In 1647, the Massachusetts “Old Deluder Satan Act” required towns in colonial New England to hire teachers. The schools were funded by local taxes to promote literacy, so people could read the Bible.

This is widely regarded as the first law that mandated publicly funded education in what would later become the United States. By the early 1800s, this idea had spread, with other New England states adopting similar town-funded schools, although southern states did not follow suit.

In the 1830s to 1850s, modern free public schooling took shape. In Massachusetts in 1837, Horace Mann championed free, universal education funded by taxes and implemented by professional teachers.

By around 1850, most Northern states had established free public elementary schools funded by property taxes. These schools were accessible to most white children, as racial equality was achieved much later.

High schools came in 1821. The Boston English High School became the first free public high school in the U.S.

If we give them a college education, they won’t work in our factories.

By the late 1800s to early 1900s, free public high schools became widespread. Compulsory attendance laws began in 1880–1918, and segregation ended (legally): 1954, Brown v. Board of Education. Truly universal access began in the mid-20th century.

Why was free schooling mandated in the past, while free advanced education is often discouraged today? The answer, as usual, involves Monetary Sovereignty and Gap Psychology,

Our Monetarily Sovereignfederal government has an unlimited ability to create dollars with just a keystroke. It never can go bankrupt or run out of money. However, it often chooses to fund tax breaks for the wealthy rather than allocate resources to education for those who are less fortunate.

Gap Psychologydescribes a common, almost universal desire to distance oneself from those lower on the income, wealth, and power scale while trying to associate more with those above. This mindset is the primary way the wealthy maintain and increase their wealth. It also ensures that people continue to work even after they receive higher pay.

WASHINGTON — The Trump administration said Tuesday that it will begin garnishing the wages of student loan borrowers who are in default early next year.

The department said it will send notices to about 1,000 borrowers the week of Jan. 7, with more notices to come at an increasing scale each month.

Millions of borrowers are considered in default, meaning they are 270 days past due on their payments. The department must give borrowers 30 days’ notice before garnishing their wages.

The department said it will begin collection activities, “only after student and parent borrowers have been provided sufficient notice and opportunity to repay their loans.”

In May, the Trump administration ended the pandemic-era pause on student loan payments and began collecting on defaulted debt by withholding tax refunds and other federal payments from borrowers.

The move ended a period of leniency for student loan borrowers. Payments resumed in October 2023, but the Biden administration extended a one-year grace period. Since March 2020, no federal student loans had been referred for collection, including those in default, until the Trump administration’s changes earlier this year.

The Biden administration tried multiple times to offer broad student loan forgiveness, but those efforts were eventually halted by courts.

Persis Yu, deputy executive director of the Student Borrower Protection Center, criticized the decision to begin wage garnishment and said the department had failed to sufficiently help borrowers find affordable payment options.

Given that:

Educated young people are vital for America’s advancement and security.

The federal government does not need or even use any form of income.

The federal government has the infinite ability to create dollars and fund anything it wishes.

Why does the government fund free elementary and high school — in fact, make attendance compulsory — but garnish the wages of our single most valuable future resource, college students?

Free basic schooling still reinforces the social hierarchy. It still supports the Gap. Early public education has been sold as moral and obedience training, workforce preparation, and national cohesion.

It teaches punctuality, deference to authority, and literacy sufficient for labor, not power.

Even in our early days, basic schooling did not threaten the Gap. Elites benefit because it make for more productive workers, fewer unruly poor, and cultural conformity

But college education for the poor is exactly what the rich do not want.

It reduces the fear of losing one’s job, thus:

It increases labor’s bargaining power (which is why the rich hate unions), and

It puts “the rabble” on a par with the rich and weakens employers’ control.

Free college would narrow the Gap.

In this context, a federally sponsored, comprehensive, no-deductible Medicare program that coversevery man, woman, and child in America would help close the healthcare Gap.

In contrast, business-sponsored healthcare insurance for workers tends to reinforce this Gap. Millions of workers fear leaving their jobs or making demands of their employers because they worry about losing their healthcare coverage.

The federal government easily could afford to provide healthcare insurance to everyone. However, instead of doing this, it offers businesses tax incentives to provide less comprehensive coverage—just enough to keep employees dependent on their jobs for healthcare.

Finally, the same would hold for federally sponsored, living-wage Social Security for everyone, of all ages. The rich make three false excuses:

If given a bare minimum stipend, no one would work because the poor have no ambition. (aka, “Keep ’em poorso they have to accept low-pay jobs and bad working conditions.:”)

And things will have to get much worse before the populace begins to understand how Monetary Sovereignty and Gap Psychology are used against them.

Only a nation of fools would give a tax break to religion but not to science and education.

Economics is filled with myths that might make one think it is taught at Hogwarts School of Witchcraft and Wizardry. A discipline that loves to use statistics often seems to disregard them in favor of intuition and confused semantics.

Monetary Sovereignty is the historical truth that the federal government created the first dollars from thin air through legislation. The government retains the unlimited authority to continue passing lawsand those laws can produce as many dollars as the government desires for any purpose it chooses.

Gap Psychology suggests that the terms “rich” and “poor” are relative. To become richer, one must widen the gap in income, wealth, and power below, while narrowing the gap above. This can be achieved either by increasing one’s own earnings or by reducing others’ earnings.

Currently, the federal government creates dollars by this process:

Congress votes to fund something.

The President approves

Computer keys are pressed

The money is credited to the appropriate accounts.

This means the federal government, being Monetarily Sovereign:

Cannot run short of dollars.

Cannot become insolvent or go bankrupt

Does not need to, and indeed does not, borrow dollars.

Neither needs nor uses tax dollars to pay its obligations

Due to the monetary non-sovereignty of state and city governments, businesses, and individuals, there are many misunderstandings and myths about federal finances.

Federal “debt.” It isn’t what most people know as “debt.” The federal government is not “in debt.” It does not borrow. It does not owe. It merely accepts deposits into U.S. Treasury savings accounts.

Those deposits are owned by the depositor, not by the government. To pay off the “debt,” the government returns the deposits plus interest. Federal taxes and taxpayers are not involved in any way.

The purpose of those accounts is not to provide the government with funds for spending. Instead, those accounts:

Assist the Federal Reserve in managing interest rates by establishing a “base” rate.

Provide a secure location for unused dollars to stabilize and enhance their value.

Here are the most common myths about T-securities deposits (aka “debt”).

1. “The debt is a burden on future generations.” Future generations are not responsible for repaying past federal debt. When Treasury securities are bought, the purchaser deposits dollars into their T-security account. Upon maturity of those securities, the buyer is paid with the dollars in that account. Future tax dollars are not involved in this process.

Future generations will benefit from the government’s interest payments.

2. “The federal government could become insolvent.” Many people believe federal finances resemble a family budget. This comparison is intuitively appealing and for some, politically advantageous.

A monetarily sovereign government creates all the currency it owes. It cannot run out of dollars any more than a scorekeeper runs out of points. It can generate the dollars required to fulfill any obligation.

3. “China ‘owns’ us and can demand repayment.” China holds U.S. Treasuries because it seeks a secure way to save in dollars. It does not have the power to make demands regarding these securities. Repayment occurs only at maturity and involves an electronic transfer from China’s T-security account at the Federal Reserve to other Chinese accounts at the same

4. “Interest will crowd out federal programs.” Paying interest simply credits bank accounts. It doesn’t deplete federal funds; the government creates the funds it pays out. Additionally, paying interest generates dollars for economic growth. Even if the government paid trillions of dollars in interest, it would not affect the government’s ability to fund its programs — not by one penny.

5. “High debt causes inflation.” Federal debt differs from personal debt. It is created when dollars are accepted into Treasury accounts, which are settled at maturity simply by returning those dollars. Inflation is related to resource shortages, not to federal debt.

There is no relationship between federal debt (red) and inflation (green). The peaks and valleys of the two lines differ substantially.

6. “High debt raises interest rates.” The Federal Reserve sets interest rates arbitrarily. Since the federal government does not have a financial need to accept T-security deposits, the demand for these investments does not influence interest rates.

The peaks and valleys of interest rate changes (gold) do not match those of federal debt, indicating that interest rate changes are not associated with changes in federal debt. One even could argue that increases in federal debt lead to lower interest rates.

7. “Our grandchildren will be saddled with the debt.” Every dollar of debt corresponds to a dollar of someone’s savings. Future generations will own both the Treasuries and the interest dollars used to service them. There is no intergenerational burden. The “debt” is not a taxpayer liability.

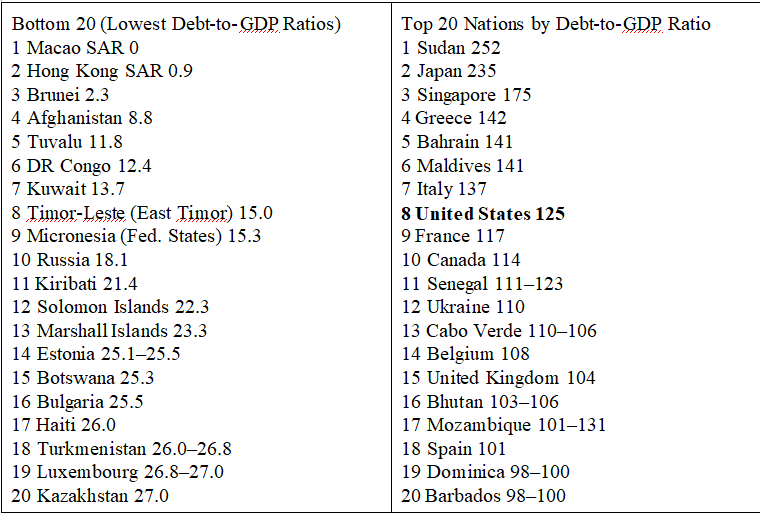

Here are the lowest and highest ratios. By analyzing these ratios, could you determine which nations you would prefer to lend to? Which nations are strongest financially? Which nations are least likely to default?

You can’t, because the Debt/GDP ratio is meaningless.

There is no relationship between the Debt/GDP ratio and financial strength.

9. “Large debt hurts economic growth.” Higher government debt correlates with stronger GDP growth because federal deficits and interest payments add growth dollars to the economy.

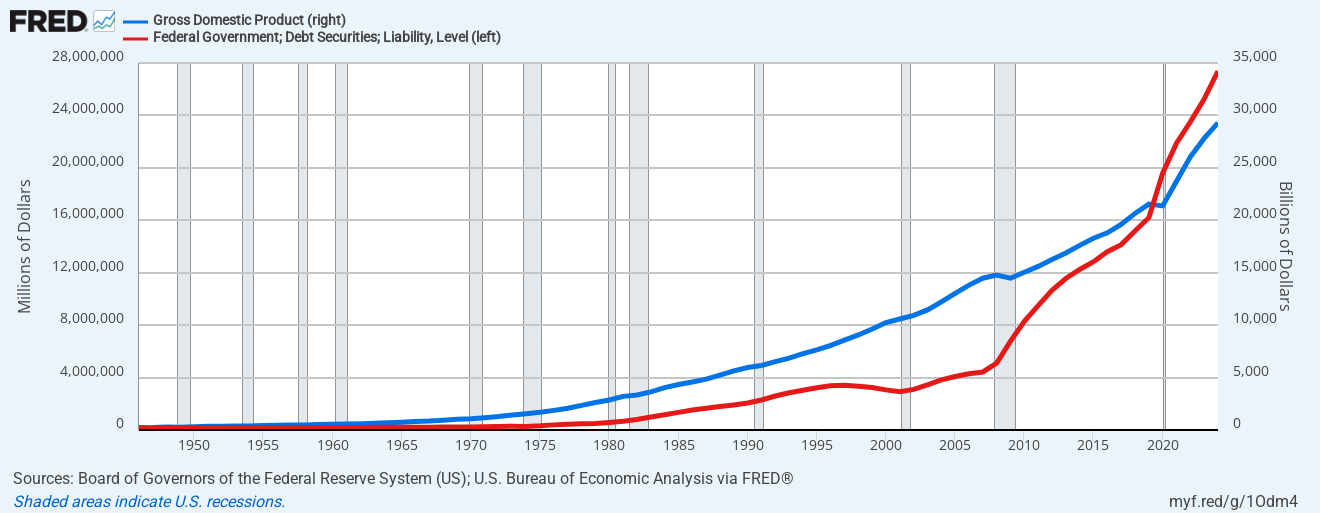

The following graph illustrates the parallel paths of Gross Domestic Product and Federal Debt. This parallelism is not coincidental. The most crucial equation in economics is GDP = Federal Spending + Nonfederal Spending + Net Exports. Federal spending adds dollars to the private sector and is necessary for economic growth.

Federal expenditures and GDP move essentially in parallel.

10. “We must reduce debt so interest payments don’t explode.” Interest payments act as a fiscal stimulus by adding growth funds to the private sector. When interest payments increase, private income also rises.

Our government, as a monetarily sovereign entity, easily manages any level of interest payments.

Interest rates (yellow, dashed line) and GDP (blue) rise and fall together.

11. “It’s irresponsible to let debt grow forever.” The federal debt is the difference between federal spending and revenue. Thus, debt adds growth capital to the economy, allowing for continuous economic growth, which is beneficial.

12. “Eventually, no one will buy our debt.” The Federal Reserve and primary dealers are obligated to purchase Treasury securities; however, the federal government has no financial need for anyone to buy its debt.

The purpose of federal debt is not to provide spending funds to the government. T-securities provide dollar users with a safe place to store unused dollars. The dollar-using world wants the insurance that T-securities provide.

13. “High deficits mean higher taxes later.” Federal taxes do not pay for the federal debt. Instead, the Treasury creates new dollars to cover the interest, and each debt account is settled at maturity by returning the dollars in that account.

Tax rates: The Highest bracket (green dashed line) and the lowest bracket (blue dashed line) are compared with annual changes in federal deficit spending (red). Tax rates have fallen as deficit spending has increased.

14. “We should have a balanced budget.” This means the federal government would not provide additional funds to the economy, which would result in a depression.

Paying down the debt requires running surpluses, which historically have led to depressions. Throughout U.S. history, every depression has been preceded by federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began in 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began in 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began in 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began in 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began in 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began in 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began in 1929. 1997-2001: U. S. Federal Debt reduced 15%. The recession began in 2001.

When federal deficit spending decreases, recessions tend to occur, which are resolved by increasing federal deficit spending. See the following graph:

Every recession (vertical gray bars) followed a decline in federal deficit spending, and all were cured by an increase in deficit spending.

15. “The federal debt is not sustainable.” This is a non-specific false claim encompassing all of the other false claims about federal debt. The term “sustainable” frequently is used by individuals opposed to debt and leaning toward Libertarian views.

However, they seldom clarify why a Monetarily Sovereign nation cannot “sustain” any level of debt, especially when the situation in question isn’t even a debt. (It’s deposits.)

And all the false claims boil down to the one underlying false claim:

16. The government and taxpayers cannot afford Medicare for All, Social Security for all, housing assistance, food assistance, or any other benefits for the middle class and the poor.The federal government, being Monetarily Sovereign, can afford anything without needing taxpayer funds.

Despite the fact that tax loopholes for the wealthy cost the government money, Congress and the President rarely oppose them. The reason: wealthy people are major campaign contributors.

Given this situation, why is Washington hesitant to provide those benefits? Why do we have “debt ceilings” and government shutdown battles over spending?

The answer: Gap Psychology.

The very wealthy still want to become wealthier. It is human nature. To become wealthier, one must widen the income/wealth/power Gap below and narrow it above.

To do that, one must increase one’s own income or decrease the income of others. The rich do both by bribing the most important information sources:

They bribe politicians via campaign contributions and lucrative jobs in “think tanks.”

They bribe economists via university endowments and promises of lucrative jobs and assignments

They bribe the media via advertising dollars and outright ownership

All are expected to promulgate the myths about federal debt so as to reduce or eliminate entirely spending for social services.

That is why it is said that the Social Security and Medicare trust funds are running out of money, when in reality, there are no actual trust funds, and the necessary funds would be available if Congress simply voted for them.

It is why Congress forces the states to fund social programs, knowing that the states are monetarily non-sovereign and often unable to fund programs properly.

SUMMARY

The federal “debt” is not real debt in the traditional sense. It refers to deposits that are essentially repaid by returning them. This process does not impact taxpayers.

The federal government, as a monetarily sovereign entity, does not borrow dollars. Instead, the purpose of this so-called debt (or deposits) is to help the Federal Reserve manage interest rates and provide a safe option for unused dollars, thereby protecting dollar users.

In summary, the federal debt does not threaten the federal government’s solvency nor hinder economic growth. In fact, it serves the opposite purpose.

I’ve researched the question, “What are the reasons against Universal Basic Income (UBI).” I call it “Social Security for All.”

Here is a summary of the anti-UBI claims:

1. Cost and Feasibility: One of the primary concerns is the high cost of UBI. For example, in the United States, a UBI of $12,000 per year for every adult would cost over $3 trillion annually/

2. Inflation: UBI could lead to inflation. If everyone has more money to spend, demand for goods and services might increase, driving up prices and potentially negating the benefits of the additional income.

3. Work Incentive: UBI might reduce the incentive to work. If people receive a guaranteed income regardless of employment, some may choose not to work, potentially leading to a decrease in the labor force and economic productivity.

4. Misuse of Funds: Recipients might misuse the funds, spending them on non-essential items rather than necessities. This could undermine the goal of reducing poverty and improving living standards.

5. Impact on Existing Welfare Programs: Implementing UBI might require cutting or restructuring existing welfare programs. This could harm those who rely on targeted support for specific needs, such as healthcare or housing.

6. Political and Social Challenges: Gaining political and public support for UBI can be difficult. Many people are skeptical of unconditional transfer programs and prefer welfare systems tied to employment or specific conditions.

Before I address #s 1 through 6, I’ll give you the real one:

7. It would narrow the income/wealth/power Gap between the rich and the rest. The Gap is what makes the rich rich. Without the Gap no one would be rich; we all would be the same.

The wider the Gap, the richer are the rich. The easiest way for the rich to remain rich is to make sure the Gap doesn’t narrow, so using their political and informational power, the rich invent and promulgate false reasons why UBI won’t work.

Now, let us address each of the reasons given for objecting to UBI.

1. Cost and Feasibility:

We already have a form of UBI, except it isn’t “U” (Universal). We call it “Social Security,” and it covers old and/or disabled people. All the ideas opposing UBI were put forth in the 1930s when Social Security first was proposed.

Contrary to popular myth, Social Security (as well as Medicare, the military, SCOTUS salaries, White House salaries, Congress’s salaries, and every other federal expenditure) are not funded by FICA or any other federal taxes.

A. When any federal government agency approves an invoice for payment, it sends instructions (not dollars) to the creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account. The instructions are in the form of a check or a wire.

B. When the bank does as instructed ( by pressing a few computer keys), dollars are created by being added to the creditor’s checking account and to the money supply measure known as “M2.”

C. The bank then balances its books by clearing the payment through the Federal Reserve, which has the infinite power to approve all federal checks and wires.

So long as the federal government has the infinite power to pass laws and to issue instructions, it has the infinite power to pay any invoices it receives. The U.S. federal government, being the original creator of dollars from thin air, never unintentionally can run short of dollars.

You often have been told that Medicare, Social Security and/or their trust funds are running out of money. It is a false claim. Unlike state/local governments, the U.S. government is Monetarily Sovereign. With the infinite ability to create dollars, it could create the above-mentioned $3 trillion at the touch of a computer key.

The sole purpose of federal taxes (unlike state/local taxes) is notto provide the government with spending money. The dual purposes are to:

Control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward and

Assure demand for the dollar by requiring taxes to be paid in dollars.

Even if the federal government didn’t collect a single dollar in taxes, it could continue spending, forever.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Mario Draghi, President of the Monetarily Sovereign European Central Bank: “We cannot run out of money.”

Further, UBI would grow the economy. It’s a mathematical certainty because the size of the economy is determined by this formula:

Gross Domestic Product (GDP) = Federal Spending + Nonfederal Spending + Net Exports.

By simple algebra, UBI would grow the economy because it would increase Federal Spending and, as a result, increase Nonfederal Spending, too.

When faced with the undeniable facts that UBI is affordable for the federal government and would grow the economy, those influenced by wealthy propaganda resort to excuse #2.;

2. Inflation: The common yet erroneous belief is that “excessive” fedeal spending causes inflation. This belief is wrong on several fronts.

First, no one knows what “excessive” means. The rich always claim federal spending is excessive (see: Historical claims the Federal Debt is a “ticking time bomb.” From Sept. 26, 1940, to July 22, 2024) because most federal spending goes to the poor. It narrows the Gap, a situation the rich despise.

By contrast, the rich favor tax deductions for the wealthy, which are not part of “spending” but widen the Gap just as federal spending does.

Economics is a pseudoscience loaded with hypotheses and flush with data— and ne’er the twain shall meet.

Some economists make this arguement based on intuition, but not on fact: They claim that people earn income by selling their labor on the labor market as a contribution to the production of goods and services for the economy. Income increases that aren’t directly related to correlating increases in production tend to result in higher prices.

It’s nonsense.

Which of these can claim their income is “directly related to correlatingincreases in production?” Taxi driver? School teacher? Musician? Flight attendant? Doctor? How about Elon Musk? If he made “just $100 million instead of a few billion, would that “directly relate to a correlating decrease in production”?

Pay has little to do with production and more with labor scarcity, politics, heredity, and other social factors. Queen Elizabeth’s pay had little to do with her output. I am retired, and my income has nothing to do with my production. Raising hotel workers’ skimpy pay or decreasing mortgage brokers’ high pay would not “directly relate to their production.”

The hypothesis is something that only an economics professor in a well-endowed think tank could dream up.

Inflation is not caused by federal spending. Inflation is caused by scarcities,most often scarcities of oil and food:

The peaks and valleys of inflation(red) do not match up with the peaks and valleys of federal spending (blue).

The peaks and valleys of inflation do match up with the peaks and valleys of oil prices, which are dictated by oil supply and demand.

Today, the federal government is spending more than ever, yet inflation is drifting down. The most recent inflation was COVID-related, not spending-related.It was caused by shortages of oil, food, computer chips, metal, lumber, shipping, and labor.

Raising everyone’s income by giving them money would not cause inflation. Scarcities of crucial items cause inflation.

Federal spending to cure scarcities cures inflation. The “federal spending causes inflation” meme is a fever dream promulgated by the rich to maintain the income/wealth/power Gap.

3. Work Incentive: Critics argue that UBI might reduce the incentive to work, decreasing the labor force and economic productivity. This is a favorite of the rich, who love to portray lower-income people as lazy slugs who, if given money, will simply loll about doing nothing.

The truth is that poor labor is harder than rich labor unless one considers costly vacations, country clubs, and having servants do one’s work to be “labor.” Virtually everyone wants a better life, and that includes the poor. Given a stipend by the government, they will work to increase their standard of living, just as the rich do.

Similarly, the vast majority of the rich want to be richer. Almost no one is satisfied, and it is certainly not a low-income family that receives Social Security.

I trust this isn’t just a projection on my part, but I began collecting Social Security at age 65. I continued to work for a living until I was 73, not because I loved work, but because I wanted more money to feel secure. I had what some may consider a lot, but I still wanted more.

That said, what is wrong with a decrease in the labor force? What is wrong with a four-day work week or a five-hour day? Work usually is not a purpose unto itself. The primary purpose of most work is to improve one’s life, however one defines “improve.”

For households in every quintile of the income distribution, the share of income required to pay for their 2019 consumption decreased, on average, because income grew faster than prices did over that four-year period.

Households in the top income quintile had the largest decline, on average, in the share of income required to pay for their 2019 consumption.

Translation: The rich kept earning more spending money than the rest of us did. Even though they had plenty of money, they wanted more, and worked for it. Why would the average and below-average income people be less motivated? They wouldn’t, but that is what the rich claim.

Artificial intelligence (AI) and automation are making it more possible to do less and accomplish more. A solution to the possible unemployment caused by AI may be UBI.

4. Misuse of Funds: Some argue that recipients might misuse the funds, spending them on non-essential items rather than necessities. This is another one the rich love — the notion that the poor are ignorant money managers and that if you give them money they’ll waste it on drugs and lottery tickets.

The reality is quite the opposite. By necessity, the poor have learned to be good money managers. In any event, it is none of the government’s business whether or not someone “misuses” their income. The idea the the government knows better is repulsive and bigoted.

5. Impact on Existing Welfare Programs: Implementing UBI might require cutting or restructuring existing welfare programs. Critics worry that this could harm those who rely on targeted support for specific needs, such as healthcare or housing.

This is easily prevented. Just don’t do it. Don’t include UBI income as part of any welfare criterion.

The current system — requiring someone to be poor to receive financial aid — is self-defeating. It encourages the very thing the rich claim to fear: people not working. It also leads to dishonesty and to gaming the system by mischaracterizing income.

6. Political and Social Challenges: Gaining political and public support for UBI can be difficult. Many people are skeptical of unconditional transfer programs and prefer welfare systems tied to employment or specific conditions.

This is the old “If I had to work for my money, why should he get money for doing nothing?” The solution would be to give every man, woman and child in America the same amounts regardless of their other income or wealth.

The money would mean little to the rich and much to the poor, but it would overcome the resistance of those who hate to see others receive something.

7. It would narrow the Gap between the rich and the rest. The Gap is what makes the rich rich. Without the Gap no one would be rich; we all would be the same.

The wider the Gap, the richer are the rich. The easiest way for the rich to remain rich is to make sure the Gap doesn’t narrow, so using their political and informational power, the rich invent and promulgate false reasons why UBI won’t work.

This is the single biggest hurdle to cross. The first six objections easily are overcome and/or are based on incomplete information. This one is based on the intense emotions of America’s most influential people.

A rich man might be generous about charity for the poor, but he doesn’t want poverty to be eliminated altogether. He needs the poor. Having a mansion is not as attractive if everyone else has a mansion. It’s the Gap that makes him rich, and narrowing the Gap makes him less rich, an unappealing prospect.

If a neighbor wins the lottery or even gets a more lucrative job, how does the rest of the neighborhood feel? What does Mark Zuckerberg think about Elon Musk having more money?

The majority of us suffers from Gap Psychology, the desire to distance ourselves from those below us on the income/wealth/power scale and to come closer to those above us. The conflict arises because those above us don’t want us closer and those below us want us closer.

SUMMARY

There are no good reasons not to begin a UBI program and plenty of reasons to start.

I suggest the following monthly payments:

$1,000 to every adult (18+)

$500 to every child

Include undocumented adults and children.

Assume:

258 million adult (citizens) + 31 million adult (non-citizens) = 289 million total adults; Annual Cost: $289 billion * 12 = $3.468 trillion

73 million children (citizens) + 14 million children(non-citizens) = 87 million children; Annual Cost: $43.5 billion * 12 = $522 billion

Combined Annual Cost: $3.468 trillion (adults) + $522 billion (children) = $3.99 trillion per year

This compares to the most recent (2023) federal expenditure of about $6.3 trillion.

Poverty generally is worse in the states that tend to vote Republican, the party that wrongly opposes social benefits, saying they are “unaffordable” and “socialism” — which they are not.

(Socialism is government control of industry, not just government funding. All governments fund things, but relatively few of those things can be called “socialism.”)

Government spending has a multiplier effect on GDP. The multiplier effect measures how much economic activity is generated by an initial amount of the expenditure. Estimates for the fiscal multiplier vary, but a typical range is between 0.5 and 2.0.

With a conservative multiplier of 1.5, GDP would grow about $6 trillion on top of the most recent 28.65 trillion for a new value of $34.65 trillion.

Improve the infrastructure and help cut global warming

And improve the entire American nation’s quality of life by using the brainpower now hampered by a lack of funding

Do all this at no cost to anyone.

Think of it. The United States of America has the power to be the first large nation on earth to eliminate poverty. Millions of men, women, and children could begin to contribute to America’s success.

Too good to be true? No, too good only for those who don’t understand the power of human thought and desire, when funded by Monetary Sovereignty.

Gap Psychology dictates that to achieve superiority, one must claim inferiors and then distance oneself from those claimed inferiors. The greater the distance—i.e., the wider the “Gap,” the greater our superiority.

“Rich” and “poor” are comparatives, not absolutes. For one to be rich, someone else must be poor, or at least poorer.

A person with $100,000 is rich if everyone else has only $100, but he/she is “middle” if everyone else has $100,000. And he is poor if everyone else has $1,000,000.

Getting richer is not simply a matter of increasing one’s ownership of money. If a middle-income person has $100,000 and doubles that to $200,000, he still is “middle” if everyone else rises to $200,000.

Getting richer requires widening the Gap below and narrowing the Gap above. It is the Gap that measures wealth, not the wealth itself.

Gap Psychology describes the desire to widen the Gap below and to narrow the Gap above.

Gap Psychology enters into virtually all aspects of human existence, not only money or wealth. A person with an IQ of 130 is smart unless everyone else has an IQ of 170.

A 21-year-old man who can do 50 chin-ups is strong unless everyone else can do 150. A child who can read at age 4 is considered smart unless every other child can read at age 3. If you can run 100 meters in 9.5 seconds, you are blazingly fast unless you are a cheetah, which means you would be laughingly slow.

Self-improvement does not require improving yourself so long as you can widen the Gap below and narrow the Gap above.

You can be strong and do just two chin-ups if you hang a 300 lb. weight from everyone else’s ankles.

If you force everyone else to wear blindfolds, you can learn to read at age 8 and be considered smart. And if you tie everyone else’s legs together, you can be fast, running 100 meters in 20 seconds.

Figuratively, that is how the rich treat the rest of us to widen the Gap. They falsely claim that the federal government “can’t afford” to provide benefits to the middle and lower classes while accepting tax benefits for themselves.

Gap Psychology even enters into the abortion controversy. The rich can easily obtain abortions and other medical procedures. It is the poor who must suffer from a lack of care. That is a Gap the rich wish to widen.

Gap Psychology leads to bigotry, classes, and the caste system. Here is an excellent summary:

The Foundations of Caste: The Origins of our DiscontentsFor more than half of American history, slavery was the dominant social institution in the South.

Wilkerson argues that even after emancipation, legally sanctioned violence, harassment, and displacement of African Americans remained—and still remains—an existential threat.

According to Wilkerson, these behavioral scripts and socially reinforced biases have become deeply encoded in the American psyche at all levels of society, which unconsciously perpetuates the system.

Her research demonstrates that all caste systems have the eight essential characteristics (Pillars) in common.

Pillar Number One: Divine Will and the Laws of Nature

Hindu cosmology holds that the caste system is an aspect of the birth of Brahma, the supreme god, who created and populated the world out of various parts of his body in a way corresponding to the social functions dictated by the traditional order.

The Judeo-Christian tradition has a contrasting story about the creation of the world’s different races descending from the three sons of the Old Testament patriarch Noah.

The two “good” sons who are rewarded for their honor become the fathers of the Eastern and Western races, while the cursed son, Ham, and his own son Canaan are fated to be people of the South, forsaken by God.

For there to be “good,” there must be “bad.”

All caste systems, religions, and cults (similar to religions but smaller and not as mainstream) identify members as “good” and outsiders as “bad” or lesser in some way.

At the time when Spain and Portugal were beginning their global circumnavigations, the native inhabitants of Africa and India were believed by Europeans to be descendants of the biblical outcasts and thus divinely ordained to suffering and subjugation.

Pillar Number Two: HeritabilityIn India, caste is inherited through the father’s line, whereas the United States has historically determined caste through the mother.

In Judaism, to be Jewish, one must have a Jewish mother. The father can be Jewish or gentile.

Presidents Bush, father and son

Because enslaved mothers had no legal right to their own children, Black birth became a production process for slave labor, as Black children were regarded as valuable, durable commodities.

The major distinction between caste and class, Wilkerson writes, is that caste is predetermined, unchanging, and generationally upheld, whereas class implies an attainmentof certain conditions based on merit and effort and is much more inclusive within its respective caste “container.”

Yet we have the expressions “new” and “old” money, with “old money: considered superior by those whose ancestors were wealthy.

In the United States, the exclusion of African Americans regardless of their level of social or professional success—an exclusion based on superficial, inescapable, inherited characteristics—resembles in practice the treatment of India’s “untouchable” populations.

Pillar Number Three: Endogamy and the Control of Marriage and MatingIt is essential for a caste system to separate and manage bloodlines in a way that preserves the impenetrability of the dominant gene pool by subordinate-caste DNA.

This protects the Gap between white and non-white. Most American parents prefer that their children marry within their religion and color.

To achieve this, miscegenation laws are passed that restrict marriage and reproduction along caste lines, a policy known as endogamy—and something Hitler admired about the American model.

The objective of this kind of social engineering is to achieve racial purity among the dominant caste, but it also concentrates resources, value, and empathy among the various levels of the dominant caste that are systematically denied to non-white subordinates.

America’s racial boundaries had been set from its earliest days, and coupled with the nation’s historic exclusion of non-European immigrants, endogamy laws effectively created a process of selective breeding that reinforced caste divisions while reserving for white men the ownership of Black reproduction.

Pillar Number Four: Purity Versus Pollution

The United States has its own unique system of gradations on a scale of racial purity that defines itself in opposition to an obsession with contamination by genetic material from a perceived inferior bloodline.

Not only was there the so-called “one-drop rule” that defined Blackness and which the Nazis found so extreme, but there was also an elaborate status-defining class subsystem within the subordinate caste based on skin tone and proportion of African ancestry.

Systems like the examples Wilkerson uses all share a rabid aversion to the idea of public spaces and utilities, particularly water and swimming pools, being similarly contaminated not by blood but by mere exposure to the skin, breath, sweat, or even shadow of the subordinate caste.

Hitler and Trump have spoken of those who “poison the blood” of the nation. Hitler primarily (though not exclusively) was talking about Jews.

Trump was talking about non-white immigrants.

Pillar Number Five: Occupational Hierarchy: The Jatis and the MudsillWilkerson returns to the architectural metaphor she introduced in chapter 2 to describe the house’s most important structural element, where the framing meets the foundation, known as a mudsill.

In the segregationist political tradition, the enslaved caste of African American servants and laborers constituted an analogous base to the American social order.

The lowly work they performed for lack of choice was seen as the limit of their capabilities and their purpose for existence, a permanent servile class upon which the American economy was built.

This is part of the belief that the poor are lazy, stupid, and cannot be trusted. It provides an excuse for widening the employment Gap.

It also alludes to benefits given to the poor, i.e., “Who is going to pick up the garbage if we give them money?”

One major difference between the subordinate Americans and Indian Dalit is that while the Indian system has many subdivisions, known as jatis, within each group that determined one’s work, the African American subordinate class has been limited in professional options with few chances to break out except as performers or athletes.

Until recently, even these luminaries were expected to reinforce popular racist stereotypes if they were to be accepted by the dominant culture.

Pillar Number Six: Dehumanization and StigmaIn order to justify the extreme and often violent measures taken to maintain the oppressive status quo, dominant-caste authority invariably engages in a process of dehumanizing subordinate groups.

By denying subordinates equal regard for their virtue, dignity, and suffering, the dominant caste can so diminish subordinates’ humanity as to make them appear mere beasts of burden, pestilent scourges, or puppets on a string, insensitive to pain and humiliation.

The subordinate group thus becomes marked with pariah status, and their punishment is seen as just and moral, commensurate with the perceived bestiality and inhumanity that relegates them to ghettoization and marginalization.

This dehumanizing mindset is inculcated in generations of dominant-caste children who are raised believing in their superiority and entitlement, which desensitizes them to the victimization of others, even in brutal extremes.

Pillar Number Seven: Terror as Enforcement, Cruelty as a Means for ControlWilkerson describes the means necessary for the sustained oppression of an outcast group, which requires only that the members of the dominant class do nothing and remain silent, maintaining a complicity in which the order will thrive.

The image of the dreaded slaver’s whip encapsulates the violence and intimidation deemed necessary to hold the subordinates in their “container,” and the public complicity that allows the brutal enforcement of the order is the result of the racist attitudes bred into the dominant caste since childhood.

The savage business of terror seems like a part of normal life when it is tolerated by the majority of people.

Trump says he will deport a million undocumented immigrants. Imagine the terror these men, women, and children will feel waiting for their lives to be ripped apart when his brown shirts come banging on the door.

1. Ipsos Poll (2013):

30% think most illegal immigrants (with some exceptions) should be deported.

23% believe all illegal immigrants should be deported.

Only 5% believe all illegal immigrants should stay legally, and 31% want most illegal immigrants to stay.

2. Pew Research Center (2021):

25% of adults say undocumented immigrants should not be allowed to stay legally, advocating for national law enforcement efforts to deport them.

3. Harris Poll (2024):

Half of all Americans favor mass deportation of people who are illegally in the U.S.

Pillar Number Eight: Inherent Superiority Versus Inherent Inferiority

Wilkerson uses old Hollywood as an example of a cultural force that helped perpetuate popular stereotypes about African Americans’ inferiority and contributed to the same majority mindset that tolerated Jim Crow cruelty and injustice.

In the South, law and custom dictated at all levels of interaction between white and Black citizens that white people enjoy unquestioned superiority, while Black people were expected to treat the dominant caste with false deference and submission.

The consequence for African Americans is that these constant reminders from almost every aspect of American culture reinforce the generational effect of believing oneself inferior, resulting in defeatism and despair.

The eight pillars can be found not only in castes but in religions and cults.

Divine Will and the Laws of Nature

Heritability

Endogamy and the Control of Marriage and Mating

Purity Versus Pollution

Occupational Hierarchy: The Jatis and the Mudsill

Dehumanization and Stigma

Terror as Enforcement

Cruelty as a Means for Control, and Inherent Superiority Versus Inherent Inferiority

Look back at #1 through #8 and visualize religions and cults in America. They all implement some forms of the pollars, and all are related to Gap Psychology.

Gap Psychology is expressed secretly and overtly in various ways: Fear, hatred, disgust, avoidance, fanaticism, and the desire to inflict pain.

We each belong to groups that we view as extensions of ourselves. We find ways to view our groups as superior to others, which helps us feel superior.

These groups range from families to sports teams, cities, states, countries, political parties, tribes, social groups, religions, and cults.

Why is this so important to them? Gap Psychology

If our group “wins,” however that is defined, we win. And, if other groups “lose,” we win.

Personal note: In my younger days, I was a Chicago Bears football fan. I was nervous watching their games because winning meant so much. Finally, in 1985, they won a Super Bowl.

Crowds of screaming Bear fans clogged downtown Chicago. Logically, I had gained nothing, but I felt I had won. Gap Psychology is not based on logic.

When Donald Trump claims, against all evidence, that he won, MAGAs believe.

They disbelieve the 64 lawsuits he lost, the women who claim he attacked them, the criminality of Trump U. and the Trump Foundation, the many convicted criminals he surrounds himself with, and a trial’s 30+ criminal convictions.

To them, the evidence against Trump proves that someone else has committed crimes. (His attempts to overturn the election constitute the proofthe election was stolen.)

That is an outcome of Gap Psychology. When Trump is compared to God, a huge branch of Christianity believes, because when your leader is Godlike, the superiority Gap between you and the non-believers widens.

Gap Psychology is not logical, but it is the single, most important factor ruling our lives. Centuries from now, if we encounter another intelligent species, we will wish to dominate them or fear they will dominate us.

opposition to an obsession with contamination by genetic material from a perceived inferior bloodline.

opposition to an obsession with contamination by genetic material from a perceived inferior bloodline.

/cdn.vox-cdn.com/uploads/chorus_asset/file/13649459/1074706918.jpg.jpg)