Scott Horsley is NPR’s Chief Economics Correspondent. He reports on ups and downs in the national economy as well as fault lines between booming and busting communities. Horsley spent a decade on the White House beat, covering both the Trump and Obama administrations. Before that, he was a San Diego-based business reporter for NPR, covering fast food, gasoline prices, and the California electricity crunch of 2000. He also reported from the Pentagon during the early phases of the wars in Iraq and Afghanistan. Horsley earned a bachelor’s degree from Harvard University and an MBA from San Diego State University.Mr. Horsley seems to believe the government will run out of money in 2033 or maybe in 2036. I say that because of the article he wrote:

Social Security (SS) is an agency of the U.S. government. The only two ways SS can run out of dollars are:The clock is ticking to fix Social Security as retirees face automatic cut in 9 years MAY 6, 2027:06 PM ET, Scott Horsley

Congress has less than a decade to fix Social Security before the popular program runs short of cash, threatening a sharp cut in benefits for nearly 60 million retirees and family members, according to a government report released Monday.

- If Congress and the President want it to run out, or

- If the U.S. government runs out.

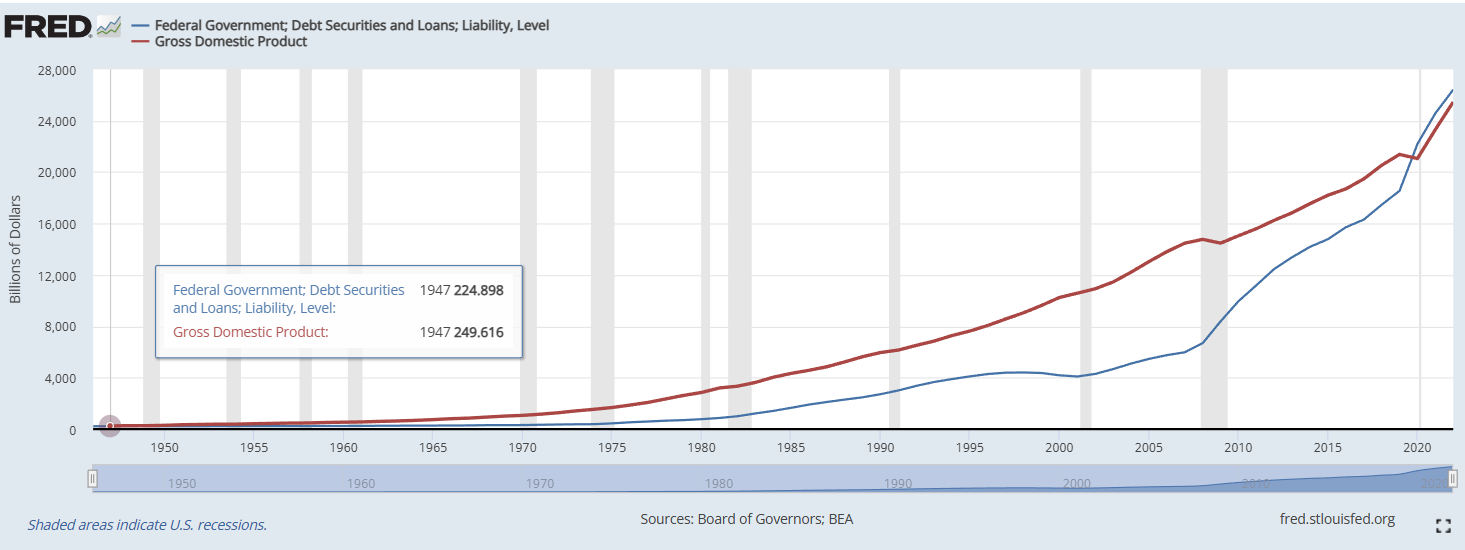

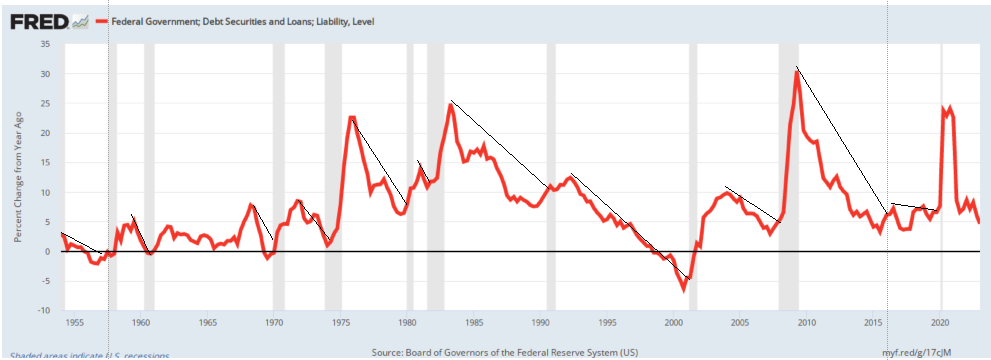

Despit what you repeatedly have been told, it isn’t a trust fund. It’s just a line item in a balance sheet. (See: “The phony trust fund controversy.“) The government can change those numbers to whatever it chooses at any time it chooses. Congress votes; the President approves; someone presses a computer key; and a one billion dollar “trust fund” instantly becomes a fifty billion dollar “trust fund.”The report from Social Security trustees predicts the retirement program’s trust fund will be exhausted in November of 2033.

Among the laws the government created were the laws creating Social Security. As an agency of the government, Social Security is funded the same way as every other agency: Congress votes, and the President approves. Congress and the President have unlimited freedom to decide how much any agency will receive:At that point, benefits would automatically be cut by 21%, unless lawmakers adopt changes before then.

- Mandatory spending – funding for Social Security, Medicare, veterans benefits, and other spending required by law. This typically uses over half of all funding. (Congress and the President make the law)

- Discretionary spending – federal agency funding. Congress sets funding levels for these each year. This usually accounts for around a third of all funding. (Congress and the President set the levels)

- Interest on the debt – this usually uses less than 10 percent of all funding. Congress and the President decide how much interest to pay and tax).

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Federal Reserve Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

The answer to the question, “When will the U.S. government run out of U.S. dollars?” is a resounding, NEVER, unless Congress and the President make that arbitrary decision. You and I are limited in our money supply. Your state, county, and city governments are limited. All businesses are limited. Banks are limited. Even euro nations are limited. All are monetarily non-sovereign. They were not the original creators of the U.S. dollar. By contrast, the U.S. government is Monetarily Sovereign. It was the creator of the dollar. It cannot unintentionally run short — not now, not in 2033, not in 2036, not ever. So why do writers like Scott Horsley think SS and Medicare, agencies of the federal government, will run short?Remember what Ben Bernanke said, “It’s not tax money… We simply use the computer to mark up the size of the account.” The federal government does not use your tax dollars to fund its spending. You (and Mr. Horsley) may be shocked to learn that every dollar you send to the U.S. Treasury is destroyed upon receipt. When you pay taxes, the dollars come out of your bank account, where they were part of the “M2 money supply measure.” When the dollars reach the Treasury, they instantly disappear from M2 and are not found in any money supply measure. They join the Treasury’s infinite money supply. Adding dollars to infinite dollars still yields infinite dollars. These dollars, which are not part of any money supply, no longer can be found. They have been destroyed. Why does the federal government collect taxes if not to fund spending?There’s some good news in the new forecast. Thanks to higher-than-expected worker productivity and a decline in expected disabilities, Social Security isn’t burning through cash as fast as trustees predicted a year ago.

Still, the long-term demographic challenges haven’t gone away.

A growing number of baby boomers are collecting benefits, while there are fewer people in the workforce paying taxes for each retiree.

Given today’s low birthrates, that mismatch is not expected to change for decades, although a surge in immigration helps.

- To control the economy by taxing what it wishes to discourage and by giving tax breaks to what it wishes to reward.

- To assure demand for the U.S. dollar by requiring taxes to be paid in dollars.

- To make you believe dollars are limited by taxes, so you will not request benefits. (This doesn’t discourage the rich from requesting and getting tax benefits unavailable to you.)

Mr. Horsley can think of only two fixes: Raise taxes or cut benefits. Both fixes predictably would impact the middle and lower income groups, thereby widening the income/wealth/power Gap between the rich and the rest. This is exactly what the rich want because the wider the Gap, the richer they are. Increasing your taxes and lowering your benefits makes the rich richer. And that is precisely what the rich bribe the media, the economists, and the politicians to do. It’s not that Mr. Horsley himself has been bribed. He may simply be following the “party line” created by others who have been bribed — just going with the flow, and not thinking about the reality that the federal government can’t unintentionally run short of dollars.Proposed Fixes Congress could fix the problem by raising taxes that support Social Security, reducing retirement benefits, or some combination of the two. But a politically palatable solution has been elusive.

Ah, yes, the famous Maya Macguineas, who repeatedly implies that the federal government is running out of dollars — now there is a “reliable” source.“When you see the two major candidates running for president tripping over themselves to promise what they won’t do to fix the problem, you have to worry because those kinds of reforms really start at the top,” says Maya Macguineas, president of the Committee for a Responsible Federal Budget.

Yes, yes, blah, blah, blah. “Committed to steps,” “Protect and strengthen.” And more blah, blah, blah. But what exactly are those steps?The Biden administration has pledged not to touch Social Security benefits.

“Seniors spent a lifetime working to earn the benefits they receive,” Treasury Secretary Janet Yellen, who leads the trustees, said in a statement.

“We are committed to steps that would protect and strengthen these programs that Americans rely on for a secure retirement.”

The classic Democrat/Republican false choices. The Dems want to soak the rich. The GOP wants to soak the rest of us.Congressional Democrats have proposed higher taxes on the wealthy to support Social Security.

Congressional Republicans have balked at that, instead calling for reducing the benefit formula and raising the retirement age for younger workers.

Why aren’t they already being chased? Because the public has been fed so many lies by so many “reliable sources,” the people don’t realize they are being lied to. On first reading of this post, most people will think, “That can’t be true.” But it’s true. The federal government could fund a comprehensive, no-deductible Medicare for every man, woman, and child in America and a generous Social Security program for everyone, all without collecting a single penny in taxes. Yes, there’s no question we can afford it. So? So? AFFORD IT!“Those who want to cut Social Security couch it in affordability,” says Nancy Altman, who heads the advocacy group Social Security Works.

“But of course, there’s no question we can afford it. It’s really a question of values. And as polarized as we are, we’re not polarized over this.”

Altman is confident that lawmakers will find a solution before automatic cuts take effect.

“If they didn’t act, not only would they all be voted out of office,” she says. “They couldn’t even remain in Washington. They’d be chased down the street.”

You have been fed lie after lie after lie. Your information sources wring their hands in mock horror that one day soon, the federal government will run short of dollars, perhaps right after the universe runs short of stars and politicians become honest. Even the densest among us can see the solution: The federal government should pay for Social Security and Medicare, period. Eliminate FICA. It doesn’t fund SS or Medicare. It doesn’t fund anything. Those FICA dollars are destroyed upon receipt. FICA serves only as a convenient excuse (convenient for the rich) to limit and cut your SS and Medicare benefits, thus widening the income/wealth/power Gap and making the rich richer and you poorer. In technical terms, that pisses me off, and it should piss you off, too. What are you going to do about it? Rodger Malcolm Mitchell Monetary Sovereignty Twitter: @rodgermitchell Search #monetarysovereignty Facebook: Rodger Malcolm MitchellBut the clock is ticking, and delay has already been costly.

“Every year the trustees warn us we have to make changes and the sooner we make them, the better and easier it will be,” says Macguineas. “And every year we fail to make those changes.”

Medicare and disability solvency While Social Security’s retirement program is in danger of running short of cash, a separate program that supports disabled people appears to be solvent for the long term, trustees said.

Medicare’s finances have also improved somewhat in the last year, thanks to a strong economy and lower-than-expected spending. Still, the program which provides health care for nearly 67 million people, is expected to face its own cash crunch in 2036.

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY