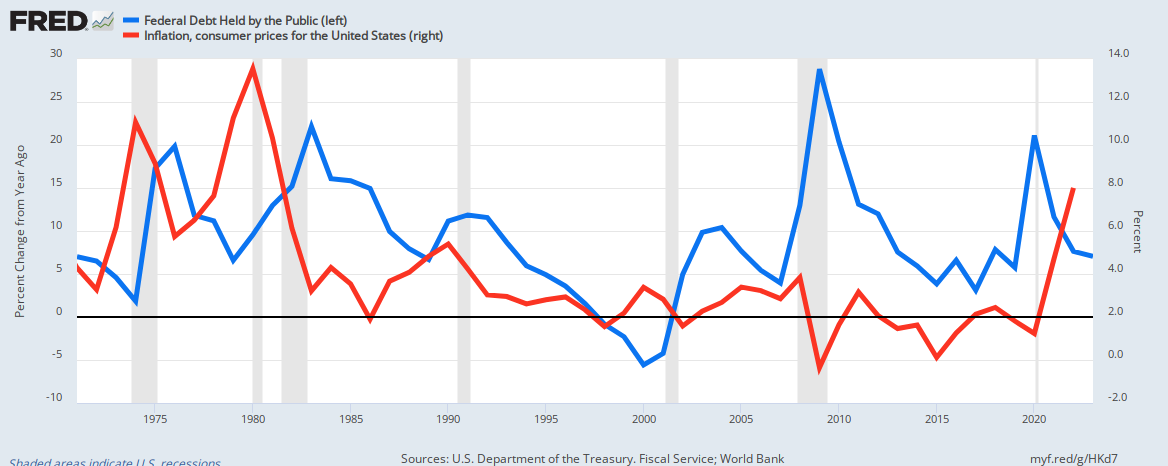

What Tuccille, the Libertarians, and the Wharton School seem not to understand is that federal deficits are absolutely necessary for economic growth. You have seen this graph many times: GRAPH I20 Years to Disaster “The United States has about 20 years for corrective action after which no amount of future tax increases or spending cuts could avoid the government defaulting on its debt.” J.D. TUCCILLE | 11.6.2023 7:00 AM

For decades, budgetary experts have warned that the U.S. federal government is backing itself—and the country—into a corner with expenditures that consistently exceed revenues, driving the national debt ever higher.

Every time the federal government “controls” (i.e. cuts) spending, we have recessions if we are lucky and depressions if we are not as fortunate:The latest red flag is raised by the University of Pennsylvania’s Penn Wharton Budget Model (PWBM), which says that the federal government has no more than 20 years to mend its ways. After this time, it will be too late to remedy the situation.

U.S. depressions come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Having learned nothing from history, Tucille, the Libertarians, and Wharton continue the same old ignorance about federal deficit spending: They equate personal finances with our Monetarily Sovereign government’s finances, not recognizing the massive differences between the two. While monetarily, non-sovereign entities like you and me need to run balanced budgets over the long term, or we’ll face bankruptcy, the federal government must never run a balanced budget and never will face bankruptcy.To say that the above is 100% bullshit would be to insult bullshit. Here’s why:20 Years to Control Spending

“Under current policy, the United States has about 20 years for corrective action after which no amount of future tax increases or spending cuts could avoid the government defaulting on its debt whether explicitly or implicitly (i.e., debt monetization producing significant inflation)” Jagadeesh Gokhale and Kent Smetters, authors of the October 6 Penn Wharton Budget Model brief, write in summarizing their findings.

“Unlike technical defaults where payments are merely delayed, this default would be much larger and reverberate across the U.S. and world economies.”

-

- The federal government, being Monetarily Sovereign, has the infinite ability to create its sovereign currency, the U.S. dollar. It has infinite dollars with which to pay its bills. It never needs to default.

- Despite concerns about “debt monetization” (aka “money printing’) causing inflation, this never has happened to any nation in world history. All inflations have been caused by shortages of crucial goods and services, most often oil and food.

- Many years of massive U.S. federal deficits didn’t cause today’s inflation. Only when COVID caused shortages of oil, food, computer parts, shipping, metals, lumber, labor, etc., did inflation arise. Now, the government’s massive spending to prevent and cure recession continues while inflation ebbs. The massive federal spending has helped cure the shortages and thus cure the inflation.

1. The historical fact that increasing government deficit spending increases economic activity (See Graph I, above) seems lost on the Wharton authors. Mathematically, GDP = Federal Spending + Nonfederal Spending + Net Exports 2. There is no historical example of “crowding out of capital formation.” In fact, the federal money added to the economy increases the funds available to the private sector for capital formation. 3. Future tax increases are not necessary because federal taxes do not fund federal spending:The reason for worrying about accumulating deficits and the resulting growing debt, the authors explain, is that “government debt reduces economic activity by crowding out private capital formation and by requiring future tax increases or spending cuts to accommodate future interest payments.”

A. All federal tax dollars are destroyed upon receipt by the U.S. Treasury. The tax dollars come from the M2 money supply measure, but when they reach the Treasury, they become part of no money supply measure. The reason: The Treasury’s money supply, being infinite, cannot be measured.

B. Even if the federal government collected zero tax dollars, it could continue spending forever. It has the infinite ability to create spending dollars.

C. The purposes of federal taxes are not to fund federal spending but rather:

a. To control the economy by taxing what the government wishes to discourage and giving tax breaks to what the government wishes to reward.

b. To assure demand for and acceptance of the U.S. dollar by requiring taxes to be paid in dollars.

c. To fool the public (and presumably Wharton economists) into believing federal benefits require federal taxes. (This last purpose is promulgated by the rich to discourage the populace from demanding benefits that would narrow the Gap between the rich and the rest.)

This is the oft-claimed “ticking time bomb” that never seems to explode. There never has been and never will be a time when the federal debt “gets too big” to be paid. Again, the Wharton economists demonstrate they don’t understand the differences between a Monetarily Sovereign government and a monetarily non-sovereign government.If debt gets too big, lenders can’t be paid back, credibility is shot, the dollar loses value, and the economy tanks.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. Scott Pelley: Is that tax money that the Fed is spending? Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Strange how history says exactly the opposite. Following many years of massive federal spending, unemployment was at historical lows. The reason: Federal spending stimulated GDP growth, which required more labor.“It would be an unfettered economic catastrophe,” economists Joseph Brusuelas and Tuan Nguyen predicted earlier this year of such a scenario. “Our model indicates that unemployment would surge above 12% in the first six months, the economy would contract by more than 10%, triggering a deep and lasting recession, and inflation would soar toward 11% over the next year.”

History shows that balancing the federal books creates recessions and depressions. The so-called “debt burden” is not debt, and it’s not a burden. It’s deposits into Treasury security bills, notes, and bond accounts which are owned by the depositors. It’s not debt because the government never touches the dollars in those accounts. The government creates dollars at will. It has no need to borrow dollars, and indeed, the U.S. federal government never borrows dollars. To “pay off” the debt (that isn’t debt), the government merely returns the dollars in the accounts to their owners. This is no burden at all. The purpose of T-securities is not to provide spending money to the government but rather to give the world with a safe, interest-paying place to store unused dollars. This makes the dollar an attractive international medium of exchange.So long as investors believe federal officials will eventually balance their books, you have a grace period as debt grows—that is until the debt burden is so enormous that it crushes economic activity.

As we have demonstrated numerous times, the Debt/GDP ratio is meaningless. It tells nothing about the current or future health of an economy. It predicts nothing; it evaluates nothing. It is 100% meaningless. That is why economists who don’t understand the fundamentals of Monetary Sovereignty love to quote it.“Even with the most favorable of assumptions for the United States, PWBM estimates that a maximum debt-GDP ratio of 200 percent can be sustained,” the authors add. “This 200 percent value is computed as an outer bound using various favorable assumptions: a more plausible value is closer to 175 percent, and, even then, it assumes that financial markets believe that the government will eventually implement an efficient closure rule.” (That’s a mix of tax and spending changes to curtail deficits and debt.)

We suspect financial markets understand history better than the economists at Wharton. We suspect they know that when the federal government spends more, stock prices rise.The 20-year countdown assumes that investors remain optimistic about the willingness and ability of U.S. officials to bring spending in-line with tax revenues. “Once financial markets believe otherwise, financial markets can unravel at smaller debt-GDP ratios,” according to the PWBM analysis.

As PWBM points out, “Financial markets demand a higher interest rate to purchase government debt as the supply of that debt increases… Forward-looking financial markets should demand an even higher return if they see debt increasing well into the future. Those higher borrowing rates, in turn, make debt grow even faster.”

Again, the Wharton experts misunderstand Monetary Sovereignty and the realities of federal financing. The federal government does not finance spending by borrowing (“issuing debt.”) It finances spending by creating dollars, ad hoc. It can allow as much or as little in T-security deposits as it wishes. If the public fails to invest as much as the Federal Reserve wishes (to stabilize the dollar), the Fed merely uses its infinite money creation ability to fill the gap. Federal spending never is constrained by the public’s desire to own T-securities. As for interest rates, the Fed sets them not to attract depositors but to control inflation. If the Fed smells inflation, it raises rates. If the inflation scare passes, the Fed lowers rates. This has nothing to do with any need for deposits into T-security accounts. (Sadly, raising interest rates, far from moderating inflation, exacerbates it by raising prices. The only thing that moderates inflation is federal spending to ease shortages of critical goods and services.)That’s already happening.

Increasing Costs and a Looming Deadline “To finance trillions of dollars in spending beyond what incoming revenue can support, the US Treasury is now issuing more debt in the form of Treasury securities than global financial markets can readily absorb,” Yahoo! Finance’s Rick Newman wrote on October 30.

“That forces the borrower—the US government—to pay higher interest rates, which in turn pushes up borrowing costs for consumers and businesses in much of the Western world.”

The notion of a “magic, unsustainable debt-to-GDP ratio” is utter nonsense. Japan already has exceeded that meaningless ratio.Just when the U.S. federal government hits that magic unsustainable debt-to-GDP ratio of between 175 and 200 percent depends on investor confidence and how much the markets charge to finance more borrowing. PWBM estimates it will happen between 2040 and 2045—if we’re lucky.

The 2001 Clinton surplus caused the 2001 recession. See Graph I.The U.S. Treasury concedes that “since 2001, the federal government’s budget has run a deficit each year. Starting in 2016, increases in spending on Social Security, health care, and interest on federal debt have outpaced the growth of federal revenue.”

Increasing taxes on high incomes would help narrow the Gap between the rich and the rest, which would be a good thing. It would do nothing to improve the federal government’s already infinite ability to pay its creditors. “Reforms” to Social Security and Medicare (i.e. cuts to benefits paid to those who need them most, while increasing taxes on those who can afford them least) also would do nothing to improve the federal government’s bill-paying ability. The “mix of tax increases and spending cuts” would take spending dollars from the private sector and cause a recession or depression. Remember this equation: GDP = Federal + Nonfederal Spending + Net Exports. Spending cuts and tax increases would decrease Federal + Nonfederal Spending, which would reduce GDP, i.e. cause a recession or depression. Simple mathematics.Options for Fixing the Mess In September, PWBM explored three policy options to render fiscal policy less disastrous: increasing taxes on high incomes, reforms to Social Security and Medicare that reduce payouts and increase taxes, and a mix of tax increases and spending cuts.

Hmmm. Giving the economy fewer Social Security and Medicare dollars and taking dollars from the economy by increasing taxes would “allow the greatest economic growth”???? Also, pouring water out of a bucket fills it??The authors predict entitlement reforms and a mix of tax increases and spending cuts would both stabilize the debt-to-GDP ratio, with entitlement reform allowing the greatest economic growth.

The above is so staggeringly ignorant one scarcely can believe it was written by humans. Indeed, it must have been written by an Artificial Intelligence gone rogue. Cuts to federal spending and tax increases do the same: They take dollars out of the economy and cause recessions and depressions. The Libertarian (aka anarchist) comments are not surprising. Anti-government ignorance is expected from them. But, if this is the best to come out of Wharton, heaven help its students. Rodger Malcolm Mitchell Monetary Sovereignty Twitter: @rodgermitchell Search #monetarysovereignty Facebook: Rodger Malcolm MitchellThe St. Louis Federal Reserve Bank has tax revenues hitting 19 percent of GDP last year—the highest share in two decades. The IRS may scream about a “tax gap” between what is owed and what it collects, and lawmakers may supercharge the tax agency with funds, but fixing the federal government’s spendthrift ways by squeezing taxpayers won’t just be unpopular—it’s a scheme that defies historical trends.

Spending cuts and entitlement reforms will also elicit resistance. But at least they’re within reach of lawmakers who could spend no more than they collect—or even to run surpluses to pay down debt.

Twenty years to fix the federal budget should be plenty of time. But brace yourself. The record so far suggests it won’t be enough.

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

:max_bytes(150000):strip_icc():format(webp)/will-the-u-s-debt-ever-be-paid-off-3970473-finalv2-acb523b4dacf43529f4915254c600777-64dc8c15fa3345438ef293f439a58046.jpg) She begins with “Cut government spending” and “raise taxes,” i.e., reduce deficit growth — precisely what we see causes recessions.

Then she adds, “Drive economic growth at a faster rate,” but does not say how to do that when government spending falls and taxes rise.

Finally, she says, “Shift spending to areas that create the most jobs.”

Again, she doesn’t explain how that would be done with less spending and higher taxes, but spending in areas that have more jobs may not be efficient, economically.

She begins with “Cut government spending” and “raise taxes,” i.e., reduce deficit growth — precisely what we see causes recessions.

Then she adds, “Drive economic growth at a faster rate,” but does not say how to do that when government spending falls and taxes rise.

Finally, she says, “Shift spending to areas that create the most jobs.”

Again, she doesn’t explain how that would be done with less spending and higher taxes, but spending in areas that have more jobs may not be efficient, economically.