Many federal programs, for instance, poverty aid, foreign aid, global warming prevention, immigration, education, etc., are unaffordable and unsustainable.

How many of these beliefs do you have? Every one of them is wrong, proven wrong by readily available data (here, here, here, here, and elsewhere in this blog).

Yet most people strongly defend one or more of these wrong beliefs, even without any evidence to support them.

Here is an example of the widespread belief that immigrants harm our economy, and our way of life.

Immigration fuels US economic growth while politicians rage.Augusta Saraiva and Enda Curran, Bloomberg NewsWhile the rising number of immigrants in the U.S. has sowed division among politicians across the country — and stoked angst among a swath of voters — there’s one place where almost everyone seems on the same, upbeat page: Wall Street.

Last month, the nonpartisan Congressional Budget Office (CBO) calculated that immigration will generate a $7 trillion boost to gross domestic product over the next decade. The agency came to that conclusion after incorporating the recent surge in immigration.

The CBO release spurred a flurry of fresh number-crunching among investment bank economists to account for the boost those newcomers are giving to the labor force and consumer spending. Goldman Sachs Group Inc. revised up its near-term economic growth forecasts Sunday.

JPMorgan Chase & Co. and BNP Paribas SA were among banks that acknowledged the economic impact from surging immigration in recent weeks.

We’ll pause to remind you that Gross Domestic Product (the most common measure of our economy) = Federal Spending + Non-federal Spending + Net Exports.

Inflation-Adjusted, Per Capita, Gross Domestic Product

Spending by immigrants increases per capita (including yours and mine) inflation-adjusted GDP. In short, immigrants make us all wealthier by working, paying local taxes, and creating and buying stuff.

That is what immigrants have done for decades, and it is what has made America prosperous.

“Immigration is not just a highly charged social and political issue, it is also a big macroeconomic one,” Janet Henry, global chief economist at HSBC Holdings Plc, wrote in a note to clients Tuesday.

No advanced economy benefits from immigration quite like the U.S., and “the impact of migration has been an important part of the U.S. growth story over the past two years.”

“Two years”? More like two hundred years.

Morgan Stanley economists Sam Coffin and Ellen Zentner noted this month that faster population growth fueled by immigration leads to stronger employment and population estimates than initially thought, though they added that the full effect might not be captured by official data.

It’s hard to pin down the exact scale of the inflows of foreign-born people, thanks to many entering without visas or other documentation. But CBO statisticians incorporated data from U.S. Customs and Border Patrol to come up with their higher projected net immigration, according to Morgan Stanley analysis.

Goldman estimates that immigration was around 2.5 million in 2023, a figure that is far above the 1.6 million implied by the change in the foreign-born population in the official household survey from the Census Bureau.

The positive tone among economists contradicts that seen on the campaign trail, as a surge in the number of undocumented immigrants entering the U.S. through the southern border stokes political strife.

The share of Americans who see immigration as the most important problem facing the U.S. is now matching a record high in data going back four decades, according to a recent Gallup poll.

The recent boost from immigration is the result of both more legal immigrants as the U.S. goes through unprecedented visa backlogs and the surge in illegal border crossings.

The nation’s 32.5 million immigrant workers now account for roughly one in five U.S. workers, a record-high in government data going back almost two decades.

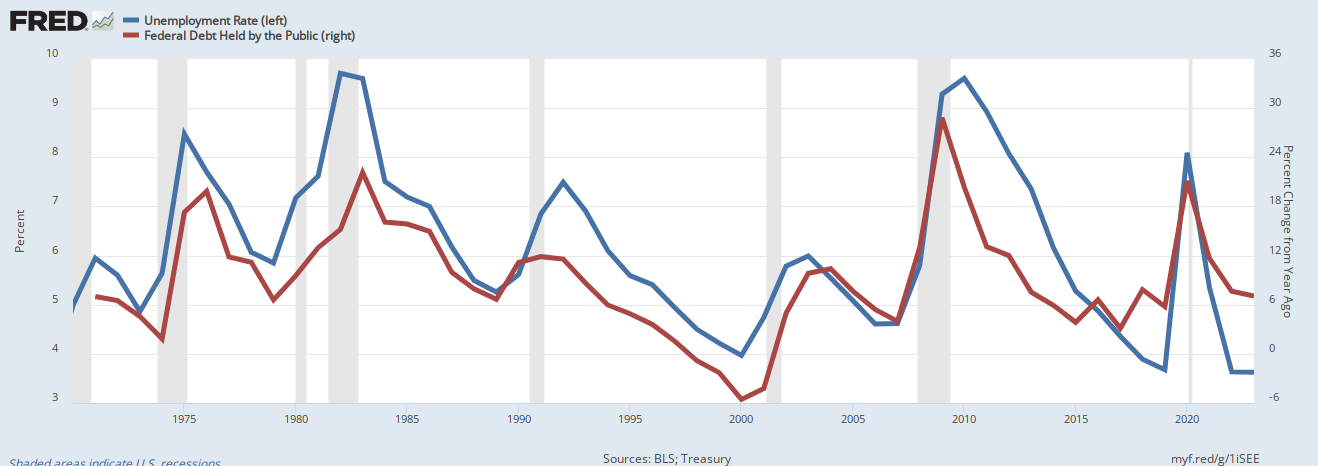

They not only are working, but their buying creates jobs. They aren’t stealing jobs as America’s xenophobes often claim. The proof: Unemployment is low “despite” (because of?) massive immigration:

Red line is federal deficits. Blue line is Unemployment. Vertical gray bars are recessions.

This interesting graph reveals several facts:

When federal deficit spending declines, we have recessions.

The recessions are cured by increases in federal deficit spending.

The recessions cause unemployment.

The unemployment, which is caused by decreases in federal deficit spending is cured by increased federal deficit spending.

Thus, unemployment is not caused by immigrants taking jobs. Quite the opposite. Unemployment and recessions have the same cause: Insufficient federal deficit spending, exactly what the conservatives want us to do.

To be sure, the connection between the higher influx of foreign workers and the rapid post-pandemic recovery has been noted by economists and policymakers alike for some time now.

The Trump GOP’s main election focus is to deport undocumented immigrants, the people who help grow America’s economy.

Federal Reserve Chair Jerome Powell has repeatedly cited immigration as one of the reasons behind strong economic growth.

In a reference to the role being played by higher labor supply, Powell pointed on Wednesday to “a strong pace” of immigration as helping on that front.

“The overall picture is a strong labor market — the extreme imbalances we saw in the early parts of the pandemic recovery have mostly been resolved, you’re seeing high job growth, you’re seeing big increases in supply,” Powell said in his press conference Wednesday.

Fed policymakers lifted their growth forecast for this year to 2.1% from 1.4%, their median estimate showed.

Businesses are ramping up calls for changes to bring in more workers through legal channels.

Almost 9 million positions are open across the economy, equal to 1.4 jobs for every job-seeker. Foreign-born workers made up a record 18.6% of the civilian workforce in 2023 and the U.S. approved a record number of work authorizations in the fiscal year through last September.

Immigration is “very policy sensitive,” Feroli cautioned, advising against extrapolating out bigger numbers beyond the end of this year. After all, policy could change after the November election, he noted.

Why does Trump and his GOP harp on immigration as America’s biggest “problem”? His success is as a fear-mongering hate-mongerer.

When he preaches hatred toward Muslims, Mexicans, gays, blacks, people from “shithole” countries — when he lies that they bring crime, drugs to America, he is preaching to people he has frightened with his bigotry. He creates scapegoats, and then claims he will deal with them.

Hitler did it. All dictators do it.

The facts are:

False beliefs, especially those repeated for months and years, are difficult to dislodge with facts. But ultimately, that is all you can do.

Just as a lie gains strength the more it is repeated, so does the truth. Learn the truths and repeat them again and again. It’s the only way to defeat the Hitlers of the world.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

I believe the people at AARP understand that our government, being Monetarily Sovereign, never can run short of its own sovereign currency, the U.S. dollar.

They must know that even if all federal tax collections — income taxes, payroll taxes, etc. — and every other form of federal government income totaled zero, the government could continue spending forever.

The sole purposes of federal taxes (unlike state, local taxes) are not to provide the government with spending money, but:

To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward.

To assure demand for the U.S. dollar by requiring taxes to be paid in dollars

And the hidden reason: To help the very rich become richer by widening the Gap between the rich and the rest.

Stated simply, the U.S. federal government can pay for anything it wishes without taxing anyone.

AARP claims it “is the nation’s largest nonprofit, nonpartisan organization dedicated to empowering Americans 50 and older to choose how they live as they age. Advocating for people age 50-plus is at the heart of our mission.”

So why does the AARP repeatedly indicate the federal government can’t afford to pay for a comprehensive, no deductible Medicare benefit for every man, woman, and child in America?

Could their lucrative insurance business be the reason?

Here are excerpts from an article in the October, 2023 AARP Bulletin: (By Dena Bunis, who covers Medicare, health care, health policy and Congress. She also writes the Medicare Made Easy column for the AARP Bulletin. An award-winning journalist, Bunis spent decades working for metropolitan daily newspapers, including as Washington bureau chief for The Orange County Register and as a health policy and workplace writer for Newsday.)

For decades, as Americans approached their 65th birthday, all they had to do to get Medicare, the nation’s government-sponsored health insurance for older adults, was sign up.

The program wasn’t all that complicated. You went to the doctor armed with your Medicare card. Your physician or hospital took care of you and billed Medicare. Then you —or the supplemental (Medigap) planyou bought — paid your out-of-pocket share. Easy.

Today’s Medicare isn’t your grandparents’ program. New enrollees have an immediate big decision to make: Should they enroll in original Medicare (also referred to as traditional Medicare) or sign up for the private insurance managed care alternative, Medicare Advantage (MA)?

But why? Why is a decision needed?

AARP doesn’t explain why there are two plans, and why people are forced to choose between them. AARP also doesn’t explain why everyone, young or old must pay for some form of healthcare insurance, or have an employer pay.

In short, AARP doesn’t discuss the true question: Why doesn’t the federal government simply pay for everyone’s healthcare?

AARP profits by providing in their words, “health security, financial stability and personal fulfillment. AARP also works for individuals in the marketplace by sparking new solutions and allowing carefully chosen, high-quality products and services to carry the AARP name.”

Clearly, Medicare for All would be a financial disaster for AARP.

The two options not only differ in how they operate but increasingly in what coverage and services they provide. Making the decision requires looking down two roads that more and more are heading in different directions.

Original Medicare’s biggest draw remains the freedom enrollees have to go to any doctor or hospital in the country that takes Medicare.

In most cases, you don’t need a referral to go to a specialist or get a covered procedure done. It’s a simple fee-for-service insurance structure that was once commonplace across America but has mostly vanished for those under 65.

InMedicare Advantage, plans can feel more familiar, as they closely resemble the managed care plans offered by many employers, often in the form of a health maintenance organization (HMO) or preferred provider organization (PPO).

An MA plan is the one-stop-shopping alternative that bundles hospital, doctor and prescription drug coverage.

Most offer extra benefits not in original Medicare. MA plans also cap how much beneficiaries must pay out of pocket each year, something original Medicare does not.

The sole purpose of government is to improve and protect the lives of the people. That said, there is no reason why a federally funded plan cannot do everything Medicare + Medicare Advantage + every company-funded plan does — and without charging the American people one cent.

That is one way our government should improve and protect our lives.

(And no, this isn’t “socialism,” which is government ownership and control. It’s merely government funding, which is what the government currently does millions of times a day.)

Another big difference: Original Medicare is managed entirely by the federal government (oversight by Congress, day-to-day operations by the Centers for Medicare & Medicaid Services (CMS), meaning it is not operated for a profit.

That’s not exactly correct. The payment is managed by the government, but the services come from the private sector. The doctors, hospitals, the technicians, etc. are in the private sector.

The exception is the VA health system, which is owned and operated by the federal government.

Advantage plans, by contrast, are operated by private and often for-profit organizations that get flat-rate payments from the government to provide health care to an enrollee.

The financial difference is more apparent than real. The federal government still pays, but with Medicare Advantage, private insurance companies and their profit requirements are inserted as (unnecessary) middlemen between the providers and the government.

MA’s promise of extra benefits and lower premiums has been effective. In 2008, only 22 percent of beneficiaries were in Advantage plans. Since then, enrollment in these managed care plans has more than doubled and continues to grow.

In 2023, more than half of Medicare’s 60 million beneficiaries who have both Medicare parts A and B are enrolled in an MA plan.

And that’s the irony of the entire system. The government pays for both medical plans, but they offer different benefits. Medicare could (and should) offer the same or even better benefits MA offers. But it doesn’t.

Why? Because Americans have been brainwashed into believing that Medicare “can’t afford” to provide such benefits, and that in some mysterious way, Medicare can run out of money.

Medicare now finds itself at a crossroads. Based on current patterns, it won’t be long before enrollment in MA plans substantially overtakes enrollment in original Medicare.

Does the original need to be changed to remain competitive with MA? More fundamentally, will original Medicare as envisioned by President Lyndon Johnson and Congress in 1965 cease to exist in the years to come?

“I genuinely do believe that the future of Medicare lies in Medicare Advantage,” says James E. Mathews, executive director of the Medicare Payment Advisory Commission (MedPAC), established by Congress to analyze the program and provide advice. Mathews expects there will be a “natural migration” to MA, but he’s not sure whether that means original Medicare will disappear.

“It remains to be seen whether there is going to be some subset of the Medicare population for whom Medicare Advantage simply will not work.”

Medicare and Medicare Advantage will work if the benefits of both plans are blended into a Medicare for All plan.

Preserving and strengthening Medicare is one of AARP’s key policy concerns. That includes maintaining original Medicare.

“We strongly believe that traditional Medicare should be protected and strengthened and that there has to be a level playing field between traditional Medicare and Medicare Advantage,” says Megan O’Reilly, AARP vice president for health and family issues.

CMS Administrator Chiquita Brooks-LaSure oversees all Medicare operations. She says her priority is to strengthen both options. “I believe it’s critical that people have a choice between traditional original Medicare and Medicare Advantage,” Brooks-LaSure said in aninterview with AARP.

It’s like claiming that people should have a choice between an all-meat diet and an all-vegetable diet. Most people would prefer to blend the two into one complete plan.

Even experts who are most bullish on Medicare Advantage say they don’t expect original Medicare to go away. The main reason is choice.

Chiquita Brooks-LaSure, Administrator of the Centers for Medicare & Medicaid Services. Does she really not know that the federal government can fund one plan that offers every benefit?

The case for keeping original Medicare

Under original Medicare, you can go to any doctor, lab or hospital in the U.S. that participates in the program (about 90 percent of medical professionals do).

In MA plans, enrollees mostly must go to providers within the plan’s network, and these networks are highly regionalized. Going out of network means facing a much higher copay for each visit. In some cases, the care may not be covered at all.

“There are always going to be a lot of people who are going to say, ‘Look, I want to go to a doctor I want, and I don’t want to be limited,’ ” says Tom Scully, who was CMS administrator from 2001 to 2003 and is a supporter of Medicare Advantage. As a result, “I think original Medicare will never go away.”

“I believe it’s critical that people have a choice between traditional original Medicare and Medicare Advantage.”

— Chiquita Brooks-LaSure, CMS Administrator

Until they enroll, many Americans don’t realize how costly and complicated Medicare can be. That is especially true if you choose original Medicare.

Most original enrollees must make three regular insurance payments: one for basic Part B coverage, one for a Part D prescription plan, and one more for a Medigap policy to cover some or all of the expenses that Medicare doesn’t.

And there are other expenses on top of the premiums; for example, original Medicare Part B has an annual deductible ($226 in 2023); there’s also a deductible for every hospital visit, which in 2023 is $1,600. Those charges take a heavy financial toll.

All those premiums, deductibles an lack of coverage are unnecessary. The federal government could, and should fund one program encompassing all benefits. Why force people to forego some benefits?

By contrast, an Advantage plan enrollee usually has just one recurring payment: It includes the government-mandated Part B coverage cost and, in some cases, a small additional premium, which varies by what plan you choose and where you live.

You pay various copays and deductibles for your services and doctor visits, but the rest is fully covered by the plan, and you know going in what the copay is for the different providers. Costs under MA can also add up, though, especially if you need hospital care; most plans have a per-day hospital charge.

An important dividing line when choosing a Medicare path is whether a beneficiary can afford to pay the added monthly costs of a Medigap policy to supplement original Medicare coverage, as well as for a separate Part D prescription plan.

The federal government could and should pay for the above coverages.

The difference in “choice” between original Medicare and an MA plan isn’t simply which doctor you can see.

In an MA plan, the care you need is likely to be more scrutinized than in an original plan.

Insurers that run MA plans often require what’s calledprior authorizationbefore paying for your tests and procedures; that means a doctor must get approval for recommended care from internal reviewers before the treatment will be covered.

Why does MA require prior authorization, while Medicare does not? MA is ruled by the profit motive, while Medicare is ruled by the political motive.

MA can refuse unprofitable procedures. Medicare can afford to fund procedures that have political support, regardless of cost.

Some MA plans also require referrals to specialists, meaning if you wish to see, say, a cardiologist, you’ll need your primary care doctor’s blessing.

People in original Medicare usually don’t need referrals to see specialists, and as long as Medicare covers a test or treatment a doctor orders, except in a few situations, Medicare will pay for it.

If you develop a health condition that requires specialized surgery or highly advanced therapies to treat; in an MA plan, you likely won’t be coveredif you seek care from a doctor or medical center that specializes in your issue but is out of the network.

The above is the result of the profitmotive taking precedence.

On the other hand, most MA plans have benefits that original Medicare does not. The out-of-pocket cap is a big one; in 2023, MA enrollees know they won’t have to pay more than $8,300 in total annual health costs, although many plans have lower out-of-pocket limits than that.

Once again, there is no out-of-pocket cap in original Medicare.

Why are people subject to any out-of-pocket costs, when the federal government has infinite money to pay for medical care? No reason outside of the false claims that the federal government can run short of money.

Most MA plans cover basic dental, vision and hearing services.

Why does Medicare not cover dental, vision and hearing? Again, no good reason. Just the Big Lie about federal finances.

Some provide what are called Medicare flex cards that beneficiaries can use to pay for over-the-counter medications and other drugstore items, as well as healthy food.

In recent years,Congress began allowing MA plansto pay for making improvements to beneficiaries’ homes, such as wheelchair ramps and shower grips in bathrooms. Some plans pay for gym membershipsor transportation to doctors’ offices.

These are benefits the federal government could and should support; they increase the health of the people.

David Lipschutz, associate director of the Center for Medicare Advocacy, supports the ability of Medicare to help pay for nonmedical services that can help keep an older American healthy.

But he says it’s not fair that enrollees must be in a Medicare Advantage plan to take advantage of those extras. “One should not be forced to enroll in a private plan to access such services,” Lipschutz says.

No, it’s not fair that people should be forced to pay for any medical benefits when the federal government has the infinite ability to pay.

Imagine you have a few trillion dollars to your name, and your daughter needs expensive surgery. Would you pay for her the life-saving health care? The government has many trillions. It should follow its mandate to protect our lives.

Advocates and patients agree that MA plans seem fine as long as you’re healthy. But too often, beneficiaries with serious illnesses find it more difficult to get the care they say they need.

A 2022 report from the Government Accountability Office (GAO), a congressional watchdog, found that “Medicare Advantage beneficiaries in the last year of life left the program to join traditional Medicare at twice the rate of other beneficiaries. This could indicate potential problems with their care.”

The profit motive incentivizes private insurance companies to be excellent premium collectors but reluctant health care providers.

“Denials may be more frequent in Medicare Advantage plans than in traditional Medicare for people who have serious health problems,” says Tricia Neuman, senior vice president and head of the Medicare program at KFF, formerly the Kaiser Family Foundation.

That could be a real concern. When people age into Medicare, they tend to be healthier than they will be as they grow older and have more health problems, and that may not be top of mind.”

A federally funded, comprehensive, no-deductible Medicare for All would not have that problem.

Original Medicare may have another disadvantage: television. Throughout the year, but most prominently during Medicare open enrollment season each fall, ads for Medicare Advantage plans blanket broadcast and cable television stations.

From NFL Hall of Famer Joe Namath to “Captain Kirk” William Shatner to Jimmie Walker of “dy-no-mite” fame, celebrities urge older adults to call an 800 number and get lots of extras and benefits from Medicare Advantage plans.

Individual insurers also run ads, and some Medigap plans take to the airwaves. There are no such commercials for original Medicare.

Plenty of money for advertising; not enough for benefits.

“There’s nothing that helps lay out the trade-offs” between original and Medicare Advantage, says Gretchen Jacobson, vice president of Medicare at the nonpartisan Commonwealth Fund. “So if you just pay attention to the Medicare Advantage marketing, you may not really understand what the advantages and disadvantages are.”

“When we did focus groups with brokers, many said they are paid more to put people into Medicare Advantage plans, sometimes much more”

— Gretchen Jacobson, vice president of Medicare at the nonpartisan Commonwealth Fund.

And here is where the profit motive really comes into play:

“When we did focus groups with brokers, many said they are paid more to put people into Medicare Advantage plans, sometimes much more,” Jacobson said. But “if they were going into Medicare tomorrow, most of them said they would choose to be in traditional Medicare.”

These brokers do not get any commission for helping someone enroll in original Medicare. Likewise, they said most Part D prescription plans don’t offer commissions; for those that do, the rate is low.

As for Medigap policies, an agent might get some money for signing people up, but agents say it’s not as much as what they get for a Medicare Advantage enrollment.

The combination of insurance company advertising and insurance broker commissions puts people into Medicare Advantage, when that may not be the wisest choice, and certainly not the least expensive choice (which would be federally funded Medicare for All).

Universal health care for everyone in the United States promises only government inefficiency and health care that ignores the realities of the country and the free market.

“The VA system is not only costly with inconsistent medical care results, it’s an American example of a single-payer, government-run system.

We should run from the attempts in our state to decrease competition in the health care system and increase government dependency, leaving our health care at the mercy of a monopolistic system that does not need to be timely or responsive to patients.

The above supposedly is a negative about Medicare for All, except it isn’t. It is a negative about something no one proposes: VA-style federally owned and operated hospitals with providers being employees of the government.

It’s a fake, perhaps intentionally misleading, negative that no one wants. Medicare for All would be federally funded, not owned and operated. It would be an expanded version of Medicare without the FICA tax.

2. The challenges of universal health care implementation are vastly different in the U.S. than in other countries, making the current patchwork of health care options the best fit for the country.

Though the majority of post-industrial Westernized nations employ a universal healthcare model, few—if any—of these nations are as geographically large, populous, or ethnically/racially diverse as the U.S.

Different regions in the U.S. are defined by distinct cultural identities, citizens have unique religious and political values, and the populace spans the socio–economic spectrum. Moreover, heterogenous climates and population densities confer different health needs and challenges across the U.S.

Thus, critics of universal healthcare in the U.S. argue that implementation would not be as feasible—organizationally or financially—as other developed nations.”

Yes, blah, blah, blah, America is too big, too diverse, too climate-challenged, all great arguments except for one small detail. Medicare already has solved those fake problems. It funds health care all over our big country, and is quite popular, thank you.

3. Government controlis a large driver of America’s health care problems.

Bureaucrats can’t revolutionize health care – only entrepreneurs can. By empowering health care entrepreneurs, we can create an American health care system that is more affordable, accessible, and productive for all,” explains Wayne Winegarden, Senior Fellow in Business and Economics, and Director of the Center for Medical Economics and Innovation at Pacific Research Institute.

Someone please tell Mr. Winegarden that bureaucrats wouldn’t be in charge of revolutionizing anything. They merely would write the checks, just as they do now for Medicare.

4. Universal health care would increase wait times for basic care and make Americans’ health worse.

If coverage was nearly universal, cost sharing was very limited, and the payment rates were reduced compared with current law, the demand for medical care would probably exceed the supply of care–with increased wait times for appointments or elective surgeries, greater wait times at doctors’ offices and other facilities, or the need to travel greater distances to receive medical care. Some demand for care might be unmet.

Rephrasing the objection: “If everyone could get free healthcare, there wouldn’t be enough doctors, nurses, and hospitals to treat us rich folks. It’s better that some poorer people do without, so we don’t have to.”

The same objection could have been made to original Medicare.

However, if the federal government, which can afford anything, pays enough to those doctors, nurses, and hospitals, more people will enter the profession and more hospitals will be built.

It is a fake objection, the purpose of which is to widen the income/wealth/power Gap between the rich and the rest.

5. Universal health care would raise costs for the federal government and, in turn, taxpayers.

Medicare-for-all, a recent universal health care proposal championed by Senator Bernie Sanders (I-VT), would cost an estimated $30 to $40 trillion over ten years.

The cost would be the largest single increase to the federal budget ever.

Here, we have come to the Big Lie in economics, the lie that federal taxes fund federal spending. It is a lie promulgated by the very rich to discourage those who aren’t rich from asking for benefits.

The rich use the confusion between monetarily non-sovereign local and state governments vs, Monetarily Sovereign federal government.

State and local governments cannot create dollars at will, so they rely on tax income to fund their spending. The federal government can create dollars at will, so it does not use tax dollars. In fact, the federal government destroys all your tax dollars upon receipt.

You pay your taxes with dollars from your checking account which are part of the M2 money supply measure. Once your tax dollars reach the U.S. Treasury, they no longer are part of any money supply measure. They effectively are destroyed.

The Federal Reserve creates dollars at willby purchasing securities from a bank (or securities dealer) and paying for the securities by adding a credit to the bank’s reserve(or to the dealer’s account) for the amount purchased. In short, the Fed creates dollars from thin air, whenever it wishes.

Former Fed Chair Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Fed Chair Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Thus, the federal government can, at the touch of a computer key, fund a free, comprehensive, no deductible, Medicare program to protect every man, woman, and child in America.

SUMMARY

There is not a single financial reason why the government doesn’t improve and protect the lives of the people’s health, one of the jobs for which it was formed.

Every argument against free Medicare for all is based on ignorance and/or a lie. In creating Medicare, we already have done the hard part. It is only left to us to expand Medicare while ending all medical taxes and fees, and voila, we have Medicare for All.

Sadly, the rich and the insurance companies prevent the government from doing its job.

You don’t have free, comprehensive, no-deductible health care. Don’t blame “insolvency,” lack of money, inflation, lack of caregivers, or any other factor.

Blame the rich and the private insurance providers like AARP et al, for promulgating theBig Lie.

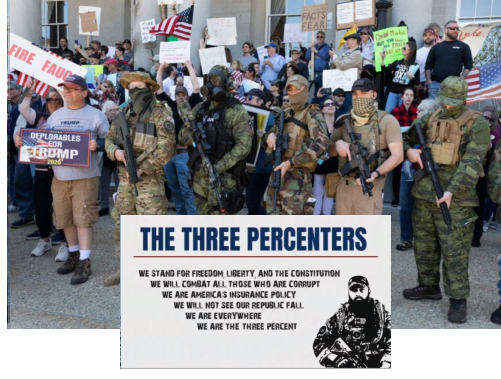

“A well-regulated Militia, being necessary to the security of a free State, the right of the people to keep and bear Arms, shall not be infringed.”

Now that the Supreme Court, in its great wisdom, has decided that the first thirteen words of the 2nd Amendment, unlike every other word in the Constitution, are useless, meaningless, and to be ignored, we can get on with the job of arming every man, woman, and child with high-powered weapons.

Thank goodness, we can count on these guys to protect America.

Heavily armed 400 members of the NFAC (Not Fucking Around Coalition)black militia marches in Lafayette, LA, August 21, 2020

Heavily-armed protesters wearing Proud Boys and Black Guns Matter masks entered the Michigan Capitol Thursday to defend their Second Amendment rights, as lawmakers continue to debate whether to ban guns from the building. Around 1,000 demonstrators gathered on the state Capitol lawn in Lansing throughout the day as part of the annual Second Amendment March that celebrates their right to open carry firearms across the state. Many protesters had AR-15 rifles slung over their shoulders, while many sported paraphernalia in support of extreme right-wing groups and Donald Trump.

There are scores of armed groups, with thousands of members who identify themselves as “militias,” though they are not “well-regulated,” as the useless and meaningless words in the Constitution demand.

From the look of those heavily-armed, “militia” people, perhaps the Supreme Court might have second thoughts about ignoring the well-regulated phrase.

But, I’m sure these guys will come to your defense if the crazy libs force you to receive Medicare, Social Security, and unemployment benefits.

Health Care Spending Is Out of Control Health insurance doesn’t just protect people from financial ruin. It insulates them from individual decisions about price and service quality.

PETER SUDERMAN | FROM THE AUGUST/SEPTEMBER 2019 ISSUE of REASON

Health care in America costs too much because we pay for it the wrong way. And it’s all but certain that we’re going to continue doing so for a very long time.

The crux of the problem is third-party payment, or, as most people think of it, insurance.

The crux of the health care problem in America is insurance??? Americans would be better off if there were no health care insurance???

Pass me another swig of snake oil.

Health insurance doesn’t just protect people from financial ruin. It insulates them from individual decisions about price and service quality.

Those decisions become invisible, outsourced to a middleman—either a private insurer or a federal program—while the patient whose health is at stake is removed from the equation. The result is a system where prices are inscrutable, if they can even be called prices at all.

More spoiler alert: Suderman’s premises are:

Health insurance is bad for America because it relieves you of an impossible task: Shopping for the best and also least expensive hospitals, doctors, nurses, etc. (He later will contradict this nonsense in his own article)

Employees are the ones who actually pay too much for health care insurance when it is provided “free” by businesses. (He doesn’t actually say this, but he should have. It’s the one thing to which I would have agreed.)

Federal taxpayers and the federal government can’t afford to pay for the increasing cost of Medicare. (This demonstrates his colossal ignorance of Monetary Sovereignty and federal financing).

The dominance of third-party payment is almost entirely a result of two policy decisions that have warped the nation’s health care system for decades.

The first was the decision to allow employers to provide fringe benefits, including health coverage, tax-free. This created an incentive for employers to provide more expansive and more expensive coverage.

It made an extra dollar in salary, which would be subject to taxes, worth less than an extra dollar in benefits, which did not incur taxes.

Apparently, Suderman would prefer that employees and employers pay taxes on health care payments, which would reduce the number of companiesthat would pay for it, and the number of peoplewho would receive it.

These reductions would benefit America how? He never says.

The result is that most private insurance is provided through employers, and it tends to be reasonably comprehensive, covering everything from ordinary doctor visits to foreseeable surgeries to truly catastrophic events.

Ooooh, “reasonably comprehensive” health care insurance. This is a bad thing, how? Suderman never says. Apparently, he thinks you should have insurance that won’t pay for . . . what?

Because employers and insurers manage the costs for everything, patients have little incentive to shop based on prices or quality, which can be difficult to determine anyway.

In addition, employers typically pay a large share of the monthly premium, meaning that tens of millions of people are kept ignorant about not only the cost of medical services but the true price of the insurance itself.

Here is where he contradicts his own premise. How many people are capable of intelligently shopping for health care based on prices and quality, which Suderman admits “can be difficult to determine anyway”?

If doctor “A” may be a less skilled diagnostician than doctor “B,” but also is less costly for some procedures, but not for others, by what intelligent criteria can a layperson measure dollars vs. quality of care?

Taking price out of the equation simplifies the task for the average person. Only the very rich can afford to say, “I want the best, no matter the cost.”

As for the rest of us, are we would be left to say, “I can’t afford the best health care, so I’ll settle for the surgeon with the shaky hands.”

Seemingly, that is what Suderman wants for you.

The second policy decision was the introduction of Medicare (and, to a lesser extent, Medicaid) in the 1960s.

Medicare expanded a system of government-run third-party payment to seniors, who, for understandable reasons, consume an outsized share of health care services.

The result was a huge new revenue stream for the health care industry, which rapidly reorganized itself around extracting funds from the program—which is to say, from American taxpayers—by any means possible.

Apparently, Suderman thinks Medicare is a bad thing, because it provides “a huge new revenue stream for the health care industry.” The fact that it happens to provide affordable medical services for the elderly is not really a consideration to Suderman.

And there it is again, the ignorance of federal financing. After all these years of promulgating misinformation, Suderman hasn’t learned that state taxpayers fund state spending, and local taxpayers fund local spending, but federal taxpayers do not fund federal spending.

Former Fed Chairman, Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

(The federal government is Monetarily Sovereign. State and local governments are monetarily non-sovereign.)

Suderman’s ignorance about this basic fact is pitiful.

In the first year alone, average daily charges for U.S. hospitals shot up by 21.9 percent, according to professors Ted Marmor of Yale and Jon Oberlander of the University of North Carolina at Chapel Hill.

The rate of growth of physician fees more than doubled in the year between the law’s passage and Medicare going into effect.

During the first five years of the program’s existence, reimbursements through the program grew by 72 percent, while enrollment grew by just 6 percent.

And still, America is short of doctors, nurses, and hospital space. But Suderman wants to cut doctor, nurse, and hospital compensation. That should help America.

Better yet, cut Suderman’s compensation, and pay doctors and nurses more. We need more doctors and nurses, and fewer writers that spread disinformation.

In their recent book, Overcharged: Why Americans Pay Too Much for Health Care (Cato), Silver and Hyman argue that the U.S. health system is best understood not as a means of delivering the best possible care but as a system for funneling as much money to health care providers as possible.

Medicare, they note, will pay for countless expensive in-hospital tests and treatments for a dying individual but not less expensive palliative care offered in that same individual’s home.

Suderman not only wants less money for doctors, nurses, and hospitals, but less for tests and treatment of “dying individuals.” (“We’re cutting off your treatments, Mr. Jones. You’ll be dead in a month, anyway, so this will just make it come a bit sooner. We hope you don’t mind.”)

And yes, the government should pay for palliative home care, just as it pays for hospice (though Suderman probably would complain about that, too, because he complains about all federal spending).

There are few meaningful checks on doctor reimbursements under the program; fraud and waste are pursued after the fact (if at all), which means doctors can always be assured of payment.

Wrong. Medicare and all private insurance companies do place limits on doctor reimbursements. In fact, Medicare’s limits are too low. Suderman surely knows this, so why does he claim otherwise?

Suderman claims your doctor is a wasteful fraud. Apparently, most doctors are, if Suderman says so.

He doesn’t like it that your doctor is “assured of payment.” Better that your doctor should have to sue or beg for payment??

The tax carve-out for employer-sponsored insurance pushes people into more comprehensive coverage, which increases overall demand for health care services, which makes health care providers more money.

If there is anything that angers Suderman, it’s people like you receiving the same “comprehensive coverage” he has.

And having such good care makes you go to the doctor when you aren’t even sick, right? Because you love getting stuck with blood test needles, and enduring digitals, just for the fun of it.

Suderman, who probably has comprehensive coverage, doesn’t want you to understand that overall demand increases when earlier programs were substandard.

It was as if the system was designed with only one goal in mind—maximizing not health or patient satisfaction but the amount of money Americans spend on health care.

The fiscally ruinous results speak for themselves.

Yes, the fiscally ruinous results of not having comprehensive care, have greatly been reduced by health care insurance. Apparently, Suderman believes only rich people deserve comprehensive care.

Silver and Hyman note that the Surgery Center of Oklahoma, a clinic that posts prices online and focuses on patients who pay cash, charges less than $20,000 for a knee replacement; the average price paid across the country is $57,000.

Uh, Peter, who are the people who can afford to pay $20,000 cash for a knee replacement? That’s right, the rich. They are the ones who trot to the Surgery Center of Oklahoma for the best care.

And what happens to the people who can’t afford $20,000 cash? Presumably, the Surgery Center of Oklahoma turns them away.

Fortunately, most people have that health care insurance you so despise.

And, the others just limp along on bad knees.

Direct payment by quality-conscious consumers is an effective way of bringing down costs and total spending. Which is exactly why it will never happen at scale.

No, direct payment by consumers won’t happen because it already has been tried, here and everywhere.

It’s called, “doing without insurance.”

Heading into the 2020 election, Democrats have proposed multiple ways of expanding Medicare, including pushing Medicare for All, a single-payer system in which the government finances nearly all health care services in the United States.

Right. And what exactly is wrong with that? Suderman never says.

The failed 2017 (Republican) effort to “repeal and replace” Obamacare would have left much of its infrastructure, including most of its spending, in place.

“ . . . Left much of its infrastructure (and) most of its spending in place“??? What the hell is Suderman talking about? He has zero idea about what would be “left in place.” He’s just babbling ignorance.

And what spending would be “left in place”? Spending by whom? Surely not by the government. It’s the spending that the GOP wants to cut.

The best hope for change is very bleak indeed. Medicare is racing toward a predictable fiscal crisis. The program’s actuaries predict it will be insolvent in 2026, able to pay only about 89 percent of its bills. That percentage will drop below 80 percent in the coming decades.

The system as it exists today, in other words, is unsustainable. It simply can’t go on like it is—and if Congress continues to do nothing, it won’t

And then we finish off with the old “federal spending is unsustainable” lie. It’s the same lie that Suderman and those of his ilk have been telling since 1940 –even before he was born.

The most important problems in economics involve the excessive income/wealth/power Gaps between the richer and the poorer.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps:

Chiquita Brooks-LaSure in Washington, DC, on August 23, 2023.")