how that is implemented.

To call the bill the “Inflation Reduction Act” is both humorous and cynical, but that’s government.

Based on the CBO score, the legislation would reduce deficits by $305 billion through 2031 – including over $100 billion of net scoreable savings and another $200 billion of gross revenue from stronger tax compliance.

Again, that’s $305 billion taken from Gross Domestic Product at a time when the economy is in a recession and needs more, not fewer dollars.

Because the prescription drug savings would be larger than new spending, CBO finds the legislation would modestly reduce net spending by almost $15 billion through 2031, including by nearly $40 billion in 2031.

It’s unclear what the above paragraph is saying, but either $15 billion or $40 billion will be taken from pharmaceutical companies, a loss for the economy.

Once fully phased in, the plan would also slightly cut net taxes by about $2 billion per year – with expanded energy and climate tax credits roughly matching the size of new tax increases.

Cutting taxes benefits the private sector.

The legislation would generate nearly $300 billion of net revenue over a decade.

Translation: The legislation would generate nearly $300 billion of net loss for the economy over a decade.

Unlike prior versions of this reconciliation bill, such as the House-passed Build Back Better Act, this legislation would reduce deficits. Along with other elements of the bill, it is likely to reduce inflationary pressures and thus reduce the risk of a possible recession.

The above paragraph is wrong. Reducing deficits does not reduce inflationary pressures, and it absolutely does not reduce the risk of a possible recession.

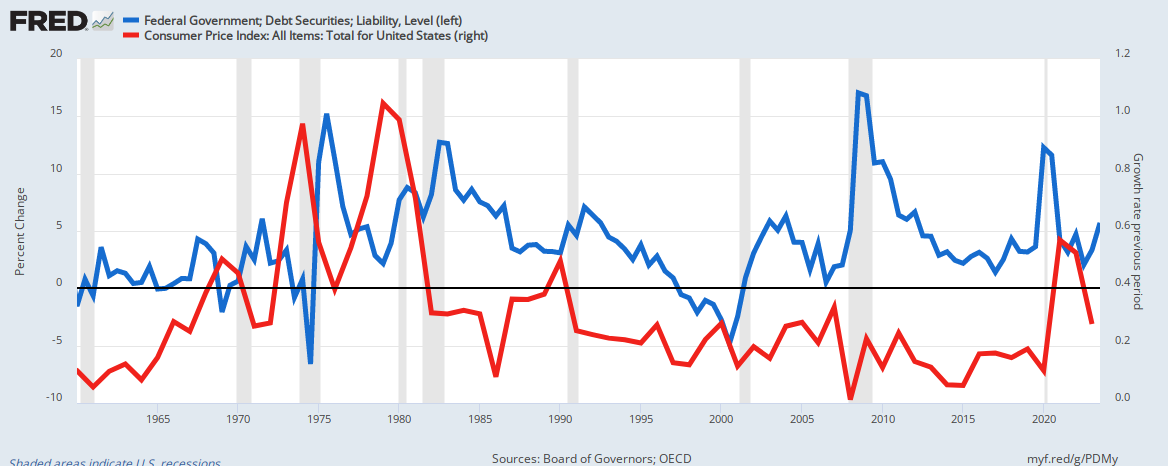

Federal deficits (blue) do not correspond with inflation (red).

SUMMARY Inflation, i.e., a general price increase, is caused by shortages, not federal deficit spending.

Federal deficit spending can cure inflation when the spending helps cure the shortages. Example: Deficit spending to fund more oil/gas production.

Deficit reductions mathematically lead to GDP reductions by taking dollars from the private sector.

The Inflation Reduction Act will do many things, some good and some bad, but it will not reduce inflation.

——-//——-

[No rational person would take dollars from the economy and give them to a federal government that has the infinite ability to create dollars.]

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps: Ten Steps To Prosperity:

Fed Chairman Jerome Powell and President Joe Biden both wish to reduce inflation, prevent (or cure) a recession, and grow the economy.

Both receive the advice of top, uh, well-paid economists. Yet both favor precisely the opposite policies.

Powell admitted he doesn’t have the right tool but insists on continuing with the wrong tool.

Powell recently said, “I do not think the U.S. is currently in a recession, and the reason is there are too many areas of the economy that are performing too well. This is a very strong labor market … it doesn’t make sense that the economy would be in a recession with this kind of thing happening.”

Translation: He doesn’t understand what’s happening but denies it’s a recession.

Yet he raised interest rates by 0.75 percentage points for a second consecutive time to “cool” the economy.

By “cool,” he means the economy is growing too fast, which causes inflation.

He wishes to slow economic growth, which in his opinion, will cure inflation but not cause the recession he denies already is happening. Apparently, Powell thinks the opposite of “inflation” is “recession.” But the two can occur together in what’s called “stagflation.”

Prices are a function of supply and demand.Inflation occurs when there is an imbalance: Too little supply to meet the demand. Today’s inflation, and indeed all inflations through history, are not caused by demand growth but by supply shrinkage.

Historically, demand increases are not sudden, but supply decreases can come overnight. So markets can adjust to the former but struggle to adapt to the latter.

Today, we have the confluence of many shortages: Oil (energy), food, transportation, computer chips, autos, lumber, appliances, homes, labor, and many items related to the basic shortages. In terms of inflation, the single most crucial shortage is the oil (energy) shortage.

Since the cause of inflation is shortages, curing inflation requires curing shortages.

But Powell’s interest rate increases do not address shortages. They do not increase supply. Interest rate increases reduce both supply and demand. They reduce supply by making borrowing by manufacturers more expensive. They reduce demand by making borrowing by consumers more expensive.

Powell hopes that his rate increases will cut demand more than supply. He has no way to know or control whether this will happen. It’s just a hope.

But Jerome, be careful what you hope for; cutting demand impoverishes the supplier section, which leads to a recession.

To quote the Wall Street Journal:

Inflation is a global phenomenon inflicting significant financial pain on families everywhere. Rising costs are an urgent problem, and interest rates play a key role in maintaining price stability.

But urgency is no excuse for doubling down on a dangerous treatment.

As with any illness, the right medicine starts with the right diagnosis.

Unfortunately, the Fed has seized on aggressive rate hikes—a big dose of the only medicine at its disposal—even though they are largely ineffectiveagainst many of the underlying causes of this inflationary spike.

It’s a global problem, as is COVID, but the U.S. can solve this problem within our borders if we use the correct solutions.

As we often have said, the Fed has been tasked with a problem for which it has no tools — shortages of crucial goods and services. Only Congress and the President have the tools to cure shortages.

Mr. Powell has acknowledged this. He noted that elevated interest rates likely wouldn’t bring down gasoline or food prices. “There are many things we can’t affect,” he admitted —namely, the key causes of today’s inflation.

This is a monumental admission. The man tasked with curing inflation has admitted he doesn’t have the tool to do the job. Still, he persists in using that one tool that will lead to recession.

Higher interest rates won’t end skyrocketing energy prices caused by Vladimir Putin’s war on Ukraine. They won’t fix supply chains still reeling from the pandemic.

And they won’t break up the corporate monopolies that Mr. Powell admitted in January could be “raising prices because they can.”

If the Fed’s interest-rate hikes won’t address many causes of today’s inflation, it’s worth asking: What would they do?

When the Fed raises interest rates, increasing the cost of borrowing money, it becomes more expensive for businesses to invest in their operations.

As a result, employers will slow hiring, cut hours and fire workers, leaving families with less money. In the bloodless language of economists, that’s referred to as “dampening demand.”

It also is referred to as “causing a recession.”

But make no mistake: If the Fed cuts too much or too abruptly, the resulting recession will leave millions of people—disproportionately lower-wage workers and workers of color—with smaller paychecks or no paycheck at all.

But that is the whole plan. Make lower-wage workers and workers of color pay to stop inflation. The general sends the poor to the front, not caring how many die.

Mr. Powell has even conceded that the Fed’s actions may lead to a downturn, saying recession “is not our intended outcome at all, but it’s certainly a possibility.”

If all you have is a hammer, every problem looks like a nail. Who cares whether it works or not?

Despite these warnings, the Fed chairman still has cheerleaders for his rate-hiking approach. Chief among them is Larry Summers. “We need five years of unemployment above 5% to contain inflation—in other words, we need two years of 7.5% unemployment or five years of 6% unemployment or one year of 10% unemployment,” the former Treasury secretary recently told the London School of Economics.

You read that correctly: 10% unemployment. This is the comment of someone who has never worried about where his next paycheck will come from.

What can I say about Larry Summers that I haven’t said here, here, here, here,here, and here? The man has my admiration for his ability to fail into better jobs repeatedly.

Summers is a magical example of the Peter Principle: Being promoted to his level of incompetency is his sole success. What next, Larry? Kill the elderly to cut Social Security costs?

If Messrs. Powell and Summers have their way, the resulting recession will be brutal.

As in past downturns, Republicans in Congress will press for austerity—tax cuts for giant corporations and the rich, weaker regulation on big businesses, and little economic support for the most vulnerable.

Democrats should be ready to reject the Republican playbook and prepared to help working families survive.

Well, maybe, just maybe, the Dems are listening, especially if Sen. Joe Manchin remembers he’s a Democrat.

From Axios:

President Biden has slowly but substantially re-engineered significant parts of the American economy — achievements obscured by COVID, inflation and broad disenchantment. e domestic semiconductor industry, and accelerated U.S. viral research and vaccine production capabilities.

He might be on the cusp of the biggest domestic clean-energy plan in U.S. history.

Interestingly, it all has an America First twist— drilling more oilhere … fixing infrastructure here … moving chip-making here … increasing manufacturing jobs here … creating vaccines here.

The $280 billion CHIPS and Science Act provides grants, tax credits and other incentives to manufacture computer chips in the U.S. The White House says it’ll eventually lower the price of cars, dishwashers and computers.

Biden could get another huge win with the climate plan secretly negotiated by Senate Majority Leader Chuck Schumer and Sen. Joe Manchin. The package would provide new tax credits for buying EVs — plus rebates for buying efficient appliances and weatherizing homes, and tax credits for heat pumps and rooftop solar panels.

Biden’s $1 trillion infrastructurebill to rebuild roads, bridges and rail is one of the biggest packages signed by a president ever.

The Biden administration said it’ll pour $3 billion into the vaccine supply chain, creating thousands of U.S. jobs, and helping prepare for future threats.

Electric-vehicle manufacturing is growing in the U.S., with GM and Ford announcing plans for massive vehicle and battery plants across the Midwest and Appalachia. Fun fact: GM’s Mary Barra, who also chairs the Business Roundtable, is the CEO this White House has hosted most often.

These developments required bipartisanship (remember that?) — something Biden promised but gets little credit for, since these thin bands of Republican support look nothing like traditional bipartisanship.

Not only did Biden land these economic measures and a gun-control bill, but same-sex marriage protection is getting close — baby steps, but in a once unthinkable direction.

Biden has only a bare 50-50 Senate “majority” (depending on Sens. Manchin and Sinema). Even then, he is limited by reconciliationto avoid a purely political GOP. It has no ideas for anything but will filibuster everything the Dems submit.

Somehow, Biden managed to accomplish far more than Trump ever dreamed of. This is partly because Trump is an incompetent, corrupt psychopath, who cares only about himself, and the GOP is a crooked election machine.

But much credit belongs to “weak, timid” Biden, who plays the long game, insults no one, closes no doors, knows how to negotiate, and doesn’t whine about everyone else being at fault.

Whereas Trump split his time evenly among golf, tweeting insults, and self-aggrandizement, Biden moved slowly, quietly, but surely to accomplish, accomplish, accomplish.

Now, if only Powell would stand up and say, “I don’t have the right tool. Interest rates won’t cure shortages. Congress must pass spending bills to end key scarcities. That would end inflation and enrich the economy. And the people would thrive.”

That bit of honesty would send more shock waves through Congress than the attempted coup did.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps: Ten Steps To Prosperity:

What process should HHS use to set the price for a drug?

Will the new system set prices only for a limited number of high-cost drugs that lack therapeutic alternatives or more broadly by including drugs that compete with other medicines?

Does the specified price represent the actual price for all sales of a drug, or is it a “ceiling” price, with payers retaining the ability to negotiate lower prices?

Will drug prices set by HHS apply to a narrow or broad population (e.g., only Medicare Part B or Part D beneficiaries or all patients, regardless of their insurance coverage)?

How would HHS assess and incorporate the value of a drug when establishing its acceptable price?

How should HHS select drugs for lowered prices?

The answers are complex, filled with “It depends” and “Maybes.”

The truth is we already havequite a bit of federal price controls, some helpful, some not. The question arises because many people now favor government negotiation of pharmaceutical prices.

Consider this brief video. It shows a woman weeping. She was suffering because the cost of a lifesaving drug was beyond her ability to pay.

In response to many thousands of similar, heart-rending stories:

U.S. Sens. Cory Booker (D-NJ) and Mark R. Warner (D-VA) reintroduced legislation to help lower the costs of needed medical care and prescription drugs for children.

The Fair Drug Prices for Kids Actwould give states the ability to purchase prescription drugs at the lowest price possible, reducing the cost of prescription drugs for children who receive coverage through the Children’s Health Insurance Program (CHIP) and generatingimmediate savings for states and the federal government.

Actually, it’s not “the lowest price possible.” It’s the lowest price being offered, anywhere. And it’s state governments that would negotiate.

But that is a digression from our real question. Should the federal government determine prices for pharmaceuticals?

Senior living: Medicare could get to negotiate drug prices under Democratic billBy KAISER HEALTH NEWS |PUBLISHED: July 25, 2022Democratic senators recently took a formal step toward reviving President Joe Biden’s economic agenda, starting with a measure to let Medicare negotiate prices with drugmakers and to curb rising drug costs more broadly.

A similar proposal died in December when Sen. Joe Manchin, D-W.Va., decided to oppose Biden’s $1.9 trillion Build Back Better bill, which also included provisions allowing for Medicare drug negotiations.

Reining in drug costs has long been wildly popular with the public, with more than 80% of Americans supporting steps such as allowing Medicare to negotiate and placing caps on drug price inflation.

The bill revealed in early July would do both. It would also limit annual out-of-pocket drug costs for Medicare beneficiaries to $2,000, make vaccines free for people on Medicare and provide additional help for lower-income seniors to afford their drugs.

The heart of the bill is the negotiation provisions.

Under the legislation, Medicare could start the new pricing procedures next year, with the secretary of Health and Human Services identifying up to 10 drugs subject to bargaining. The resulting prices would go into effect in 2026. As many as 10 additional drugs would follow by 2029.

The use of the word “negotiate,” when talking about the federal government, is ludicrous if one side has all the power.

The federal government arbitrarily can set an unprofitable price for any drug. But, that drug won’t be sold, which is unacceptable to the public or drug companies.

The populace, which has a limited amount of money available for any spending, always wants, often needs, feels it deserves, and usually will vote for, lower prices.

The federal government, being Monetarily Sovereign, has an unlimitedamount of spending money.

With no more effort than to touch a computer key, it can pay the full, asking prices for any drugs, or it can set prices by law. Clearly, when people are made to suffer from high prices, market forces are not working.

So why not either:

Have the federal government pay the asking price for all drugs and offer them free to the people or,

Have the government set an “affordable” price for all drugs, despite what the drugmakers want.

Solution #1 has problems: Healthcare providers, including pharma makers, would jack up prices to astronomical levels, and simply feed off the government’s trough.

There would be no profit motive for the Research & Development of new drugs, because the current drugs would provide infinite profits.

Government price-setting is a risky business. It often has the opposite results from what one would hope. Rent controls are a perfect example.

Limit rents, and landlords will refuse to maintain or upgrade apartments.

Costly, time-consuming, not itself profitable.

Limit profits, and fewer people will become doctors; fewer hospitals will upgrade ; fewer new drugs will be created; fewer patients will be served.

Solution #2 also has problems. It too would not provide the profits needed for the Research & Development of new drugs, especially drugs for rare diseases and low-profit categories (anti-biotics, for example).

Sincethe Orphan Drug Actwas signed into law in 1983, the FDA has approved hundreds of drugs for rare diseases, but most rare diseases do not have FDA-approved treatments.

The FDA works with many people and groups, such as patients, caregivers, and drug and device manufactures, to support rare disease product development.

In one sense, Medicare already does #2.

Without negotiation, it sets the healthcare prices it is willing to pay, on a take-it or leave-it basis with healthcare practitioners.

That policy has generated the “concierge doctor” system. For annual fees, primary care (usually) doctors can limit their practices to a manageable 600-800 patients, allowing plenty of time to devote to each patient.

This compares with the more typical 2500+ patient load, characterized by quick, robotic diagnoses, treatments, then on-to-the-next.

There is a commonality to the problem of all federal price setting. It doesn’t pay for improvements.

When rents are controlled, landlords don’t maintain or upgrade. When doctor’s fees are controlled, doctors are not rewarded for being better doctors. They are not rewarded for doing the daily “R&D” to keep themselves up to date with the latest procedures. Nor are they rewarded for taking more time with patients.

When the primary reward is numbers sold — how many apartments, how many patients, how many sales — hospitals, convalescent homes, pharmaceutical companies, etc. are rewarded for more, but not for better.

You have heard that the Federal Reserve is trying to cure inflation by raising interest rates slowly.

And you may repeatedly have read on this site (here, and here, and here, and here) that the Fed does not have the best tools to stop inflation, and that despite their best efforts, inflation will continue and be joined by recession..

The Fed has two tools: Raising interest rates and to some degree, reducing money-supply growth.

Contrary to popular belief, neither can cure inflations, but both are very good at creating recessions.

Sadly, a recession is not the opposite of inflation. (Deflation is.) A recession is the opposite of growth and prosperity. The Fed is trying to cure inflation via recessionary means.

Today, as we predicted, the Fed is failing miserably in its assigned task.

The annual inflation rate for the United States is 9.1%for the 12 months ended June 2022, the largest annual increase since November 1981 and after rising 8.6% previously, according to U.S. Labor Department data published July 13.

Since the Fed doesn’t have the tools to cure inflations, who does? As you will see, Congress and the President have that power. But, out of ignorance, intent, or political chicanery, Congress and the President won’t use their power of the purse to prevent or end inflation.

To explain this, we first must discuss the myth that raising interest rates cures inflation.

It isn’t a secret that prices have risen over the past year. Americans have seen the highest inflation rates since 1982, based on the CPI (Consumer Price Index), which increased by 0.8 percent in February and 7.9 percent YoY.

Now, the Federal Reserve is about to raise interest rates.

The CPI measures the average change over time in the prices for urban consumers on typical consumer goods and services.

Although raising interest rates might seem harsh when prices are already high, it’s intended to eventually lead to a drop in inflation.

The primary reason the Federal Reserve (or the Fed) raises interest rates is to cause a slowdown in economic growth.

Interest rates determine how costly it is for consumers and businesses to borrow.

Economic growth is not the same as inflation. We can have fast economic growth without inflation, so slowing growth is not a cure for inflation.

Yet, the purpose of raising interest rates is to slow growth, and that is recessionary.

When no one is rich or poor.

A recession is “a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.”

The Fed does not want to cause a recession, so its interest rate increases must slow economic growth (i.e., GDP growth) while not causing GDP to fall.

The Fed hopes that by raising interest rates, consumers and businesses will delay new investments, which will help lower demand and temper prices.

The Gapbetween the rich and the rest is what makes them rich. Without the Gap, no one would be rich. We all would be the same. The wider the Gap, the richer they are.

Although that is what the Fed claims to hope, delaying new investments does not lower demand.

It likely willlower supply by discouraging investment in Research & Development and production.

Let’s examine the logic. Inflation exists when the demand for critical goods and services exceeds the supply of those goods and services, creating shortages.

Shortages cause all inflations. ALL.

Because reducing demand leads to recessions, the non-recessionary prevention/cure for inflation is to increase the supply of scarce, critical goods and services.

Here are some of the critical goods and services for which supply must be increased:

I. Oil. As we have shown in several previous posts (here, here, here, here, etc.), inflation is highly impacted by the price of oil. It is the most critical product affecting inflation.

Oil prices are determined by scarcity. Inflation (red) closely parallels oil scarcity (blue).

Every industry and virtually every product and service uses oil in some way. Any increase in oil prices will cause a general rise in product/service prices (aka inflation).

Oil prices are determined by scarcity.

It is essential to reduce the oil shortage to fight inflation.

The oil shortage could be cured by reducing demand, but that would be recessionary.

The non-recessionary method for reducing the oil shortage involves federal fundingfor oil research, exploration, drilling, refining, and distribution, plus federal funding for oil substitutes like solar, wind, geothermal, electrical, nuclear, etc. power.

More federal funding, not less, could cure inflation. Interest rate manipulation does nothing to increase the supply of oil.

Higher interest rates could exacerbate the oil scarcity situation by negatively affecting the oil supply.

Interest rate manipulation can affect the oil demandonly to the degree that it depresses the economy. Exchanging recession and depression for inflation is a bad tradeoff, yet that is the Fed’s solution.

II. Food. Second to oil, food is the next most crucial inflation-related product. Food shortages have caused many hyperinflations around the world.

The infamous Zimbabwe hyperinflation began when the government took farmland from experienced white farmers and gave it to inexperienced black farmers. The predictable result: A massive food shortage leading to an equally massive increase in food prices.

Raising interest rates will not help farmers grow more food.

An ongoing outbreak of highly pathogenic avian influenza (HPAI) reduced the U.S. egg-layer flock and drove a 5.0-percent increase in retail egg prices in May 2022 following a 10.3-percent increase in April.

Higher interest rates will not cure the meat and egg shortage.

The ongoing HPAI outbreak has also contributed to increasing poultry prices as over 40 million birds in 36 States have been affected.

The disease prevalence also impacts international demand for U.S. poultry. Price impacts of the outbreak will be monitored closely.

Poultry prices are now predicted to increase between 13.0 and 14.0 percent, and egg prices are predicted to increase between 19.5 and 20.5 percent in 2022.

Higher interest rates will not solve the poultry shortage.

Fish and seafood prices are now predicted to increase between 8.5 and 9.5 percent in 2022.

Higher interest rates will not cure the fish and seafood shortage.

Rapid increases in the consumption of dairy products have driven increases in retail prices in recent months.

This trend continued in May 2022 with a 2.6-percent increase in the prices for dairy products.

Dairy product prices are predicted to increase between 10.5 and 11.5 percent in 2022.

Higher interest rates will not cure the dairy shortage.

Following large price increases in January–May 2022, forecast ranges for fats and oils, processed fruits and vegetables, sugar and sweets, cereal and bakery products, and other foods have been adjusted upward.

In 2022 compared with 2021, fats and oils prices are predicted to increase between 14.0 and 15.0 percent, processed fruits and vegetables prices between 7.5 and 8.5 percent, sugar and sweets prices between 6.5 and 7.5 percent, cereal and bakery product prices between 10.0 and 11.0 percent, and other food prices between 10.0 and 11.0 percent.

Higher interest rates will not cure food shortages unless the plan is to force people to starve because of food scarcity and unaffordability.

A plan to solve inflation by forcing people to eat less food is repugnant to any but the most heartless demagogue. Yet that is exactly the Fed’s plan.

Interest rates are the Fed’s primary tool for impacting inflation. Borrowing is more expensive, but on the plus side, earnings on high yield savings accounts increase.

An increase in earnings on high-yield savings accounts cannot begin to offset the damage of inflation. It’s like using a sponge to offset the floods caused by global warming.

The food shortages can be moderated by additional federal deficit spending to support farming.

The government should pay farmers to grow rather than pay them not to grow, as was done when there were surpluses.

Additional federal fundingfor farmer education, the use of more efficient land use and crops, farm insurance, modern farm equipment, and shipping would reduce the shortage of farm products.

Strangely, the Fed focuses on “core inflation” which eliminates consideration of oil and food, the primary inflationary instigators. It’s like eliminating thoughts about hitting and pitching to arrive at “core” baseball wins.

III. Labor. COVID precipitated a labor shortage that has not abated. Federal deficit spending for the development and administration of vaccines and other healthcare helped moderate the shortage of labor.

Although the shortage, which manifested during COVID, and still continues, other factors were involved, notably compensation.

The salaries and benefits being offered were not tempting enough for many potential workers.

While the right-wing favors cutting benefits to force employees back to work, the more humanitarian approach is to increase remuneration.

Not only are employers forced to cut salaries to make room for FICA, but employer-provided healthcare insurance is an additional employment cost that must be considered when determining salaries.

These costs could be eliminated, salaries could be raised, and more people would come to work, if the federal government funded comprehensive, no-deductible Medicare for all, and took that burden from the salary consideration.

That reduction in labor scarcity would require additional federal deficit spending.

The Federal Reserve plans to raise interest rates several times in 2022.

The Fed’s main objectives are maximum employment, stable prices, and moderate long-term interest rates.

2 percent is the target interest rate, so 7.9 percent over the past year is nearly quadruple that rate.

Interest rate increases will do nothing to achieve maximum employment, nothing to stabilize prices, and of course, nothing to achieve 2% interest rates.

The Fed currently is doing nothing to achieve its three goals. Quite the opposite. The Fed is doing the exact opposite of its stated goals by hoping to “cool” the economy (Fedspeak for recessing the economy).

In short, the Fed is applying leeches to cure anemia.

To fight the economic impacts of the COVID-19 pandemic, the Fed dropped rates to zero.

The Fed has been talking about rate hikes for months. Increases were expected even before Russia invaded Ukraine and impacted oil and raw material costs.

Economists expect up to seven incremental rate increases, beginning with a likely quarter-point raise (25 basis points), according to CNBC. Some economists have suggested the Fed may add 50 basis points on some of these increases.

Why seven increases? How did the Fed arrive at that number? No one knows.

Consumers have already been hit with high prices on goods like groceries, furnishings, clothing, airline fares, and especially high fuel prices.

IV. Other shortages. Lumber, housing, computer chips, shipping, cars, clothing, airline seats, etc. all are in short supply, and each scarcity could be moderated by well-directed federal spending.

Think of any scarcity, and you will have no trouble imagining how the federal government could help cure that scarcity via additional federal spending.

The federal government’s greatest skill is to throw money at a problem. It costs taxpayers nothing; it stimulates the economy; and when properly planned, can help solve the problem.

The proposed interest rate hikes will not increase the supply of oil or food. Nor will they increase the supply of housing, lumber, computer chips, cars, clothing, airline fares, furnishings, shipping, or labor, all of which are in short supply.

Additional deficit spending, not reductions in deficit spending, can reduce the shortages of scarce goods and services. Inflations always are caused by shortages.

Interest rate hikes will exacerbate those shortages, thus exacerbating inflation. The only possible “benefit” of rate increases (if one can call it a “benefit”) is that it will cut Gross Domestic Product and recess the economy.

A recession isn’t expected due to promising labor markets, but low-income workers will likely suffer.

And there we have it. The usual government response to any emergency is to punish the poor and middle-income classes. When deficits (wrongly) are deemed too high, the first instinct is to cut Social Security, cut medicare, and cut all poverty aids.

So far, it appears that a recession is unlikely in 2022, largely due to the fact that the labor market is strong.

Diane Swonk, the chief economist at Grant Thornton, told CNBC the employment market continues to improve.

However, the Fed must be cautious to avoid raising rates too quickly, which could slow down the economic recovery and lead to higher unemployment.

The labor market is “strong” (i.e., low unemployment) because people must work to pay their high bills. But the labor market is “weak” because there is a shortage of labor.

Raising interest rates will not reduce the shortages that cause inflation. Cutting federal spending only will recess an economy already weakened by scarcity and previous interest rate increases.

The government could end the inflation with more, not less, government spending to eliminate shortages and with lower, not higher, interest rates.

But the government, ruled by the rich, prefers to pretend that inflation must be cured at the expense of the poor and middle classes.

The Gap makes them rich, and the wider the Gap, the richer they are. Everything the Fed does is in service of a wider Gap.

At the start of this post, we told you that Congress and the President could prevent and cure inflations. But they pretend federal spending causesinflation.

For many in Congress, this is sheer ignorance. For others it is politics. Neither side wants the other side to succeed, and because Congress now is evenly divided, no one can overcome the minority rule system.

America’s founders created the minority rule system to entice the low-population states to join the union, so between the two-Senators-per-state voting system and the filibuster, a minority can prevent any progress unless one party has a super majority.

Add in House gerrymandering and the Presidential electoral college, and you have a creaky, arthritic government designed for obstruction, not for progress.

If all that were not bad enough, we are burdened with a Supreme Court that claims money is free speech and should not be limited, so money in politics has reached outrageous levels.

Finally, we also have a Supreme Court that now does not want agencies making decisions that offend the right wing, when in reality, agencies are the only ones capable of making decisions, thus tossing so many wrenches into the gears of progress, we are frozen.

In short, the Fed doesn’t have the tools, Congress doesn’t have the will, and the President doesn’t have the Congress or agencies.

Inflation will charge along with no one solving the scarcity problem until the private sector does it.

Capitalism, with its focus on profits and competition, eventually will reduce scarcities, at which time the Fed, Congress, the President, and both political parties will claim credit for “getting us out of this mess.”

The rich will prosper and the rest will suffer, and life will return to its normal domination by the rich.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps: Ten Steps To Prosperity: