In 1647, the Massachusetts “Old Deluder Satan Act” required towns in colonial New England to hire teachers. The schools were funded by local taxes to promote literacy, so people could read the Bible.

This is widely regarded as the first law that mandated publicly funded education in what would later become the United States. By the early 1800s, this idea had spread, with other New England states adopting similar town-funded schools, although southern states did not follow suit.

In the 1830s to 1850s, modern free public schooling took shape. In Massachusetts in 1837, Horace Mann championed free, universal education funded by taxes and implemented by professional teachers.

By around 1850, most Northern states had established free public elementary schools funded by property taxes. These schools were accessible to most white children, as racial equality was achieved much later.

High schools came in 1821. The Boston English High School became the first free public high school in the U.S.

If we give them a college education, they won’t work in our factories.

By the late 1800s to early 1900s, free public high schools became widespread. Compulsory attendance laws began in 1880–1918, and segregation ended (legally): 1954, Brown v. Board of Education. Truly universal access began in the mid-20th century.

Why was free schooling mandated in the past, while free advanced education is often discouraged today? The answer, as usual, involves Monetary Sovereignty and Gap Psychology,

Our Monetarily Sovereignfederal government has an unlimited ability to create dollars with just a keystroke. It never can go bankrupt or run out of money. However, it often chooses to fund tax breaks for the wealthy rather than allocate resources to education for those who are less fortunate.

Gap Psychologydescribes a common, almost universal desire to distance oneself from those lower on the income, wealth, and power scale while trying to associate more with those above. This mindset is the primary way the wealthy maintain and increase their wealth. It also ensures that people continue to work even after they receive higher pay.

WASHINGTON — The Trump administration said Tuesday that it will begin garnishing the wages of student loan borrowers who are in default early next year.

The department said it will send notices to about 1,000 borrowers the week of Jan. 7, with more notices to come at an increasing scale each month.

Millions of borrowers are considered in default, meaning they are 270 days past due on their payments. The department must give borrowers 30 days’ notice before garnishing their wages.

The department said it will begin collection activities, “only after student and parent borrowers have been provided sufficient notice and opportunity to repay their loans.”

In May, the Trump administration ended the pandemic-era pause on student loan payments and began collecting on defaulted debt by withholding tax refunds and other federal payments from borrowers.

The move ended a period of leniency for student loan borrowers. Payments resumed in October 2023, but the Biden administration extended a one-year grace period. Since March 2020, no federal student loans had been referred for collection, including those in default, until the Trump administration’s changes earlier this year.

The Biden administration tried multiple times to offer broad student loan forgiveness, but those efforts were eventually halted by courts.

Persis Yu, deputy executive director of the Student Borrower Protection Center, criticized the decision to begin wage garnishment and said the department had failed to sufficiently help borrowers find affordable payment options.

Given that:

Educated young people are vital for America’s advancement and security.

The federal government does not need or even use any form of income.

The federal government has the infinite ability to create dollars and fund anything it wishes.

Why does the government fund free elementary and high school — in fact, make attendance compulsory — but garnish the wages of our single most valuable future resource, college students?

Free basic schooling still reinforces the social hierarchy. It still supports the Gap. Early public education has been sold as moral and obedience training, workforce preparation, and national cohesion.

It teaches punctuality, deference to authority, and literacy sufficient for labor, not power.

Even in our early days, basic schooling did not threaten the Gap. Elites benefit because it make for more productive workers, fewer unruly poor, and cultural conformity

But college education for the poor is exactly what the rich do not want.

It reduces the fear of losing one’s job, thus:

It increases labor’s bargaining power (which is why the rich hate unions), and

It puts “the rabble” on a par with the rich and weakens employers’ control.

Free college would narrow the Gap.

In this context, a federally sponsored, comprehensive, no-deductible Medicare program that coversevery man, woman, and child in America would help close the healthcare Gap.

In contrast, business-sponsored healthcare insurance for workers tends to reinforce this Gap. Millions of workers fear leaving their jobs or making demands of their employers because they worry about losing their healthcare coverage.

The federal government easily could afford to provide healthcare insurance to everyone. However, instead of doing this, it offers businesses tax incentives to provide less comprehensive coverage—just enough to keep employees dependent on their jobs for healthcare.

Finally, the same would hold for federally sponsored, living-wage Social Security for everyone, of all ages. The rich make three false excuses:

If given a bare minimum stipend, no one would work because the poor have no ambition. (aka, “Keep ’em poorso they have to accept low-pay jobs and bad working conditions.:”)

And things will have to get much worse before the populace begins to understand how Monetary Sovereignty and Gap Psychology are used against them.

Only a nation of fools would give a tax break to religion but not to science and education.

I’ve researched the question, “What are the reasons against Universal Basic Income (UBI).” I call it “Social Security for All.”

Here is a summary of the anti-UBI claims:

1. Cost and Feasibility: One of the primary concerns is the high cost of UBI. For example, in the United States, a UBI of $12,000 per year for every adult would cost over $3 trillion annually/

2. Inflation: UBI could lead to inflation. If everyone has more money to spend, demand for goods and services might increase, driving up prices and potentially negating the benefits of the additional income.

3. Work Incentive: UBI might reduce the incentive to work. If people receive a guaranteed income regardless of employment, some may choose not to work, potentially leading to a decrease in the labor force and economic productivity.

4. Misuse of Funds: Recipients might misuse the funds, spending them on non-essential items rather than necessities. This could undermine the goal of reducing poverty and improving living standards.

5. Impact on Existing Welfare Programs: Implementing UBI might require cutting or restructuring existing welfare programs. This could harm those who rely on targeted support for specific needs, such as healthcare or housing.

6. Political and Social Challenges: Gaining political and public support for UBI can be difficult. Many people are skeptical of unconditional transfer programs and prefer welfare systems tied to employment or specific conditions.

Before I address #s 1 through 6, I’ll give you the real one:

7. It would narrow the income/wealth/power Gap between the rich and the rest. The Gap is what makes the rich rich. Without the Gap no one would be rich; we all would be the same.

The wider the Gap, the richer are the rich. The easiest way for the rich to remain rich is to make sure the Gap doesn’t narrow, so using their political and informational power, the rich invent and promulgate false reasons why UBI won’t work.

Now, let us address each of the reasons given for objecting to UBI.

1. Cost and Feasibility:

We already have a form of UBI, except it isn’t “U” (Universal). We call it “Social Security,” and it covers old and/or disabled people. All the ideas opposing UBI were put forth in the 1930s when Social Security first was proposed.

Contrary to popular myth, Social Security (as well as Medicare, the military, SCOTUS salaries, White House salaries, Congress’s salaries, and every other federal expenditure) are not funded by FICA or any other federal taxes.

A. When any federal government agency approves an invoice for payment, it sends instructions (not dollars) to the creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account. The instructions are in the form of a check or a wire.

B. When the bank does as instructed ( by pressing a few computer keys), dollars are created by being added to the creditor’s checking account and to the money supply measure known as “M2.”

C. The bank then balances its books by clearing the payment through the Federal Reserve, which has the infinite power to approve all federal checks and wires.

So long as the federal government has the infinite power to pass laws and to issue instructions, it has the infinite power to pay any invoices it receives. The U.S. federal government, being the original creator of dollars from thin air, never unintentionally can run short of dollars.

You often have been told that Medicare, Social Security and/or their trust funds are running out of money. It is a false claim. Unlike state/local governments, the U.S. government is Monetarily Sovereign. With the infinite ability to create dollars, it could create the above-mentioned $3 trillion at the touch of a computer key.

The sole purpose of federal taxes (unlike state/local taxes) is notto provide the government with spending money. The dual purposes are to:

Control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward and

Assure demand for the dollar by requiring taxes to be paid in dollars.

Even if the federal government didn’t collect a single dollar in taxes, it could continue spending, forever.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Mario Draghi, President of the Monetarily Sovereign European Central Bank: “We cannot run out of money.”

Further, UBI would grow the economy. It’s a mathematical certainty because the size of the economy is determined by this formula:

Gross Domestic Product (GDP) = Federal Spending + Nonfederal Spending + Net Exports.

By simple algebra, UBI would grow the economy because it would increase Federal Spending and, as a result, increase Nonfederal Spending, too.

When faced with the undeniable facts that UBI is affordable for the federal government and would grow the economy, those influenced by wealthy propaganda resort to excuse #2.;

2. Inflation: The common yet erroneous belief is that “excessive” fedeal spending causes inflation. This belief is wrong on several fronts.

First, no one knows what “excessive” means. The rich always claim federal spending is excessive (see: Historical claims the Federal Debt is a “ticking time bomb.” From Sept. 26, 1940, to July 22, 2024) because most federal spending goes to the poor. It narrows the Gap, a situation the rich despise.

By contrast, the rich favor tax deductions for the wealthy, which are not part of “spending” but widen the Gap just as federal spending does.

Economics is a pseudoscience loaded with hypotheses and flush with data— and ne’er the twain shall meet.

Some economists make this arguement based on intuition, but not on fact: They claim that people earn income by selling their labor on the labor market as a contribution to the production of goods and services for the economy. Income increases that aren’t directly related to correlating increases in production tend to result in higher prices.

It’s nonsense.

Which of these can claim their income is “directly related to correlatingincreases in production?” Taxi driver? School teacher? Musician? Flight attendant? Doctor? How about Elon Musk? If he made “just $100 million instead of a few billion, would that “directly relate to a correlating decrease in production”?

Pay has little to do with production and more with labor scarcity, politics, heredity, and other social factors. Queen Elizabeth’s pay had little to do with her output. I am retired, and my income has nothing to do with my production. Raising hotel workers’ skimpy pay or decreasing mortgage brokers’ high pay would not “directly relate to their production.”

The hypothesis is something that only an economics professor in a well-endowed think tank could dream up.

Inflation is not caused by federal spending. Inflation is caused by scarcities,most often scarcities of oil and food:

The peaks and valleys of inflation(red) do not match up with the peaks and valleys of federal spending (blue).

The peaks and valleys of inflation do match up with the peaks and valleys of oil prices, which are dictated by oil supply and demand.

Today, the federal government is spending more than ever, yet inflation is drifting down. The most recent inflation was COVID-related, not spending-related.It was caused by shortages of oil, food, computer chips, metal, lumber, shipping, and labor.

Raising everyone’s income by giving them money would not cause inflation. Scarcities of crucial items cause inflation.

Federal spending to cure scarcities cures inflation. The “federal spending causes inflation” meme is a fever dream promulgated by the rich to maintain the income/wealth/power Gap.

3. Work Incentive: Critics argue that UBI might reduce the incentive to work, decreasing the labor force and economic productivity. This is a favorite of the rich, who love to portray lower-income people as lazy slugs who, if given money, will simply loll about doing nothing.

The truth is that poor labor is harder than rich labor unless one considers costly vacations, country clubs, and having servants do one’s work to be “labor.” Virtually everyone wants a better life, and that includes the poor. Given a stipend by the government, they will work to increase their standard of living, just as the rich do.

Similarly, the vast majority of the rich want to be richer. Almost no one is satisfied, and it is certainly not a low-income family that receives Social Security.

I trust this isn’t just a projection on my part, but I began collecting Social Security at age 65. I continued to work for a living until I was 73, not because I loved work, but because I wanted more money to feel secure. I had what some may consider a lot, but I still wanted more.

That said, what is wrong with a decrease in the labor force? What is wrong with a four-day work week or a five-hour day? Work usually is not a purpose unto itself. The primary purpose of most work is to improve one’s life, however one defines “improve.”

For households in every quintile of the income distribution, the share of income required to pay for their 2019 consumption decreased, on average, because income grew faster than prices did over that four-year period.

Households in the top income quintile had the largest decline, on average, in the share of income required to pay for their 2019 consumption.

Translation: The rich kept earning more spending money than the rest of us did. Even though they had plenty of money, they wanted more, and worked for it. Why would the average and below-average income people be less motivated? They wouldn’t, but that is what the rich claim.

Artificial intelligence (AI) and automation are making it more possible to do less and accomplish more. A solution to the possible unemployment caused by AI may be UBI.

4. Misuse of Funds: Some argue that recipients might misuse the funds, spending them on non-essential items rather than necessities. This is another one the rich love — the notion that the poor are ignorant money managers and that if you give them money they’ll waste it on drugs and lottery tickets.

The reality is quite the opposite. By necessity, the poor have learned to be good money managers. In any event, it is none of the government’s business whether or not someone “misuses” their income. The idea the the government knows better is repulsive and bigoted.

5. Impact on Existing Welfare Programs: Implementing UBI might require cutting or restructuring existing welfare programs. Critics worry that this could harm those who rely on targeted support for specific needs, such as healthcare or housing.

This is easily prevented. Just don’t do it. Don’t include UBI income as part of any welfare criterion.

The current system — requiring someone to be poor to receive financial aid — is self-defeating. It encourages the very thing the rich claim to fear: people not working. It also leads to dishonesty and to gaming the system by mischaracterizing income.

6. Political and Social Challenges: Gaining political and public support for UBI can be difficult. Many people are skeptical of unconditional transfer programs and prefer welfare systems tied to employment or specific conditions.

This is the old “If I had to work for my money, why should he get money for doing nothing?” The solution would be to give every man, woman and child in America the same amounts regardless of their other income or wealth.

The money would mean little to the rich and much to the poor, but it would overcome the resistance of those who hate to see others receive something.

7. It would narrow the Gap between the rich and the rest. The Gap is what makes the rich rich. Without the Gap no one would be rich; we all would be the same.

The wider the Gap, the richer are the rich. The easiest way for the rich to remain rich is to make sure the Gap doesn’t narrow, so using their political and informational power, the rich invent and promulgate false reasons why UBI won’t work.

This is the single biggest hurdle to cross. The first six objections easily are overcome and/or are based on incomplete information. This one is based on the intense emotions of America’s most influential people.

A rich man might be generous about charity for the poor, but he doesn’t want poverty to be eliminated altogether. He needs the poor. Having a mansion is not as attractive if everyone else has a mansion. It’s the Gap that makes him rich, and narrowing the Gap makes him less rich, an unappealing prospect.

If a neighbor wins the lottery or even gets a more lucrative job, how does the rest of the neighborhood feel? What does Mark Zuckerberg think about Elon Musk having more money?

The majority of us suffers from Gap Psychology, the desire to distance ourselves from those below us on the income/wealth/power scale and to come closer to those above us. The conflict arises because those above us don’t want us closer and those below us want us closer.

SUMMARY

There are no good reasons not to begin a UBI program and plenty of reasons to start.

I suggest the following monthly payments:

$1,000 to every adult (18+)

$500 to every child

Include undocumented adults and children.

Assume:

258 million adult (citizens) + 31 million adult (non-citizens) = 289 million total adults; Annual Cost: $289 billion * 12 = $3.468 trillion

73 million children (citizens) + 14 million children(non-citizens) = 87 million children; Annual Cost: $43.5 billion * 12 = $522 billion

Combined Annual Cost: $3.468 trillion (adults) + $522 billion (children) = $3.99 trillion per year

This compares to the most recent (2023) federal expenditure of about $6.3 trillion.

Poverty generally is worse in the states that tend to vote Republican, the party that wrongly opposes social benefits, saying they are “unaffordable” and “socialism” — which they are not.

(Socialism is government control of industry, not just government funding. All governments fund things, but relatively few of those things can be called “socialism.”)

Government spending has a multiplier effect on GDP. The multiplier effect measures how much economic activity is generated by an initial amount of the expenditure. Estimates for the fiscal multiplier vary, but a typical range is between 0.5 and 2.0.

With a conservative multiplier of 1.5, GDP would grow about $6 trillion on top of the most recent 28.65 trillion for a new value of $34.65 trillion.

Improve the infrastructure and help cut global warming

And improve the entire American nation’s quality of life by using the brainpower now hampered by a lack of funding

Do all this at no cost to anyone.

Think of it. The United States of America has the power to be the first large nation on earth to eliminate poverty. Millions of men, women, and children could begin to contribute to America’s success.

Too good to be true? No, too good only for those who don’t understand the power of human thought and desire, when funded by Monetary Sovereignty.

I long have favored a federal plan in which every man, woman, and child in America would receive a monthly stipend from the federal government. (Some call it UBI—Universal Basic Income. Others call it GI—Guaranteed Income, or Social Security for All.)

A federally funded Social Security for All program was described in a post published seven years ago.

Today, that post was brought to mind by the following article:

An Illinois Senate appropriations committee would review “the landscape of cash supports available to low-income residents” and identify “populations without significant access to cash supports.”

The bill, as filed, says after the board is dissolved at the end of 2027, DHS would administer the program with monthly cash payments of $1,000 to Illinois residents, regardless of immigration status, who provide care for a child or specified dependent, recently gave birth or adopted a child or is enrolled in an educational or vocational program.

By law, the Monetarily Sovereign U.S. government is an infinite horn of plenty, capable of creating an unending stream of dollars at the touch of a computer key without collecting a penny in taxes.

Mike Buehler, an opponent of the measure, said it’s irresponsible to discuss such a program without knowing how much it will cost taxpayers.

You may be surprised that I oppose this and other similar plans.

Here is why:

1. Localgovernments are monetarily non-sovereign (unlike the federal government, which being Monetarily Sovereign, has the infinite ability to create dollars).

With few exceptions, local governments get their spending money from taxpayers.

That is why it can run trillion-dollar deficits with no funding problem at all.

State, county, or city taxpayers pay for local government-funded UBI programs.

Most local tax dollars come from sales taxes and/or local income taxes, most of which are paid by middle—and lower-income residents. Extracting dollars from middle—and lower-income taxpayers is exactly the opposite of the UBI plan’s basic purpose.

2. While the federal government has unlimited access to dollars,local governments have limited abilities to pay for things. So, the benefits must be limited to local governments’ affordability estimates.

This, in turn, requires limiting benefits to specific groups and denying benefits to other groups, which creates two problems:

A. The government must set up a complex and expensive apparatus for monitoring recipients so that people do not cheat.

B. People just outside the limit of qualifications are unjustly deprived of aid, and/or try to find unanticipated ways to qualify.

“I understand that you would have to be a person with a child, or caring for someone in your home or school to be eligible for the benefits.

A local government would have to hire dozens (or thousands?) of people to monitor these qualifications. (Do you have a child? How old? Are you really “caring for” that boarder? Are you still in school, and exactly what is a “school.” How many days or hours do you attend?

Additionally, there would be extensive and expensive paperwork filed, read, and authenticated.

That could be millions of people and the cost could be in the tens of billions of dollars,” Buehler told The Center Square. “And where’s the state going to come up with these funds and the only place to come up with that is to get it from the taxpayers.”

Guaranteed income programs in Chicago and the Metro East St. Louis areas are ongoing, costing taxpayers millions. In 2022, the city of Chicago was in line to spend $31.5 million for $500 a month to go to 5,000 low-income residents.

That same year, Illinois legislators approved a pilot program using state taxpayer fundsworth $3.6 million for the Metro East St. Louis area.

Inevitably, a state-run, money-restricted program would evolve to a “nanny-state,” where the money only could be used for approved purposes. And that would have to be monitored.

Ameya Pawar with the Economic Security Project said there are 150 different programs across the country. He gave examples of people using the money to buy sports goods for their children or even to take a vacation.

There is widespread belief that the poor who receive money from taxpayers, should be told what to do with the money (the poor supposedly being too ignorant to know what is best for them). Buying sports goods and taking vacations is not “good” for the poor.

The nanny preference is only to feedstarving children, not just make them happy with toys and entertainment. Note the hinted outrage Ameya Pewar expresses for recipients buying baseballs to entertain their kids.

“And all of this money that goes into the pockets to stabilize households flows through local businesses,” Pawar told the committee. “So you see some of this money back in sales taxes, and other taxes.”

No buying from Amazon allowed??

Buehler said there could be unintended consequences, like reducing work productivity and more.

“For regardless of immigration status, I think an unintended consequence could be a flood of migrants coming to Illinois looking for benefits and not having to work for it,” he said.

3. If one state, county, city, or village offers better benefits than another, people will tend to go where the money is and the taxpayers will pay. This is true for citizens as well as migrants.

And note the common but false belief that the poor are so lazy and unmotivated, if you give them money, they won’t get jobs.

Pawar said the proposed statewide guaranteed program of “unrestricted cash” should be in addition to other taxpayer-funded safety net programs.

Programs like Supplemental Nutrition Assistance Program funds go to buy food. The Low Income Housing Energy Assistance Program is for heating bills. The Temporary Assistance for Needy Families program provides monthly cash assistance to low-income families with children.

“And to get this income, they may not necessarily spend that in their own best interest or the interest of the citizens at large,” he said.

Again, the taxpayer requirement exacerbated the nanny-state belief that the poor are too stupid to spend in their own best interests. “Why am I, as a taxpayer helping these people to take vacations, if I can’t afford one myself.”

All the above-mentioned problems would be addressed by a federally-funded, Social Security program covering every man, woman, and child in America, regardless of income or wealth.

The rich, poor, citizens, non-citizens, young, old, married, single, renter, homeowner, in or out of school, etc., all would receive the stated benefits — and unlike with state and local government programs, no one would pay a penny.

Federal Social Security payments made to every man, woman, and child, require much less monitoring. Most importantly, affordability would cease to be an issue. The federal government can afford anything, and without collecting taxes.

All of the money spent by the federal government would be addedto the local economy, increasing everyone’s income.

8 Million Have Slipped Into Poverty Since May as Federal Aid Has Dried Up, October 15, 2020. (By Leigh Lynes: New studies show the effect of the emergency $2 trillion package known as the Cares Act and what happened when the money ran out.)

Here are excerpts from another article on the subject.

Actually, there are “strings,” in the form of qualifications.

More than interest — when former US presidential candidate Andrew Yang announced that a UBI program of $1,000 direct payments to citizens every month would be the keystone policy of his platform, he drew an unexpected amount of grassroots support in a crowded primary year.

Guaranteed income programs have been gaining even more traction during the pandemic, which took a particular toll on low-wage workers and threw many Americans into poverty.

At least 11 direct-cash experiments went into effect this year, Bloomberg estimated in January.

Former Stockton, California mayor Michael Tubbs, took the idea to the next level by launching the Mayors for a Guaranteed Income network. As of this year, there are 60 mayors in the program, advocating — and launching pilot programs for — guaranteed income for their residents.

California recently launched the first statewide guaranteed income program in the US, providing up to $1000 per month to qualifying pregnant people and young adults leaving the foster care system.

“Young adults leaving foster care” and “pregnant people” comprise two, very narrow classes, and $1000 a month is a meager amount. The task of verifying qualifications would be costly. (Imagine trying to verify pregnancy for thousands of people, and who monitors when pregnancies end before birth?)

The basic income program that Tubbs launched in Stockton in 2019, the Stockton Economic Empowerment Demonstration, has been considered the model for other cities that have followed in its footsteps, offering low-income residents hundreds of dollars a month and measuring their job prospects, financial stability, and overall well-being afterward.

It seems like a massive and expensive project for just hundreds of dollars’ worth of benefits.

According to SEED, participants improved in all those metrics.

“Guaranteed income makes a case for investing in our undocumented neighbors and formerly incarcerated residents. In doing so, it addresses the reality of the nation’s fragmented, punitive welfare structure.”

Will taxpayers consider this a reward for being undocumented or incarcerated? (Want to make an easy few hundred dollars a month? Go to jail for some minor charge.)

This kind of program isn’t a new idea, however. The Eastern Band of Cherokee Indians Casino Dividend in North Carolina has been giving tribal members annual funds since 1997, for instance. Alaska has been paying residents out of its oil dividends since 1982.

The Eastern Band of Cherokee Indians Casino Dividend in North Carolina gets its money from casino revenue. Alaska gets its dividend money from oil. Neither collects taxes to pay recipients. That is a major consideration.

Here are a few of the 33 examples mentioned in the above article.

Compton, California. Duration: December 2020 to December 2022. Income amount: $1,800 every three months for 2 years. Number of participants: 800

Tacoma, Washington,Duration: December 2021 to December 2o22, Income amount: $500 every month for 1 year, Number of participants: 110

Stockton, California, Duration: February 2019 to February 2021, Income amount: $500 every month for 2 years, Number of participants: 1ount: Based on the annual dividend from state-owned oil companies, ranged from roughly $2,000 per person in 2015 to $800 in years with lower gas prices.

Oakland Resilient Families,Duration: Summer 2020 to present, Income amount: $500 per month for 18 months, Number of participants: 600

Alaska Permanent Fund , Duration: Annual, Income amount: Based on the annual dividend from state-owned oil companies, ranged from roughly $2,000 per person in 2015 to $800 in years with lower gas prices , Number of participants: Alaska residents

North Carolina, Cherokee Tribe, The Eastern Band of Cherokee Indians Casino Dividend pays every tribe member annually, Duration: Annual, Income amount: $4,000 – $6,000 per year, Number of participants: Every tribal member.

The Alaska and Cherokee programs succeed long term because they are not funded by taxpayers. A federally funded program would succeed for the same reason. Federal spending is not taxpayer funded.When state and local taxpayers fund a spending program, the result is that a large group of middle- and low-income people transfers some of their money to a smaller group of middle- and low-income people.

The large group includes all those who pay sales and income taxes. The small group is all those who receive those tax dollars. It’s just dollars rotating within the municipality, enriching some residents at the expense of others. The municipality’s economy receives nothing.

By contrast, when the federal government funds a guaranteed income program the government creates new dollars and sends them to the nation’s recipients. The result is that there is no expense to anyone, but the nation’s economy is enriched with net dollars. (GDP = Federal Spending + Nonfederal Spending + Net Exports).

Guaranteed income programs help narrow the income/wealth/power Gap between the rich and the poorer. While reducing poverty, in of itself, is a worthwhile goal, narrowing the Gap also helps address related, social problems:

Wide Gaps affect not only poverty itself, but health and longevity, education, housing, law and crime, war, ownership, bigotry, taxation, GDP, scientific advancement, the environment, human motivation and well-being, and virtually every other issue related to economics.

The most successful guaranteed income programs share several features:

Funded by a Monetarily Sovereign government or by state owned and controlled businesses. This takes taxpayer costs out of the equation.

Minimal requirements for participants achieve voter support by making the plan fairer.

Significant benefits. Trivial payments, i.e. $100 a month, etc. will not generate positive voter sentiment.

Easy entry and supervision. Difficult entry results in negative feelings by voters. Easy supervision lowers costs.

Easily understood goal.

Many good reasons for, and no good reasons why not.

A national Social Security for All plan, with a minimum benefit if $5,000 per year for each adult (18 and over) and $2,500 a year for a child would begin to address the abovementioned social problems.

The Cost:

The U.S. has about 260 million adults (18+) and about 70 million children.

At the $5,000/2,500 level, the benefit cost of the Social Security for All would be $1.3 trillion for adults and $175 billion for children, totaling somewhat south of only $1.5 trillion.

Why do I say “only”? By comparison:

In 2023, the federal government spent about $6.2 trillion.

The Gross Domestic Product (GDP) for the year 2023 had a current-dollar value of $27.36 trillion.

In 2023, the U.S. federal government collected a total of approximately $4.71 trillion in tax revenue.

In fiscal year 2023, the federal government’s spending exceeded its revenues, resulting in a deficit of $1.70 trillion

By the end of 2023, the cumulative federal deficit was $26.236 trillion.

The U.S. M2 money supply is about $20 trillion.

Given that:

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

and

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

A Monetarily Sovereign government spending $1.7 trillion to send an additional $5,000 to every adult and $2,500 to every child — and at no cost to anyone — would seem to be a bargain price and a great investment for America.

Further, because of the multiplier effect*, that additional $1.7 trillion in federal spending, would increase Gross Domestic Product far more than $1.7 trillion.

*Per Investopedia:A government increases spending or decreases taxes in part to inject more money into the system.

Such fiscal policy has a multiplier effect. That is, every dollar spent can be expected to cause an increase in the gross domestic product (GDP) by more than a dollar.

This is due to the sheer momentum created by the policy. Consumers spend more so businesses produce more goods.

Businesses have to hire more to produce more goods, so more people have more money to spend on goods.

The same phenomenon occurs for both government spending increases and tax cuts. Either tends to increase GDP disproportionately.

A cut in government spending can reduce GDP by a greater degree than the amount saved by the cut.

The expanded Child Tax Credit had a multiplier effect of 1.25 on GDP in the first quarter of 2021, according to an analysis by Moody’s Analytics. The increase in the Supplemental Nutrition Assistance Program boosted GDP by a 1.61 multiplier effect in the same period. Increased defense spending had a 1.24 multiplier effect.

Infinite benefits at no cost to anyone: Can any knowledgeable person object to Social Security for All?

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

We did it with the “Economic Stimulus Act 2008. The federal government simply sent people money.

Generally, low and middle-income taxpayers received up to $300 per person or $600 per couple.

The purpose was to stimulate economic growth and to cure the recession.

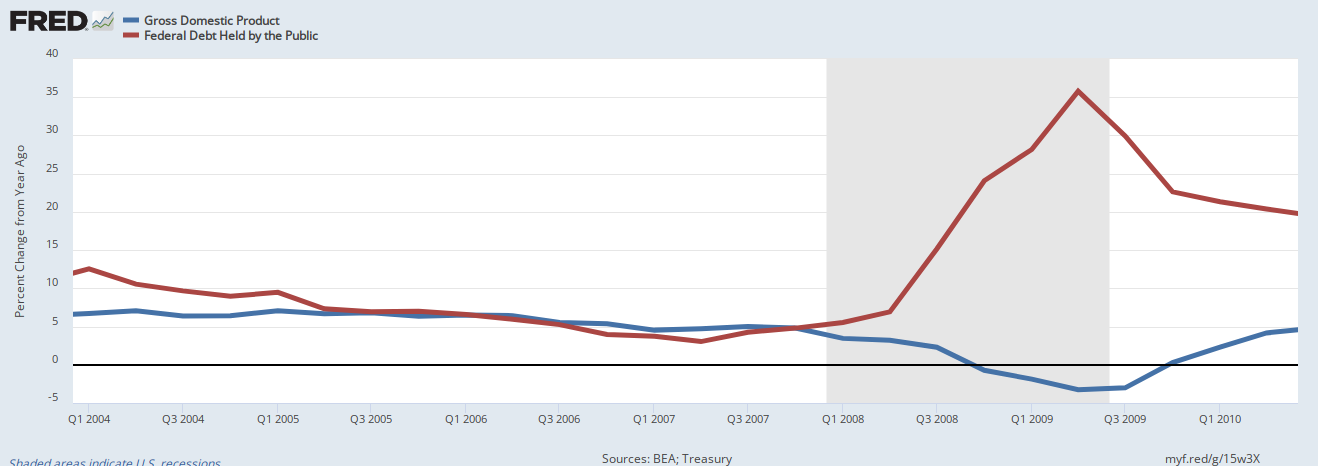

It worked:

As federal deficits (blue) declined, we fell into a deep recession, cured only by a robust increase in federal deficit spending (red).

Gross Domestic Product (GDP) is a common measure of the economy. The above graph should come as no surprise. The formula for economic growth is:

GDP = Federal Spending+ Nonfederal Spending + Net Exports

Mathematically, as federal deficit spending decreases, economic growth falls, and as federal deficit spending increases, economic growth increases.

If you want economic growth, you want federal deficit spending to increase.

I’ve written about this many times.It’s simple algebra. I’m not sure why this is a mystery to the politicians who think a debt limit is prudent finance. It’s exceedingly ignorant finance.

I mention this again because of an article I just read on MEDPAGETODAY:

Uninsured Rate Hits Record Low of 8.3% — But that number will slowly rise as pandemic health insurance protections unwind, experts say by Joyce Frieden, Washington Editor, MedPage Today May 24, 2023

WASHINGTON — The uninsured rate in the U.S. has fallen to a record-low 8.3%, but that percentage is expected to gradually increase as insurance protections from the COVID-19 pandemic wind down, according to officials from the Congressional Budget Office (CBO).

Why will insurance protections “wind down.” For the same reason we currently have a debt=limit battle in Congress. Sheer ignorance.

The federal government has repeatedly proved that it has the infinite ability to pay for anything. Why is it “winding down” payments for healthcare insurance?

The temporary policies enacted in the wake of the COVID-19 pandemic “have contributed to a record low uninsurance rate in 2023 of 8.3% and record-high enrollment in both Medicaid and ACA [Affordable Care Act] marketplace coverage,”said Caroline Hanson, Ph.D., principal analyst at the CBO, during a briefing sponsored by Health Affairs.

“As those temporary policies expire under current law, the distribution of coverage will change and the share of people who lack insurance is expected to increase by 2033.”

CBO is projecting an uninsured rate of 10.1% by 2033, and “while that’s obviously higher than the 8.3% that we’re estimating for 2023, it is nevertheless lower than the uninsured rate in the last year prior to the COVID-19 pandemic,” which was about 12%, she said.

Think about it. America has about 330 million people. A ten percent uninsured rate means 33 MILLION (!) people in America will have to do without health care insurance. I hope you’re not among them.

Whether or not you have insurance, here are some data that should concern you:

“A widely cited study published in the American Journal of Public Health in 2009 analyzed data from the National Health Interview Survey and found that uninsured individuals had a 40% higher risk of death compared to their insured counterparts. This study estimated that lack of health insurance contributed to approximately 45,000 deaths annually in the United States.

“Another study published in the Annals of Internal Medicine in 2017 conducted a systematic review and meta-analysis of previous research. The analysis concluded that uninsured individuals faced a 25% higher risk of mortality compared to those with insurance.”

When you don’t have healthcare insurance, you die younger.

“Throughout the 2023-33 period, employment-based coverage will remain the largest source of health insurance, with average monthly enrollment between 155 million and 159 million,” Hanson and co-authors wrote in an article published in Health Affairs.

Employer-based health care insurance has two features seldom discussed.

It ties employees to their employer, making job negotiation and movement much more difficult

It is paid for by the employee because the employer figures the cost as part of the employment. Salaries could be higher without this “perk.”

If the federal government funded a comprehensive Medicare for All plan, employees would earn more without costing employers more.

However, they added, “in addition to policy changes over the course of the next decade, demographic and macroeconomic changes affect trends in coverage in the CBO’s projections.”

The Families First Coronavirus Response Act of 2020 gave states a 6.2-percentage-point boost in their Medicaid matching rates as long as the states didn’t disenroll anyone in Medicaid or CHIP for the duration of the COVID public health emergency.

Hanson noted that this law “allowed people to remain enrolled regardless of their changes in eligibility. So, for example, even if they had an income increase that would have made them ineligible but for the policy,” they were still able to stay on Medicaid.

The COVID public health emergency has been canceled now. Disenrollments can begin.

As a result of the law, Medicaid enrollment has grown substantially since 2019 — by 16.1 million enrollees, she said. But that has been superseded by another act of Congress, which allowed states to begin “unwinding” the continuous eligibility rules and start disenrolling people from Medicaid and CHIP beginning on April 1.

In total, “15.5 million people will be transitioning out of Medicaid after eligibility redetermination,” said Hanson. “Among that 15.5 million people, CBO is estimating that 6.2 million of them will go uninsured and the remainder will be enrolled in another source of coverage,” such as individual coverage or employment-based coverage.

Of those who are leaving Medicaid, how many are leaving voluntarily and how many are “falling through the cracks” because they didn’t receive their disenrollment notification or failed to fill out the required paperwork to reapply?

“We recognize that before these continuous eligibility requirements were put into place, people were losing Medicaid coverage, both because they were becoming no longer eligible for Medicaid, and … because they did not complete the application process despite remaining eligible,” said CBO analyst Claire Hou, PhD. However, she added, “we’re currently not aware of any data that would allow us to quantify the size of those two different groups.”

All of the above would be unnecessary if our Monetarily Sovereign federal government (which has unlimited funds) simply would fund a comprehensive, no-deductibles Medicare for All program.

Hanson delivered some bad news for those footing the bill for private health insurance. “We are projecting relatively high short-term premium growth rates in private health insurance, and this is for a few reasons,” she said.

“One is the economy-wide inflation that we’re experiencing in 2023 and that we have been experiencing, and that has not fully reflected itself in premiums yet.

And another contributor is the continued bouncing back of medical spending after the suppressed utilization that we saw earlier in the pandemic.”

The study authors project average premium increases of 6.5% in 2023, 5.9% during 2024-2025, and 5.7% in 2026-2027.

The current and projected-to-increase hardship on the American people is totally unnecessary. The federal government efficiently could ameliorate this hardship by:

Funding comprehensive, no-deductible Medicare for every man, woman, and child in America

Funding Social Security benefits for every man, woman, and child in America.

Both would add dollars to Gross Domestic Product, thus growing the economy.

Instead, Congress battles over the unbelievably stupid debt ceiling. How do those people manage to dress themselves in the morning, much less be elected to America’s Congress? It boggles the mind.