When you are faced with an unwanted effect, the solution is to find and then solve the cause. If you don’t understand the cause, you will be faced with the same effect again and again.

Washington Post headline:

Inflation emerges as defining economic challenge of Biden presidency, with no obvious solution at handAmerica is emerging from the pandemic facing its biggest inflationary spike in decades, as startling and persistent price hikes threaten to undermine the recovery, while posing an entirely new kind of economic challenge to the Biden presidency.Policymakers are facing the devilish and unfamiliar quandary of booming consumer demand and dramatic supply disruptions combining to push higher the cost of necessities such as food, gas and housing.

I’m not sure why this is such a mystery. All inflations are caused by the same thing: Shortages of key goods and services.

The cure for any inflation is to increase the availability of the scarce goods and services. So when the Washington Post says, “no obvious solution at hand,” they may be talking about no obvious political solution.

This inflationary burst has no single cause and no obvious solution.

The cause is a shortage of key goods and services. The cause is notfederal deficit spending.

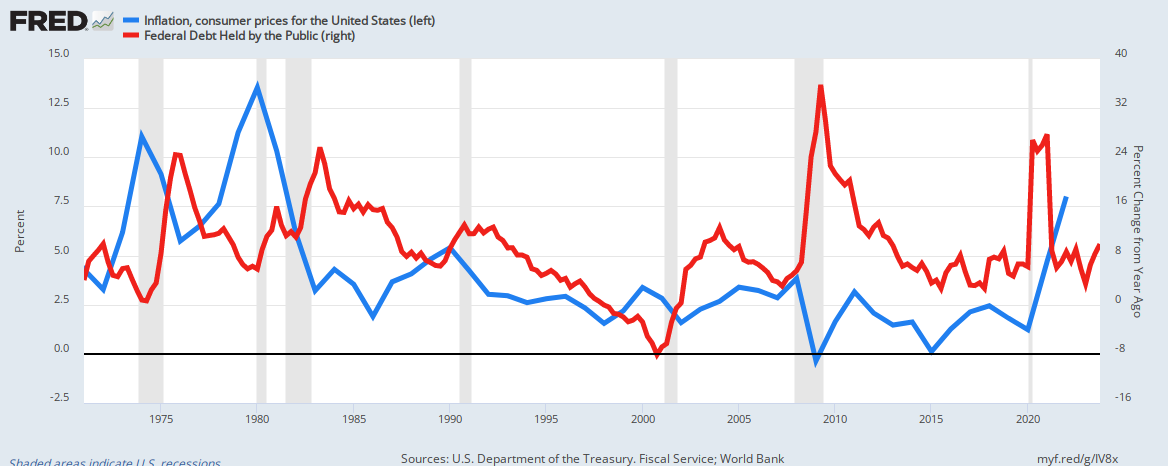

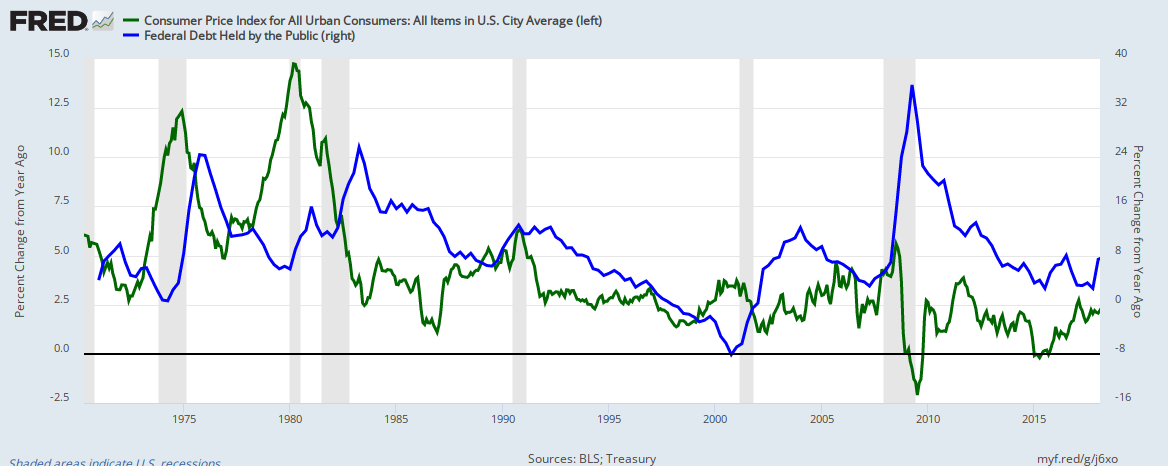

This graph shows there is no historical relationship between federal deficit spending (red) and inflation (blue). The graph also shows that reductions in deficit growth lead to recessions (vertical bars) which are cured by increases in deficit growth.

The economic solution is quite plain: Federal deficit spending to increase the supply of energy, food, computer chips, supply-chain methods, and labor.

Trillions of dollars in federal aid approved by Congress in response to the pandemic have led American consumers and companies to purchase more goods than ever before, putting new strains on global supply chains to accommodate the soaring volume. But that higher demand has collided with shortages in workers, supplies and transportation capacity — challenges caused in part by the pandemic as well as long-standing structural deficiencies in the national economy.

It is those shortages, not federal deficits, that have caused inflation. Cure the shortages and you cure the inflation.

A record 4.4 million Americans quit their jobs in September as labor market tumult continued.

The labor shortage exists partly because people quit their jobs for a variety of reasons including:

Need for child home care

Low wages

FICA cost

Bad hours.

Virus fear

There are others, but these all could be solved by federal deficit spending — a kind of “Manhattan Project” to cure the shortages that cause inflation.

Federal pay for child home care

Higher minimum wage together with the elimination of business taxes, to help fund the higher wages

Elimination of FICA and reduction of income taxes at the low pay scales

Standard 4-day week and/or shorter workday

Federal support for vaccination rewards in selected industries.

The federal government also should reduce the need for human labor by funding more development of Artificial Intelligence (AI) and mechanization along with other labor-saving initiatives.

This inflationary burst has no single cause and no obvious solution.

The single cause is shortages. The obvious solution is to cure the shortages.

Trillions of dollars in federal aid approved by Congress in response to the pandemic have led American consumers and companies to purchase more goods than ever before, putting new strains on global supply chains to accommodate the soaring volume. But that higher demand has collided with shortages in workers, supplies and transportation capacity — challenges caused in part by the pandemic as well as long-standing structural deficiencies in the national economy.

In the Eisenhower years, the federal government spent billions to improve highway traffic. Today, not only do highways need to be improved, but all other elements of the supply chain need similarly to be improved.

Our railroads are a mess. Our ports are inadequate. The quasi-privatized postal service is struggling. Shipping itself should be funded. These all are critical national needs, surely as important as weapons development.

Gas prices are at a seven-year high amid a global energy crisis, exacerbated by unusually high demand in Europe and a coal shortage in China.

Solutions: Temporarily fund increased oil drilling while funding more research and development of renewable, non-carbon fuels.

Food prices are rising at the highest level in 12 years amid severe droughts and spiking demand from families and restaurant reopenings. Meat, fish and egg prices are up nearly 12 percent from a year ago — the highest increase since 1979 (other than the early days of the pandemic) — partly fueled by processing plants’ struggle to find workers.

While other industries have mechanized, food processing remains in the electronic dark ages. Federal funding of computerization would help, significantly, as would federal financial support for raising wages.

Droughts are being caused by climate change, which has been denied by the right wing and largely ignored by the left. Federal support for non-carbon energy sources would help solve the problem.

The longer inflation lasts, the greater the political problem for the White House and congressional Democrats. Already news of the October inflation spike spurred new head winds for President Biden’s signature and key legislative initiative — the roughly $2 trillion Build Back Better package — exacerbating fears that other moderate Democrats may echo the concerns raised by Sen. Joe Manchin III (D-W.Va.) this past week about more spending. Congress won’t use their infinite supply of water to put out our economic fire.Meanwhile, Republicans have sharpened their attacks over inflation, seeing it as among their best arguments against the Biden’s presidency.

In other words, our boat is burning, but the politicians won’t put out the fire because they don’t want to use water.

Yet many economists say that the inflationary pressures hitting the U.S. economy were necessary to avoid the far worse scenario of a prolonged downturn and that focusing on rising prices risks obscuring the healthy facets of the current rebound such as the rapid rebound in jobs.Most families have more financial resources than they did before covid, especially among the bottom third. Even when accounting for inflation, disposable income has been roughly 9.5 percent higher in 2021 than it was before the coronavirus pandemic hit in 2019, according to Julia Coronado, president and founder of MacroPolicy Perspectives.“It’s safe to say the bottom 40 percent of Americans are definitely better off in the past year from a combination of rising wages and government aid, even with inflation,” said Arindrajit Dube, economics professor at the University of Massachusetts Amherst.

The Democrats are laughably (or “cryably”) bad at telling their story. Somehow, they expect the public to see “the obvious,” but history shows that the public would rather believe the words of a personality than the facts.

The U.S. economy is growing at a very fast clip, especially compared with the rest of the world, and could recover the lost economic output from the pandemic by the end of next year, according to some projections. Workers at the bottom of the income distribution are seeing meaningful wage increases, even factoring in inflation. Job openings are plentiful. The stock market has continued its meteoric rise under Biden, with the S&P 500 jumping by more than 20 percent since he took office. Inflation is up globally, not just in the United States, and the supply chain dysfunction reflects a decades-long trend of companies scattering their production sources across the globe.

All of the above is true, but who is telling the story? Certainly not Biden. And not the Vice President, whatever her name is and wherever she is hiding.

The old saw is, “If you’re defending you’re losing”, and the Dems aren’t even defending.

The approximately 50 percent rise in gasoline prices from last year — and 6 percent jump in October alone — has proved one of the most visible burdens on American families, spurred by a mixture of factors from Chinese manufacturing and an acute energy crisis in Europe.

To the average American voter, gas prices = inflation. The federal government has the financial ability to lower gas prices, although it may not have the political ability, unless someone in the government figures out how to tell the story.

Sadly, a personality like Donald Trump could do it, and he would do it, if it benefited him.

Supply chain backlogs also show little sign of easing before early 2023, said Phil Levy, chief economist at freight company Flexport. While shipping rates from Shanghai to Los Angeles came down modestly from their September peaks and auto companies report slightly easier access to semiconductors now, a record 81 container ships were sitting off the southern California coast on Tuesday, according to the Marine Exchange.

A “Manhattan Project” for America’s supply chain could fix the problem.

Rent prices also jumped 0.4 percent from September to October, continuing an upward trend, while the sales price of a single-family home jumped by 16 percent over one year, according to the National Association of Realtors.A red-hot housing market has been spurred on in part by low interest ratesand shortages in supplycaused by a freeze in construction during the pandemic.

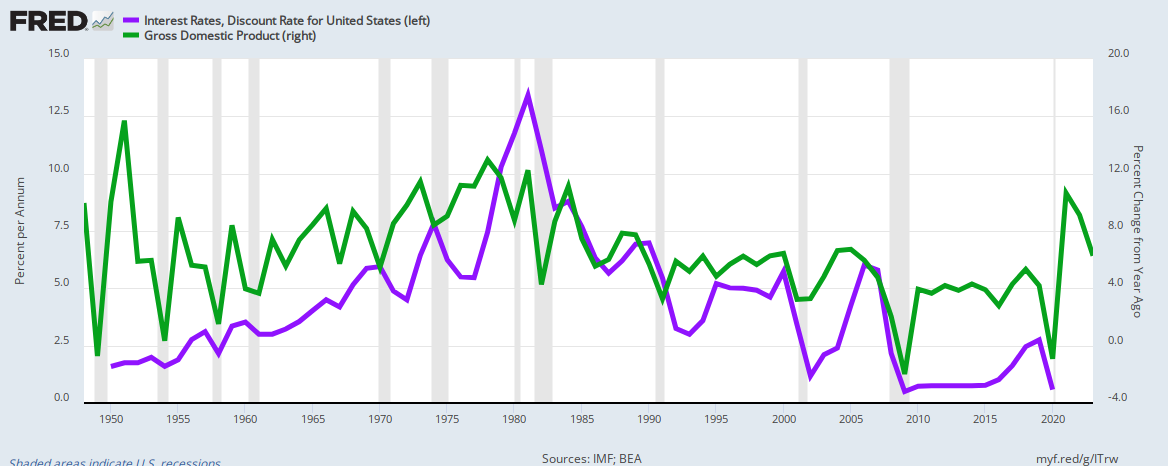

Annual interest rates (purple) vs. annual growth of Gross Domestic Product. Rate reductions do not stimulate GDP growth.

Shortages in supply always cause price increases.

However, as with so many myths in economics, the myth that low interest rates are stimulative has no basis. In fact, there is evidence, as you can see from the above graph, that high interest rates are stimulative.

The reason: High rates cause the federal government to pour more interest dollars into the economy.

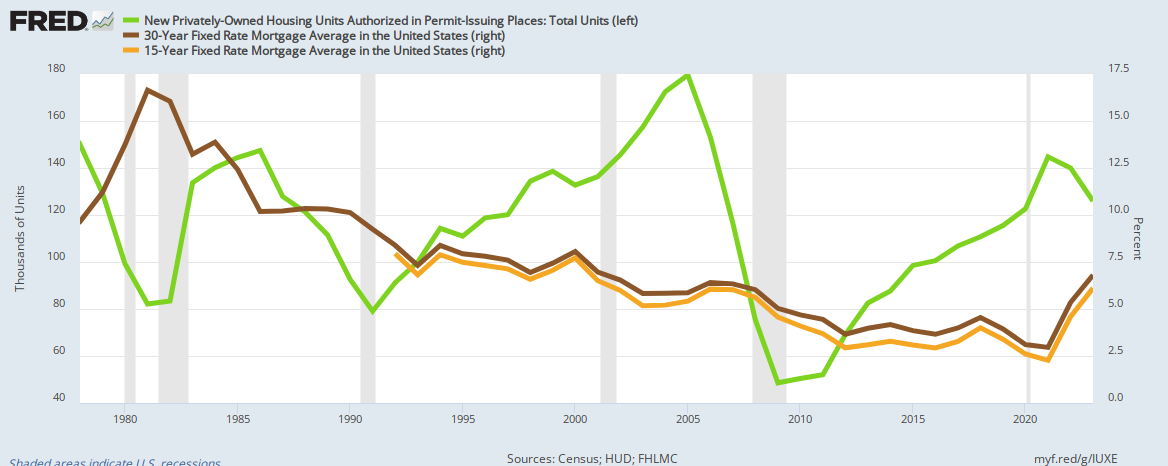

New housing construction (green) does not correlate with reductions in 30-year (brown) or 15-year (gold) mortgage rates.

New housing construction does not correlate with reduced mortgage rates. Both 30-year and 15-year mortgage rates have drifted downward since 1982, yet new housing construction (green) has changed wildly.

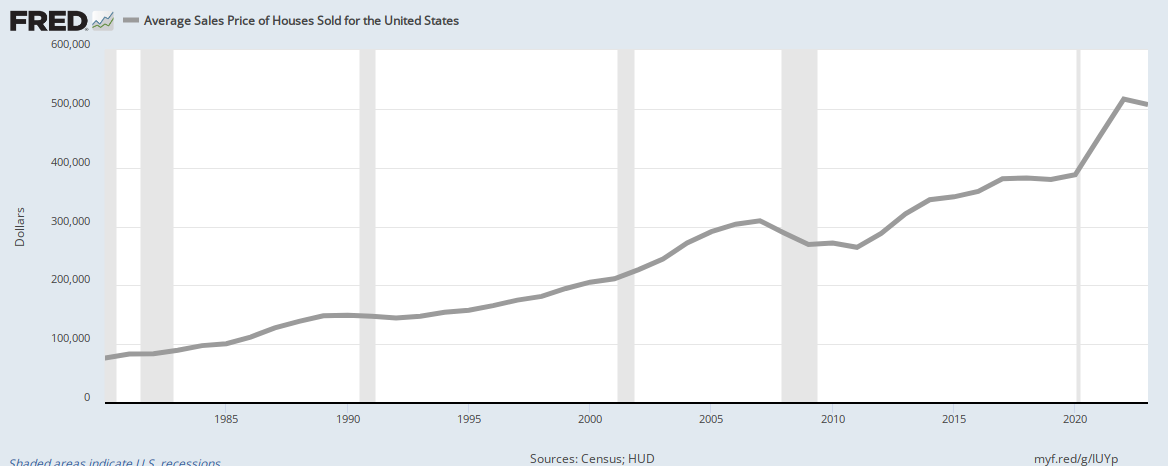

One reason for the lack of correlation may be that interest rates are not the deciding factor for home buyers.Since 1980, the average sales price of a house has increased from $80,000 to $450,000. A 1% drop in mortgage rates for a $450,000 house (less 20% down) comes to $3,600 per year or $300 per month, not nearly enough to encourage or discourage the purchase of a $450,000 house.

Thus, contrary to common knowledge and Federal Reserve dogma, reducing interest rates is not stimulative, and in fact, the argument could be made that rate reductions are recessive.

Interest rates should be raised and home construction, especially the construction of modestly priced homes, should be federally aided.

Raising interest rates also would mitigate against inflation, by increasing the value of the U.S. dollar.

If price increases continue, the Federal Reserve may raise interest rates, which would not only slow the pace of inflation, but also the pace of job and economic growth.

Yes and no. Yes, it would slow the pace of inflation, and no, it would not slow economic growth, as the above graphs indicate.

SUMMARY

The single greatest asset of the U.S. federal government is its Monetary Sovereignty. Yet myths and politics both have prevented the efficient use of this asset.

The federal government has the infinite ability to create U.S. dollars, and the addition of dollars is economically stimulative. Further, there is no evidence that federal deficit spending causes inflation, and massive evidence that it does not.

In short, there scarcely is an economic problem facing America that cannot be addressed by the wise addition of federal dollars, and there are no economic problems that can be solved by reductions in federal spending.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

To answer the title question, we begin with three questions:

What is the primary cause of inflation?

What is the primary cure for inflation?

What do high interest rates do to Gross Domestic Product?

If you ask the media, most economists, and the public to answer question #1, you probably will receive an answer something like the following:

Should we worry about inflation? The Week, March 3, 2018

“Until recently, inflation seemed to be dead or, at least, in a prolonged state of remission,” said Robert Samuelson at The Washington Post.

Thanks to cautious companies holding down wages and prices in the aftermath of the recession, annual inflation between 2010 and 2015 averaged just 1.5 percent, “often too small to be noticed.”

Apparently. Mr. Samuelson believes that prior to the “Great Recession,” companies were not cautious, and so were willing to pay employees more. But, having been frightened by the recession, they now refuse to pay employees more — and that has prevented inflation.

Utter nonsense. Caution has nothing to do with it.

Employers are buyers of talent. Like all buyers, employers try to pay as little as possible to obtain the employee quality they want. Isn’t that what you do when you buy anything?

Companies cannot “hold down” wages at will.

And as for prices, they are a reflection of each company’s market analysis. Companies try to set prices at levels that will provide the highest short- and long-term profits, volume, and share-of-market.

While Robert Samuelson wrongly seems to believe that business “caution” has prevented inflation, most people wrongly believe that federal deficit spending causes inflation.

The green line is inflation. The blue line is federal deficit spending.

Federal deficit spending does not parallel inflation.

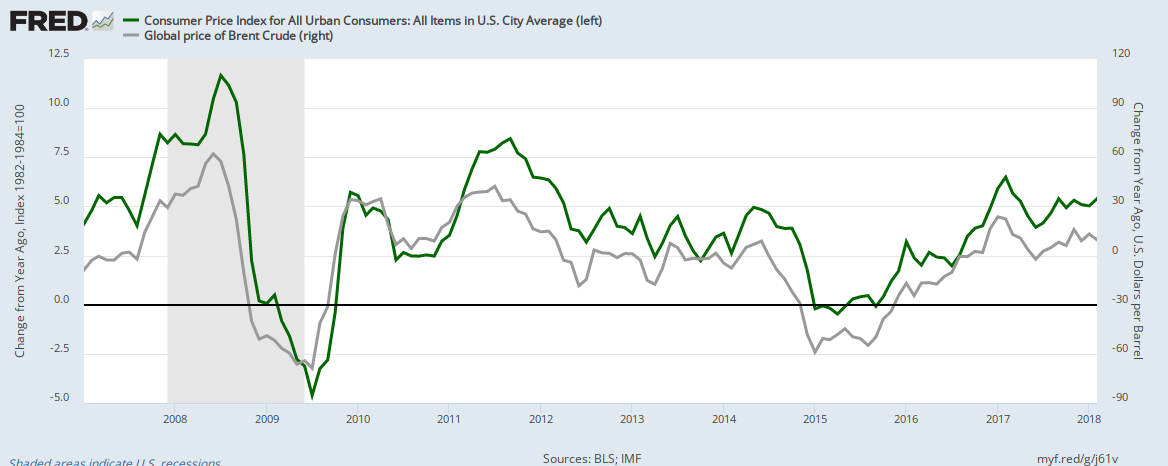

Inflation is a general increase in prices, and if there is one thing that generally increases (or decreases) prices it’s oil.

The green line is Inflation; the silver line is the price of Oil.

No other factor so closely parallels inflation as does oil — not food, not housing and certainly not wages:

The green line is Inflation; the violet line is Wages

Contrary to popular wisdom, wage increases do not parallel inflation increases.

In January, the Consumer Price Index, which tracks everything from the price of groceries to education costs, surged 0.5 percent; at that pace, annualized inflation would hit 6 percent by the end of the year.

It almost certainly won’t go that high, but it leaves newly installed Federal Reserve chairman Jerome Powell “facing a tricky task”: to contain inflation “without killing the economy.”

Traditionally, the Fed would respond by raising interest rates, said The Wall Street Journal in an editorial.

Yes, while inflation primarily is caused by rising oil prices, inflation is controlled by increasing the value of the dollar, which is accomplished by raising interest rates.

(Value of the dollar = Demand/Supply; Demand=Reward/Risk; Reward=Interest)

But the corporate tax cut and President Trump’s deregulatory agenda could rapidly accelerate economic growth.

That could further fuel inflation, prompting the Fed to raise rates faster than anticipated. In the worst-case scenario, this will severely roil markets and darken the economic outlook.

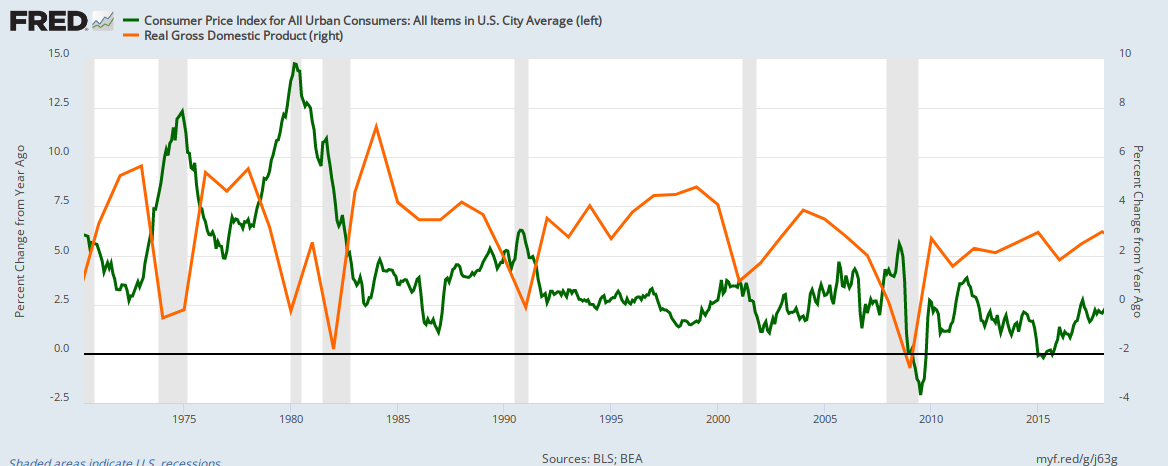

Contrary to popular wisdom, economic growth does not cause inflation:

The green line is inflation. The orange line is GDP growth.

GDP growth does not parallel inflation.

The Fed’s most potent tool in fighting downturns is cutting interest rates. “Total cuts of 5 to 6 percentage points have been the norm in recent recessions.”

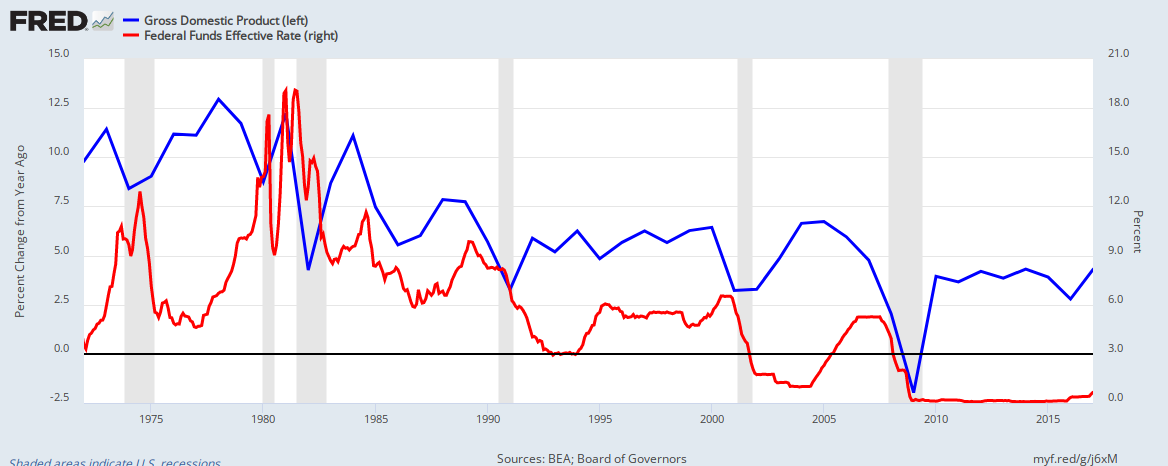

Wrong, again. Low interest rates do not stimulate economic growth:

The blue line is GDP growth. The red line is interest rates.

As interest rates fall, economic growth falls. There are several reasons for this, but the point is that low rates are not stimulative. In fact, by increasing the amount of interest money the government pumps into the economy, high rates can be stimulative.

Goldman Sachs expects the Fed to raise interest rates eight times over the next two years, largely to head off higher prices.

Each time the Fed raises rates, the stock market will respond negatively, only to rebound within a few days.

The negative response will be due to traders’ predictions that the market will respond negatively, not to any fundamental factors. It is a self-fulfilling prophecy.

Finally, we come to tax cuts. Although business tax cuts ostensibly help businesses grow, by cutting business costs, tax cuts actually help shareholders profit. The real, net effect of business tax cuts is to widen the gap between the rich and the rest.

BUSINESS The news at a glance Taxes: Firms spend tax windfall on buybacks The Week (US)

U.S corporations are spending most of their (tax cut) windfall not on higher wages or investment but on “buying their own shares,” said Matt Phillips in The New York Times. Over the past month, nearly 100 U.S. corporations have announced more than $178 billion in share buybacks—“the largest amount unveiled in a single quarter.”

Cisco is devoting $25 billion to buybacks; PepsiCo has announced $15 billion for shares; and Alphabet, home-improvement company Lowe’s, and chip equipment maker Applied Materials are each devoting between $5 billion and $9 billion.

“Such purchases reduce a company’s total number of outstanding shares, giving each remaining share a slightly bigger piece of the profit pie.”

“If the buyback frenzy continues, the administration is going to have some explaining to do,” said Jennifer Rubin in The Washington Post.

Part of the problem is that the Trump administration predicted that tax reform would boost U.S. household income by at least $4,000 a year.

Business tax cuts will stimulate the economy and will boost total household income, because tax cuts add dollars to (or remove fewer dollars from) the economy.

However, the benefits will go primarily to the upper-income groups.

In summary, contrary to popular opinion:

Inflation has not been related to federal deficit spending but rather to oil prices.

Wage increaseshave not been associated with inflation

Inflation and economic growth have not been related

Interest rate cuts have not stimulated economic growth, nor have interest rate increases slowed economic growth

While business tax cuts do stimulate overall economic growth, the benefit primarily goes to the upper-income groups, thereby widening the gap between the rich and the rest.

•All we have are partial solutions; the best we can do is try.

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money no matter how much it taxes its citizens.

•No nation can tax itself into prosperity, nor grow without money growth.

•Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

•A growing economy requires a growing supply of money (GDP = Federal Spending + Non-federal Spending + Net Exports). Federal deficit spending grows the supply of money

•The limit to federal deficit spending is an inflation that cannot be cured with interest rate control. The limit to non-federal deficit spending is the ability to borrow.

•Progressives think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.