Much has changed in the past 13 years, but not the realities, and it is these realities that seem to mystify our thought leaders.

Today’s post will give you those realities, so you will understand why our economy continually lurches from recession to recession, with Congress, the President, and the Federal Reserve flailing about in apparent helplessness against the winds of fate.

Our leaders are not helpless. On the contrary, they have all the tools necessary to exert absolute control over our economy, even during the most stressful times. Even in the face of war, COVID, global warming, and population changes, etc., recessions, depressions, and inflations could be prevented, and prosperity could be implemented, but for the prevailing lack of knowledge or effort.

Economists wish to portray economics as a mathematically-based science, similar to physics, where precise predictions often are possible. But because economics is intertwined with psychology, at best a pseudo-science, predictions veer from inaccurate to just plain WAG (Wild Ass Guesses).

Knowing that exact replication of economics studies is impossible, and even approximations can be wrong, economists tend not to stray far from earlier WAGs and to quote liberally from the past.

Unfortunately, the past, at least the more distant past, omitted Monetary Sovereignty. It is the recognition that the creator of a currency never can run short of that currency, does not need or use income to pay for things, and has absolute control over all aspects of that currency.

The finances of a Monetarily Sovereign entity are nothing like those of a monetarily non-sovereign entity. Confusingly, similar words are used to describe both.

Words like “debt,” “deficit,” “trust fund,” “taxes,” “financial burden,” “prudent,” “money supply,” “borrow,” and even “pay” have different meanings and implications when applied to Monetarily Sovereign entities vs. monetarily non-sovereign entities. These differences are not widely understood or taught in schools.

What follows is a summary-in-brief of those differences.

But if it ever becomes widely understood, the intelligent application of Monetary Sovereignty will significantly reduce the incidence of inflations, recessions, depressions, poverty, hunger, homelessness, street crime, illiteracy, sickness, and the collection of taxes.

Here are some facts of which you may not be aware:

The U.S. government arbitrarily created the U.S. dollar from thin air. There were no U.S. dollars in the thousands of centuries before the 1780s.

Then suddenly, the U.S. government created U.S. dollars from thin air — as many as it wanted to — by creating new laws, also from thin air, which it has the infinite ability to do.

Just as laws have no physical existence, so do U.S. dollars have no physical reality. Dollars are nothing more than numbers on balance sheets controlled by the government. Those printed dollar bills are only titles to dollars. Just as a house title is not a house and a car title is not a car, a dollar bill is not a dollar.

Every form of money is a form of debt. Bank savings accounts, checking accounts, money market accounts, C.D.s, travelers’ checks, and corporate bonds all are owed by someone or something. Even the dollar billrepresents a debt of the federal government, which is why it has the words “federal reserve note” printed on it. “Bill” and “note” are words referencing debt.

Just as a car title is not a car, and a house title is not a house, a dollar bill is not a dollar. It is a bearer title to a dollar, which is no more physical than a number.

Because dollars have no physical existence but are only numbers, the federal government has the power to create infinite dollars merely by pressing computer keys. It makes as many dollars as it wishes.

(Former Federal Reserve Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press [or, today, its electronic equivalent], that allows it to produce as many U.S. dollars as it wishes at essentially no cost.“)

Today, the federal government retains the power to create laws that develop infinite dollars and to give those dollars whatever value it wishes.

This ability is called “Monetary Sovereignty.” The federal government is sovereign over the U.S. dollar.

While the federal government is Monetarily Sovereign, state/local governments, businesses, and people are monetarily non-sovereign.

Monetarily non-sovereign entities do not have the infinite ability to create U.S. dollarsor to give those dollars arbitrary values. Monetarily non-sovereign entities can run short of dollars.

While the U.S. government and the governments of the U.K., Mexico, Canada, Australia, Sweden, and others are Monetarily Sovereign, the governments of France, Italy, Germany, Portugal, and others are monetarily non-sovereign. They use the euro. They cannot control their money supplies, nor do they have the ability to fight inflation, recession, or depression.

The European Union (E.U.) is sovereign over the euro. The E.U. is run by the rich. It can fight inflation, recession, and depression but instead forces the poorest people of the euro nations to shoulder that burden.

The U.S. federal government cannot unintentionally run short of dollars, even if it collects no taxes.

Federal taxes and American federal taxpayers do not fund federal government spending. The federal government could provide unlimited benefits (Medicare for All, Social Security for All, College for All, etc.) without taxes. The term, “spending taxpayers’ money,” when referring to the federal government is incorrect. The government does not spend taxpayers’ money.

The purpose of federal taxes is not to provide the federal government with dollars but rather to: A. Control the economy by taxing what it wishes to discourage and giving tax breaks to what it wishes to encourage B. To assure demand for the dollar by requiring dollars to be used for tax payments, and C. to discourage the public from asking for benefits. This is a function of Gap Psychology — the desire of the rich to distance themselves from the middle- and lower-income/wealth/power public.

Money is the way modern economies are measured. By definition, a large economy has a larger money supply than does a small economy. Therefore, a growing economy requires an increasing supply of money. QED. The graph shows the essentially parallel paths of GDP (red) vs. a broad measure of the U.S. money supply, Domestic Non-Financial Debt (blue)

Medicare and Social Security are not funded by so-called “trust funds,” which are not real trust funds but only balance sheet lines. WHAT ARE FEDERAL TRUST FUNDS? September 20, 2016, Peter G. Peterson Foundation A federal trust fund is an accounting mechanism used by the federal government to track earmarked receipts (money designated for a specific purpose or program) and corresponding expenditures. The largest and best-known funds finance Social Security, Medicare, highways and mass transit, and pensions for government employees. Federal trust funds bear little resemblance to their private-sector counterparts. In private-sector trust funds, receipts are deposited, and assets are held and invested by trustees on behalf of the stated beneficiaries. In federal trust funds, the federal government does not set aside the receipts or invest them in private assets. Instead, the receipts are recorded as accounting creditsin the trust funds, and the receipts themselves are comingled with other receipts that Treasury collects and spends.

The government has total control over these balance sheet numbers, belying the false claim that the “trust funds” soon will run short of dollars. The federal government has absolute control over those balance sheet numbers. It can add to them or reduce them at will.

Your Social Security check comes from a mythical trust fund that contains no money and receives no money. Social Security (and Medicare) benefits are paid ad hoc by the U.S. government, not from a trust fund, and are not dependent on FICA taxes. Which can and (opinion) should be eliminated.

The federal government creates new dollars ad hoc by paying bills. No receipts by the Treasury are spent. They all are destroyed.

Debt is not a burden on the federal government. It is not, as some have been calling it for over eighty years, “a ticking time bomb.”The infinite ability to create dollars means the government can service any debt denominated in dollars by creating dollars, ad hoc.

The federal Debt/GDP ratio often is quoted with alarm. A high ratio wrongly is thought to indicate the federal government’s difficulty paying its debts. In fact, the Debt/GDP ratio is meaningless, having zero predictive power. Looking at a list of countries by their Debt/GDP ratiowill not tell you which countries are better or worse able to pay their bills.

It is impossible to evaluate any aspect of a nation’s economy by looking at its Debt/GDP ratio. The ratio says nothing about the health of the U.S. economy or about the federal government’s ability to pay its bills. See Debt to GDP ratio by country.

The federal government creates dollars by paying creditors. A. To pay a creditor, the federal government sends instructions (not dollars) to the creditor’s Bank, instructing the Bank to increase the balance in the creditor’s checking account. B. The instant the Bank obeys those instructions, new dollars are created from thin air and added to the M1 money supply measure. C. The instructions then are cleared through the Federal Reserve and the government agency issuing the instructions.

What is commonly called “debt” is the total of dollar depositsinto privately owned Treasury Security accounts by the purchase of T-bills, T-notes, and/or T-bonds. A. To make a deposit into a T-security account, one opens a T-security account and uses U.S. dollars to invest in a T-bill, T-note, or T-bond. B. The government never touches those dollars other than to make interest deposits. C. The government does not use those dollars; it creates new dollars, ad hoc, to pay its bills. D. Upon maturity, the government returns the account balance to the account owner. Visualize how a bank treats deposits in safe deposit boxes. E. Because the dollars already exist in the T-security accounts, returning them is not a financial burden on the U.S. government or any taxpayer.

Not needing an input of dollars, the government provides T-bills, etc., only to provide a safe place to store unused dollars and to help it control interest rates. Both purposes help the government stabilize the dollar.

Even if large holders of T-securities (China is a notable example) were to stop buying T-securities (the term “lending” erroneously is used), the federal government could continue spending as before. If the Federal Reserve felt a need to issue T-securities, they could buy them themselves. There is no financial need for the U.S. to sell T-securities to China.

Some worry that one day the U.S. dollar will cease to be the world’s reserve currency. That should not be a concern. A reserve currency is nothing more than a currency banks hold in reserve to facilitate international commerce. Many currencies function as reserve currencies, including: the euro, Japanese yen, British pound, Chinese yuan, and others.

A federal “deficit” is the difference between dollars the government creates and sends to the economy (aka “the private sector”) vs. dollars the private sector sends to the government.

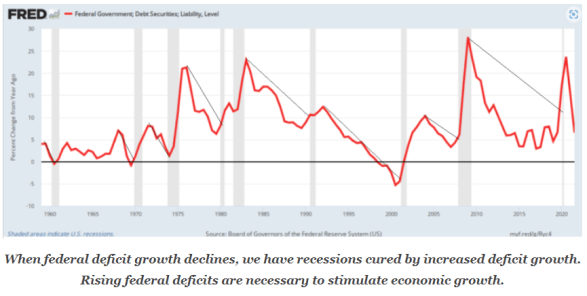

When federal deficit and debt growth are reduced we experience recessions and depressions. 1804-1812: Federal Debt reduced by 48%. Depression began 1807. 1817-1821: Federal Debt reduced by 29%. Depression began 1819. 1823-1836: Federal Debt reduced by 99%. Depression began 1837. 1852-1857: Federal Debt reduced by 59%. Depression began 1857. 1867-1873: Federal Debt reduced by 27%. Depression began 1873. 1880-1893: Federal Debt reduced by 57%. Depression began 1893. 1920-1930: Federal Debt reduced by 36%. Depression began 1929. 1997-2001: Federal Debt reduced by 15%. The recession began 2001.

Federal deficits enrich the economy and are necessary to grow the economy. They add dollars to the economy, and they help prevent and cure recessions.

Gross Domestic Product (GDP) is a measure of dollars spent in the economy, which is why adding dollars to the economy stimulates GDP growth.

Balanced budgets, though appropriate for personal finances, cause recessions and depressions when attempted by the federal government. To grow, the private sector needs to receive more dollars from the federal government than it pays to the federal government (aka a federal deficit).

The federal government receives dollars from the economy through taxes, fines, and other payments.

All dollars received by the federal government are destroyed upon receipt. a. Taxes are paid from the private sector (aka “the economy) checking accounts (Those dollars are part of the “M1” money supply) and are sent to the U.S. Treasury. b. When dollars reach the Treasury, they cease to be part of any money supply measure. Because the government has the infinite ability to create dollars, there can be no measure of how many dollars the government has. It has infinite dollars. (Infinite dollars + Tax Dollars = Infinite dollars. No change.) c. Because tax dollars do not increase the federal government’s money supply, they are effectively destroyed. d. Dollars sent to monetarily non-sovereign state/local governments, businesses, and people are not destroyed. They are deposited into private sector banks and remain part of the M1 money supply.

Monetarily non-sovereign entities (state/local governments, businesses, etc.) create dollars by borrowing and lending. a. When a bank lends dollars, it does not lend depositors’ funds. It adds dollars to the borrower’s checking account (M1) and balances its books by counting the borrower’s note as dollars. b. Upon consummating the loan, the Bank has dollars (the note), and the borrower also has the dollars it borrowed. Thus a loan creates dollars. c. As the loan is paid down, dollars held by the borrower are sent to the lender, and the loan balance loses value.

By contrast, the federal government does not borrow its own sovereign currency, the U.S. dollar. It pays all its bills by creating new dollars.

The federal government collects taxes not to fund spending but to: a. Control the economy by taxing what it wishes to discourage and giving tax breaks to what it wishes to encourage b. Create demand for the dollar by requiring taxes to be paid in dollars c. Create the false impression that taxes are necessary to fund spending so that the public acquiesces to benefit limits.

Import duties are taxes levied on imported goods. These taxes are paid by the purchaser, not by the seller. For example, a duty on imports of Chinese goods is paid by the American consumer, not by the Chinese exporter.

Inflation is a general increase in prices.

Prices increase because supply is insufficient to satisfy demand (scarcity).

Historically, dollar creation has not caused an increase in demand sufficient to cause inflation. Federal deficit spending does not cause inflation.

There is no relationship between increases in federal deficit spending (red) and inflation (blue)

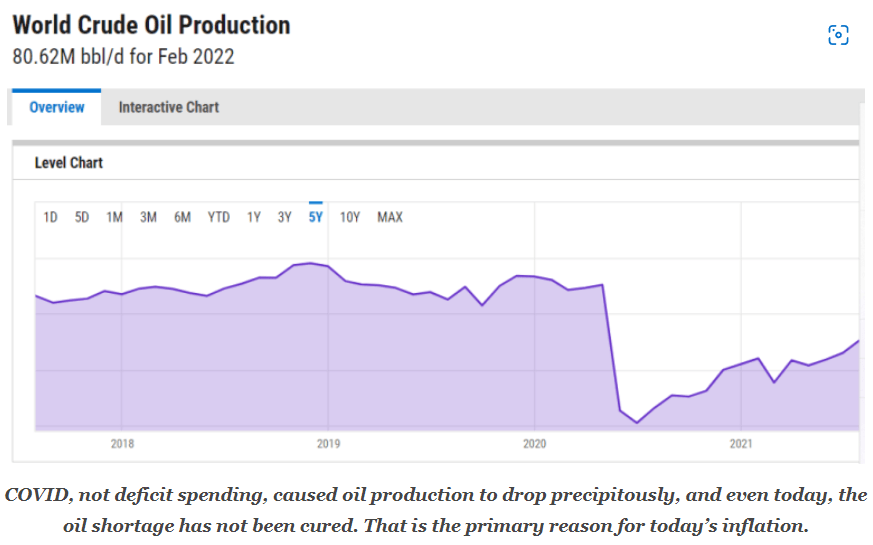

A. All inflations have been caused by the insufficient supply of critical goods and services, most often oil and food. B. Today’s inflation is caused by scarcities of oil,food, lumber, computer chips, shipping (supply chain), labor, and other COVID-related factors.

Oil shortages cause most inflations. Curing oil shortages cures most inflations.

C. These shortages are not caused by money creation and cannot be cured by restricting money creation plans such as interest rate increases.Those plans do not remedy the scarcities that are responsible for inflation. D. Curing inflation requires curing shortages, not recessing the economy.

Federal deficit spending does not cause inflation. E. Shortages often begin with a disease, weather, war, or government mismanagement. COVID caused many shortages and was the original impetus for today’s inflation. F. The famous Zimbabwe inflation began when the government took farmland from experienced farmers and gave it to people who didn’t know how to farm. The resultant food shortage, not Zimbabwe’s money creation, caused hyperinflation.

The federal government can cure shortages by additional deficit spending to obtain scarce goods and services or encourage their creation.

Eliminating the FICA tax would fight inflation by lowering labor costs and thus the cost of most goods.

There is no economic benefit to privately owned banks. The federal government should own all the banks. Because the federal government doesn’t have a profit motive, there would be none of those risky securities the big banks have dreamed up. These garbage contracts led to the Big Recession of 2008, and because the banks were not punished, no lessons were learned. The same problems are happening today.

More efficient and generous immigration laws would fight inflation by reducing the labor shortage.

Low interest rates are not stimulative. Low interest rates (purple) do not correspond with high economic growth (green).

Increasing interest rates can make the dollar more valuable and have some stimulative effect because low rates force the government to pay more interest dollars into the economy. But low rates do not cure shortages. They actually can exacerbate shortages and intensify inflation.

Interest rate increases make private sector money creation (borrowing) more difficult, which can recess the economy.

On balance, high and low interest rates have both stimulative and recessive elements. But they do not cure inflations, and it is the inflations that lead to recessions or “stagflation” (the combination of a stagnant economy and inflation).

A symptom of this bifurcation is the stock market’s adverse reaction to good economic news. Any good news (low unemployment, high GDP growth, etc.) impels the Fed to raise interest rates, which the public believes will hurt business and depress securities.

Recessions have no agreed-upon definition but often are defined as a decline in real Gross Domestic Product (GDP) for two consecutive quarters. GDP is a measure of spending. Federal Spending + Nonfederal Spending + Net Exports = GDP.

Depressions often are defined as recessions that last at least two years.

The prevention and cure for recessions and depressions is federal deficit spending,which adds dollars to the economy (aka the private sector) and increases GDP.

Reductions in federal deficit spending or surpluses lead to recessions and depressions, providing the private sector with insufficient growth dollars.

The Fed has no cure for stagflation, though Congress and the President do. A. The “stagnation” part of stagflation is cured by federal stimulus spending, as is done to cure every recession. B. The “inflation” part of stagflation is cured by federal spending to obtain the goods and services whose scarcity is causing inflation.

Though state and local governments are monetarily non-sovereign concerning the U.S. dollar, nothing stops any entity –you, me or anyone–from creating their own sovereign currency and being Monetarily Sovereign concerning that currency. A. The currency would face the problem of demand, i.e., the acceptance of the money in payment, which in part would depend on the “full faith and credit” of the issuer. B. Many forms of money exist in America. One example is manufacturer coupons. They are issued by businesses, have a stated value, and are accepted by retailers. C. Some aspects of the U.S. dollar’s “full faith and credit” are: i. The government will accept only U.S. currency in payment of debts to the government ii. It unfailingly will pay all its dollar debts with U.S. dollars and will not default iii. It will force all domestic creditors to accept U.S. dollars, if offered, to satisfy any debt. iv. It will not require domestic creditors to accept any other money v. It will protect the value of the dollar. vi. It will maintain a market for U.S. currency vii. It will continue to use U.S. currency and will not change to another currency. viii. All forms of U.S. currency will be reciprocal; five $1 bills always will equal one $5 bill, etc.

An example of Monetary Sovereignty and full faith & credit can be found in the board game, “Monopoly®.” By rule, the Bank in that game never can run out of Monopoly dollars, and it does not rely on income to pay its debts. Thus, the Monopoly bank is Monetarily Sovereign.

Being Monetarily Sovereign, the Bank has infinite Monopoly dollars, and neither its deficits nor its debt is a burden on the Bank or on the players (corresponding to the real-world economy).

Gold and silver are not, and never have been money. At most, they have been value standards to which the value of money is compared.

Gold or silver never “backed” the dollar. The prices of gold and silver vary wildly, but through the years, the federal government arbitrarily and often has changed the value of dollars vs. gold and silver (which destroys the “backed” claim.) The only thing backing the U.S. dollar is the full faith and credit of the U.S. government.

The prevention and cure for street crime is not more police or more severe punishment. The prevention and cure for street crime is to reduce poverty.

The federal government has the power to reduce poverty and thus to reduce street crime) by paying for health care insurance (Medicare for All), living expenses (Social Security for All), education (college for all), food (Supplemental Nutrition Assistance Program — SNAP for all), life insurance for all, and housing (rent assistance for all).

“Rich” and “poor” are relative terms. A person having a million dollars would be poor if everyone else had ten million. A person with a thousand dollars would be rich if everyone else had ten dollars. The income/wealth/power difference between those who have more and those who have less is the Gap.

The wider the Gap, the richer are the rich.

To become more prosperous, the rich (who run our world) continually attempt to widen the Gap. They can widen the Gap by gaining more for themselves or byforcing the poorer to have less.

To force the poorer to have less, the rich feed them the disinformation that the federal government cannot afford to pay for benefits, that federal spending causes inflation, or that benefits require taxes. None are true. A. The federal government can afford anything (It’s Monetarily Sovereign); B. federal spending never has caused inflation (shortagesof oil and other goods and services cause inflation); C. federal taxes don’t pay for anything (the federal government creates dollars, ad hoc, to pay for all its spending). Federal taxes are destroyed upon receipt.

The rich also spread the disinformation that if the federal government provides benefits, the poor will refuse to work. To debunk this myth, one only needs to look at the rich, or even at the upper middle classes, who continue to work despite receiving massive tax benefits.

Human wants are unlimited. Even the rich wish to be richer, more powerful, more respected, more envied, more admired, and to have more of everything. Most people want a better life for themselves and their children.

Thus, even upon receiving free medical care, housing, food, clothing, education, etc., people will continue to work for more than what is considered “basic” at any moment in time.

To help spread their disinformation, the rich bribe: A. Politicians(via political donations and promises of future employment), B. Economists (via university donations and jobs in think tanks), and C. The media (via advertising dollars and media ownership).

The rich bribe politicians to pass tax laws and other laws favorable to the wealthy and unfavorable to the rest of us, to widen the income/wealth/power Gap.

Congress’s approval of benefits reveals an ugly part of the human psyche: Jealousy. President Biden’s approval of student loan debt reduction elicited cries of “Unfair” from those who already had paid off much or all of their student loan debt.

But all benefits are felt to be “unfair” by those who didn’t receive the benefit before it was begun. This demonstrates the intimate relationship between economics and psychology.

The European Union (E.U.) is Monetarily Sovereign over the euro and is run by the rich, forcing the euro nations to struggle for lack of euros. This helps widen the Gap between the European rich and the rest.

The United States is a not-very-democratic republic. While we, the people, do elect our leaders, the election system is highly skewed toward rural power. The Senators’ elections and the national Presidential elections give excessive power to rural voters vs. urban voters. This originally was done by our founders to encourage rural states to join the union.

Within the Senate, voting rules give a few Senators, sometimes only one Senator, extreme power. Even the supposedly population-based House of Representatives accomplishes this dubious, undemocratic achievement via gerrymandering,the manipulation of an electoral constituency’s boundaries so as to favor one party or class.

The Supreme Court, the final arbiter of all laws, proudly pays no attention to what the public wants. Instead, they are nine (currently) unelected people who make national decisions based on their personal and religious philosophies and party affiliation.

As such, the unelected Supreme Court’s desired impartial functions have been superseded by the Justices’ personal biases. A case could be made for eliminating the Supreme Court and allowing the electedExecutive and Legislative branches of government, which more closely reflect the desires of the public, to fill the role. An alternative would be to impose term limits on SCOTUS justices.

The above points are merely summaries of broader truths about the U.S. economy. Most have been discussed at greater length in this blog’s preceding posts.

9 thoughts on “What you should know about our economy that others don’t know.”

#4 is actually the entire problem.

#40a is partially true, but speculative excess, other kinds of financialization and unconsciousness of the monopoly paradigm of Debt Only (#4) are deeper causes.

Your comment reminds me that I want to add another point: There is no economic benefit to privately owned banks. The federal government should own all the banks. The federal government doesn’t have a profit motive for the crazy securities the banks have dreamed up. They led to the big recession of 2008, and because the banks were not punished, no lessons were learned. The same problems are happening today.

Yep. Private money creation is a huge 5000 year old acculturated and hence unconscious parasite as its “product” is always either pre-production (production loans) or post retail sale (mortgages and credit card debt). A true national public bank is the ultimate answer, and as a national bank would not require making a profit it would be easy (and humane and intelligent) to implement a second 50% discount/debt jubilee policy at the point of loan signing. Then we could truly become the “ownership economy”.

Bottom line, I wouldn’t even want to “kill off” banks. I would like to see the federal government offer convenient, honest banking services to everyone, not just without profit but essentially without income.

Loan interest would be at the fed funds rate — the rate the banks charge each other. It’s the rate the Fed sets as the floor for all other lending, and for maintaining the strength of the dollar.

Just as Medicare doesn’t “kill off” medical privately offered health care insurance, the government shouldn’t kill off private banking services — at least not directly.

Indirectly, however, a government bank has the power to outcompete private banking services simply by offering better, more honest service at better rates. Think of it as Medicare in the banking industry.

Also, credit unions are not immune from misdeeds. Look up the Hyfin Credit Union, CUSO Financial Services, LPL Financial LLC, and Cetera Advisor Networks LLC, St. Paul Croatian Federal Credit Union, Barnstable Community Federal Credit Union, Municipal Credit Union, Broome County Teachers Federal Credit Union, and numerous others.

And let us never forget Charles Keating and the U.S. savings and loan crisis of the 1980s and early 1990s. 747 savings and loan associations in the United States failed. The ultimate cost of the crisis is estimated to have totaled around $160.1 billion

The banks have also managed to count interest payments in the NIPA statistics as part of GDP even though they are non-productive asset transfers. This makes it look like private banks are a vital part of the US economy, when all they really do is widen the gap by siphoning off economic surplus and transferring it to wealthy investors.

Credit unions and even banks could survive in the new pardigm, but only lending already created and saved money…and only lending to those entities that the true national public bank wouldn’t lend to like hard core pornography and to enterprises that will not qualify for the 50% Discount/Rebate policy at retail sale like assult rifles and ammo. And even then they’d have to agree to strict regulation. Banks as we currently know them could not compete with banks as a public utility. wisdomicsblog.com Systems were made for Man, not Man for Systems.

#4 is actually the entire problem.

#40a is partially true, but speculative excess, other kinds of financialization and unconsciousness of the monopoly paradigm of Debt Only (#4) are deeper causes.

LikeLike

Thanks, chdwr,

Your comment reminds me that I want to add another point: There is no economic benefit to privately owned banks. The federal government should own all the banks. The federal government doesn’t have a profit motive for the crazy securities the banks have dreamed up. They led to the big recession of 2008, and because the banks were not punished, no lessons were learned. The same problems are happening today.

Just added it at # 43.

LikeLike

Yep. Private money creation is a huge 5000 year old acculturated and hence unconscious parasite as its “product” is always either pre-production (production loans) or post retail sale (mortgages and credit card debt). A true national public bank is the ultimate answer, and as a national bank would not require making a profit it would be easy (and humane and intelligent) to implement a second 50% discount/debt jubilee policy at the point of loan signing. Then we could truly become the “ownership economy”.

LikeLike

You’d kill off the non-profit credit unions too?

LikeLike

Bottom line, I wouldn’t even want to “kill off” banks. I would like to see the federal government offer convenient, honest banking services to everyone, not just without profit but essentially without income.

Loan interest would be at the fed funds rate — the rate the banks charge each other. It’s the rate the Fed sets as the floor for all other lending, and for maintaining the strength of the dollar.

Just as Medicare doesn’t “kill off” medical privately offered health care insurance, the government shouldn’t kill off private banking services — at least not directly.

Indirectly, however, a government bank has the power to outcompete private banking services simply by offering better, more honest service at better rates. Think of it as Medicare in the banking industry.

LikeLike

https://twitter.com/NagaSlateTTV/status/1580383945899749376 Haha #BankOfAmericaIsCommieTrash was trending earlier because as a bank in a free market they canceled some Q-kook’s account

LikeLike

Also, credit unions are not immune from misdeeds. Look up the Hyfin Credit Union, CUSO Financial Services, LPL Financial LLC, and Cetera Advisor Networks LLC, St. Paul Croatian Federal Credit Union, Barnstable Community Federal Credit Union, Municipal Credit Union, Broome County Teachers Federal Credit Union, and numerous others.

And let us never forget Charles Keating and the U.S. savings and loan crisis of the 1980s and early 1990s. 747 savings and loan associations in the United States failed. The ultimate cost of the crisis is estimated to have totaled around $160.1 billion

LikeLike

The banks have also managed to count interest payments in the NIPA statistics as part of GDP even though they are non-productive asset transfers. This makes it look like private banks are a vital part of the US economy, when all they really do is widen the gap by siphoning off economic surplus and transferring it to wealthy investors.

LikeLike

Credit unions and even banks could survive in the new pardigm, but only lending already created and saved money…and only lending to those entities that the true national public bank wouldn’t lend to like hard core pornography and to enterprises that will not qualify for the 50% Discount/Rebate policy at retail sale like assult rifles and ammo. And even then they’d have to agree to strict regulation. Banks as we currently know them could not compete with banks as a public utility. wisdomicsblog.com Systems were made for Man, not Man for Systems.

LikeLike