……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

#Monetary Sovereignty – Mitchell

Economics, Money and Debt

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

Those who do not understand (or who pretend not to understand) economics, repeatedly confuse federal finances with personal finances.

Those people decry the size of the federal deficits and debt as being “unsustainable,” which these measures would be if they were personal deficits and debt.

The federal government, being uniquely Monetarily Sovereign, never can run short of its sovereign currency, the U.S. dollar, so the government can “sustain” any size deficit and debt.

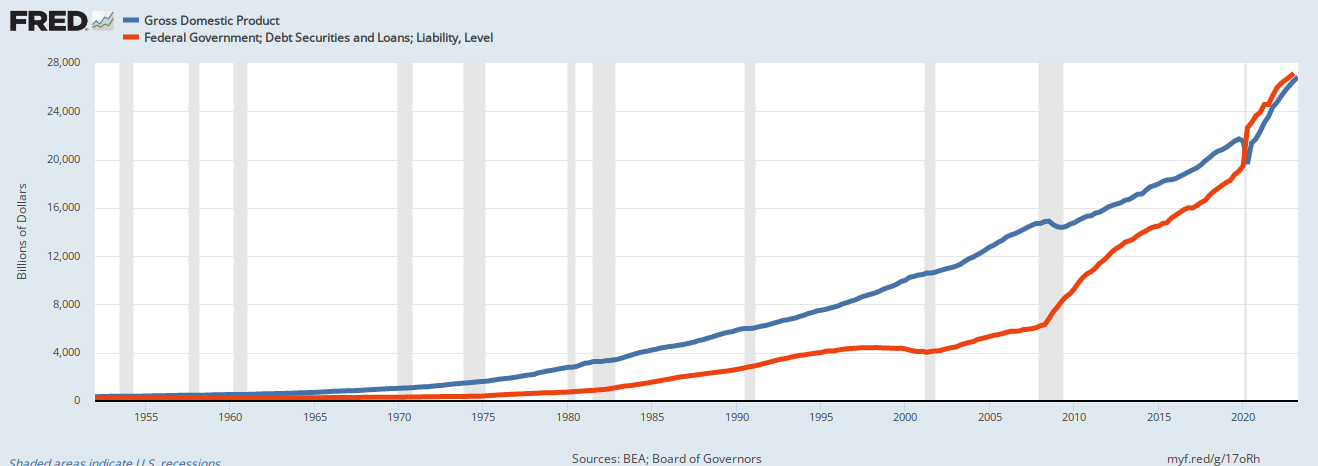

GDP = Federal Spending + Non-federal Spending + Net Exports

If the deficit critics were correct, you would expect to see:

Yet that is exactly the opposite of what you see.

*Historically, reduced deficits have caused recessions and even depressions. Increased deficit spending is necessary to cure recessions and depressions.

.

.

.

.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

The following graph compares the annual federal debt percentage changes (red line) which reflect deficits, vs. GDP percentage changes (blue line). The vertical bars are recessions.

What you do see is:

For clarity, let’s examine individual segments of the above graph:

Prior to 1974, federal deficits rose then fell, pulling GDP along with them. This reduced deficit spending precipitated the recession of 1974, which was cured by increased deficit growth through 1976.

The increased deficit growth precipitated increased GDP growth, with momentum carrying GDP through 1979, when it too began to fall.

……………………………………………………………………………………………………………………………………………………..

As a result of the long period of falling deficit growth, even the short upturn in the last quarter of 1979 could not save the economy, and the falling momentum of GDP resulted in the recession of 1980.

The increased deficit growth cured the recession, which ended in the 3rd quarter of 1980, when GDP turned up, and continued to be pulled up by more deficit growth.

……………………………………………………………………………………………………………………………………………………..

Continued, increasing deficit growth pulled GDP up, and even when deficit growth declined, in 1981, momentum pulled GDP upward.

……………………………………………………………………………………………………………………………………………………..

Yet again, you see that familiar pattern. Declining deficits lead to the recession of 1981, which growing deficits cure by the end of 1982.

Increasing deficits pull GDP upward, and even when deficit increases end in the 2nd Qtr of 1983, momentum continues to carry GDP upward.

……………………………………………………………………………………………………………………………………………………..

The enormous deficits of 1983 force powerful GDP growth momentum, which reverses as deficit growth continues to decline.

……………………………………………………………………………………………………………………………………………………..

And there again, the familiar pattern: Reduced deficit growth forcing down GDP growth, and even a short period of deficit growth increase cannot forestall the recession of 1990-1991.

And again, increased deficit growth cures the recession and turns GDP growth upward.

……………………………………………………………………………………………………………………………………………………..

As always, the predictable pattern:

……………………………………………………………………………………………………………………………………………………..

And here we go again: Massive deficit spending pulls us out of a recession; after escaping that disaster we begin again to cut deficit growth, then (in mid-2007) we increase deficit growth; but it’s too late, and we enter yet another recession; this one is the “Great Recession” of 2008.

……………………………………………………………………………………………………………………………………………………..

Now here we are, today. Huge deficit growth, having cured the recession, we continue not only those big deficits, but even grow them, first at 30% annually, finally leveling off at about 5% annual deficit growth — a big number, considering the size of the deficit.

This has caused GDP to average a robust average of about 4% annual growth.

……………………………………………………………………………………………………………………………………………………..

Despite all the incontrovertible data, the next time you open your newspaper, or watch you local federal finance TV “expert,” you will be told that the federal debt and/or deficit are (oh, horrors) at record highs, and are “unsustainable,” or a “ticking time bomb.”

It’s no coincidence that GDP is at record highs, too. Federal deficit spending lifted it there.

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell

Search #monetarysovereignty Facebook: Rodger Malcolm Mitchell

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

The most important problems in economics involve:

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

2. Federally funded Medicare — parts A, B & D, plus long-term care — for everyone

3. Provide a monthly economic bonus to every man, woman and child in America (similar to social security for all)

4. Free education (including post-grad) for everyone

5. Salary for attending school

6. Eliminate federal taxes on business

7. Increase the standard income tax deduction, annually.

8. Tax the very rich (the “.1%”) more, with higher progressive tax rates on all forms of income.

9. Federal ownership of all banks

10. Increase federal spending on the myriad initiatives that benefit America’s 99.9%

The Ten Steps will grow the economy and narrow the income/wealth/power Gap between the rich and the rest.

MONETARY SOVEREIGNTY