The federal government is “Monetarily Sovereign.” That means, it creates all the money it spends by pressing computer keys. It never, never, never can run short of dollars.

Even if the federal government didn’t collect a single penny in taxes, it could continue to spend forever. Who says so?

Who says so?

Fed Chairman, Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Fed Chairman, Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.

Fed Chairman Jerome Powell stated, “As a central bank, we have the ability to create money digitally.

The St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Chat GPT: “The federal government is not financially constrained and does not need to ‘fund’ its spending.”

Treasury Secretary, Paul O’Neill: “I come to you as a managing trustee of Social Security. Today we have no assets in the trust fund. We have promises of the good faith and credit of the United States government that benefits will flow.”

Mario Draghi, President of the Monetarily Sovereign European Central Bank “We cannot run out of money.”

Paul Krugman (Nobel Prize–winning economist): “The U.S. government is not like a household. It literally prints money, and it can’t run out.”

Why does the federal government collect taxes if the government doesn’t need the money?

- To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward.

- To assure demand for the U.S. dollar by requiring dollars to be used to pay taxes.

You pay taxes with money from the M2 money supply measure. When your dollars reach the Treasury, they cease to be part of any money supply measure. Effectively, they are destroyed.

Why are they not included in any money supply measure? The government has infinite money, and therefore there is no measure for infinity.

When Donald Trump claims to reduce the debt through tariffs, he is misleading you in two ways.

- Tariffs are paid by the buyer. They are part of the price you pay for imported goods.

- Tariff dollars come out of the U.S. economy. They reduce economic growth and lead to recessions.

Thus, Trump’s tariffs hurt you in three ways.

- They take dollars directly out of your pocket

- They cause overall inflation.

- And they lead to recessions.

The side effects of inflation and recessions include demands to cut social benefits and increase taxes to “fund” them.

Trump relies on your not understanding the differences between federal finances and your personal finances. You cannot create dollars from thin air. You must have sufficient income to cover your expenses.

The federal government can create dollars from thin air, and it neither needs nor uses income to fund its spending.

And no, federal deficit spending does not cause inflation.

So what does cause inflation? Shortages of crucial goods and services, most notably shortages of energy.

To prevent and cure inflation, we never should cut federal spending. All that does is cause recessions. Instead, we should cure the shortages that caused the inflation.

When the primary cause is an oil shortage, the government should:

- Deficit spending to support oil drilling and refining

- Support the production of renewable energy (wind, solar, geothermal, atomic).

- Support the use of renewable energy (i.e., electric cars and trucks)

- Fund research into creating more energy sources

Sadly, we are doing the opposite. Trump is discouraging the development of wind energy (his “windmills”) and solar power, while also discouraging the use of renewable energy sources (such as credits for solar installations and electric cars).

The massive tariff collections + discouraging the production of renewable energy + discouraging the use of renewable energy combine to make a perfect inflation/recession storm (aka “stagflation.”)

When the inevitable stagflation happens, we Trump will blame it on Biden, Obama, the Fed, any data-gathering agency that tells the truth, China, Mexico, Canada, NATO, black “criminals,” Mexican “rapists,” immigrants, “woke,” people collecting social benefits like Medicare, Social Security, Obamacare, and “stolen” elections.

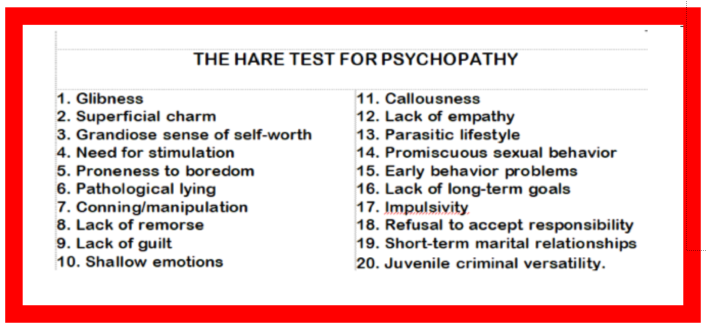

Why do we assume this? Because this is his history and because he cannot help himself. See: “A Psychopath Slipped Into the White House.”

He seemingly scores “high” on the Hare Test for Psychopathy , meaning he strongly indicates psychopathy.

The test is scored 2 (definitely present), 1 (possibly present), and 0 (not present). A total score of 30 or more is generally considered the threshold for diagnosing psychopathy.

Although you may not be a professional psychologist, and you may only have a distant observation of Donald Trump and his actions and statements, you can come to your own private conclusion about him. My guess is that the result will not be in question.

SUMMARY and PREDICTIONS

The federal deficit is necessary for economic growth and to prevent/cure recessions and depressions. You, not a foreign nation, pay for the tariffs.

Trump’s wildly eccentric and highly damaging use of tariffs will result in stagflation, which he will deny exists and/or blame on others or on world situations.

His proven reluctance to accept adverse facts will prevent him from addressing stagflation, which will worsen as he remains in power.

He will attempt to remain in office even after his current term ends, and at least three members of the Supreme Court — Alito, Thomas, and Gorsuch — will approve of his “creative” efforts to remain president in name or in fact(i.e., running as a Vice President with the intention of having the President resign).

Rodger Malcolm Mitchell

Twitter: @rodgermitchell

Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell;

MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell;

……………………………………………………………………..

A Government’s Sole Purpose is to Improve and Protect The People’s Lives.

MONETARY SOVEREIGNTY

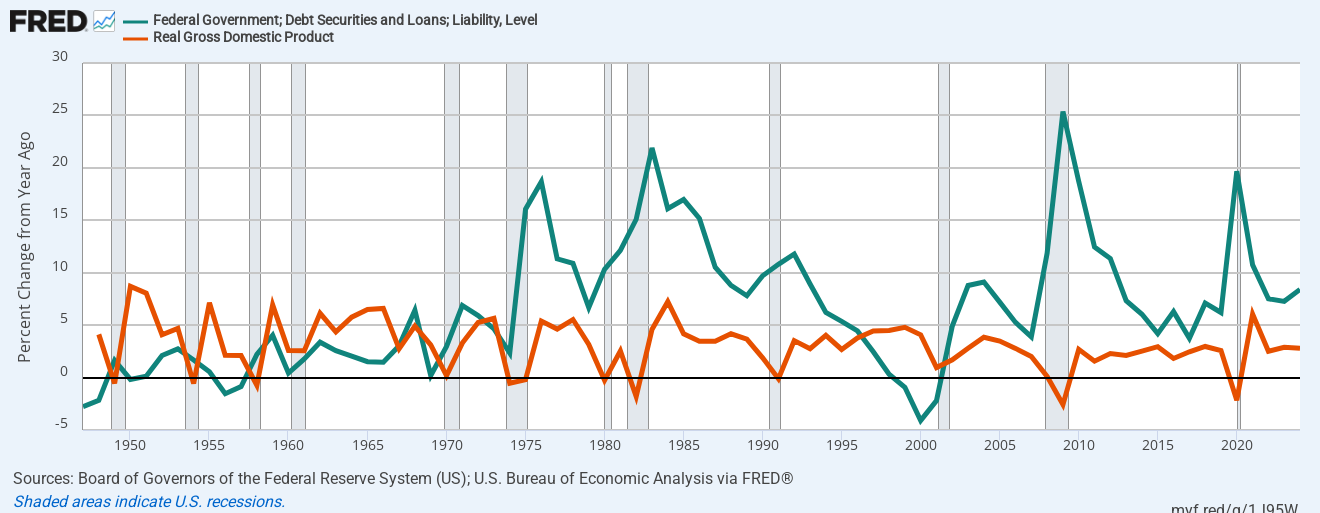

It shows one of the prime measures of economic growth, the annual change in real per capita gross domestic product. If anything should measure the “heat” of an economy, this is it.

A year ago, in early 2021, one might have said the economy is pretty “hot.” No longer. The economy now seems to be growing at a normal rate. So why does it need “cooling”?

Notice what happens before we have a recession. The annual change drops, which is exactly what the Fed wants to happen now.

I’ve been at this for twenty-five years, and I still don’t know what it means for an economy to be too hot. What I do know, however, is what causes inflation: Shortages of key goods and services.

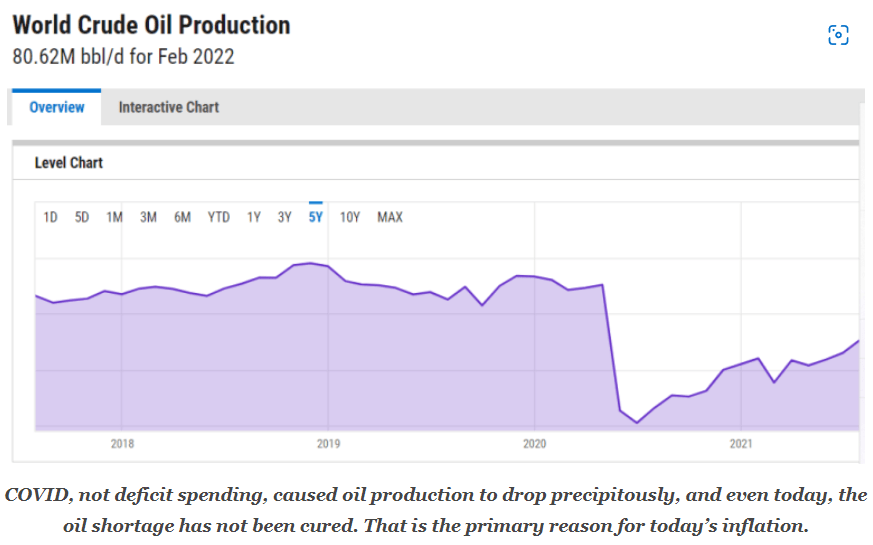

Today, we have those shortages, not because demand is too great, and not because interest rates are too low, and not because the federal deficits are too high. We have shortages because the confluence of COVID, the Russian war, and reduced oil pumping caused supply to constrict.

It shows one of the prime measures of economic growth, the annual change in real per capita gross domestic product. If anything should measure the “heat” of an economy, this is it.

A year ago, in early 2021, one might have said the economy is pretty “hot.” No longer. The economy now seems to be growing at a normal rate. So why does it need “cooling”?

Notice what happens before we have a recession. The annual change drops, which is exactly what the Fed wants to happen now.

I’ve been at this for twenty-five years, and I still don’t know what it means for an economy to be too hot. What I do know, however, is what causes inflation: Shortages of key goods and services.

Today, we have those shortages, not because demand is too great, and not because interest rates are too low, and not because the federal deficits are too high. We have shortages because the confluence of COVID, the Russian war, and reduced oil pumping caused supply to constrict.

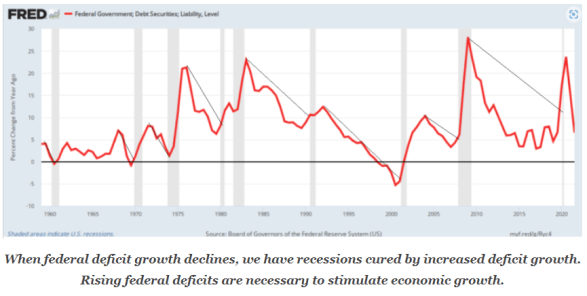

The parallels are stunning. Inflation follows oil prices because oil affects the price of every other product. The price of oil is determined by supply and demand. Increase the supply, and inflation will go down.

The same is true regarding demand. Decrease the demand for oil, and inflation will fall. But short of causing a recession, how does one decrease the demand for oil? The only answer is something we are just beginning to do: Find substitutes for oil.

Most oil is used for energy, so businesses must expand production of solar, wind, nuclear, geothermal, and tidal energy sources — and this will require increased government spending and lower interest rates.

The parallels are stunning. Inflation follows oil prices because oil affects the price of every other product. The price of oil is determined by supply and demand. Increase the supply, and inflation will go down.

The same is true regarding demand. Decrease the demand for oil, and inflation will fall. But short of causing a recession, how does one decrease the demand for oil? The only answer is something we are just beginning to do: Find substitutes for oil.

Most oil is used for energy, so businesses must expand production of solar, wind, nuclear, geothermal, and tidal energy sources — and this will require increased government spending and lower interest rates.