Once again, the so-called “debt ceiling” is in the news. The Republicans, who traditionally favor limiting federal spending, now support increasing it. The Democrats, who traditionally favor increased federal spending, now advocate for limiting it.

So, as of this writing, we are headed toward a stalemate, which threatens America’s economy.

The Basic Problem: Inflation

Money was created as a store of value and a medium of exchange. It is the basis of economics.

The earliest form of “standard money” appeared between 3000 and 2000 BCE in Mesopotamia, among the Sumerians and Babylonians. They utilized silver, measured by weight in shekels, as a standard of value for trade and record-keeping, even before the invention of coins. In Egypt, grain, metals, and other commodities served as units of account.

By around 2500 BCE, a form of money as a unit of account and medium of exchange was already in use.

Since then, nations have faced recessions, depressions, and stagflation; however, the primary concern in economics is inflation—the decrease in the value of a nation’s currency.

Money is an artificial construct of value. A dollar bill is simply printed paper, just like a check. Neither possesses intrinsic value, and both can be easily created. The concern is that creating too much money will lead to a reduction in its value.

To prevent inflation, governments try to limit their ability to create money.

Gold and silver are permanently available in physical form and somewhat scarce, so linking money to these elements (gold and silver standards) was a means of restricting the creation of money.

Gold Standard and the Debt Limit

The debt limit serves as a modern equivalent to the historical gold standard. While the two concepts have different impacts, both aim to limit the government’s ability to create money.

If not for the fear of inflation, neither a gold standard, a silver standard, nor a debt limit would have been invented.

Under a gold standard, each unit of currency (dollar, pound, franc, etc.) was pegged to a fixed weight of gold. The U.S. Gold Standard Act of 1900 set 1 troy ounce of gold to be equal to, $20.67. People could, in theory, redeem paper money for gold at that fixed rate.

The government couldn’t create new money freely; it had to maintain sufficient gold reserves to back it.

If a government runs large deficits and needs to spend heavily, it risks losing gold reserves because creditors or foreign nations might demand repayment in gold. Additionally, “breaking the peg” could trigger panic, bank runs, and a loss of confidence.

In practice, deficit spending was tightly constrained by gold holdings. Countries often had to raise interest rates, cut spending, or deflate their economies to protect reserves.

Gold standards and other physical currency pegs limit economic growth. This limitation is both their purpose and their shortcoming.

When the economy grows faster than the supply of gold, it leads to deflation, meaning there isn’t enough money relative to the amount of goods available. Moreover, if gold is depleted—such as when it’s sent overseas to cover trade deficits—countries are forced to reduce credit and spending, even during recessions.

This is why the gold standard worsened the Great Depression: the U.S. and Europe focused on defending gold reserves instead of stimulating their economies.

The U.S. suspended gold convertibility for domestic purposes in 1933.

Following World War II the Bretton Woods system was established, which pegged various currencies to the U.S. dollar. The dollar, in turn, was pegged to gold at a rate of $35 per ounce.

In 1971, President Nixon ended gold convertibility by “closing the gold window.” Since that time, the U.S. dollar has become fiat money, meaning it is not backed by any physical commodity but rather by U.S. law and the “full faith and credit” of the U.S. government.

The years spent dealing with the challenges of the gold and silver standards have ultimately been in vain. Today, inflation is no greater a problem since those standards have been abolished. Additionally, we have not experienced a depression since the end of the gold standard.

The debt ceiling is a legal limit set by Congress on the total amount of money that the U.S. Treasury can borrow to fulfill existing obligations.

The stated purpose is to control borrowing. It was originally intended (in 1917, with expansion in 1939) to give Congress oversight of federal borrowing while allowing the Treasury to issue debt without constant, individual approval.

Supporters claim it forces Congress to confront federal deficits and spending levels. Also, it allows legislators to make a public statement about debt, deficits, or fiscal responsibility.

In reality, the debt ceiling does not control new spending. Rather, it restricts the payment of existing obligations. Spending levels and taxes are set by Congress through separate budget and appropriations laws. Once those laws are passed, the Treasury is obligated to pay the bills.

The debt ceiling creates a risk of default. Once the ceiling is reached, the Treasury cannot issue new debt, even though it must meet legally required obligations such as Social Security, interest on the debt, Medicare, military pay, and contracts. This situation forces the use of “extraordinary measures,” and if it continues for too long, it could lead to a U.S. default.

Additionally, the debt ceiling has become a political tool. In recent decades, political parties have used debt ceiling votes to advance unrelated policy goals.

Most economists view the debt ceiling as economically unnecessary and politically hazardous. It does not actually limit future debt, as spending and tax laws determine that. Instead, it introduces an unnecessary risk of default that can destabilize markets and increase U.S. borrowing costs.

The United States is unique in having a separate debt limit; few other advanced economies impose such a restriction, as they allow borrowing to flow automatically based on budget decisions.

In summary, while the stated purpose of the debt ceiling is to promote fiscal restraint, its actual effect is often a result of political posturing that can have serious economic consequences.

Major Debt Ceiling Crises

Congress raised the debt ceiling several times during President Eisenhower’s presidency.

Even then, this effort has been more about political strategy than actual debt control. While Republicans have aimed to project a fiscally more conservative image, the ceiling continued to rise under both parties.

1979 – “Technical Default”: A clerical error, plus temporary cash-flow issues, caused a brief delay in paying Treasury bills. Investors demanded higher yields afterward—showing even the hint of default costs taxpayers.

1995–96 – Clinton vs. Gingrich: The Republican House, led by Speaker Newt Gingrich, refused to raise the ceiling without big spending cuts. Result: Two government shutdowns. The ceiling was eventually raised with no major long-term cuts.

2011 – Obama vs. House Republicans: The Republicans refused to raise the ceiling unless Obama agreed to major deficit reduction. Outcome: The U.S. came within days of default. The “Budget Control Act” imposed automatic spending caps (sequestration).

S&P downgraded the U.S. credit rating for the first time in history due to political dysfunction. As a result, stock markets fell and borrowing costs rose.

2013 – Obama Again: Another showdown over Obamacare and spending. The Treasury used “extraordinary measures” for months. The ceiling finally was suspended—but markets were rattled, with short-term Treasury yields spiking.

2013 – Obama Again: Another confrontation over Obamacare and spending. The Treasury employed “extraordinary measures” for several months. The ceiling was ultimately suspended, but markets were unsettled, causing short-term Treasury yields to spike.2013 –

2019 – Trump: A bipartisan deal suspended the debt ceiling for two years. Republicans largely dropped opposition to debt increases when they controlled the White House.

2021–2023 – Biden Era: Republicans initially refused to raise the ceiling; Mitch McConnell allowed a temporary extension at the last minute.

2023: With Republicans controlling the House, Speaker Kevin McCarthy negotiated a deal with Biden. The deal capped some discretionary spending growth for 2 years. Treasury had been within days of running out of money.

Notice the pattern? The stated purpose always is to “control debt and deficits,” but the actual outcome is that the debt ceiling always is raised or suspended (78 times since 1960), the so-called “debt” continues to rise, and the economy continues to grow.

Meanwhile, the side effects are market turmoil, higher borrowing costs, political theater, and in 2011, a credit downgrade.

Other advanced countries do not have this issue. In those countries, borrowing authority is automatically granted through the budget process.

The U.S. debt ceiling is unique because it creates artificial crises without altering fiscal reality.

Even the fundamental beliefs are wrong.

I. The Federal Government Does Not Borrow Dollars.

Federal finances are not like personal finances.

The federal government uniquely is Monetarily Sovereign. It has the unlimited ability to create dollars simply by pressing computer keys. It never unintentionally can run short of dollars.

Even if the federal government collected $0 taxes, it could continue spending trillions upon trillions of dollars, forever.

The notion that the government “borrows” comes from the semantic misunderstanding of the words “notes.” “bills,” and “bonds.” In the private sector, those words signify debt. But in the federal sector, they merely are forms of money, like “dollar bill” and “federal reserve note.”

II. Federal Deficit Spending Is Necessary for Economic Growth

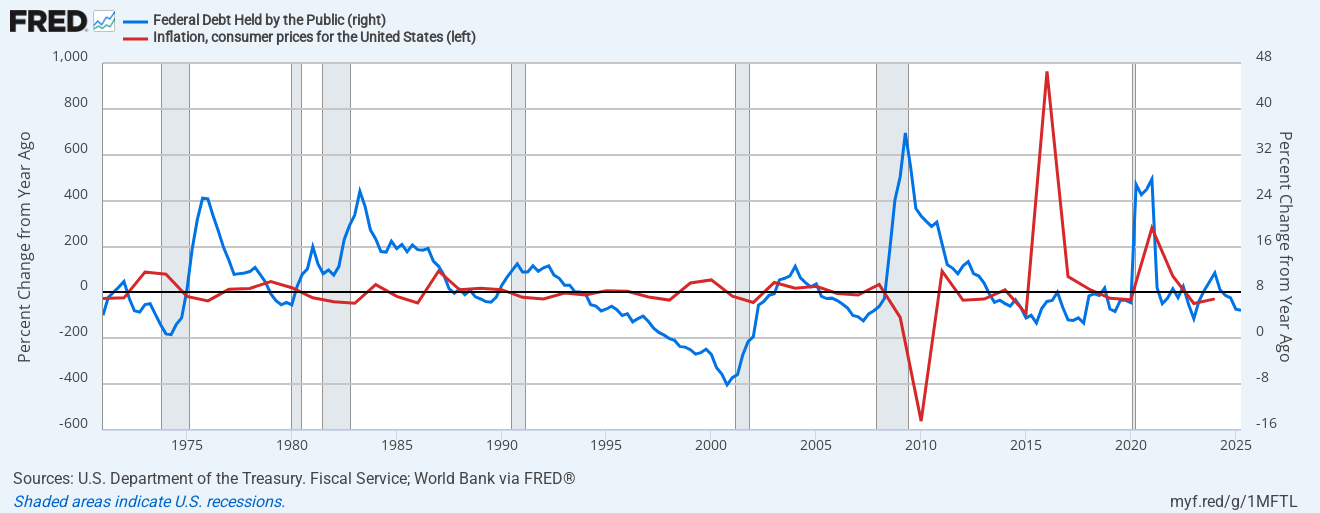

Reductions in federal deficits lead to recessions (vertical gray bars). Recessions are cured by increased federal deficits.

Federal deficits inject growth capital into the economy. While the federal government has unlimited currency, the economy needs a steady inflow of dollars for expansion.

Over the years, as federal deficits have increased, the Gross Domestic Product has also risen.

If federal deficits were economically harmful, one would not expect to see the graph above, which shows the economy’s growth paralleling the growth of deficits.

The reason is clear. GDP=Federal Spending + Nonfederal Spending + Net Exports.

III. Federal Deficit Spending Does Not Cause Inflation

You may have heard that inflation is too much money chasing too few goods and services. You’re about to learn that it simply is not true.

Question:Does massive federal spending cause inflation?

First, let us answer the intermediate question: Can our Monetarily Sovereign federal government massively spend without raising taxes?

Alan Greenspan, former Federal Reserve Chairman: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke, former Federal Reserve Chairman: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishesat essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Jerome Powell, Federal Reserve Chairman: “As a central bank, we have the ability to create money digitally.

St. Louis Fed, in their publication titled “Why Health Care Matters and the Current Debt Does Not”:

“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit marketsto remain operational.”

Paul O’Neill, former Secretary of the Treasury: “I come to you as a managing trustee of Social Security. Today, we have no assets in the trust fund. We have promises of the good faith and credit of the United States government that benefits will flow.”

Mario Draghi, former president of the (Monetarily Sovereign) European Central Bank, asked, “Can the ECB ever run out of money?”

Mario Draghi: Technically, no. We cannot run out of money.

Paul Krugman, Nobel Prize–winning economist: “The U.S. government is not like a household. It literally prints money, and it can’t run out.”

Hyman Minsky, Economist: “The government can always finance its spending by creating money.”

Eric Tymoigne, Economist: “A sovereign government does not need to collect taxes or issue bonds to finance spending. It finances directly through money creation.”

Three Federal Reserve Chairmen, the Secretary of the Treasury, the President of the European Central Bank, and three economists agree that the Monetarily Sovereign U.S. can never run short of dollars. This means it can always pay all its debt without borrowing or taxing.

Warren Mosler (MMT Founder): “Federal taxes don’t pay for anything. They function to remove money from the economy. The government doesn’t need taxes to spend—it taxes after spending to manage demand.

Frank Newman (Former Deputy Secretary of the U.S. Treasury): “The government creates money when it spends. Taxes are just a way to remove money.”

Stephanie Kelton (Economist, former Senate Budget Committee Chief Economist): “The U.S. government is not like a household. It is the issuer of the currency. It doesn’t need to ‘get’ money from anyone else—not from taxpayers, not from China.”

James Galbraith (Economist, advisor to Congress): “The U.S. government spends money into existence. It does not need to collect taxes to spend.”

Federal deficits and debt (i.e., the total of deficits) are not burdens on the federal government.

Concerns about the size of a federal deficit or the federal debt are misplaced. The federal debt, no matter how large, never is a burden on the government or on taxpayers.

Even if federal tax collections fell to $0, the government could continue spending forever. Think about this the next time someone says Medicare and Social Security are running short of money. This cannot happen unless Congress and the President want it to.

Why then does the government collect taxes, if not to pay for spending:

To control the economy by taxing what it wishes to discourage and by giving tax breaks to what it wishes to reward.

To assure demand for the U.S. dollar by requiring taxes be paid in dollars.

All those articles you read and speeches you hear expressing horror at the size of a federal deficit or the U.S. debt result from ignorance or an attempt to mislead you.

Federal deficits and debt are necessary to grow the economy. When the federal government runs a deficit, it pumps growth dollars into the economy.

Recessions occur when deficits are too small for economic growth.

Recessions (vertical gray lines) immediately follow declines in federal deficit spending growth. Recessions are cured by increases in federal deficit spending growth.

Federal deficit spending adds growth dollars to the economy. Rather than calling it a “federal deficit,” it should be called an economy’s surplus.

This brings us to the central question: Does massive federal spending cause inflation?

Here are the inflations that have occurred since 1940, the start of World War II

U.S. Inflations Since 1940 — Causes Explained

1941–1947, Inflation Peak: ~20% in 1947

Cause: World War production and rationing replaced production for the economy, causing shortagesof oil, food, rubber, steel, and other war goods.

Consumer goods were scarce.

The inflation was not caused by “too much money” but by total war mobilization stretching supply chains.

1950–1951 – Korean War Inflation Inflation Peak: ~9% in 1951

Cause: Sudden demand surge for military goods. Civilian supply shortages as factories shifted to war production.

Another classic case of resource reallocation causing shortages.

1966–1969 – Vietnam War + Great Society Buildup Inflation Peak: ~6% by 1969

Cause: High military spending. Shortages of labor created wage/price pressures. Fed kept rates too low, allowing demand to overrun capacity.

1973–1975 – First Oil Shock Inflation Peak: ~12% in 1974

Cause: OPEC oil embargo caused energy shortages. Gasoline, transportation, and heating costs soared. Knock-on effects on food prices and shipping. Classic inflation from a shortage of a critical resource—oil.

1979–1981 – Second Oil Shock + Supply Constraints Inflation Peak: ~14.8% in 1980

Cause: Iranian Revolution disrupted oil supply. Ongoing energy bottlenecks from the 1970s. Rising wage expectations and commodity prices. Again, a supply-side crisis, not monetary excess.

1990 – Gulf War / Oil Price Spike Inflation Peak: ~6% in 1990

Cause: Oil price spike due to Iraq’s invasion of Kuwait. Temporary, short-lived inflation driven by energy costs. Again, a supply-side external shock—oil.

1992–2019 – Low and Stable Inflation

Cause: Globalization, technology, slack labor markets, and stable commodity supply kept inflation low. Despite massive federal deficit spending, the Fed met its 2% inflation target (or missed below it) for most of this era. No notable inflation episodes for ~30 years because there were no serious shortages.

2021–2022 – Pandemic Inflation Inflation Peak: ~9.1% in June 2022

Cause: COVID-19 supply chain disruptions. Labor shortagesand shipping bottlenecks. Oil/gas price surge from Russia–Ukraine war. Housing and car shortages(semiconductors, construction delays). Not simply “too much stimulus”—inflation started after supply chains snapped, not when money was spent.

2023–2025 – Disinflation (Monetary Sovereign view fits here: shortage-driven, not money-driven.Inflation Falling)

Inflation has been falling steadily, despite continued government spending. Supply chains have recovered, and energy prices normalized. A strong example of how inflation eases when shortages ease—even with ongoing deficits.

There is no relationship between federal deficit spending (green) and inflation (red). Deficit spending does not cause inflation.

However, there is a strong relationship between an oil shortage and inflation.

Oil prices respond quickly to oil shortages, and because oil prices affect all other pricing, oil shortages cause inflation.

While oil shortages are important, shortages of other products can also affect inflation: Other energy sources, food, transportation, steel, lumber, labor, housing, and computer chips all contribute to inflationary pressure.

And it’s not only in America. Here are a few foreign hyperinflations and their causes:

Weimar Germany (1921–1923)

Cause: War reparations from the Treaty of Versailles had to be paid in foreign currency. The shortage of foreign currency plus shortages caused by the loss of industrial capacity in the Ruhr region after French and Belgian occupation.

Zimbabwe (2007–2008)

Cause: The land reform program disrupted agricultural production, especially of tobacco and maize, key exports.

There was a massive drop in food and export production. Severe shortages of food and essential goods caused inflation to spiral.

Hungary (1945–1946)

Cause: After World War II, Hungary’s infrastructure and economy were destroyed, leading to shortages of goods, services, and production capacity.

Yugoslavia (1992–1994)

Cause: War and sanctions after the breakup of Yugoslavia led to the loss of industrial output and massive shortages.

Venezuela (2016–present)

Cause: The collapse of oil production and exports, which were the main source of foreign exchange. The import-dependent economy faced extreme shortages of food, medicine, and goods.

In every case, shortages caused prices to rise.However, rather than address the scarcities, the governments printed currency, which gave the illusion that the currency caused inflation.

SUMMARY

While “excessive federal spending” is often blamed for inflation, the data do not support that common belief.

The data show that inflation is caused by shortages and is cured by addressing them.Printing currency merely pours gasoline on the fire that would be quenched by removing the fuel—the shortages.

So the next time you read or hear that the federal debt or deficit is too big, write or ask the authors to show you proof. If they say that Germans pushed wheelbarrows filled with money or merely claim that Zimbabwe is an example, show them this article and see if they can pick it apart.

Inflation is most definitely not “too much money” chasing anything. Inflation is too few goods and services. Cure the shortages, and you cure the inflation.

LUTNICK, magically GDP changes to the numbers we want. We simply change the definition

When a Trump appointee realizes the facts contradict his boss, he either misrepresents the facts or hides them.

The facts are the facts. They never change, but for a Trumper, it’s the perception, not any fact, that matters.

Thus, when Trump claims Ukraine invaded Russia, the lie doesn’t change the facts. But Trump and his MAGAs care only about public perception.

The economy is measured by a statistic known as Gross Domestic Product (GDP), calculated using the formula: Federal Spending + Non-federal Spending + Net Exports.

In the U.S., the National Bureau of Economic Research (NBER)—a nonprofit, nonpartisan organization dedicated to economic research—determines when we are in a recession by examining indicators of prolonged economic decline across various sectors.

It analyzes data points including real income, which reflects individuals’ purchasing power after adjusting for inflation; employment levels; industrial production output; wholesale and retail sales; and gross domestic product (GDP).

Mathematically, imposing high tariffs on imports, while deporting millions of workers and consumers, must raise prices and decrease GDP. Neither of these is a hypothesis or a prediction. It is a statistical certainty.

When GDP declines over several months, it is referred to as a “recession.” Conversely, when GDP decreases significantly and/or extensively, it is known as a “depression.”

Trump’s advisors must have realized that Trump’s plan to levy import duties and cut federal spending must result in inflation and recession or depression.

Rather than trying to correct Trump’s flawed policies, and actually prevent the depression, MAGAs prefer to change the measure.

Imagine selling a 2,000-square-foot house and wanting to tell the buyer it’s bigger than 2,000 square feet. Instead of physically enlarging the house, you simply change the measurement and decide that from now on, a foot will be eight inches long.

So your 2,000 foot house suddenly would be listed as 4,500 square feet. The house didn’t change, but by arbitrarily changing the measure, you could claim it was bigger.

Sounds ridiculous, even fraudulent, doesn’t it? But that is exactly what the Trump administration wants to do with GDP, in a futile effort to hide the inevitable recession and depression.

“A more accurate measure of GDP would exclude government spending,” Musk wrote on his social media platform. “Otherwise, you can scale GDP artificially high by spending money on things that don’t make people’s lives better.”

Is Musk asserting that federal spending on bridges, roads, dams, flight control, disaster recovery, anti-poverty efforts, medical research and development, Social Security, Medicare, Medicaid, and countless other initiatives the government undertakes to enhance our lives “doesn’t create value for the economy”?

That’s such nonsense.

Due to Musk’s budget cuts, GDP will decline. This presents a significant issue that Musk is well aware of. He is scared silly that when people see the decrease in GDP, they will accurately conclude that he is responsible for causing a recession.

The argument as articulated so far by Trump administration officials appears to play down the economic benefits created by Social Security payments, infrastructure spending, scientific research and other forms of government spending that can shape an economy’s trajectory.

“If the government buys a tank, that’s GDP,” Lutnick said Sunday. “But paying 1,000 people to think about buying a tank is not GDP. That is wasted — inefficiency, wasted money. And cutting that, while it shows in GDP, we’re going to get rid of that.”

Is Lutnick paid to come up with such a nonsense objection? His salary could be considered a waste of money. Thinking about war strategy is as important as building tanks.

The Commerce Department’s Bureau of Economic Analysis published its most recent GDP report on Thursday, showing that the economy grew at an annual rate of 2.3% in the final three months of last year.

The economy will drop like a stone under Trump, no matter how hard he tries to fake the numbers. While he remains in office, we will fall deeper and deeper into a depression.

The report makes it possible to measure the forces driving the economy, showing that the gains at the end of last year were largely driven by greater consumer spending and an upward revision to federal government spending related to defense.

Still, the federal government’s component of the GDP report for all of 2024 increased at 2.6%, slightly lower than overall economic growth last year of 2.8%.

Thus, even eliminating Federal Spending from the GDP equation won’t save Trump. His economy is doomed and everyone will know it. Fudging the figures won’t save him.

Lutnick’s false claim that federal spending doesn’t “make people’s lives better” is evident. Cutting federal spending will reduce personal income.

The government is not always a contributor to GDP and can subtract from it, which is what happened in 2022 as pandemic-related aid expired.

Lutnick said that the Trump administration would balance the federal budget with spending cuts, saying that would help growth and reduce the interest rates paid by consumers.

Historically, balancing the federal budget has led to depressions.

“When we balance the budget of the United States of America, interest rates are going to come smashing down,” Lutnick said. “This is going to be the best economy anybody’s ever seen. And to bet against it is foolish.”

Under Biden, the economy grew massively. Under Depression Don Trump it will sink. My advice: Do what I have done. While Depression Don remains in office, convert a significant part of your asset portfolio to Treasuries.

Mitchell’s laws: The more budgets are cut and taxes inceased, the weaker an economy becomes. Austerity = poverty and leads to civil disorder. Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

This is an update of a post that ran in 2009.

Kermit the frog famously said, “It isn’t easy being green.” It also isn’t easy convincing people that traditional economics not only is hypothetically wrong, not only is factually wrong, but is wrong to such a degree it is extremely harmful to our economy.

The more extreme debt hawks believe the U.S. federal government should run a balanced budget or even have no debt at all. The more moderate debt hawks feel some debt may be necessary at times, but to them, federal debt is like bitter medicine you take only when absolutely necessary.

All debt hawks, whether extreme or moderate, are long on twisted “facts” but short on evidence.

Their “facts” inevitably include federal deficit and debt measures, projections for the future, debt/GDP ratios, and spending on Medicare and Social Security.

However, when they interpret the facts, they provide no evidence that their interpretations reflect reality.

By contrast, here are facts and a few opinions, which you may interpret for yourself.

1. Fact: Money is the way modern economies are measured. By definition, a large economy has a larger money supply than does a small economy. Therefore, a growing economy requires a growing supply of money. QED

The graph below shows the essentially parallel paths of GDP vs. perhaps the most comprehensive measure of the money supply, Domestic Non-Financial Debt:

One could argue that money begets production or that production begets money, and both would be correct. The point is that money supply (i.e. debt) and GDP go hand-in-hand. Reduced debt growth results in reduced economic growth.

Gross Domestic Product = Federal Spending + NonFederal Spending + Net Exports.

Thus, by formula, a cut in federal spending cuts GDP.

2. Fact: All money is debt and all financial debt is money. In addition to being state-sponsored, legal tender, there are four criteria for modern money:

–Monetarily Sovereign money must be defined in a standard unit of currency.

–MS money has no, or limited, intrinsic value.

–The demand for money is determined by its risk (danger of default or devaluation, i.e., inflation) and its reward (interest rates).

–To have value, money must be owned by an entity other than the entity that created it.

The above criteria describe many forms of money, including currency, bank accounts, T-securities, corporate bonds, and money markets. All forms of money are debt, and a growing economy requires a growing supply of debt/money.

2.a. Fact: Federal “deficit” is a statement of the net amount of money the federal government has created in one year. Opinion: The word “deficit” is pejorative. A more neutral description would be money “created” or “added,” as in, “The government has created $1 trillion,” or “The government has added $1 trillion to the economy.”

Compare the psychological meaning of those statements with the current phrasing, “The government has run a $1 trillion deficit.”

3. Fact: U.S. depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

4. Fact: Recessions tend to follow reductions in federal debt/money growth (See graph below), while debt/money growth has increased when recessions are resolving.

Taxes reduce debt/money growth. No government can tax itself into prosperity, but many governments tax themselves into recession.

Recessions repeatedly come on the heels of deficit growth reductions, and are cured with deficit growth increases.

5. Fact: On August 15, 1971, the federal government gave itself the unlimited ability to create debt/money by completely abandoning the gold standard. This ability is called Monetary Sovereignty.

Because the federal government now has the unlimited ability to create dollars, it neither taxes or borrows in order to obtain dollars. It simply creates them ad hoc. Tax dollars are destroyed upon receipt.

When you pay your taxes, you take dollars from your checking account. These dollars were part of the M2 money supply measure.

When they reach the Treasury, they cease to be part of any money supply measure. They effectively are destroyed. To pay its bills, the federal government creates new dollars, ad hoc.

6. Fact: Federal “debt” is the total of outstanding Treasury Securities. Here is how Treasury Securities, incorrectly termed “borrowing” come into existence.

–You tell the government to debit your checking account and credit your Treasury security account by the same amount. The process is similar to transferring money from your checking account to your bank savings account.

To “pay off” the Treasury Security, the government simply debits your T-security account and credits your checking account.

Thus, the government could pay off all its so-called “debt” tomorrow simply by debiting all T-security accounts and crediting the T-Security owners’ checking accounts.

The entire process neither adds nor subtracts money from the economy (but for interest paid).

Our Monetarily Sovereign government does not borrow the money it has already created but rather exchanges one form of U.S. money (T-securities) for another (dollars). The entire “borrowing” process is nothing more than an asset exchange.

Do T-securities have any benefit? Yes, federal interest payments add to the money supply, an economically stimulative event. Federal interest payments help the government control interest rates and the dollar’s value. (The higher the interest, the greater the value of the dollar, and the more the economy receives in growth dollars.)

The most important purpose of T-securities is to provide a safe place to store unused dollars. This stabilizes the dollar while increasing its value.

T-securities (debt) are not functionally related to the difference between taxes and spending (deficits). They are related only by laws requiring the Treasury to create T-securities in the amount of the deficit.

The Treasury can create T-securities (debt) without a deficit, and the government can run a deficit without creating T-securities. Federal debt is not functionally the total of federal deficits.

The federal government could pay off the entire so-called “debt” today, merely by returning the dollars to the T-security depositors.

7. Fact: Federal taxes, as a money-raising tool, are unnecessary, harmful and futile:

— unnecessary because since 1971 (when the U.S. government became fully Monetarily Sovereign), the government has had the unlimited ability to create money without taxes,

— harmful because taxes reduce the money supply, which reduction leads to recessions and depressions, and

–futile because tax money sent to the government is destroyed upon receipt by the U.S. Treasury.

When you send taxes to the government, you are sending M2 dollars, but when they reach the Treasury, they cease to be part of any money supply measure. They effectively are destroyed.

Our Monetarily Sovereign government does not store dollars for future use. It can create unlimited dollars ad hoc by paying bills.

The so-called “debt” merely accounts for the total outstanding T-securities created out of thin air by the federal government.

The government decides to create T-securities equal to the deficit, but this requirement became obsolete in 1971 when we went off the gold standard and became Monetarily Sovereign.

Today, the federal government creates money by spending, i.e. it credits checking accounts to pay its bills. This crediting of checking accounts adds dollars to the economy.

The federal “deficit” is the net money created in one year and the federal “surplus” is the net money destroyed in one year. In short, deficit spending creates money and taxing destroys money. If taxes fell to $0 or rose to $100 trillion, this would not affect by even one dollar, the federal government’s ability to spend.

Further, (opinion)all tax (money-destroying) systems are unfair. See: http://rodgermitchell.com/FairTaxes.html. For a country with the unlimited power to create money, spending is not related in any way to taxing.

8. Fact: Contrary to popular myth, there is no post-gold standard relationship between federal debt and inflation. (See graph, below)

Also, contrary to popular myth, inflation is not caused by “excessive federal spending.” Inflation is caused by shortages of crucial goods and services, most often oil and/or food. (See the graph, below)

In this regard, hyperinflations are not caused by “money-printing,” but rather by shortages. So-called “money printing” (ala Zimabwe and Germany), were the governments’ response to hyperinflation, not the cause.

The Zimbabwe inflation was caused by food shortages. (The government stole land from farmers and gave it to non-farmers.) Money “printing” was the faulty response to inflation, not the cause.

The most recent inflation was caused by COVID-related shortages of oil, food, shipping, computer chips, metal, housing, lumber, and labor, among other things. As the shortages have been reduced, so has the inflation.

WWII Context: During World War II, many consumer goods were in short supply because production was focused on the war effort. When the war ended, the supply of goods resumed, and the previously unmet demandwas suddenly able to be fulfilled.

Oil Crises: Similarly, during the oil crises of the 1970s, the reduced supply of oil caused prices to spike, not because of a sudden increase in demand, but because the existing demand couldn’t be met.

COVID-19 Pandemic: Supply chain disruptions and production bottlenecks during the pandemic created shortages in various goods, leading to price increasesonce supply constraints eased and the pent-up demand was met.

While the underlying demand might have been consistent, the ability to fulfill that demand was constrained by supply issues. When supply bottlenecks were removed, the previously suppressed demand could finally be expressed, leading to price increases.

Latent Demand: The concept of latent demand suggests that consumers’ desire for goods remains constant, but it is the availability of those goods that fluctuates.

Supply Constraints: Supply-side constraints create temporary mismatches between demand and supply, leading to inflationary pressures once those constraints are lifted.

Observing changes over time can reveal the true causes of economic phenomena. By examining what happens just before and during an inflationary period, we often find that supply-side disruptions are the primary drivers.

Gradual Demand Changes: Demand usually changes slowly, giving the economy time to adjust. This gradual change rarely leads to significant price fluctuations on its own.

Sudden Supply Changes: Supply-side shocks, such as natural disasters, geopolitical events, or production bottlenecks, can occur rapidly and unpredictably. The economy struggles to adjust quickly to these disruptions, leading to price increases as a balancing mechanism.

9. Fact: There is no post-gold standard relationship between federal debt and your taxes.

Unlike state/local governments, which are monetarily non-sovereign, the federal government does not use tax dollars to pay its bills. It creates new dollars, from thin air, every time it pays a creditor.

The sole purposes of federal taxes are:

–To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward.

–To assure demand for the U.S. dollar by requiring all federal taxes to be paid in dollars.

Taxes do not pay for federal spending. Federal spending creates dollars.

9.a. Fact: Federal deficit spending does not use “taxpayers’ money.” Federal spending creates money ad hoc.

When the government spends it credits bank accounts. No taxes involved. By definition, deficit spending means taxes do not equal this year’s spending let alone previous year’s spending. Only surpluses use taxpayers’ money, by causing recessions.

For the above reasons, our children and grandchildren will not pay for today’s money creation. Still, they will benefit from today’s deficit spending — better infrastructure, army, education, R&D, safety, security, health, and retirement.

Any time you hear or read about the federal government spending “taxpayers’ money,” know that the person is ignorant about Monetary Sovereignty. The federal government doesn’t spend taxpayers’ money. Period.

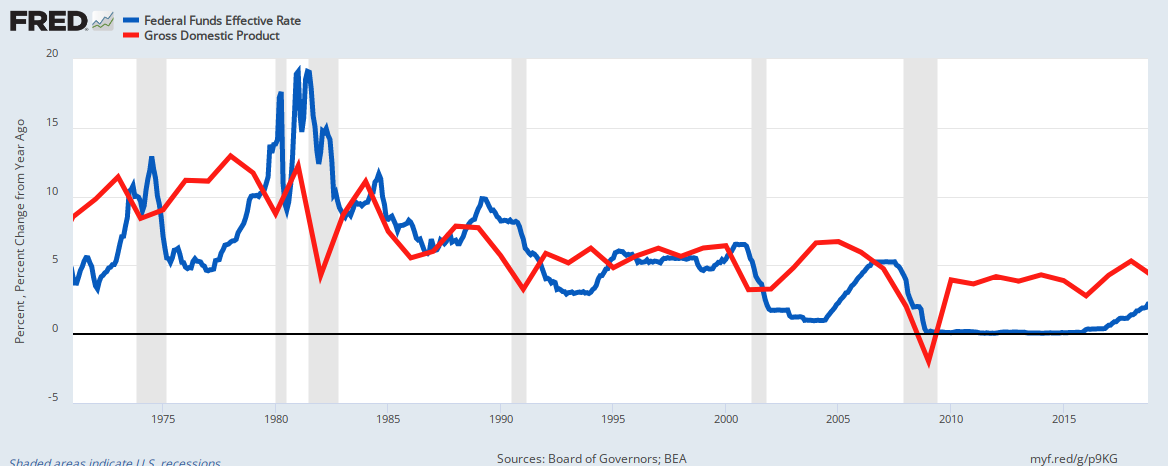

10. Fact: There is no post-gold standard relationship between low interest rates and high GDP growth. Opinion: The opposite seems true:

The interest rate and economic growth lines move in opposite directions.

Why do high interest rates stimulate? Opinion: High rates force the federal government to pay more interest, pumping more money into the economy.

The Fed increases interest rates to fight inflation. But increasing interest rates increases the prices of goods and services, i.e. causes inflation.

The Fed, in a sense, is using leeches to fight anemia.

11. Fact: The Federal debt/GDP ratio is a meaningless fraction, because it measures two, mathematically incompatible pieces of data. It’s an apples/oranges comparison. GDP is a one-year measure of output; federal debt is the net outstanding T-securities created since the nation’s birth.

The T-securities created years ago affect this year’s debt in the debt/GDP ratio, while even last year’s GDP does not affect this ratio. See: Debt/GDP

Because federal debt is the total of T-securities, and the federal government has the functional ability to stop creating T-securities at any time, the Debt/GDP ratio easily could fall to 0, depending on federal law.

11.a. Fact: The debt/GDP ratio does not measure the federal government’s ability to pay its bills. The government does not pay bills with GDP; it creates the money ad hoc to pay its bills.

Were GDP to be $0, the government still could pay bills of any size, simply by crediting the bank accounts of its creditors.

12. Facts: In 1979, gross federal debt was $800 billion. In 2009 it reached $12 trillion, a 1400% increase in 30 years. During that period, GPD rose 440% (annual rate of 5.5%>) with acceptable inflation. The same 1400% increase would put the debt at $180 trillion in 2039, a mean annual deficit of $5+ trillion.

This calculates to a 9.5% annual debt increase for the past 30 years. Repeating that growth rate would put the 2010 deficit at about $1.14 trillion, and the 2011 deficit at about $1.25 trillion. The deficit for year 2039 would be about $15.8 trillion.

Opinion: I know of no reason why the results would not be the same as they have been in the past 30 years. However, increasing the debt growth rate above 9.5% might show even better results:

In the 10 year period, 1980 – 1989, federal debt grew 210%, from $900 billion to $2.8 trillion (a 12% annual debt increase), while GDP grew .96% from $2.8 trillion to $5.5 trillion (a 7% annual increase). During that same period, inflation fell from 14.5% in 1980 to 5.2% in 1989. See graph, below.

The peaks and valleys of federal deficits (blue) generally correspond to the peaks and valleys of real (inflation adjusted) Gross Domestic Product growth. The reason: GDP = Federal Spending + Nonfederal Spending + Net Exports

Facts: In summary, large deficits have coincided with real (inflation adjusted) GDP growth

12. Facts: Any health insurance proposal that covers more people will cost more money. Extracting that money from doctors, hospitals, pharmaceutical companies, by necessity, would reduce the availability of health care.

Increasing taxes on any individuals (even the wealthy) or on businesses, will depress the economy by removing money from the economy. Only the federal government can supply additional money while stimulating the economy.

13. Fact: Social Security is supported neither by FICA nor by a trust fund. Were FICA eliminated, and benefits doubled, Social Security still would not go bankrupt unless Congress decided to make this happen.

In June, 2001, Paul O’Neill, Secretary of the Treasury said, “I come to you as a managing trustee of Social Security. Today we have no assets in the trust fund. We have promises of the good faith and credit of the United States government that benefits will flow.“

Yet, SS continues to pay benefits. Your Social Security check comes from a mythical trust fund that contains no money and receives no money.

Social Security (and Medicare) benefits are paid ad hoc by the U.S. government, not from a trust fund, and are not dependent on FICA taxes. which (opinion:) can and should be eliminated. See: FICA

14. Fact: The finances of the federal government are different from yours and mine and businesses’ and state, county and city government finances.

Unlike the federal government, which is Monetarily Sovereign, we cannot create unlimited amounts of money to pay our bills. We first need to acquire money, either by borrowing or by saving, to spend.

The federal government does not acquire money. It creates money by spending. As an accounting principle, the tax money you send to the government is destroyed upon receipt. Then the federal government creates new money to pay its bills. The government has no fund from which it pays bills.

Fact: Were taxes to decrease to zero, this would not change by even one penny, the federal government’s ability to spend.

Opinion: The failure to recognize the difference between the Monetarily Sovereign federal government and all other entities, which are monetarily non-sovereign, is the primary reason for recessions and depressions.

15. Fact: The federal government has the unlimited ability to create the dollars to pay any bill of any size. It never can run short of dollars; it never can go broke.

Opinion: The federal government should distribute dollars to each monetarily non-sovereign state, on a per capita basis.

The states would determine how they distribute the dollars (to counties, cities and/or taxpayers). I suggest a distribution of $5,000 per person or a total of $1.5 trillion.

Fact: In 1971, the U.S. went off the gold standard, thereby becoming a Monetarily Sovereign nation, and at that moment, all economics textbooks became obsolete. Sadly, mainstream economists, the politicians and the media have not yet caught up.

Summary: So there you have a list of facts, plus a few opinions, which I have noted. Read the facts and draw your own inferences.

You can find a great number of debt-hawk sites (i.e. Concord Coalition, Committee for a Responsible Federal Budget), which in essence are privately funded think tanks, paid to influence popular belief, with propaganda masquerading as data.

There, you will see data showing the size of the federal debt. These data are presented in a way designed to imply that the debt (money created) is too large.

But you will find no proof of these ideas. You will see no historical graphs equating debt with any negative economic outcome, simply because such graphs do not exist. Debt hawks believe federal deficits are so obviously bad, no proof is needed.

Yet, despite lacking proof, debt-hawks have foisted their opinions on the media, the politicians, weak-minded economists, and the public, much to the detriment of our economy.

The prevention and cure for a loss of democracy is an informed and energized electorate.

With Donald Trump ripping the government and the economy apart, here is what you should know during the two years before casting your vote in the next Congressional elections.

{kind=link}