Are you in one of these positions? You want to ask for a raise, but you fear you could get fired. Or, you would like to change jobs or quit working altogether.

But you are held captive by your health care insurance. Your company pays some of the premiums, and you can’t afford to pay the total amount yourself.

Or you have a pre-existing condition and will not be able to find another policy. It’s about to get even worse for you and for your company:

Higher premiums are coming. Much higher Data: Kaiser Family Foundation

It cost an average of $22,463 to cover a family through employer-sponsored health insurance in 2022, according to an annual benefits survey from the Kaiser Family Foundation.

Though your employer may seem to pay the $22,463, you actually pay it. Your employer figures those dollars as part of your employment cost and your salary, sick days, vacation days, lunchroom, and any other perks you receive.

If there were no healthcare costs, your employer could raise your salary by that average of $22,463. Instead of paying it to you, he pays it to the health care insurance company.

Why it matters: Nearly 159 million Americans get health coverage through work, and coverage costs and benefits have become a critical factor in a tight labor market.

While families and individuals paid similar amounts for coverage in 2022 and 2021, premiums have increased by 20% over the past five years, KFF said.

And because many premiums for 2022 were finalized in the fall of 2021, before the effects of inflation were clear, KFF expects a higher increase in average premiums for 2023 than what’s been observed in recent years.

A single person paid $7,911 on premiums in a year for their employer health plan in 2022.

Again, while it may seem that you only paid “only” $7,911, you actually paid the full premium in lost wages — wages you should have received, but didn’t.

Between the lines: Employers are making tough choices in a competitive labor market and in some instances, absorbing rising costs of coverage instead of passing them on to workers.

An October survey of 1,200 small businesses found that nearly half of them have increased the cost of their goods or services to offset the rising costs of health care. Four in 10 businesses surveyed stopped offering health insurance altogether.

Angry about inflation? Much of the blame goes to the ballooning cost of health care. You pay inflated costs directly via premiums and insurance deductibles, and indirectly via the lost wages your employer would have paid you.

You also pay the inflated costs of the goods and services you purchase from companies that have had to raise their prices to cover increased insurance costs.

In short, employer-supplied health care insurance is a net loser for everyone except for the insurance companies.

It cuts your salary while increasing what you pay for goods and services.

The cost of care is expected to continue to increase in the coming years, putting added pressure on employers to offer competitive benefits packages.

Employer-sponsored plans have seen increased demand for mental health services, and 44% of companies surveyed with 200 or more employees offered mental health or self-care apps as benefits, accompanying research in Health Affairs says.

Covered workers are picking up a portion of the cost when they visit in-network physicians: Average copayments were $27 for primary care and $44 for specialty care, and there was even more cost-sharing for hospital admissions or outpatient procedures.

A large majority of firms with 50 or more employees cover some telemedicine in their largest health plan. What’s next: Premiums are likely to surge next year as inflation persists.

“Premium increases may be even higher than the 3–4 percentage points that we have seen in recent years,” the Health Affairs study authors write.

It’s the classic vicious circle. The cost of health care goes up which directly increases inflation, Then, inflation pushes the cost of insurance up, which impacts your net salary. And ’round and ’round we go.

Your net take-home pay is numerically reduced by the insurance premiums, while it is functionally reduced by inflation.

Employer-provided health care insurance costs you both ways.

THE SOLUTION The U.S. federal government has infinite dollars. It neither needs nor uses tax dollars to pay its bills. Even if all federal tax collections totaled $0, the government could continue spending any amount, forever.

In fact, all federal tax dollars are destroyed upon receipt.

Without collecting a penny in taxes, the federal government could provide you and your family with free, comprehensive, no-limit health care insurance, that includes everything you can imagine — eyes, dental, psychiatric, every form of health-related equipment, etc.

Your healthcare could cost you nothing, either for services or for premiums. It could be Medicare for All only much, much better. And it wouldn’t increase the cost of goods and services, because, unlike employer-provided insurance, it wouldn’t increase employers’ costs.

Unlike employer-funded medical insurance, which does nothing for the economy, federally funded Medicare for All would grow the economy by adding stimulus dollars.

SO WHY NOT? Why don’t you have this plan, already?

Because you have been led to believe three lies.

Lie #1. You shouldn’t trust the government to provide health care.

But, a comprehensive Medicare for All plan would not involve the government providing health care. The plan would involve the government only paying for health care.

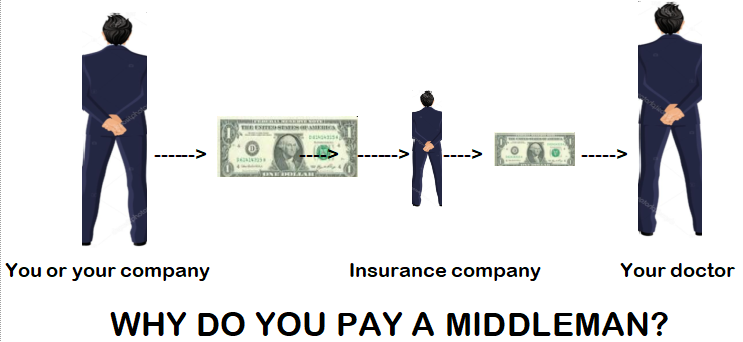

The actual care still would be provided by your same doctors, nurses, hospitals, therapists, and equipment manufacturers. It merely would cut out the wholly unnecessary and costly middlemen, the insurance companies.

The insurance companies provide no medical function. They merely collect your dollars, take some for themselves, and pass the rest on to the real medical practitioners.

The government would function as your insurance company. The big differences would be no dollars would be taken from you, and the government never can run short of dollars.

Lie #2. Your taxes would go up.

The U.S. federal government, unlike state and local governments, is Monetarily Sovereign. It cannot unintentionally run short of U.S. dollars.

It can spend forever without collecting any tax dollars.

Compare the federal government to state and local governments. They are monetarily non-sovereign. While state and local taxes fund state and local spending, federal taxes do not fund federal spending.

The purpose of federal taxes is not to help the government spend, but rather:

a. To control the economy by taxing what the government wishes to reduce and giving tax breaks to what the government wishes to reward.

b. To create demand for the U.S. dollar by requiring taxes to be paid in dollars.

c. To reduce your demand for services (like free health care insurance), by making you believe taxes are necessary to pay for benefits.

Lie #3. Federal spending causes inflation.

No inflation ever has been caused by spending. All inflations, including the current one, are caused by shortages of key goods and services, most often oil and food.

During and after the Great Recession of 2008, we had massive government spending without inflation. We only experienced inflation when COVID caused shortages of oil, food, lumber, computer chips, shipping, labor and other products and services.

If you understood that the federal government has infinite money and does not need or use taxes, you would demand Medicare for All, Social Security for All, College for All, Food Assistance for All, Housing Assistance for All, etc.

Why don’t we have it?

The very rich, who run America, don’t want it. They are rich because of the income/wealth/power Gap between them and you. The wider the Gap, the richer they are. But the more free benefits you receive, the narrower the Gap becomes.

Your free benefits actually make the rich less rich.

So the rich bribe the politicians (via campaign contributions and promises of employment), the media (via advertising dollars and media ownership), and the economists (via donations to schools and employment in think tanks).

The rich bribe these people to tell you “the Big Lie” that federal taxes fund federal spending, and if you want more benefits you’ll have to pay for them.

It’s all a con to keep you ignorant. An ignorant public is a docile public, which is exactly what the rich want. It keeps them rich.

Sen. Bernie Sanders recommended a Medicare for All plan, but his plan had three serious faults:

Fault #1. It claimed to rely on tax collections, the same fault current Medicare has. So Sanders struggled to show how it was tax-neutral.

That was unnecessary. He should have explained that federal taxes do not fund federal spending and that the federal government would do what it always does: Create dollars, ad hoc, to pay every bill.

Fault #2. It was not comprehensive. It still required co-pays and didn’t cover many medical problems. This was done to save money and balance against tax collections — an unnecessary step.

The federal government does not need to save dollars. It has infinite dollars. It never can run short of dollars, even if it collects zero taxes.

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Former Federal Reserve Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

The scare stories about federal “debt” and deficits are just that: Scare stories. False scare stories.

So called federal “debt” and deficits are no burden on a government with the infinite ability to pay its bills. If the federal government and your political representatives were doing their job, you would have free, comprehensive Medicare for All right now.

Why do you pay a middleman when the government can provide better service, free?

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

Saw on the news the Mississippi river is drying up. Cargo barges stalled in shallow water. Prices are expected to rise even higher than expected. The rich must really be happy with that news. The worse everything gets, the better off they are…up to a point; but then they have to hope and pray the whole mess will conclude in their favor, allowing them to emerge unscathed. If not, monetary soveriegnty to the rescue! Then they eat crow and forever after will be forced into humble silence while the work of the world goes on.

LikeLike

Indeed, the concept of employer-sponsored health insurance is really quite bizarre when you think about it. It first came into being via an accident of history following WWII, and remains propped up by a tax code that favors it. And it is an obsolete form of serfdom that really belongs on the trash heap of history.

Medicare For All will take it off the bargaining table for good, giving workers far more bargaining power as a result. Businesses will benefit from far lower costs of doing business. And the entire economy and society will benefit as well. A win-win-win for everyone but the oligarchs, basically.

So what are we waiting for?

LikeLike