Self-evaluation corresponds with intelligence. If you are smart, being smart lets you understand that you are smart. If you are stupid, being stupid keeps you from knowing you are stupid. Thus, everyone thinks they are smart.In related issues, everyone thinks they are above-average drivers and that the federal government can run short of dollars.

==============/////=================

A rose by any other name may smell as sweet, but what if they called it “stinkwort”? Labels do matter. Visualize this scenario:

The boater must take more water from the ocean than he receives from the ocean. That is, the ocean must run a water deficit for the boater to survive, just as the federal government must run a dollar deficit for the economy to survive.

A man sits in a rowboat in the Pacific Ocean.

Using his desalinization kit he fills his canteen with one pint of water, which he later drinks and excretes as urine,

But, because of perspiration evaporation and breathing, he excretes only 9/10th pint of urine.

So, for boater the Pacific Ocean runs a deficitof 1/10th pint of water.

Does anyone care?

No, the Pacific Ocean running a 1/10th pint of water deficit is meaningless, because for all intents, the ocean has infinite water.

Infinite water minus 1/10th pint still equals infinite. No change.

Now imagine the same scenario, except instead of viewing it from the ocean’s standpoint, view it from the boater’s standpoint.

The man has drunk a pint of water, 9/10th of which he has excreted as urine into the ocean, and used the rest for perspiration, and other bodily functions.

That pint of water has allowed him to live for a certain time. Without the pint of water, he would have died.

That’s important.

In both scenarios we gave you the same information, but in one case we labeled it as a water measure from the standpoint of the ocean, and in the other case we labeled it as a water measure from the standpoint of the boater.

The following graph comes from https://www.chartr.co/newsletters/2023-02-08/. It labels money flow from the standpoint of the U.S. government:This graph shows the nation’s money flow from the standpoint of the U.S. government, not from the standpoint of the economy.

Here are excerpts from the accompanying article:

State of the union’s walletLast night, President Biden held the annual State of the Union. A big theme was the economy. He threatened to veto any proposal that would cut spending on Social Security and Medicare while also imploring Congress to raise the debt ceiling.

I O U $1.4 trillion: In fiscal year 2022, the federal government collected nearly $5tn in revenue, with more than 50% of that coming from individual income taxes.

However, the US government spent even more, leading to a nearly $1.4tndeficit.

To make up for the difference the US government does what everyone who overspends their budget does — they borrow.

This then adds to its already enormous tab (AKA the national debt), which currently sits at the $31.4tn debt ceiling limit.

With a debt pile that big, the interest payments aren’t small. Indeed, last year the US government spent ~$480bn on net interest payments, just shy of Ireland, Norway or Nigeria’s annual GDP.

There are three major problems with the above scenario.

It draws a false parallel between the finances of our Monetarily Sovereign governmentand the finances of monetarily non-sovereign “everyone.” The former has infinite money and the latter does not.

It falsely states that the federal government must borrow in order to “make up the difference.” The federal government, having the infinite ability to create its sovereign currency, never borrows dollars, and never needs to “make up the difference.” To pay all its obligations, the federal government creates new dollars, ad hoc. It destroys all the tax dollars it receives.

It labels the money movement from the standpoint of the federal government rather than from the standpoint of the economy.

Think of the Pacific Ocean as analogous to the U.S. federal government, and the boater as analogous to the economy.

Like the Pacific Ocean’s water, the federal government has infinite dollars. And like the boater’s limited water supply, the economy has limited dollars.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Quote from from 60 Minutes:Scott Pelley: Is that tax money that the Fed is spending?Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

(The final sentence, above, is Fed-speak for, “The government does not borrow to pay its bills.”)

The U.S. government is not the only Monetarily Sovereign government. The European Central Bank also is Monetarily Sovereign (and like the U.S. economy, individual euro nations are monetarily non-sovereign.)

Press Conference: Mario Draghi, President of the ECB, 9 January 2014Question: I am wondering: can the ECB ever run out of money?Mario Draghi: Technically, no. We cannot run out of money.

To survive, the boater needs the Pacific Ocean to run a water deficit. Similarly, to survive, the economy needs the federal government to run a dollar deficit.

The Pacific Ocean does not need to receive any water from the boater nor does the Ocean “owe” the boater any water. Similarly, the economy should not be asked to give the federal government any money, nor does the government “owe” the economy any money.

Finally, the Pacific Ocean does not borrow water to give water to the boater.

Think of the Pacific Ocean and the boater the next time you hear about federal debt limits and taxes.

Labels matter.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Here is an easy way to detect economics bullshit: If someone tells you that U.S. federal government spending — any U.S. federal government spending — is “unsustainable” without explaining why, you can be sure that person is a liar or a fool. No exceptions.

“Unsustainable” long has been the word of choice for those who spread fear about federal deficits, federal debt, Social Security, Medicare, Medicaid, aid to the poor, and everything else the rich don’t like.

But what exactly is “unsustainable” about federal spending? Will the federal government, which created the very first laws out of thin air, and will the laws that created the dollar out of thin air, suddenly be unable to create more dollars out of thin air?

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

When challenged, the liars and fools reluctantly admit, “No, the government can’t run out of dollars, but deficit spending causes inflation.”

We’ve debunked that myth so many times my typing fingers are worn down. See here, here, here, here, and here, and many other places.

The simple and obvious fact is that inflation is not caused by federal deficit spending. And inflation is not caused by interest rates that are too low. The cause of all inflations is scarcities of key goods and services, most notably oil and food.

So the cure for inflation is not to cut federal deficit spending, nor is it to raise interest rates. The treatment for inflation is to cure the scarcities of critical goods and services, most notably energy and food.

How does one cure those inflation-causing scarcities? Federal deficit spending to obtain and provide the scarce goods and services.

Sadly, the Libertarian Reason.com’s solution to all ills is to claim government spending is “unsustainable.”Libertarianism = Anarchy

Medicare? “Unsustainable.” Social Security? “Unsustainable.” Military spending? “Unsustainable.” Everything the federal government does? “Unsustainable.”

Never mind that we have been “sustaining” huge and growing federal deficit expenditures for more than 80 years, while the economy has grown massively.

When you’re a Libertarian, you hate the government. Period. You are an anarchist.

And here is an example of that, from Reason.com’s website:

For The New York Times’ Paul Krugman, the real crisis facing America’s entitlement programs is that the media isn’t working hard enough to ignore their impending collapse.

“I’ve seen numerous declarations f,rom mainst,ream media that of course Medicare and Social Security can’t be sustained in their present form,” Krugman wrote in a Times op-ed this week. “And not just in the opinion pages.”

Perhaps that’s because the unsustainable trajectories of Social Security and Medicare aren’t a matter of opinion.

They’re factual realities, supported by the most recent annual reports of the programs’ trustees and the independent analysis of the Congressional Budget Office central). Social Security’s main trust fund will hit insolvency somewhere between 2033 and 2035, according to those projeleadingns, while one of the main trust funds in Medicare will be insolvent before the end of this decade.

Have you ever wondered why you never hear worries about the “trust fund” for the military? Or the “trust fund” to support the Supreme Court?

And why no concern about “trust funds” to fund the White House, the Senate or the House of Representatives?

Federal Trust Funds Are Not Real Trust Funds

Here is what the Peter G. Peterson Foundation says about these “trust funds”:

Federal trust funds bear little resemblance to their private-sector counterparts, and therefore the name can be misleading.

A “trust fund” implies a secure source of funding. However, a federal trust fund is simply an accounting mechanism used to track inflows and outflows for specific programs.

In private-sector trust funds, receipts are deposited and assets are held and invested by trustees on behalf of the stated beneficiaries. In federal trust funds, the federal government does not set aside the receipts or invest them in private assets.

Rather, the receipts are recorded as accounting credits in the trust funds and then combined with other receipts that the Treasury collects and spends.

Further, the federal government owns the accounts and can, by changing the law, unilaterally alter the purposes of the accounts and raise or lower collections and expenditures.

Get it? Trust funds aren’t real funds. They are just accounting mechanisms to track inflows and outflows. The federal government owns the books andcan change the books at will.

The federal government can change the purposes of the Medicare and Social Security “Trust Funds”; it can add or subtract dollars at will; it can continue to fund Medicare and Social Security in any desired way and in any desired amounts.

The government and its liars and fools wring their hands and claim the trust funds are in danger of insolvency. But no federal agency can become insolvent unless that is what the President and Congress want.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

The federal government literally has the power to change the account books simply by passing a law. All the bleating and worrying about a federal agency becoming insolvent is a lie.

If the federal government wished, it instantly could add a trillion dollars to the Medicare “trust fund,” and eliminate FICA altogether. Keep in mind: The government owns the books.

When insolvency hits, there will be mandatory across-the-board benefit cuts—for Social Security, that’s likely to translate into a roughly 20 percent reduction in promised benefits.

“Mandatory,” until the government decides it isn’t mandatory.

Alan Greenspan: “The United States can pay any debt it has because we can always print the money to do that.”

Nevertheless, Krugman says he’s got a solution that “need not involve benefit cuts.”

His argument boils down to three points. First, Krugman says the CBO’s projections about future costs in Social Security and Medicare might be wrong.

Second, he speculates that they might be wrong because life expectancy won’t continue to increase.

Finally, if those first two things turn out to be at least partially true, then it’s possible that cost growth will be limited to only about 3 percent of gross domestic product (GDP) ov,er the next three decades and we’ll just raise taxes to cover that.

There never is a need to raise federal taxes. There is no funding need for federal taxes at all. The federal government destroys all tax dollars it receives, and creates new spending dollars, ad hoc.

When you pay your taxes, your dollars come from the M2 money supply measure. When they reach the Treasury, they cease to be part of the M2 money supply or any other money supply measure. They literally are destroyed.

When the federal government spends, it sends instructions (not dollars) to the creditors’ banks, instructing the banks to increase the balances in the creditors’ checking accounts.

This creates the new dollars that are added to the M2 money supply.

The banks clear the instructions through the Federal Reserve preserving the tidy, double-entry bookkeeping.

If you remember just one thing from this post, remember that dollars are not physical things. They are legal, bookkeeping entries, and the federal government controls the laws and the books.

If the government wished, it could eliminate all federal trust funds, or add a trillion dollars to each of them, and it all would just be bookkeeping.

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

“America has the lowest taxes of any advanced nation; given the political will, of course we could come up with 3 percent more of G.D.P. in revenue,” he writes. “We can keep these programs, which are so deeply embedded in American society, if we want to.

Killing them would be a choice.”

Federal taxes do not fund the federal government. The purpose of federal taxes is to control the economyby taxing what the government wishes to discourage and giving tax breaks to what the government wishes to encourage.

The federal government could eliminate all federal taxes, yet continue to spend forever.

It’s notable that Krugman sees benefit cuts as “a choice” but believes that implementing a massive tax increase on American employers and workers would be “of course” no big deal.

But that hardly addresses the substance of what he gets wrong. Let’s take each of his three arguments in order and show why they’re incorrect.

First, he says the CBO’s projections about future costs for the two programs might be inaccurate because the agency is assuming that health care costs will continue to grow faster than the economy as a whole.

At best, that means postponing insolvency by a few years. The structural imbalance between revenues and outlays means that depletion of the trust funds is a question of “when” and not “if,” as this chart from the Committee for a Responsible Federal Budget makes clear.

The above would be true if the federal government were monetarily non-sovereign, like the states, counties, cities, euro nations, you and me.

We monetarily non-sovereign entities do not have the unlimited ability to create our sovereign currencies. We have no sovereign currencies.

But the U.S. government is absolutely sovereign over the U.S. dollar. It can create as many or as few dollars as it wishes.

It can give those dollars any values it wishes and it can change those values (which it has done many times) at will.

The U.S. dollar is a tool of the U.S. government.

The Reason.com Libertarians seem ignorant of the difference between Monetary Sovereignty and monetary non-sovereignty, and thus ignorant of economics

Krugman even concedes that despite a decline in the expected rate of growth in future health care costs, those costs are still expected to rise faster than the economy grows.

Combined with the aging of America’s population, this is a demographic and fiscal time bomb. Ignoring that reality is certainly not a sound policy strategy.

Even if healthcare costs were to triple tomorrow, the federal government could fund Medicare while not collecting a single penny in FICA taxes.

Second, he speculates that mortality rates might continue to drop. While that might be good news from an actuarial perspective, it seems both morally horrifying and incredibly risky to base a long-term entitlement program on the assumption that more people will die at a younger age.

Even if every American retired at 50 and lived to age 200, the federal government could fund Medicare for All, and a generous Social Security for All, again while not collecting a penny if FICA taxes.

In fact, Krugman gets this point exactly backward. Instead of banking on a decline in life expectancy, Congress ought to raise the eligibility age for collecting benefits from Social Security and Medicare.

That would create the same demographic benefits on the accounting side even as people live hopefully longer, better lives.

And there you have it. The Libertarian solution for all government problems is to cut benefits, especially those benefits that aid the poor and middle classes.

The Libertarians refuse to accept this vital truth: The sole purpose of any government is to protect and improve the lives of the governed.

How cutting benefits accomplishes that purpose has yet to be explained.

Krugman would no doubt see such a change as an unacceptable benefit cut, but in reality, it would restore Social Security to its proper role as a safety net for the truly needy, not a conveyer belt to transfer wealth from the younger, working population to the older, relatively wealthier retired population.

The so-called “conveyer belt” would only be true if federal taxes funded federal spending. But they don’t.

Federal taxes fund nothing. FICA could and should be eliminated, while Social Security benefits should be increased.

When Social Security launched in 1935, the average life expectancy for Americans was 61. That’s changed, so the program’s parameters should too.

Yes, Social Security parameters should change. Benefits are too low. FICA should be eliminated.

Finally, the blitheness of Krugman’s actual solution—a massive tax increase—ignores all the knock-on effects of that idea.

Keeping Social Security and Medicare whole will require a tax increase in excess of $1 trillion, which would have massive repercussions on wages, the costs of starting a business, and economic growth in general.

It’s far from an ideal solution.

Keeping Social Security and Medicare whole will require no tax increase at all. The programs are not funded by tax dollars, which are destroyed upon receipt. The programs are funded by laws, and Congress controls the laws.

Paraphrasing Reason.com’s claim, eliminating FICA would have massive positive effects on wages, the costs of starting a business, and economic growth in general.

In all, Krugman’s column amounts to an argument that his addiction to donuts is totally sustainable as long as someone else agrees to keep buying donuts for him (and as long as he ignores the long-term costs to his health).

Maybe the doctors are wrong about the projected consequences of eating too many donuts. Maybe it will turn out that living longer just isn’t all that great anyway.

But if all else fails, at least he’s got someone else willing to pay for his habit—and making any changes would be tantamount to killing a tradition deeply embedded in the Krugman morning routine. We must take that option off the breakfast table.

The above analogy might make some sense for monetarily non-sovereign governments, but it is completely false for the federal government.

Instead of lying to their readers and constituents, America’s thought and political leaders (not just President Joe Biden and Krugman but lawmakers and media commentators on all sides) should start acknowledging that America’s entitlement programs are not sustainable in their current form.

Instead of lying to their readers and constituents, Libertarians (not just Reason.com) should acknowledge the differences between Monetary Sovereignty and monetary non-sovereignty.

Without changes, they will wreck the economy or force many retirees to deal with sudden cuts to benefits they expected to receive. Maybe both.

Waiting to deal with this problem will only make it worse. If Krugman’s column is the best argument for the long-term sustainability of America’s two major entitlement programs, it should only underline how seriously screwed they are.

No, Krugman’s column is not the best argument for long-term sustainability.

Using the facts about Monetary Sovereignty is the absolute guarantee of long-term sustainability.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Debt-to-GDP Ratio: How High Is Too High? It DependsOctober 07, 2020, By Heather Hennerich

How much federal debt is too much? Is there a tipping point at which it becomes a big problem for a country?

One way to gauge the size of a country’s national debt is to compare it with the size of its economy—the ratio of debt to GDP. (GDP serves as a measure of an economy’s overall size and health, measuring the total market value of all of a country’s goods and services produced in a given year.)

Gross Domestic Product (GDP) is one measure of size, but it is not a measure of health. There is no relationship between the health of an economy and the Debt/GDP ratio.

Heather Hennerich’s claim that “GDP serves as a measure of an economy’s overall size and health” simply is false. In fact, the Debt/GDP ratio signifies nothing, nothing at all.

Yes, it’s a fraction that is quoted all the time by people who should know better. But you might as well quote an apples/Apple phones comparison.

Debt is a cumulative measure of federal government deficitssince the beginning of time.GDP is a one yearmeasure of an entirenation’sspending.

If you want a similar comparison try the total amount of water a city has wasted vs. the amount of orange juice the mayor drank, yesterday. Call it the “waste/OJ” ratio, and claim it means something.

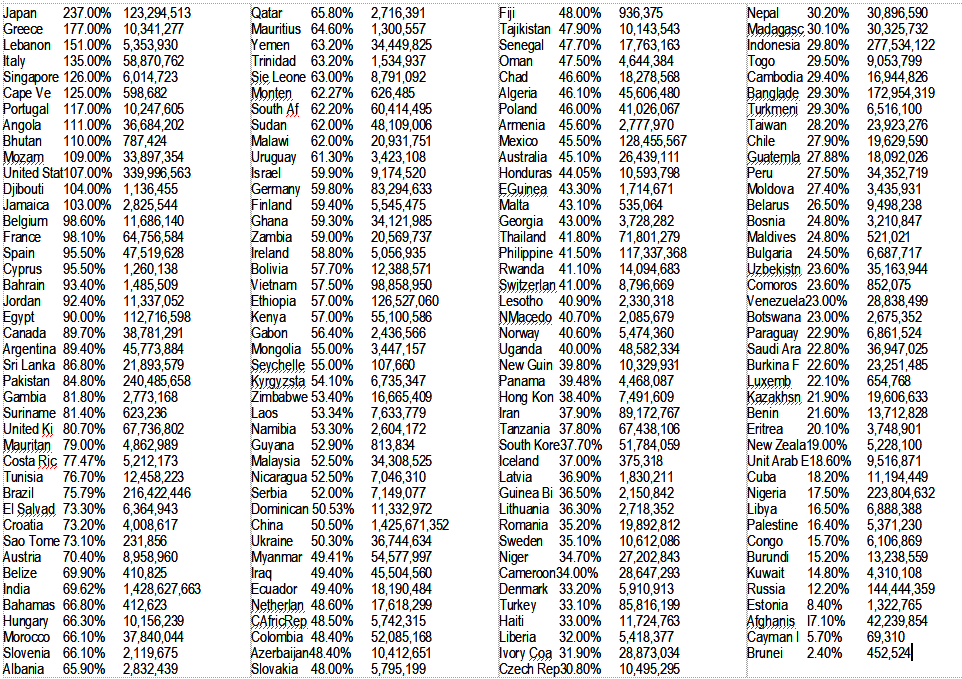

Skim the following list of Debt/GDP ratios, and see if you can find any relationship between the Debt/GDP ratio, the population of the nation, and what you know about the health of its economy.

Begin with the fact that wealthy, powerfulJapan and weak, impoverished Greece are 1,2 on the list. The United States falls right between Mozambique and Djbouti on the list. Russia has one of the lowest ratios, indicating the “health” of its economy.

NATION — DEBT/GDP RATIO — POPULATION

The Debt/GDP ratio does not measure the health of an economy.

The next time you hear or read some pundit’s concerns about America’s Debt/GDP ratio, you will know that pundit does not know what he/she is talking about.

The U.S. federal debt-to-GDP ratio was 107% late last year, and it went up to nearly 136% in the second quarter of 2020 with the passage of a coronavirus relief package.

By comparison, Japan’s ratio at the end of 2019 was higher: about 200%, according to data from the Bank of Japan and Japan’s Ministry of Foreign Affairs and calculations by St. Louis Fed Economist Miguel Faria-e-Castro.

By comparing the total federal debt to the size of a country’s economy, we can see how that government can use the resources at hand to finance the debt, according to Your Guide to America’s Finances from the U.S. Department of Treasury.

This wrongly assumes that federal (Monetarily Sovereign) finances are like personal (monetarily non-sovereign) finances.

The federal government does not “finance” its debt. (Here the word “finance” seems to mean pay it off or perhaps pay interest on it.)

The so-called “debt” is nothing more than deposits into privately owned, Treasury Security accounts. We say “privately owned” because the federal government never touches those dollars. As a depositor, you alone decide when to take dollars out or leave them in (following certain initial rules). The dollars are yours when you deposit them and when you retrieve them.

That’s why they are not a “loan.”If they were a loan, the borrower would control them. But there is no borrower. The federal government never borrows dollars.

These accounts are similar to safe deposit boxes into which you place your valuables. Just as the bank never touches those valuables, the federal government, being Monetarily Sovereign, never needs to touch your deposited money.

To pay off the so-called “debt” the government merely returns your dollars to you, the depositor.

As for the “resources at hand,” we assume this means that in some mysterious way, the government supposedly uses GDP or perhaps Lake Michigan, to pay off T-securities. No one knows how that works.

It’s all gibberish and nonsensical.

In his research, Faria-e-Castro explores big questions about the economy, so we asked him about this issue last year.

Deficit spending means that a government is choosing not to raise taxes today to pay for that spending but is choosing to wait until tomorrow, Faria-e-Castro said.

Monetarily non-sovereign governments (state, local, euro) use taxes to fund spending. But Monetarily Sovereign governments (US, Canada, Japan, Australia, et al) do not use taxes to fund spending. A huge difference Faria-e-Castro seems not to understand. (And he’s an economist for the St. Louis Fed!!)

Monetarily Sovereign governments use taxes to direct their economies by taxing what they want to discourage and giving tax breaks to what they want to encourage.

There is scant similarity between federal finances and state/local government finances. Those who do not understand the difference should not be writing for the Federal Reserve.

While state/local governments rely on tax income, the federal government could continue spending, forever, with no tax income at all.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Then we come to this bit of misinformation, that applies to state/local governments, but not to the federal government:

When federal spending exceeds revenue, the difference is a deficit. The government mostly borrows money to make up the difference.

The federal government doesn’t borrow dollars. Why would it, given its infinite ability to create new dollars?

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

Greenspan understood Monetary Sovereignty. Too bad he didn’t make his knowledge clear so we no longer would have ridiculous laws mandating a “debt ceiling.”

Now, again, the nation is paralyzed by the useless debt ceiling while the GOP demands spending cuts though they have no idea what they want to cut. (They don’t have the courage to admit they really would like to cut Social Security and Medicare, so as to help the rich become richer.)

The total national debt is an accumulation of federal deficits over time, minus any repayments of debt, among other factors.

By law, the federal government accepts deposits into T-security accounts equal to the accumulation of federal deficits. This is a point of confusion, because people mistakenly are led to believe that the deposits pay for the deficits. They don’t. The deposits pay for nothing.

The purpose of deposits (i.e. T-securities) is to provide a safe place to store dollars, which stabilizes the dollar.

A big consequence of deficit spending is that the fiscal burden shifts from one generation to the next, Faria-e-Castro said.

This is entirely wrong. You never have endured a “fiscal burden” for previous deficits. The government pays for all its deficits by creating new dollars from thin air. This is not a burden on anyone, not on you and not on the government.

The “fiscal burden” myth, promulgated through the decades, is a result of ignorance about Monetary Sovereignty.

That’s fine if a country’s economy is growing, because you know that the next generation will, on average, be better off than the current one, and likely able to pay a little more in taxes to decrease the debt, Faria-e-Castro said.

But if a country’s economy is slowing and economic growth rates are lower than they used to be, “this starts becoming a more divisive issue.”

It’s only divisive for those who are ignorant about federal finances. “The next generation” doesn’t pay for back debt. The taxes paid by every generation see the same fate: All federal taxes are destroyed upon receipt.

Tax dollars are paid from what is known as “the M2 money supply measure.” The moment they are received by the Treasury, they cease to be part of any money supply measure. In short, they are destroyed.

Say the government of “Country X” borrows money to cover its deficits, Faria-e-Castro said. Investors—many of them international—buy that debt and then want to be repaid.

“One day, the president of Country X can just organize a press conference and just tell people, ‘OK. We’re not paying,’” Faria-e-Castro said. “That’s an outright hard default.”

But countries that take that action will have trouble borrowing again. Lenders will be less willing to lend to them and will charge higher interest rates.

Here, Faria-e-Castro displays remarkable ignorance of national finance because he doesn’t differentiate between Monetarily Sovereign governments and monetarily non-sovereign governments.

The monetarily non-sovereign governments borrow money because they have no sovereign currency.

“The president of Country X can call the governor of the central bank and say, ‘OK, you have to print money to pay for this debt,’” Faria-e-Castro said.

In a country where the central bank is not an independent authority, the central bank can be pressured more easily by politicians to start printing money to pay for the country’s debt, he said.

But the flow of new money will invariably lead to high inflation in that country. That erases the value of the debt—a “soft default”—but it also typically kicks off hyperinflation, Faria-e-Castro said.

Astoundingly, that is precisely what does not happen, and the evidence is there for all to see.

Whether one views federal debt as “Federal Debt Held by The Public” (first graph below) or as “Federal Debt as a Percent of Gross Domestic Product” (2nd graph below), there is no relationship between federal debt and inflation.

There is no relationship between federal debt held by the public and inflation. Peaks and valleys do not correspond.There is no relationship between the Debt/GDP ratio and inflation. Peaks an valleys do not correspond.

It never ceases to amaze that obvious and readily available statistics are ignored by so-called “experts” in favor of hand-me-down beliefs having no basis in fact.

Inflation is not related to federal spending because inflation is caused by shortages of key goods and services.

Some claim that federal deficit spending causes those shortages, but for years and years, we’d seen massive federal spending, with low inflation.

The federal dollars that led to increased demand also facilitated increased supply. That is how capitalism works; supply rises to meet demand.

But suddenly, in 2020, we began to see inflation. What suddenly changed in 2020?

COVID.

The inflation that came suddenly in 2020, an inflation we still endure, was caused by COVID-related shortages of oil, food, computer chips, lumber, steel, shipping, labor, etc.

There is no statistical relationship between federal deficit spending and inflation.

But would you like to see something that does have a relationship with inflation?Shortages of key goods and services (most often oil) cause inflation. Oil prices are closely related to supply. The peaks and valleys correspond between oil supply and inflation.

Yes, if you’re looking for the primary cause of inflation, start with oil shortages, which then relate to other shortages. COVID was responsible for shortages of oil, food, etc.

It would be hard to make the case that after decades of big deficits, suddenly federal spending caused an increase in oil demand. Inflations are supply-related.

Federal spending actually can cure inflation if the spending is directed toward obtaining the scarce goods and services and distributing them to the public.

Contrary to popular wisdom, restricting federal spending during an inflation is counterproductive.

Hyperinflation is excessive inflation, with very rapid and out of control general price increases. Economists usually consider monthly inflation rates of above 50% as hyperinflation episodes, as noted in a 2018 On the Economy blog post.

Faria-e-Castro explained, countries that are not politically stable and don’t have independent central banks are not going to have very credible institutions. As a consequence, they can’t borrow easily: Investors won’t be willing to lend them that much for fear of future default.

But the debt of countries with strong institutions and independent central banks—like the U.S. and Japan—doesn’t present the same risks, Faria-e-Castro said.

He thinks the difference between countries has to do with a “strong, central bank.” Poppycock.

The central bank of a Monetarily Sovereign nation is strong because Monetary Sovereignty makes it strong. It has the unlimited ability to create its nation’s sovereign currency.

Monetarily non-sovereign nations also have central banks. Sadly, these banks are weak because they do not have the unlimited ability to create sovereign currency: They have no sovereign currency to create.

Few believe, for example, that the Japanese government will ever pressure the Bank of Japan to actually “print” money to pay for the country’s debt, Faria-e-Castro said.

First, the Bank of Japan “prints” (creates) yen all the time. No “pressure” needed. It’s a normal, daily process.

And second, those yen do not pay for the country’s debt. They pay for the country’s purchases. Like the U.S., the Japanese government does not borrow to pay for anything. It creates yen to pay for everything.

“As a consequence, these countries can typically sustain very high levels of debt to GDP,” he said. “Because people really believe that they will be repaid, so they can keep lending.”

There’s that phony Debt/GDP ratio, again. The U.S. doesn’t borrow. It issues Treasury bills, notes, and bonds, and if not enough are issued to satisfy the law, the Federal Reserve Bank simply buys the rest.

The strength of institutions also affects interest rates on the debt, which is another factor in determining the sustainability of high debt-to-GDP ratios.

No, the Fed determines short-term interest rates by fiat. And that meaningless Debt/GDP ratio is infinitely sustainable.

If a country has strong institutions, interest rates on the debt will be low, which means the cost of borrowing will be low, Faria-e-Castro said.

When he talks about the “cost of borrowing,” he mistakenly believes government T-securities represent borrowing. They don’t. They represent deposits.

These deposits are paid off, not with taxes but by returning the dollars that are in the accounts.

And whether interest rates are high or low is irrelevant to a Monetarily Sovereign nation having the infinite ability to create the currency to pay interest.

Because the institutional strength and riskiness of countries varies, there’s no rule of thumb for how high a debt-to-GDP ratio can be before it poses a risk to a country’s economy.

“At the end of the day, it all boils down to strong and independent institutions,” Faria-e-Castro said.

“A lot of economists try to study this. There’s no single measure that we can come up with… Measuring institutional strength is not obvious.”

It’s not obvious because Faria-e-Castro is confusing federal financing with private financing. He doesn’t understand the difference between Monetary Sovereignty and monetary non-sovereignty. And he’s speaking for the Federal Reserve!? Yikes!

He falls in line with the current mistaken belief that fighting inflations requires the pain of recession that cuts in federal spending beget.

That is the kind of leadership that destroys nations.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Your federal tax dollars are taken from the economy and are destroyed upon receipt.

Unlike state/local tax dollars, federal tax dollars are destroyed the second they are received by the government.

State/local governments, being monetarily non-sovereign, need tax dollars to support spending. The Monetarily Sovereign federal government does not.

Federal tax collections do nothing but take dollars from the U.S. economy and therefore are recessive. (State/local tax dollars remain in the economy.)

Thus, steps to reduce federal tax collections are economically stimulative because those steps keep money in the economy.

An article from the Wall Street Journal discusses the latest Republican steps to reduce federal tax collections — the right move for the wrong reasons.

GOP House Takes First Swipe at IRS Money A bill expected to be first legislation from the new Republican majority would rescind billions in funding for tax agency

WASHINGTON—The new Republican-controlled House is poised to vote as soon as Monday to repeal tens of billions of dollars in Internal Revenue Service funding, taking up a bill that is unlikely to become law but that previews coming battles with Democrats over the tax agency’s expansion.

Initially, this repeal would be recessive. It would prevent the federal government from adding tens of billions of growth dollars to the economy.

However, if those dollars were to be used to increase the collection of taxes, repealing the added federal spending could be stimulative.

The bill—expected to be the first legislation advanced by the Republican majority that took over the House last week—aims to erase a key policy priority of the Democrats, who used their control of the government to enact it last year.

Democrats, who still hold the Senate and White House, could block the legislation. But Republicans’ emphasis on clawing back IRS funding marks it as a top concern and demand for the House majority, one that could re-emerge when lawmakers turn to raising the debt ceiling or passing annual spending bills later this year.

The bill, sponsored by Rep. Adrian Smith (R., Neb.), would rescind almost all of the $80 billion in IRS funding that Congress approved in August in the climate, health, and tax law known as the Inflation Reduction Act.

In short, whether the Smith bill would be stimulative or recessive depends on whether the $80 billion would result in more or fewer federal tax dollars being collected.

If rescinding the $80 billion investment would prevent the collection of more than $80 billion tax dollars, the Republican bill would be stimulative. Until that point, however, rescinding the $80 billion investment would be recessive.

That’s just arithmetic.

The other consideration is why the Republicans wish to rescind this expenditure.

House Speaker Kevin McCarthy (R., Calif.) promised, “Our very first bill will repeal the funding for 87,000 new IRS agents. We believe government should be to help you, not go after you.”

The IRS would keep $3.2 billion for taxpayer services, which it started using to hire thousands of customer-service representatives to answer phone calls during the coming tax-filing season. In fiscal year 2022, the agency’s level of service—a measurement of how often phones are answered—was 17.4%, below its 30% target for that year, its 75.9% level from 2018, and the 85% target for this year.

The Republicans, the party of law and order — the party that is pro-police — tells America that added IRS “police” would “go after” the public. The Dems deny it.

The fact that the IRS would keep $3.2 billion is stimulative from the standpoint of dollars added to the economy. Using that money to improve customer service is stimulative in that it increases the efficient use of time. Increased efficiency is stimulative.

The IRS would also keep $4.8 billion for systems modernization, which the agency plans to use to update aging technology.

If updating aging technology would increase federal tax collections by more than $4.8 billion, the systems modernization would be recessive.

But tens of billions designated for enforcement, operations, the inspector general’s office, the U.S. Tax Court and the Treasury Department would be rescinded.

Democrats championed the $80 billion IRS expansion to bolster the agency, which had generally flat or declining budgets for much of the past decade. The IRS has shed staff and conducts audits less frequently than it did in the past.

Conducting audits less frequently is stimulative because it leaves more dollars in the private sector (i.e., the economy).

The biggest piece of the money went to enforcement, and administration officials say they want to focus on high-income taxpayers and large corporations. The Congressional Budget Office estimated that the $80 billion in spending would generate $180.4 billion in additional revenue.

If the Congressional Budget Office is correct, the Democrat’s bill would be $100 billion recessive.

But then we come to the huge unknown, the key phrase, “. . . focus on high-income tax-payers and large corporations.”

To the degree that the $80 billion would focus on high-income taxpayers, the program would help narrow the income/wealth/power Gap between the rich and the rest. That Gap is currently too broad, and it is widening. Narrowing the Gap would help the economy.

But the effect of large corporations on the economy is primarily positive. On balance, large corporations can better provide efficient services than small businesses.

While the economy needs small businesses’ creativity and employment power, using tax laws to punish large companies seems counter-productive.

The administration has said audit rates for taxpayers with incomes below $400,000 would stay around recent or historical levels. But the IRS hasn’t specified what those audit rates would be, and audit rates have fluctuated over time.

Democrats argued that removing the funding would offer comfort to tax cheats, making it harder for the IRS to find and penalize tax dodging.

Federal taxes are a significant drag on the economy, and tax laws exacerbate the Gap between the rich and the rest of us. So again, we have a split decision.

Tax dodging helps the economy by leaving more dollars in the private sector, but the rich are more able to do it, hurting the economy.

Perhaps, a vital issue is motive.

The Democrats wish to collect more taxes from the rich, using the false premise that those additional tax dollars would pay for more benefits given to the poor.

The GOP wishes to collect less tax from the rich because it, more than the Democrats, is ruled by the rich. As perhaps an overly broad generalization, the Republicans are the party of the rich, while the Democrats are the party of the rest — at least from a purely financial standpoint.

Race, religion, and country of origin affect that metric.

IN SUMMARY

Federal taxes are an unnecessary drag on the economy. They pay for nothing and are destroyed on receipt. Anything that reduces federal tax collections benefits the private sector (aka, “the economy”).

The sole function of federal taxes is to control the economy by punishing what the government wishes to discourage and by giving tax breaks to what the government wishes to encourage.

The economic drag could be eliminated if the government gave financial rewards to what it wishes to encourage, and simply didn’t reward what it wishes to discourage.

Federal taxes can and should be eliminated.

The Democrats wish to increase federal tax collections while promulgating the false notion that federal deficits are too high and federal taxes are necessary to minimize deficits while paying for benefits.

The Democrats correctly, wish to narrow the income/wealth/power Gap between the rich and the rest, but increasing federal taxes is a poor strategy for that purpose.

The Republicans wish to widen the Gap and enrich the rich by cutting tax collections from the rich. They promulgate the lie that the middle classes and the poor should pay more taxes to fund such benefits as Medicare, Medicaid, and Social Security, though federal taxes do not fund those benefits.

The GOP’s stated concern that additional IRS agents would attack the low-paid is camouflage for their genuine concern that additional agents would focus on the rich.