Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

Mitchell’s laws:

●Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

●The more federal budgets are cut and taxes increased, the weaker an economy becomes. .

●Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

●Austerity is the government’s method for widening the gap between rich and poor.

●Until the 99% understand the need for federal deficits, the upper 1% will rule.

●To survive long term, a monetarily non-sovereign government must have a positive balance of payments.

●Everything in economics devolves to motive, and the motive is the Gap.

==================================================================================================================================================================

Professor Allen W. Smith is professor of economics, emeritus, from Eastern Illinois University. He wrote an article titled, “Is the government able and willing to repay Social Security debt?”

His article demonstrates the false information being given, not only to the public, but to students of economics, and not only to students at Eastern Illinois University, but to students at universities all across America and the world.

Many of these students will become influential leaders, and so will pass this false information to other students and to the public. This is how the Big Lie has been, and is being, promulgated.

Here is my open letter to Professor Smith:

Dear Professor Smith;

Your article, “Is the government able and willing to repay Social Security debt”? appeared in the February 25th issue of the Sun Sentinel.

I knew immediately, from the title alone, that your article would be filled with inaccuracies, because our Monetarily Sovereign government is able to repay any debt of any size, though it may not always be willing.

The U.S. government, being Monetarily Sovereign, by definition is sovereign over its own currency. It can create as much as it wishes, any time it wishes.

The federal government never can run short of dollars, which it creates ad hoc, every time it pays a bill. The federal government never needs to ask anyone for U.S. dollars — not you, not me, not China.

Here are a few excerpts from your article, and my comments:

“The short-term solvency of Social Security is in the hands of the federal government. Enough payroll taxes have been paid to cover full benefit payments until 2033. But $2.7 trillion of that money was taken by the government and spent for non-Social Security purposes. The spent money was replaced with government IOUs, called Special Issues of the Treasury.”

Social Security is an agency of the U.S. federal government, which can pay any size bill at any time, simply by pressing a computer key. The federal government pays its bills by sending instructions (not dollars) to each creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

At the moment the bank complies, and not before, dollars are created.

There is no financial limit to the amount of instructions our Monetarily Sovereign federal government can send to banks. The federal government never can be insolvent, and so, no federal agency can become insolvent, unless Congress wills it.

The White House, Congress, and the Supreme Court are three of the 1,000 federal agencies, for which no federal tax is collected. Yet they cannot become insolvent.

How then could Social Security (which does have a federal tax — FICA — collected on its behalf) become insolvent? Clearly, it cannot.

“The financial condition of the United States government is dire. The national debt, which first reached $1 trillion in 1981, is today more than $18 trillion. The credit of the United States government today is not nearly as good as it was in 1981.”

This statement is based on the popular, though false, belief that federal finances are like personal finances, where debt is a burden. For our Monetarily Sovereign government, debt is no burden whatsoever.

First, as we have said, the federal government has the unlimited ability to pay any bill denominated in its sovereign currency, the dollar. But more importantly, federal debt is considerably different from personal debt (and different from city, county and stated debt).

To “lend” to the federal government, you buy a T-security (T-bill, T-note, T-bond, etc.). You instruct your bank to transfer dollars from your personal checking account to a T-security account at the Federal Reserve Bank. You become a depositor at the FRB.

To repay your “loan,” the FRB does what any bank does when it pays a depositor: It transfers existing dollars from your T-security account to your personal checking account.

It’s a simple asset transfer. No new dollars are needed, except for interest, which our Monetarily Sovereign government creates ad hoc.

What most people do not understand, though I’m sure you do, is that all bank deposits are considered bank debt. So when you put money into your bank savings account, your bank’s debt increases by that amount.

Yet your bank boasts about the size of its deposits, while the public wrings its hands about the size of federal “debt” — which is nothing more than the total of deposits in T-security accounts at the FRB. Federal “debt” = deposits in T-security accounts at the FRB. Debt is bank deposits.

If you and your colleagues would more properly refer to federal “deposits,” rather than federal “debt,” all the concerns about federal “debt” would disappear.

“The statement, ‘Social Security has enough money to pay full benefits until 2033,’ is made over and over as proof of Social Security’s short-term solvency. It has been repeated so many times that almost nobody questions its validity. But it is not true.

“Social Security does not have the means to pay full benefits, even for the current year. Since 2010, the cost of paying full Social Security benefits has exceeded tax revenue, and the gap is widening at an increasing rate.”

The U.S. government became Monetarily Sovereign (on August 15, 1971). Federal taxes no longer fund federal spending.

Even if all federal tax collections fell to $0, the federal government could continue spending, forever. It simply would continue to send instructions to banks, telling the banks to increase checking account deposits, thereby creating dollars.

This means, FICA does not fund Social Security benefits. FICA could, and should, be eliminated, and Social Security benefits should be increased.

Again, you confuse federal finances with personal finances.

“Each year, the government has to borrow money to fill the gap. Without the borrowing, full Social Security benefits could not currently be paid.”

Absolutely, 100% false. The federal government never needs to ask anyone for its own sovereign currency. It does not need to borrow money to “fill the gap,” or for any other reason. Nor does it need to levy taxes so to pay its bills.

Taxation and the issuance of T-securities (falsely known as “borrowing”) are relics of the gold standard days, when the federal government was not Monetarily Sovereign.

“On Oct. 3, 2013, President Obama warned that unless the debt ceiling was raised Social Security checks would not go out on time.”

Sadly, the President of the United States, every member of Congress, most media and most mainstream professors tell the Big Lie — the lie that federal spending relies on federal taxing.

Even more sadly, some politicians may simply be ignorant of the facts, but the professors are not. But have been paid to go along with the Big Lie.

The rich — the upper .1% — are rich because of the Gap between them and the rest of America. If there were no Gap, no one would be rich, and the wider the Gap, the richer they are.

So, the primary goal of the rich is not just to make more money, but rather, to widen the Gap, either by lifting themselves or pushing the rest of us down — or both.

The rich bribe those of influence. They bribe the President and Congress via campaign contributions and promises of lucrative employment later.

They bribe the media via ownership. They bribe mainstream economists via contributions to universities. They even fund “independent” think tanks to spread the gospel (i.e. the Big Lie) that benefits to the poor- and middle-income people depend on taxes. And since current taxes are less than benefits, either the benefits “must” be decreased or taxes “must” be increased.

“David Walker, the Comptroller General of the GAO, tried to make it clear that the trust fund did not hold any real bonds. He said, ‘There are no stocks or bonds, or real estate in the trust fund. It has nothing of real value to draw down.'”

Of course. To the public, this may sound shocking, but it always has been true. In fact, the Unites States Federal Government neither has nor needs dollars. It pays its bills, not with dollars, but by sending instructions, ad hoc, to banks, telling the banks to create dollars by increasing the balances in checking accounts.

If you receive a check from the federal government, that check is not money. It is a set of instructions, telling your bank to increase the balance in your checking account.

“President Bill Clinton’s 2000 budget proposal included a statement of just what the IOUs truly were: ‘The Social Security Trust Fund does not consist of real economic assets that can be drawn down in the future to fund benefits.

Instead, they are claims on the Treasury that, when redeemed, will have to be financed by raising taxes, borrowing from the public, or reducing benefits or other expenditures.'”

President Clinton, who like President Obama today, was owned by the rich, so he said what the rich told him to say. His comment is a clever combination of truth and the Big Lie.

It is true that “The Social Security Trust Fund does not consist of real economic assets that can be drawn down in the future to fund benefits. Instead, they are claims on the Treasury . . .” But the rest is the Big Lie.

These claims on the Treasury will not need to be “. . . financed by raising taxes, borrowing from the public, or reducing benefits or other expenditures.” That is what the rich want the populace to believe.

“Raising taxes and reducing benefits” is exactly how the Gap has been widened over the years.

Then professor, you finish your article with your final summation of the Big Lie:

“If the government repaid its debt to Social Security, there would be no short-term Social Security solvency problem.”

The government does not owe a debt to its own agency. Like the federal government as a whole, Social Security neither has nor needs dollars. It pays all its debts by sending instructions to banks.

Similarly, there is no “Social Security solvency problem.” This is an invention by the rich, to justify increase in taxes on the rest of us, of reducing benefits to us.

The politicians, had they any morals, would be ashamed at what they are doing. The media too, which pretend independent news dissemination, should be ashamed.

But, the most ashamed should be the mainstream economics professors, who spend their lives investigating the facts, then turn their backs on the facts and teach eager young minds the Big Lie.

For shame, Professor Smith! For shame, Eastern Illinois University! For shame, America’s academic institutions!

For shame!

Rodger Malcolm Mitchell

Monetary Sovereignty

===================================================================================

The Ten Steps to Prosperity:

1. Eliminate FICA (Click here)

2. Federally funded Medicare — parts A, B & D plus long term nursing care — for everyone (Click here)

3. Provide an Economic Bonus to every man, woman and child in America, and/or every state a per capita Economic Bonus. (Click here) Or institute a reverse income tax.

4. Federally funded, free education (including post-grad) for everyone. Click here

5. Salary for attending school (Click here)

6. Eliminate corporate taxes (Click here)

7. Increase the standard income tax deduction annually. (Refer to this.)

8. Tax the very rich (.1%) more, with higher, progressive tax rates on all forms of income. (Click here)

9. Federal ownership of all banks (Click here and here)

10. Increase federal spending on the myriad initiatives that benefit America’s 99% (Click here)

Initiating The Ten Steps sequentially will add dollars to the economy, stimulate the economy, and narrow the income/wealth/power Gap between the rich and the rest.

——————————————————————————————————————————————

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

![]()

No nation can tax itself into prosperity, nor grow without money growth. Monetary Sovereignty: Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

1. A growing economy requires a growing supply of dollars (GDP=Federal Spending + Non-federal Spending + Net Exports)

2. All deficit spending grows the supply of dollars

3. The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

4. The limit to non-federal deficit spending is the ability to borrow.

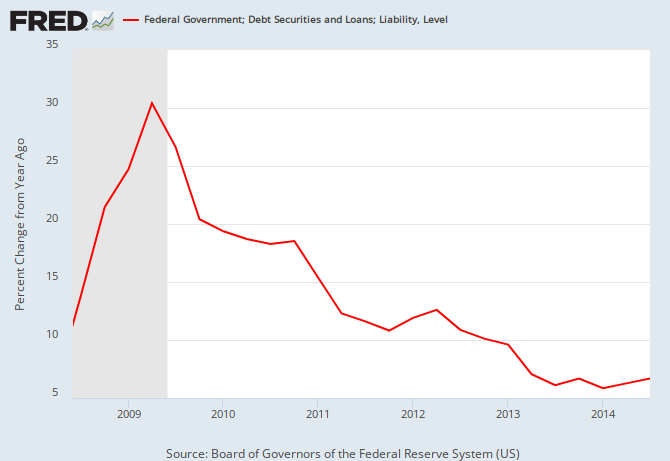

THE RECESSION CLOCK

Vertical gray bars mark recessions.

As the federal deficit growth lines drop, we approach recession, which will be cured only when the growth lines rise. Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

#MONETARYSOVEREIGNTY

It would be wonderful if the professor replied. At least Prof. Krugman admits that personal and federal finances are not the same and that the federal debt is not “bad”.

LikeLike

Yes, it would.

Here is how he describes himself:

He’s written a bunch of books, mostly with the same nonsense about Social Security being broke. And every year, eager, young minds are infected with that foolishness.

Truly sad.

LikeLike

I’d like to see his full response posted on this site and your counter-argument.

I am 100% sure he will not agree with you on just about all counts. There are many liars out there, I don’t think Professor Smith is one of them.

LikeLike

In the unlikely event he deigns to respond, I most definitely will post his response — and answer it.

Just curious: With which “accounts” do YOU disagree? Perhaps you can be his proxy, since you seem to know him so well.

LikeLike

Amusingly and ironically, I think, Dr. Smith has a web site named “thebiglie.net”, promoting his book and its theme. He certainly does believe taxes are sacred and he likes to use the word “embezzled” a lot. For some reason he thinks (or says) that there is something fundamentally different between so-called “income” taxes and so-called “payroll” taxes as though some taxes are not really taxes.

From Dr. Smith’s site: “Why isn’t the government’s embezzlement of the Social Security trust fund money common knowledge today? It’s not common knowledge because the government does not want the public to find out that it has been using Social Security payroll tax revenue, as if it were income-tax revenue, for the past 30 years.”

LikeLike

Jim,

Actually, there is something fundamentally different between income taxes and payroll taxes:

Everyone pays income taxes, even the rich, although the rich manage to avoid a large percentage of theirs.

By contrast, payroll taxes (specifically, FICA) are paid only on the first $100K of payroll, which makes them the most regressive taxes in America — worse even than sales taxes.

As for the “government’s embezzlement of Social Security trust fund money,” this is so wrong it would be merely ignorant if said by a lay person, but downright stupid if said by an economist.

The “embezzlement” actually is the collection of FICA, which is 100% unnecessary — merely a way to impoverish the lower income groups and widen the Gap.

Unlike state and local governments, the federal government neither needs, nor even uses, federal tax money. All those federal taxes you pay disappear into a giant black hole, never to be seen, again.

For every dollar the federal government spends, the government creates brand new money, or more accurately, instructs banks to create brand new money.

There is no “pass through” of dollars the way there is when you and I spend our income. The federal government does not spend its income.

LikeLike

Sure, I get that FICA dollars, by definition, hit the same virtual tax shredder as do income tax dollars. What kills me is that, for some reason, most of my (normally rational) friends recoil from that revelation. The thought of FICA dollars being anything other than SS contributions is repulsive to their psyches, apparently, even as they complain about too high income taxes. Most would inexplicably prefer to rage at the government for “embezzling” their Social Security dollars than clamor for an end to FICA. That’s cognitive dissonance at work, I guess. As for Dr. Smith, well, he has tapped into a ready and willing audience.

LikeLike

A few comments:

1. The US having a debt denominated in dollars is like Parker Brothers having a debt in monopoly money, in terms of ability to pay.

2. “But $2.7 trillion of that money was taken by the government and spent for non-Social Security purposes.” People seem to think that the money could have been invested risk free at 5%. Who would be willing to borrow that money? There was no other reasonable option for that money but to have been spent by the USG.

3. “The national debt, which first reached $1 trillion in 1981, is today more than $18 trillion.” In 1981 the professor was liely saying that the debt is unsustainable. Now it has increased 18-fold and the dollar is a strong as ever. If that isn’t a perfect example of sustainability, what is?

LikeLike

Ian, your #1. and #3. are correct.

As for #2., that $2.7 trillion was not spent on anything, and could not be invested in anything. The moment those dollars hit the Treasury, they disappeared.

When the federal government spends, it sends instructions to banks to create brand new dollars, by increasing the balances in checking accounts.

As I told Jim (above), the federal government does not “pass though” its income, the way you and I and local governments do.

When it takes in tax dollars, it destroys them. Then creates new dollars when it spends.

LikeLike

“The short-term solvency of Social Security is in the hands of the federal government. Enough payroll taxes have been paid to cover full benefit payments until 2033. But $2.7 trillion of that money was taken by the government and spent for non-Social Security purposes. The spent money was replaced with government IOUs, called Special Issues of the Treasury.”-Allen W. Smith

From US govt. “Trust Fund” data site:

Question #7:

Q:Why do some people (um, such as certifiably idiotic Professor Allen W. Smith, who apparently can’t read) describe the “special issue” securities held by the trust funds as worthless IOUs? What is SSA’s reaction to this criticism?

A: ‘Money flowing into the trust funds is invested in U. S. Government securities. Because the government spends this borrowed cash, some people see the trust fund assets as an accumulation of securities that the government will be unable to make good on in the future. Without legislation to restore long-range solvency of the trust funds, redemption of long-term securities prior to maturity would be necessary.

Far from being “worthless IOUs,” the investments held by the trust funds are backed by the full faith and credit of the U. S. Government. The government has always repaid Social Security, with interest. The special-issue securities are, therefore, just as safe as U.S. Savings Bonds or other financial instruments of the Federal government.’

http://www.ssa.gov/oact/progdata/fundFAQ.html#a0=6

(Of course no money flows into the SS trust funds. The funds are an accounting fiction, easily manipulated by the US govt/Congress if needed, even under current SS law.)

LikeLike

Exactly. Smith seems to think federal financing is like personal (and state and local government) financing, where income dollars are saved, and later are spent.

In federal financing, income dollars are destroyed. When the government spends, it creates new dollars, ad hoc.

For a professor of economics not to understand this basic fact is shocking (or would be shocking if the majority of economics professors didn’t promulgate the same falsity.)

LikeLike

What is the difference between the government giving me 200 bucks I can use to buy 200 dollars worth of food. Or if the government forced an establishment to give me 200 dollars worth of food?

LikeLike

If the government gave you $200, that would add $200 to the economy, thereby stimulating the economy.

If an establishment gave you $200 worth of food, no new money would be added to the economy, so there would be no stimulus.

Is there some deeper point to your question?

LikeLike

Perhaps,

I was not asking about the impact of adding new money, I simply ask because I don’t see any difference.

In terms of “stimulus”, can you explain how adding money to an economy stimulates it?

If the government creates the $200 or forces the establishment to fork over the goods, it’s essentially the same. So I struggle to understand how businesses would be stimulated by this.

LikeLike

You said, “If the government creates the $200 or forces the establishment to fork over the goods, it’s essentially the same.”

Adding money to an economy stimulates GDP, because:

GDP = Federal Spending + Non-Federal Spending + Net Exports

Federal Spending and Net Exports add dollars to the economy. Those are net additional dollars that circulate though the economy, and beget more spending.

When an establishment “forks over” dollars, it now has fewer dollars to fork over. So these are not net additional dollars to circulate through the economy.

GDP essentially is spending, and adding dollars facilitates spending.

LikeLike

I’m glad you take the fight to the clowns who support the silly and wrong ideas about macroeconomics.

No wonder it’s called a religion – like “science”, but it has no equivalent of a society like the AMA or AIA does for doctors and architects, or any other proper profession. So economists must know they speak dodgy “science”.

Sooner or later the tide will turn, but first these practitioners will have to start acknowledging there just might be something to MMM. [aka MMT]

It should not be news when the Reserve bank of Chicago wrote about it in 1963! Yet it still is news!

Eventually people like the professor will be caught saying it is self evident.

LikeLike

Mr. Mitchell, can you explain the relationship between the Treasury and the Fed? I understand that the Fed is not a government agency but instead is an invention of and owned by the 1%. If I understand corectly the Treasury incurs debt and interest liablity by issuing tresuries to the Fed as a process to create dollars through the Fed? If this is true then the US government spending has created a huge interest liability that must be paid. If you could clarify that relationship and the impact of it I would appreciate it. Thanks

LikeLike

The “Fed” is a government agency. The President of the U.S. appoints the Board of Governors including the Chairman, with approval by the Senate.

The Federal Reserve is not privately owned (any more than Congress is privately owned.)

The Treasury issues Treasury securities (T-bills, T-notes, T-bonds and dollar bills), which contrary to popular myth, do not fund federal spending.

The primary purpose of T-securities in a Monetarily Sovereign government, is to help the Fed control interest rates.

LikeLike

How does that work? How does issuing securities help control interest rates.

LikeLike

The Fed controls short term rates directly, via the Fed Funds rate. It controls long term rates via its purchases of T-bonds.

The more T-bonds the Fed purchases, the higher the price of T-bonds (Increased demand = increased price).

Bonds move inversely to interest. So when the bond price goes up, the interest rate goes down.

(Consider a bond selling for $1000 with an annual coupon rate of 3%. That means a buyer investing $1,000 will receive $30 per year. If the price of the bond rises to $1,100, a buyer still will receive $30, which will make the interest fuctionally 2.7+%).

LikeLike

Why would the Fed want low rates? Why would it want higher rates?

LikeLike

The Fed wants low rates, because it believes low rates are stimulative. The Fed is wrong in that regard. (See: https://mythfighter.com/2009/09/09/low-interest-rates-do-not-help-the-economy/)

In fact, those low rates reduce the amount of interest money the government pays into the economy, so low rates are recessive.

The Fed wants high rates when it wishes to cure or prevent inflation. The Fed is correct in that regard.

LikeLike

I agree on both counts. Low rates are not stimulative – I actually believe it’s almost impossible to “stimulate” the economy although I know you don’t see it that way. I feel that any attempt to “stimulate” will have the same result as low rates.

What the Fed is essentially doing is picking winners and losers – it’s making it cheap for borrowers to borrow at the expense of someone else’s income. So someone gets cheap rates, while someone doesn’t earn returns on their savings they should have – it’s a zero sum game. This, by the way, is eating up people on fixed incomes (retirees) and insurance companies that tend to have tons of cash laying around from premiums and need a consistently decent return to manage losses from accidents.

I also agree that higher rates remove currency from the system and help “slow down” inflation. But I would argue that the market would actually increase rates on it’s own if the level of perceived risk increased in the market.

Finally, I am completely amazed and stupefied when I see headlines about how the fed is somehow controlling things by updating/removing “wording” from their statements. Do people really believe that it’s “wording” that runs the economy and financial system?

Why do we need a central bank then?

LikeLike

Actually, higher rates add dollars to the economy, because the federal government must pay more interest. However, higher rates strengthen the dollar, which makes imports less costly, one way they fight inflation

LikeLike

Yes, the government does pay higher interest on newly issued bonds.

But the Fed and banks charge higher interest across ALL loans in the economy – which, I assume, is significantly more than the government pays out in interest.

Net net, higher rates decrease the amount of credit in the system.

LikeLike

No, net, net higher rates increase the money supply. Federal interest adds to the money supply, and bank lending also adds to the money supply.

No, banks do not lend their deposits (contrary to popular myth). Banks lends against their capital. Your bank deposits remain in your account.

LikeLike

So lowwring rates remove mone from the money supply? Not in a million years. Rates have been falling since the 80s. There is no sense in comparing today’s money supply to that in the 80s.

Lending creates money, and there is more propensity to take on debt when rates are decreasing. When rates spike, as they did the the 80s, asset prices as well as lending drop.

What is the purpose of taking deposits and paying interest on them?

LikeLike

One more thing.

When credit spreads widen in 2008-2009, it caused a cascade of bankrupcies. Not only did large funds and corporations go under, trillions in housing wealth vanished over night.

Without a doubt, high rates contract the money supply.

LikeLike

Thank you for clarifying that.

LikeLike

To cant think:

Your comments indicate you believe lower interest rates stimulate borrowing. Not correct, for these reasons:

1. Businesses do not base borrowing decisions on a 2% or 3% rate difference. That difference in interest rates comprises only a tiny fraction of a typical company’s cost of doing business.

Instead, borrowing decisions are based on business needs.

2. Business borrowing creates “temporary” dollars, which disappear as loans are paid down.

3. People do not buy homes because of a low interest rate, which translates into a minuscule monthly payment difference. What really happens when rates are reduced is people refinance existing mortgages, which reduces the money supply.

4. Low interest rates reduce federal interest payments on T-securities, which are “permanent” dollars, as they do not disappear when the T-securities are paid down.

These are the reasons why low interest rates do not stimulate economic growth.

LikeLike

Hey RMM-

Technically, if T-securities are paid down during budget surplus periods, those dollars are being destroyed.

T-securities balances mature and are converted to reserve balances =>

No new T-securities are issued to replace maturing T-securities balances

More reserve balances are removed through taxation then added through spending => money is is destroyed.

This is part of the unnecessary complication that thinking of TSY securities and reserves as distinct generates (not saying you do this) and thinking of both as types of bank deposits clarifies.

US Currency = All dollar deposits at the Fed + physical cash

Deficits = increased dollar deposits at Fed

Surpluses = reduced dollar deposits at Fed

The exact mix of securities to reserve balances is largely irrelevant (when excluding interest rate impacts).

Therefore, US currency is permanent to the extent that the Govt does not run budget surpluses.

LikeLike

I disagree that increased lending stimulates anything. You are simply shifting demand forward. You won’t buy tomorrow, what you buy today. If we are talking about the economy, there is no stimulus when debt is created.

If we are talking prices, people did buy homes because of lower rates, which increased demand and prices. The money related to refinancing is miniscule when compared to sales, and refinancing doesn’t remove money, it adds money. People normally refinanced for greater loans at lower rates and reset to 30 years.

The idea that the money added via federal spending is more, than say, 50 trillion of housing wealth that was erased overnight in 2008 is ludicrous.

The market is greater than the federal government, than the fed, and than you and I whether we like it or not.

Auburn,

Bank currency, the bulk, is missing from your post.

LikeLike

“Shifting demand forward” is known as “stimulus.”

Refinancing doesn’t add money. Money is debt. By reducing total debt, refinancing reduces the money supply.

No one said federal spending exceeded the loss of wealth during the housing crisis. And no one said the “market” (whatever that means) is less than the federal government (whatever that means).

LikeLike

I did not leave out anything, we were talking about Govt IOUs not private bank IOUs. They are different and only Govt IOUs are legal state currency.

Lower rates on mortgages due drive up home prices because the same amount of monthly payment allows for a larger mortgage. E.G. If you can afford $2000 per month on a mortgage, that allows you to buy a $350K house @ 10% and a $500K house @ 1%. (the math is not correct, Im just illustrating a point).

LikeLike

Hey Auburn,

Here is how the government “pays down” your T-securities. It merely transfers your existing dollars from your T-security account at the FRB to your checking account at your private bank.

Simple asset transfer. No change in dollar amount.

You are correct that taxes destroy dollars.

LikeLike

Right, Im just saying that Govt currency (Fed balances + cash) isnt necessarily “permanent” because its destroyed when budget surpluses are occurring.

The aggregate supply of private bank deposits is “permanent” to the extent that the nominal level of bank loans continues to increase

which is roughly equivalent to….

The aggregate supply of public bank deposits (currency) is “permanent” to the extent that the govt continues to deficit spend.

So neither are technically “permanent” as both are conditional on continued deficits (net bank lending = bank deficits in this framework)

LikeLike

RMM, thanks for sharing this letter to Prof. Smith. Your interpretation of our economic fiasco, however, causes some gaps in my own limited understanding of how our money distribution works; or, could/should work. And I grasp, completely I think, all that you are saying about the U.S. Treasury being able to legally print/electronically transfer all of the dollars, whether paper or digital, that it needs. And yes, most, if not all, of Congress either is ignorant of this, or feigns ignorance to keep themselves financially lubricated, and out of trouble with the controllers. My question is this: Why does not the uncontrolled distribution of dollars, paper or digital, not directly cause or exacerbate inflation? More money than there are goods and services is what enables inflation, is it not? Am I wrong about this, and if so, can you help me understand this scenario more accurately. Thanks for considering my question. alan

LikeLike

We don’t have an “uncontrolled distribution of dollars.” And, we don’t have too much money chasing too few goods.

Although the federal government has the power to create infinite dollars, there is a limit to dollar creation, and that is inflation. The government should continue to create dollars ala the “Ten Steps to Prosperity,” until it reaches a point at which inflation cannot be controlled by raising interest rates.

The U.S. never has reached that point, in its 240 year history.

Up ’til very recently, inflation had been caused by oil prices, and cured with interest rates.

LikeLike

Here is the key to your misunderstanding:

“More money than there are goods and services is what enables inflation, is it not?”

The amount of goods and services is linked directly to aggregate demand, unemployment, and foreign trade. More spending causes businesses to increase output via more machines and more workers, and there are 10’s of millions of unemployed and part-time workers that can be used to increase output to go along with more spending.

And this doesnt even count foreign trade, there are literally billions of people who would love to work around the globe to make goods and services to sell to America, that they dont is the result of the lack of US consumer spending power, not that the rest of the world is incapable of producing more stuff for the USA’s benefit.

Because of the way the sectoral balances work, if the Govt deficit spent 10% of GDP and the private sector sent that 10% ($1.7 trillion) worth of money to the rest of the world via our trade deficit, then the domestic private sector at home would still not be accumulating net financial wealth at a pace fast enough to produce inflation that was problematic.

In other words, the only rule of thumb that you need to know for the proper way to run the federal budget is this:

If unemployment is too high = > the deficit is too small

if inflation is too high => the deficit MAY be too big (the inflation may be from oil prices and not demand like it was in the 1970’s).

The only two periods of high inflation caused by demand in the 20th century would have been WWI and WWII, and both of those problems were solved by rationing. In other words, as Rodger likes to say, in 240 years as a nation, we have never had a serious case of too much spending and too few goods and services.

LikeLike

Many great questions in this comment section. But back to the original point, one reason FDR included SS payroll taxes was so that people would feel like they were owed their benefits, and would defend the program politically. And it worked well; for decades SS has been a political ‘third rail.’ But labor’s share of national income has been falling for some time, and so proportionally payments into the Trust Fund, contributing the perceived ‘shortfall.’ This seems to me to be a political vulnerability that SS’s opponents are likely to continue to try to exploit going forward.

LikeLike

You are correct. President Roosevelt was well aware that FICA does not fund Social Security benefits, but he believed that if people paid FICA, no one could take SS away from them.

Unfortunately, the deficit ignorants have been able to chip away at SS, by taxing it and by raising the benefits age.

LikeLike