Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

Mitchell’s laws:

●Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

●The more federal budgets are cut and taxes increased, the weaker an economy becomes. .

●Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

●Austerity is the government’s method for widening the gap between rich and poor.

●Until the 99% understand the need for federal deficits, the upper 1% will rule.

●To survive long term, a monetarily non-sovereign government must have a positive balance of payments.

●Everything in economics devolves to motive, and the motive is the Gap.

==================================================================================================================================================================

At its foundation, economics is simple and obvious. All you really need to remember is:

1. A Monetarily Sovereign nation, by definition, has the unlimited ability to create the money — its sovereign currency — to pay its bills. It never can run short of its sovereign currency.

2. For that reason, a Monetarily Sovereign nation neither needs nor uses tax money or borrowing to fund its spending. Deficits are no burden on its ability to pay its bills.

3. A growing economy requires a growing supply of money.

4. Deficit reduction reduces the supply of money.

5. Interest strengthens a currency by increasing the demand for that currency. Strengthening a currency reduces inflation, which is why central banks increase interest rates to fight inflation.

That’s the basis for all economics. Everything else is amplification.

Yet it seems beyond the understanding, not only of the general public, but of the world’s financial and political leaders. Consider the sad case of the United Kingdom:

January 1, 2015 3:58 pm

Annual FT economists’ survey: Spending cuts plans ‘not plausible’

Chris Giles and Emily CadmanThe UK government’s goal of cutting public spending so public finances are back in the black by 2018-19 with a large annual surplus by the end of the next parliament will not be delivered, most economists believe.

The UK government servants wish to be “in the black,” i.e. run a surplus. They want taxes (money coming out of the economy) to exceed spending (money going into the economy). They want the UK economy to be drained of money. That is the plan.

What will draining money out of the economy accomplish? What does applying leeches to the body of an anemic accomplish?

However, a majority do think deficit reduction will continue more or less as planned until the middle of the next parliament and events may make more action unnecessary.

(Of the 87 economists who answered a question on deficit reduction,) there is a consensus that Britain has to endure more cuts or tax increases to reduce the deficit, although the pace of cuts could be slowed from current plans.

As the British have been taught, the deficit is bad. No one knows why it is bad, but it surely is bad. Seemingly, the British people have too much money (i.e. blood), and this money must be removed from the economy to make the economy healthier.

Plans for £50bn of extra spending cuts a year were widely seen as not credible and unlikely to be achieved.

Ray Barrell of Brunel University said alternatives would include more borrowing and higher taxes for pensioners and property owners.

Or, the UK government, being Monetarily Sovereign, simply could create the pounds to pay its bills, thereby adding blood to the anemic patient.

Ian Plenderleith, a former MPC member, said it was “very important” to keep reducing borrowing.

This position was supported by Kathrin Muehlbronner, vice-president of sovereign risk at credit rating agency Moody’s. “Downward pressure on the UK’s sovereign bond rating could arise if fiscal consolidation stalled,” she said.

Ah yes, Moody’s. We know all about Moody’s. They are the ones who gave top ratings to worthless, mortgage-related investments, thereby helping to cause the Great Recession. By all means, let’s take seriously what Moody’s has to say.

Ryan Bourne of the Institute of Economics Affairs added that there was little likelihood of a “catastrophic event” if the deficit was not reduced “but failure to start getting public debt back on a downward path even now, when the economy is growing robustly, would put the UK in a very vulnerable position to shocks and longer-term fiscal headwinds due to an ageing population”.

The Monetarily Sovereign UK government never can run short of its sovereign currency, the pound. It can pay any bill denominated in pounds. It doesn’t need to borrow the pounds it already has created.

So why the need to reduce the “deficit,” (i.e., why reduce the money supply?) The debt Henny-Pennys scream “the sky is falling,” and that creating money causes inflation.

Their screams are punctuated by their favorite words: “Weimar,” “Zimbabwe” and “Argentina” to demonstrate that hyperinflation lurks right around the corner. (Never mind that Weimar, Zimbabwe and Argentina are not in any way related to the UK situation.)

14 October 2014

UK inflation rate of 1.2% is lowest in five yearsThe CPI is the rate the Bank of England targets and it is charged with keeping inflation at about 2%.

While some economists had speculated that the Bank of England might raise interest rates from the current record low of 0.5% before the end of the year, most had expected a rise early next year.

However, the latest inflation figures means a rate rise could be pushed back further.

“There is little sign of any inflationary pressures on the horizon,” said Martin Beck, senior economic advisor to the EY Item Club.

Governments control inflation by raising and lowering interest rates. Raising interest rates strengthens a currency by increasing the demand for that currency.

So, despite interest rates at a record low — below the target rate — and inflation the lowest in five years, the British government still wishes to starve the nation of money by cutting the deficit.

Why?

Very simply, it’s what the rich want.

Deficit spending benefits the 99% poor- and middle-income people far more than the 1% rich. So deficit spending narrows the Gap between the rich and the rest — exactly what the rich do not want.

It is the Gap that makes the rich rich, and the wider the gap, the richer they are. So the rich bribe the politicians and the economists to pretend that government financing is like personal financing, and that the government could run short of pounds.

The following were asked, “Do you think the next government will deviate from the current deficit reduction plans? Does it matter?”

Not one of the following had the courage or the honesty to stand up and object, “Austerity, for a Monetarily Sovereign nation, is nuts. It rewards the rich, punishes the rest and slows economic growth. It is the very last thing the UK should do. Those who favor austerity are ignorant or criminals.”

Many of them suggested cutting benefits to the poor as a method for reducing the deficit. The poor will suffer, the UK will stagnate and the Gap will widen — all at the behest of the rich.

Here are those whose names should be inscribed on a Wall of Shame. If you know any of these people, contact them and see if you can humiliate them into telling the truth:

Adam Posen, director Peterson Institute

Sir Alan Budd, former MPC member

Andrew Hilton, Centre for the Study of Financial Innovation

Azad Zangana, Schroders

Bart van Ark, The Conference Board

Bridget Rosewell, director, Volterra

Bronwyn Curtis, OMFIF

Charles Davis, Centre for Economics and Business Research

Charles Goodhart, former MPC member

Costas Milas, Liverpool University

Danny Blanchflower, Dartmouth University and former MPC member

David Cobham, Heriot-Watt University

David Kern, British Chamber of Commerce

Diane Coyle, Enlightenment Economics

Dieter Helm, Oxford university

George Magnus, Adviser to UBS

Howard Archer, IHS Global Insight

Sir Howard Davies, former MPC member

Ian Plenderleith, former MPC member

James Knightley, ING

James Meadway, New Economics Foundation

Sir John Gieve, former MPC member

John Hawksworth, PwC

John Llewellyn, consultant

John Muellbauer, Oxford university

John Philpott, consultant

Dame Kate Barker, former MPC member

Keith Wade, Schroders

Kitty Ussher, Tooley Street Research

Mark Miller, Economist Intelligence Unit

Matthew Whittaker, Resolution Foundation

Neil Blake, CBRE

Neil Williams, Hermes

Nicholas Barr, London School of Economics

Patrick Minford, Cardiff University

Peter Dixon, Commerzbank

Peter Warburton, Economic Perspectives

Peter Westaway, Vanguard

Phil Thornton, Clarity Economics

Ray Barrell, Brunell University

Richard Batley, Lombard Street Research

Richard Jeffrey, Cazenove

Robert Wood, Berenberg Bank

Ryan Bourne, Institute of Economics Affairs

Tony Dolphin, IPPR

Tony Yates, Bristol University

Melanie Baker, Jacob Nell, Morgan Stanley

Nick Bosanquet, Imperial

George Buckley, Deutsche Bank

Frances Cairncross, Heriot-Watt University

Jagjit Chadha, University of Kent

Kevin Daly, Goldman Sachs

Danny Gabay, Fathom Consulting

Sarah Hewin, head of macro research Europe, Standard Chartered Bank

Neville Hill, Credit Suisse

Brian Hilliard, Société Générale

Stephen King, HSBC

Ruth Lea, Arbuthnot Securities

Gerard Lyons, Chief Economic Adviser to The Mayor of London Boris Johnson

Allan Monks, JPMorgan

Kathrin Muehlbronner, vice-president sovereign risk group, Moody’s

Andrew Oswald, Warwick University

David Owen, Jefferies

Vicky Pryce, CEBR

Michael Saunders, Citi

Andrew Smithers, Smithers and Co

Phillip Shaw, Investec

David Tinsley, UBS

Daniel Vernazza, UniCredit

Simon Wells, chief UK economist, HSBC

Mike Wickens, York University

Chris Williamson, Markit

David Riley, head of credit strategy at BlueBay Asset Management

John van Reenen, director of the Centre for Economic Performance at the London School of Economics

Andrew Simms, fellow at the New Economics Foundation

Dhaval Joshi, chief strategist at BCA Research

Gary Styles, director — GPS Economics

Sir Christopher Pissarides, Regius Professor of Economics, LSE

Simon Kirby, economist NIESR

Samuel Tombs, senior UK economist, Capital Economics

Jonathan Portes, director, National Institute of Economic and social Research

Andrew Smith, economist

Andrew Sentance, PwC and former MPC member

Rodger Malcolm Mitchell

Monetary Sovereignty

===================================================================================

Ten Steps to Prosperity:

1. Eliminate FICA (Click here)

2. Federally funded Medicare — parts A, B & D plus long term nursing care — for everyone (Click here)

3. Provide an Economic Bonus to every man, woman and child in America, and/or every state a per capita Economic Bonus. (Click here) Or institute a reverse income tax.

4. Free education (including post-grad) for everyone. Click here

5. Salary for attending school (Click here)

6. Eliminate corporate taxes (Click here)

7. Increase the standard income tax deduction annually. (Refer to this.)

8. Tax the very rich (.1%) more, with higher, progressive tax rates on all forms of income. (Click here)

9. Federal ownership of all banks (Click here and here)

10. Increase federal spending on the myriad initiatives that benefit America’s 99% (Click here)

The Ten Steps will add dollars to the economy, stimulate the economy, and narrow the income/wealth/power Gap between the rich and the rest.

——————————————————————————————————————————————

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

![]()

No nation can tax itself into prosperity, nor grow without money growth. Monetary Sovereignty: Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

1. A growing economy requires a growing supply of dollars (GDP=Federal Spending + Non-federal Spending + Net Exports)

2. All deficit spending grows the supply of dollars

3. The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

4. The limit to non-federal deficit spending is the ability to borrow.

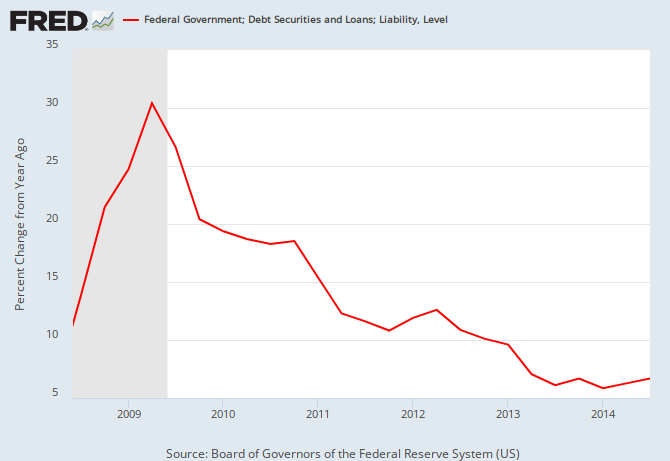

THE RECESSION CLOCK

Vertical gray bars mark recessions.

As the federal deficit growth lines drop, we approach recession, which will be cured only when the growth lines rise. Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

#MONETARYSOVEREIGNTY