Imagine someone with these credentials not understanding how federal finance works.

This is a man who spends a good part of his life being asked to pontificate about economics, yet he promulgates the same old intuitive myths that history has disproven.

I’m talking about

“John Howland Cochrane, an American economist specializing in financial economics and macroeconomics. Formerly a professor of economics and finance at the University of Chicago, Cochrane serves as the Rose-Marie and Jack Anderson Senior Fellow at the Hoover Institution at Stanford University.”

Here he is, on the right, being interviewed on CNN by Michael Smerconish:

I won’t subject you to the entire interview, but rather with the following quotes give you the gist.

John Cochrane: “Sooner or later debt has to be paid off. The real worry for me is there is no plan to pay off this debt.

“Sooner or later bond markets notice you have no plan to pay it off”

Throughout the interview, Cochrane demonstrates he has no idea what Monetary Sovereignty is, and no desire to learn from history.

The federal “debt” (which isn’t really debt as you know it), is instead, the net total of all deposits into Treasury Security accounts.

When you invest in these securities (aka T-bills, T-notes, T-bonds), you actually open a T-security account in your name. It resembles a safe deposit box with one difference: The federal government pays interest into T-security accounts.

The federal government, being Monetarily Sovereign, has the unlimited ability to create its own sovereign currency, the U.S. dollar. Thus, it has no need to borrow dollars and indeed, the federal government does not borrow dollars.

The purpose of normal “borrowing” is to provide the borrower with money to use for some purpose.

But because the federal government has the unlimited ability to create dollars it does not borrow, the T-securities are not “loans,” and the federal “debt” is not a debt.

That is why, for instance, any money you may put into a bank safe deposit box is not considered a debt of the bank, and it is no burden on the bank to “pay off” that box. It simply returns to you what already is yours.

When you open a T-security account, you are aware of the exact date upon which the dollars in the account will be returned to you. That is called the “maturity” date.

During that period of time, your dollars remain in your account, earning interest. They are not used by any agency of the federal government.

At maturity, the dollars in the misnamed “debt” are paid off (i.e. returned to you) by the simple act of sending the money in your T-security account to your bank checking account.

This is not a burden on the federal government, nor is it a burden on future taxpayers. It is a simple money transfer from one of your bank accounts to another of your bank accounts.

It is not a transfer of dollars from the government to you. “Paying off” federal debt is a transfer of your dollars to yourself.

At one point Cochrane draws a parallel between federal debt and household debt. Thus he demonstrates abject ignorance of federal financing. The federal government is Monetarily Sovereign. You and I are monetarily non-sovereign.

You and I can run short of dollars, which is why we borrow money. The federal government never can run short of dollars, which is why it never borrow moneys.

At one point, Cochrane says:

“The more the government borrows the less is available for private capital.”

This short sentence is wrong on three counts:

First, the government does not borrow.

Second, the amount available for private capital is based on federal deficit spending and bank lending, not on deposits into T-securities (which in fact are privately owned capital).

Third, according to Cochrane, the federal government has “borrowed” trillions of dollars, yet there is plenty available for private capital. He simply ignores the obvious facts on the ground.

The Cochrane said,

“This is like a financial crisis. It’s like a run on the bank. It’s like an earthquake. You can’t predict it. The sky falls when people lose confidence that the U.S. will pay back the debt.

The next crisis when the U.S. wants to borrow another $10 trillion, and the bond market says, ‘You guys are not worth it.”

The implication is that the federal government can run short of dollars if the “bond market” won’t lend to them. Utter nonsense.

As we’ve said, the federal government does not borrow and cannot run short of dollars. It creates dollars at will, which it surely has proved in the past 12 months by creating trillions of stimulus dollars.

Further, if Cochrane is implying that somehow the federal government will not be able to sell its T-securities, he has it all backward.

The sole purpose of T-securities is not to provide spending money for the government. The sole purposes are:

- To help the Federal Reserve control interest rates by setting a bottom rate, and

- To provide a safe parking place for unused dollars, which helps stabilize the dollar.

In the event that the federal government wished to sell T-securities but was unable to find a buyer, the Federal Reserve Bank can (and always has) buy whatever it deems necessary.

The Treasury never can be “stuck” with something it really has no need to sell in the first place.

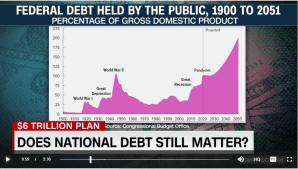

At one point in the interview, Cochrane displays the following graph to shock you:

It shows the absolutely meaningless fraction: Debt/GDP (Gross Domestic Product).

Its rise is a favorite scare tactic by those who cannot explain why the total of deposits into T-security accounts (aka “federal debt”) should have any significant relationship to Gross Domestic Product.

The graph also demonstrates the gigantic increase in the Debt/GDP ratio, which according to debt hawk should by now, have cause an economic disaster of biblical proportions. So where is the disaster?

The fraction Debt/GDP is not predictive of anything and it is not evaluative of anything. It says nothing about future booms, busts, inflations, recessions, depressions, poverty, or prosperity. It is a 100% meaningless fraction that economisfits use all the time.

To demonstrate how meaningless it is, look at these ratios:

Here were some of the lower Debt/GDP ratios a few years ago:

Here were some of the higher Debt/GDP ratios at the same time:

Oh, and did we mention that powerhouse Japan’s ratio was 223?

Niow, looking at just the numbers in these two tables, you would expect Lybia to have the healthiest economy, and Puerto Rice to have the sickest, with the U.S. somewhere in the middle.

So called “economists” ignore these obvious facts.

Finally, after briefly admitting that, yes, the government can’t run short of dollars, Cochrane mumbles something about “that would cause inflation.”

Wrong yet again, Mr. Cochrane. Here are excerpts from an article Cochrane wrote ten years ago:

“For several years, a heated debate has raged among economists and policymakers about whether we face a serious risk of inflation.

“That debate has focused largely on the Federal Reserve — especially on whether the Fed has been too aggressive in increasing the money supply, whether it has kept interest rates too low, and whether it can be relied on to reverse course if signs of inflation emerge.

“But these questions miss a grave danger.

“As a result of the federal government’s enormous debt and deficits, substantial inflation could break out in America in the next few years.”

OMG! That was ten years ago, and this guy still is peddling the same old “federal-debts-cause-inflation” nonsense he spouted way back then (!), and he has learned absolutely nothing since.

Debt and deficits have grown, while interest rates and inflation have stayed low, and still the same old, same old.

Oh, but the BS goes on and on:

“If people become convinced that our government will end up printing money to cover intractable deficits, they will see inflation in the future and so will try to get rid of dollars today — driving up the prices of goods, services, and eventually wages across the entire economy.”

The government has run enormous deficits, and people like Cochrane have been telling the people this would cause inflation.

But being smarter than the know-nothing economists, the people have not tried to “get rid of dollars,” and they have not driven up the prices of goods, services, and sadly, “wages across the country” barely have budged.

“This would amount to a “run” on the dollar.

“As with a bank run, we would not be able to tell ahead of time when such an event would occur. But our economy will be primed for it as long as our fiscal trajectory is unsustainable.“

And there it is again, the favorite word of the wrong-for-80-years debt hawks: “Unsustainable.”

Any time you read that the U.S. federal debt is, or even soon might be, “unsustainable,: immediately stop reading. The author knows nothing, and reading what he/she says is a waste of your valuable time.

It’s almost as bad as reading that the federal debt is a “ticking time bomb” (which it supposedly has been since 1940, and still ticking).

I am an economist, but for the past 25 years, I have told all who would listen that economics is not a science. It could be. It should be. But it isn’t, because the practitioners deny the obvious and instead rely on their vague intuition.

Not that there aren’t data in economics. There are mountains of data. But econodufuses would rather juggle abstruse data than look at the clear and obvious facts all around them.

They keep predicting causes and effects when the causes keep happening without the predicted effects.

They talk about ticking time bombs that never explode.

They talk about unsustainable deficits and debt that have been sustained for 80 years.

They talk about cutting the debt, when every time the debt is cut, we have depressions. (Once, only a recession).

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

They keep making claims that the facts on the ground disprove.

This is science?

And then guys like Cochrane repeatedly go on TV, and write articles, and spout absolute nonsense, with no basis in fact.

And sadly, people believe it. Even President Biden seems to believe it, and that is the real tragedy.

We could have the Ten Steps to Prosperty (below), end poverty, reduce crime, improve education, and make America that “shining city on a hill,” were it not for the debt hawks.

The debt hawks are to economics as the creationists are to biology.

Those, who do not understand Monetary Sovereignty, do not understand economics.

…………………………………………………………………………

Rodger Malcolm Mitchell

[ Monetary Sovereignty, Twitter: @rodgermitchell, Search: #monetarysovereignty Facebook: Rodger Malcolm Mitchell ]

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE. The most important problems in economics involve:

- Monetary Sovereignty describes money creation and destruction.

- Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps: Ten Steps To Prosperity:

- Eliminate FICA

- Federally funded Medicare — parts A, B & D, plus long-term care — for everyone

- Social Security for all

- Free education (including post-grad) for everyone

- Salary for attending school

- Eliminate federal taxes on business

- Increase the standard income tax deduction, annually.

- Tax the very rich (the “.1%”) more, with higher progressive tax rates on all forms of income.

- Federal ownership of all banks

- Increase federal spending on the myriad initiatives that benefit America’s 99.9%

The Ten Steps will grow the economy and narrow the income/wealth/power Gap between the rich and the rest.

MONETARY SOVEREIGNTY

Rodger

You may have seen this from the “Corporate Finance Institute”, whatever that is. More bull.

https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/treasury-bills-t-bills/

And while the following link is from 2009, seems to me it still applies. https://www.bills.com/personal-finance/dollars-and-sense/why-is-the-fed-buying-t-bills

*”…the US has no known limits to its money supply. This is because as the ‘last man standing’ after WWII, we took the opportunity to establish the world economy, with ourselves as its head. There are ‘trappings’ of equality among states, but that’s why they are called ‘trappings.’ We effectively became the only government that can, as some put it, ‘print gold.’ Our T-bills have replaced gold as the means many governments use to back their currency. Unless there is a total collapse politically, culturally and demographically of the United States, our currency will continue to be the standard for value for most major economies.*

*”Part of the reason people do not realize our elevated position is that when we are told that we are the world’s largest economy, it is rarely followed up with how really huge it is compared with the rest of the world. To illustrate, Japan is the world’s second largest economy, and China is often stated to be the new rival to the US with a huge and growing economy fueled by its population. Yet if you add the GDP of both countries, it is much less than half of the US GDP. Other countries really have no choice but to continue large investment in the U.S. economy; after all, they willingly invested their monetary reserves in US T-bills instead of physical gold. They each now have as much stake in the value of the U.S. economy as we do in our own prosperity. Our failure becomes their failure, and no one has offered a realistic alternative.”*

I would enjoy your explanation of the above, 12 years later. Your understanding far exceeds mine. In particular, your explanation of:

1. Other governments use T-bills as the means to back their currency 2. Japan+China GDP far less than half the US, still true? 3. Countries have no choice but to continue buying T-bills and investing in our economy

Thank you, Sir!

JD

LikeLike

1. True to some degree, although the nation’s full faith and credit is the single important backing. For euro nations, the full faith and credit of the EU is prime.

2. True. It’s less, but not to that extreme. China has come up significantly. See: https://fred.stlouisfed.org/graph/fredgraph.png?g=DBkv

3. Mostly true due to international trade. The dollar is the most important bank reserve currency for international trade.

LikeLike

From: https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/treasury-bills-t-bills/

“When an investor buys a Treasury Bill, they are lending money to the government. The US Government uses the money to fund its debt and pay ongoing expenses such as salaries and military equipment.”

FALSE. The money remains in the buyer’s account, which the buyer easily can see merely by asking how much money is in his account. The federal government has no need to borrow. It has the legal, unlimited power to create infinite numbers of U.S. dollars.

LikeLike

Unfortunately what happens with regard to Treasury securities is over simplified on both sides of the argument, which leads to misunderstanding and confusion. When an investor buys a Treasury security, the reserves associated with that sale are actually deposited into a TLA (Tax and Loan Account), which are Federal Reserve owned accounts at various commercial banks through the U.S. (this is also where payroll withholding goes). Money, or more specifically reserves, in these accounts are still part of the banking system and M0 money supply.

When the Treasury spends money, it comes from their demand account at the Federal Reserve, which is not part of the M0 money supply. As the Treasury spends money, it debits its account at the Federal Reserve and credits reserve accounts at various commercial banks. At this point the money (i.e. reserves) then becomes part of the money supply. In order to maintain its minimum daily balance requirement of $150B, reserves are then transferred from a TLA to the Treasury’s demand account as needed, thus removing those reserves from the money supply.

The misunderstanding comes from the fact that the point of this operation is not to fund government spending, but rather to coordinate taxing/Treasury sales with spending to maintain a steady supply of reserves within the banking system in order to stabilize interest rates. Without this operation, there would be large discrete fluctuations in money supply resulting from taxing, Treasury sales, and spending, with corresponding upward or downward pressure on interest rates. The point of Treasury sales in this respect is not to fund the debt, but rather as a mechanism to temporarily remove reserves from the banking system to allow the government to deficit spend without increasing total reserve supply, which would put downward pressure on interest rates.

These requirements have been established by law in order to prevent the government’s routine fiscal operations from impacting monetary policy (i.e. interest rates and the supply of reserves in the banking system). These same laws also prevent the Federal Reserve from buying Treasury securities directly from the U.S. Treasury, which is a holdover from gold standard days. Unfortunately, the flow of reserves from the TLAs to the Treasury’s demand account gives the appearance that government taxing and “borrowing” is funding spending, hence the confusion. MMT has shown that this is not the case, mostly through research work at UMKC by Randall Wray, Stephanie Kelton, and Matthew Forstater; however, the explanations can be rather complex. This gives way to the MMT and MS simplified argument that taxes and “borrowing” simply do not fund spending, which is at odds with what many orthodox economists and finance types familiar with government fiscal operations actually “observe” in the real world.

LikeLike

B.

Thank you for your factual explanation. Good luck explaining it to a populace that cannot even understand the simplicity of Monetary Sovereignty.

The key point is that the federal government’s financial operations are not constrained by taxes or by spending. It has the power to set bank reserves any level it wishes, and it has the power to spend at any level it wishes, despite taxing, or the lack thereof.

As I have mentioned in many posts, the federal government’s byzantine bookkeeping system is 100% under its control. Ultimately –and that is the key word — ultimately, the U.S. government’s finances are not subject to anything except its own whims.

The government (i.e Congress, the President, the Treasury, the Federal Reserve collectively) can do anything it wishes, with taxation or without taxation. Think of the government as a painter with infinite paints and the U.S. economy as its canvas.

The TGA at the FR is not allowed to run a deficit, so they go through various machinations to accomplish what they want to do. It’s a Rube Goldberg machine that goes through a few dozen steps in order to send me a dollar, and those few dozen steps have the real purpose of confusing the public so that the people will think benefits are unaffordable.

While MMT does try to make the point that federal taxes don’t fund spending, Randy wrongly claims taxes are necessary to provide demand for dollars, and Stephanie wrongly claims deficit spending can lead to inflation, and the whole bunch of them wrongly claim JG is the heart of MMT.

I respect and love them dearly, especially my frequent “pen-pal” Stephanie, but their mixed messaging dilutes and/or casts doubt on the simple and central message: The federal government has the infinite power to spend without income, and can do so while controlling inflation.

The very rich, who run the government, understand the facts. But they do not want the gap between the rich and the rest to narrow, lest the poor and middle-classes refuse to labor on behalf of the rich.

So the government, which has the infinite ability to lift the poor and middle, seemingly “struggles” but fails to do so. That failure provides the desperate people to “pick up the garbage.”

Have you noted the panic among the rich lately, with the news that some businesses are unable to hire people because the difference between unemployment compensation vs. wages is not large enough? The “solution” provided by the rich: Stop spending so much on unemployment, because the debt is too high.

LikeLike

“and the whole bunch of them wrongly claim JG is the heart of MMT.”

You haven’t yet come around to accepting Bill Mitchell as your lord and savior? A JG did wonders for Cambodia in 1975.

LikeLike