Let me begin at the end, with a summary: “Inflation,” or “price inflation” as some prefer to call it, never is the traditional “too much money chasing too few goods.” It always is “too few goods (and services).” Never, “too much money.”

Inflation always is caused by shortages of key goods and services, most often, energy, food, and/or labor.

I’ll explain by quoting from the following article:

High Inflation Is Here To StayBut the people in power won’t even say as much, let alone do something about it.BRUCE YANDLENews that the September Consumer Price Index (CPI) rose by 5.4 percent on a year-over-year basis should be evidence enough for Federal Reserve Chair Jerome Powell, White House economists, and even the president to admit that we have more than a temporary inflation uptick on our hands. Better yet, it’s proof that we should avoid adding fuel to the fire, even if it means cutting back on President Joe Biden’s multi-trillion-dollar American Rescue Plan.

“Fuel to the fire” means federal deficit spending. Mr. Yandle wrongly believes federal deficits lead to inflation. So let us address that myth directly.

If the myth were true, an increase in federal deficit spending should correspond to an increase in prices. But does it?

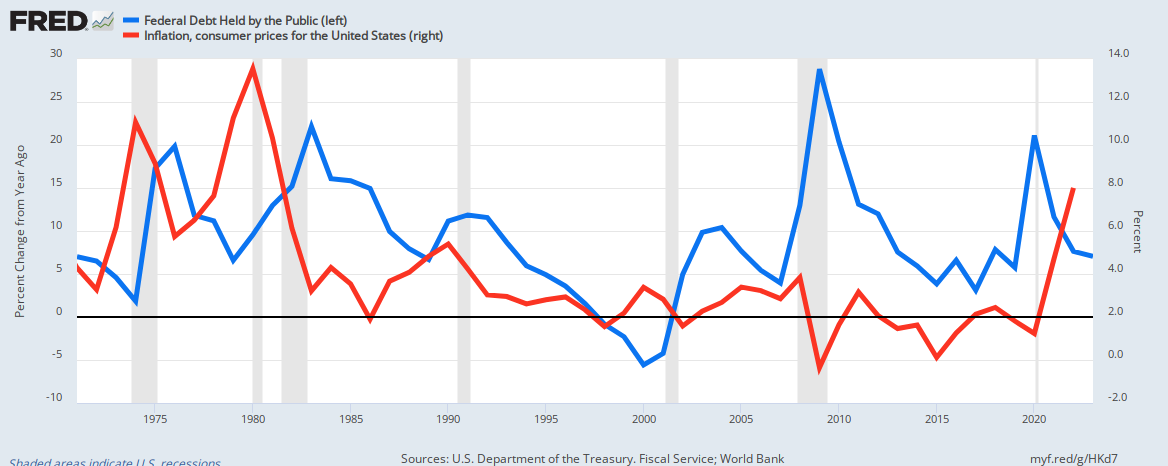

There is no relationship between inflation (red line) and changes in federal deficit spending (blue line).

We see absolutely no evidence that deficit spending has led to today’s, or any day’s, inflation. Sadly, the myth is taken for granted as truth, and seldom do we see anyone daring to doubt it.

Until recently, evidence of inflation exceeding 2 percent—the Fed’s traditional goal for inflation—has been dismissed as temporary or transitory, and for good reason. Newly printed stimulus money has been passing through the system. This, accompanied by serious supply-chain disruptions, might be over in another 12 months—if we’re lucky.

Ah, “supply-chain disruptions,” (aka shortages). Here, too briefly, Mr. Yandle hints at the fact that shortages are primary cause of inflation.

Does that give Mr. Yandle a clue? Apparently not:

Then in August, the Biden administration indicated that 2021’s economy would show as much as 4.8 percent inflation—but, with an optimistic spin, would fall to 2.5 percent the next year. Meanwhile, there is some stimulus money pending in the yet-to-be determined infrastructure bill, and that complicates the issue.Avoiding the hard truth or waiting before countering inflationary forces carries a cost. In this case, delays could mean harsher action later when, for example, the Fed hits the money brakes harder to cool the economy. In such a case we might see interest rates head to the ceiling, construction activity and high-tech investment plummet, and the economy roll into a recession.

Mr. Yandle, staying with the false “spending causes inflation” trope, is not clear about what he means by “money brakes.”

If he thinks that raising interest rates would lead to recession, you would expect there to be an inverse relationship between interest levels and Gross Domestic Product growth.

Is there?

There is not the expected inverse relationship between interest rates (brown) and GDP growth (green).

The above graph does not indicate Mr. Yandle’s expected inverse relationship between interest rates and GDP growth. In fact, we see something of a positive relationship.

Contrary to the knee-jerk, temporary reaction of the stock markets, high interest rates seem to correspond with high GDP growth.

Why? Probably because higher rates force the federal government to pump more interest (i.e. growth) dollars into the economy.

If by, “hit the money brakes,” Mr. Yandle means add fewer dollars to the economy, he undoubtedly is correct. Economic growth, by formula, requires money growth.

GDP = Federal Spending+ Non-federal Spending + Net Exports

Clearly, GDP growth relies on spending growth, and one seldom will see spending growth without money growth.

In 1978, the CPI was exceeding 7.5 percent and economic growth was slowing because of deliberate Fed action to cool the economy.

“Cool the economy” surely is not anyone’s goal, if “cooling” means reduced economic growth. But Mr. Yandle, and other economists love to use ambiguous terminology, to protect themselves from error.

Increasing interest rates does not “cool” an economy, but reducing federal deficits does “cool” economic growth.

Fed chair Paul Volcker “hit the brakes” long and hard and squeezed out inflation, along with employment growth.

Although rising interest rates didn’t cut into GDP, there is a very close relationship between the money supply (approximated by total debt) and GDP growth.

Again, Yandle, intentionally or unintentionally uses imprecise terms. In what way did Volker “hit the brakes”? We assume Yandle means “raised interest rates.”

If so, that clearly does not hit any economic brakes, nor ever has. Higher interest rates do not cause recessions.

But increases in money supply do cause increased GDP growth.

No one in authority wants to admit that the dollars we hold are systematically losing their purchasing power.

“No one”? Actually, everyoneunderstands and says we are in an inflation. The only questions being, Why?”“How deep?” and “How long?”

The “why” is shortages. The “how deep” and “how long” depend on what the government does. If it spends to reduce shortages, the inflation will not be deep or long. If it does as Mr. Yandle wants — cuts spending — we probably will fall into a stagflation.

We are being quietly robbed by Washington’s dollar-printing press, with politicians calling the shots. The presses are not operating without drivers.

Wrong, wrong, wrong. As we have shown in the first graph (above), the “dollar-printing press” does not cause inflation.

Seemingly, it’s okay for the Fed chair to recognize CPI heading north, but only if he qualifies the trip by calling it temporary. And while Washington analysts argue that COVID-19 disruptions are affecting just some key items, such as used cars and lumber—

“Just some key items”? Really? How about, virtually all items and labor? How about oil, food, electronics, rare earths, etc., etc.

— and that ports clogged with container ships waiting for workers, drivers, and trucks to be unloaded are the culprit—an analysis of the price movements in the July Consumer Spending Index, which is the Fed’s preferred inflation measuring rod, shows 84 percent of included items rising.

That’s right. Clogged ports and a shortage of workers and drivers, also leads to the product shortages that are the causes of inflation. Amazing that Mr. Yandle doesn’t see it.

The price increases are widespread, which suggests they are embedded.

“Embedded” into shortages.

What Mr. Yandle doesn’t recognize is that increased federal spending can cure inflationby curing shortages.

No matter how analysts choose to slice and dice the data, the answer is the same: The U.S. inflation rate calls for taking offsetting actions, such as avoiding direct distributions of stimulus or minimum family income dollars (though not harsh, invasive measures to cool off the economy).

The perfect right-wing solution to everything: Cut family income.

Let us not forget that inflation is not about rising prices. The rising price level is the result of an inflated money supply—all those trillions of stimulus dollars now out and chasing harder after goods and services.

Exactly and diametrically wrong. Inflation IS about rising prices and IS NOT about money supply. Despite all the counter-evidence, Mr. Yandle promulgates the “deficits cause inflation” myth.

Why does he avoid fact in favor of fiction? Here’s a hint:

BRUCE YANDLE is a distinguished adjunct fellow with the Mercatus Center at George Mason University.Wikipedia: The Mercatus Center at George Mason University is a libertarian, non-profit, free-market-oriented research, education, and outreach think tank. The Koch family has been a major financial supporter of the organization since the mid-1980s. Charles Koch serves on the group’s board of directors.

And there you have it. Yandle is a Libertarian being paid by a think tank that is supported (bribed) by the infamous and wealthy Kochs. Their goal in life seems to be to widen the Gap between the rich and the rest.

Widening the Gap is how the rich become richer. (Without the Gap no one would be rich. We all would be the same.) The rich widen the Gap, i.e. become richer, by gaining more for themselves or by forcing the rest to have less.

By blaming federal deficits for inflation, Yandle, Mercatus, and the Kochs are able to demand the next “logical” step, cut deficit spending on such social programs as: Social Security, Medicare, and all poverty aids.

Along with the military, those constitute the largest federal deficit expenditures.

Libertarians and Republicans falsely claim that deficit spending should be cut to cure inflation. They are deceptive and wrong.

The rich widen the Gap by bribing thought leaders:

Economists are bribed via “think tank” salaries and payments to universities

The Media are bribed via ownership and advertising dollars

Politicians are bribed via political contributions and promises of lucrative employment later

Libertarians and Republicans wrongfully claim that deficit spending should be cut to cure inflation.

But, cuts to federal deficit spending do not cure inflation. Rather, spendingcuts cause recessions and depressions, while punishing the poor and middle classes.

Yandle’s suggested cuts simply would make the rich richer and the rest, poorer. In short, Yandle’s cuts would widen the Gap between the rich and the rest, and we believe that is what he is paid to want.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

7 thoughts on “Libertarians and Republicans sell the inflation myth to widen the Gap between the rich and the rest.”

Some thoughts:

So, who got a Ph.d for proving that spending and inflation are related, when, in view of your graphs, they aren’t? Where did that come from? Or that high interest rates will “cool” GDP growth when, as you state, higher interest rates mean pumping in more federal money; therefore a stimulus, not a cooling.

Fear and professional rejection controls those three groups–politics, media and teaching. Monetary Sovereignty will no doubt rob the .1% of their “ace in the hole.” It’s no wonder Monetary Sovereignty is practically unheard of.

As I’ve written in the past, even our friends get it wrong. I just dropped this note to my occasional pen pal, Stephanie Kelton, whose recent book was right about “the Big Lie,” but unfortunately included the “spending / inflation” misunderstanding.

————————————————————————————–

Hi Stephanie,

I hope all is well for you.

Some thoughts:

The current economic atmosphere provides a perfect learning experience for MMT. The Big Lie (“Federal taxes fund federal spending”) hasn’t changed, but some things have:

1. The JG (Jobs Guarantee) has become more obviously wrong. Workers are demonstrating that they won’t accept the jobs a JG would by necessity offer. It’s time to get off that horse.

2. The fact that inflation did not earlier occur with federal deficit spending, but rather now, with shortages, demonstrates again that the old trope, “Inflation is too much money chasing too few goods” is wrong.

The new trope is: “Inflation is too few goods and services”. Period.

Every inflation in history has been caused by scarcities. The scarcities usually are food, energy, and labor (although today’s scarcity of computer chips has entered the mix).

The cure for today’s inflation will require more federal spending to acquire the scarce goods and services.

–More spending on renewables, so that everyone has access to electrical power rather than fossil fuels.

–More spending for farming, especially indoor farming.

–More spending for free healthcare services.

–More spending for domestic chip manufacture

Sadly, the government again is misinterpreting the situation, and wrongly believing that federal deficit spending causes inflation, has begun to look for ways to cut social benefits and increase taxes.

Democrats need to replace spending with spenvesting. For sure it would make people stop in their tracks and wonder ‘ WTF….did I just hear that right!?’ Then the media would pick up on it since it sounds crazy and, of course, they love bringing “crazy” to everyone’s attention. Then you pound it home… NO it wasn’t crazy or a misspeak. Spenvesting means you get back more in return for what you’ve spent money on. The money doesn’t disappear down a rabbit hole. It comes full circle as a stimulus for job creation, consumption, more profits, less crime, less waste, etc.

The poorer a man is, the more inflation hurts him.

Inflation always takes from the creditor and gives to the debtor by devaluing dollar-denominated assets.

But how, you many ask, can a poor man be a creditor and a rich man be a debtor?

One first needs credit in order to qualify for debt, and the poorer a man is, the less he is able to become a debtor.

The working poor are always forced by the social construct to be a creditor.

Inflation always takes from the wage-earner and gives to the employer, to whom he has credited his labor while he awaits payday.

Inflation always takes from the renter and gives to the landlord, to whom he has advanced his rent and security deposit.

Inflation always takes from the wage-earner who deposits his wages and gives to the banker, whose very business is one of managing debt.

Inflation takes from the pensioner on a fixed income and gives to the financial sector, as economist Richard Cantillon explained in the “Cantillon Effect” nearly four centuries ago.

Inflation is a direct redistribution of wealth from the working poor to the financial sector, which explains the extraordinary enrichment of the financial sector in the US since the end of the gold standard in the 1970s.

The rich man owns real estate, stocks and other assets that are relatively safe from inflation. But the working poor must pay the inflation tax on everything that they own, including the labor of their own hands.

Inflation is the most regressive tax, and the most cruel. This is why there is so often starvation in nations with hyper-inflation; inflation preys on the most vulnerable in society, and the greater the inflation, the greater the harm inflicted upon the poor.

⸺ Thomas R. Eddlem

Similarly, the rich benefit from recessions, in that the Gap between rich and poor widens. The rich are able to pay desperate people lower salaries.

And of course, the rich are able to retain ownership of stocks and real estate, whose value has fallen, and even buy more at discount prices, waiting for the recession to end, and values bounce back up.

Some thoughts:

So, who got a Ph.d for proving that spending and inflation are related, when, in view of your graphs, they aren’t? Where did that come from? Or that high interest rates will “cool” GDP growth when, as you state, higher interest rates mean pumping in more federal money; therefore a stimulus, not a cooling.

Fear and professional rejection controls those three groups–politics, media and teaching. Monetary Sovereignty will no doubt rob the .1% of their “ace in the hole.” It’s no wonder Monetary Sovereignty is practically unheard of.

LikeLike

As I’ve written in the past, even our friends get it wrong. I just dropped this note to my occasional pen pal, Stephanie Kelton, whose recent book was right about “the Big Lie,” but unfortunately included the “spending / inflation” misunderstanding.

————————————————————————————–

Hi Stephanie,

I hope all is well for you.

Some thoughts:

The current economic atmosphere provides a perfect learning experience for MMT. The Big Lie (“Federal taxes fund federal spending”) hasn’t changed, but some things have:

1. The JG (Jobs Guarantee) has become more obviously wrong. Workers are demonstrating that they won’t accept the jobs a JG would by necessity offer. It’s time to get off that horse.

2. The fact that inflation did not earlier occur with federal deficit spending, but rather now, with shortages, demonstrates again that the old trope, “Inflation is too much money chasing too few goods” is wrong.

The new trope is: “Inflation is too few goods and services”. Period.

Every inflation in history has been caused by scarcities. The scarcities usually are food, energy, and labor (although today’s scarcity of computer chips has entered the mix).

The cure for today’s inflation will require more federal spending to acquire the scarce goods and services.

–More spending on renewables, so that everyone has access to electrical power rather than fossil fuels.

–More spending for farming, especially indoor farming.

–More spending for free healthcare services.

–More spending for domestic chip manufacture

Sadly, the government again is misinterpreting the situation, and wrongly believing that federal deficit spending causes inflation, has begun to look for ways to cut social benefits and increase taxes.

Keep up the good work.

Rodger Mitchell

LikeLiked by 1 person

Democrats need to replace spending with spenvesting. For sure it would make people stop in their tracks and wonder ‘ WTF….did I just hear that right!?’ Then the media would pick up on it since it sounds crazy and, of course, they love bringing “crazy” to everyone’s attention. Then you pound it home… NO it wasn’t crazy or a misspeak. Spenvesting means you get back more in return for what you’ve spent money on. The money doesn’t disappear down a rabbit hole. It comes full circle as a stimulus for job creation, consumption, more profits, less crime, less waste, etc.

LikeLiked by 1 person

I like it.

Or maybe, just call it what it is: “Investing,” as in investing in health, investing in education, investing in food, investing in happiness.

LikeLiked by 1 person

The poorer a man is, the more inflation hurts him.

Inflation always takes from the creditor and gives to the debtor by devaluing dollar-denominated assets.

But how, you many ask, can a poor man be a creditor and a rich man be a debtor?

One first needs credit in order to qualify for debt, and the poorer a man is, the less he is able to become a debtor.

The working poor are always forced by the social construct to be a creditor.

Inflation always takes from the wage-earner and gives to the employer, to whom he has credited his labor while he awaits payday.

Inflation always takes from the renter and gives to the landlord, to whom he has advanced his rent and security deposit.

Inflation always takes from the wage-earner who deposits his wages and gives to the banker, whose very business is one of managing debt.

Inflation takes from the pensioner on a fixed income and gives to the financial sector, as economist Richard Cantillon explained in the “Cantillon Effect” nearly four centuries ago.

Inflation is a direct redistribution of wealth from the working poor to the financial sector, which explains the extraordinary enrichment of the financial sector in the US since the end of the gold standard in the 1970s.

The rich man owns real estate, stocks and other assets that are relatively safe from inflation. But the working poor must pay the inflation tax on everything that they own, including the labor of their own hands.

Inflation is the most regressive tax, and the most cruel. This is why there is so often starvation in nations with hyper-inflation; inflation preys on the most vulnerable in society, and the greater the inflation, the greater the harm inflicted upon the poor.

⸺ Thomas R. Eddlem

LikeLiked by 1 person

Yes.

Similarly, the rich benefit from recessions, in that the Gap between rich and poor widens. The rich are able to pay desperate people lower salaries.

And of course, the rich are able to retain ownership of stocks and real estate, whose value has fallen, and even buy more at discount prices, waiting for the recession to end, and values bounce back up.

LikeLiked by 1 person

So you are more in the Consumer Monetary Theory camp? https://medium.com/@alexhowlett/introduction-to-consumer-monetary-theory-78905b0606ca

LikeLike