Discovery is realizing that the great thinkers are wrong.

Every great thinker is known as a great thinker because he/she showed how previous great thinkers were wrong. Subsequently, he will be shown to be wrong. That is called “science.”

Einstein’s gravity theories showed Newton’s gravity theories to be wrong. And though Einstein’s have stood for a century, they are incompatible with quantum mechanics, so there is a strong likelihood part of Einstein will be proved wrong.

In the previous post, On second thought, I was wrong. It’s not stupidity; it’s reasonable terror, I criticized a Chicago Tribune columnist for quoting the economics party line (aka “The Big Lie”) that federal finances are like personal finances.

His response was to send me the following survey, to prove his point:

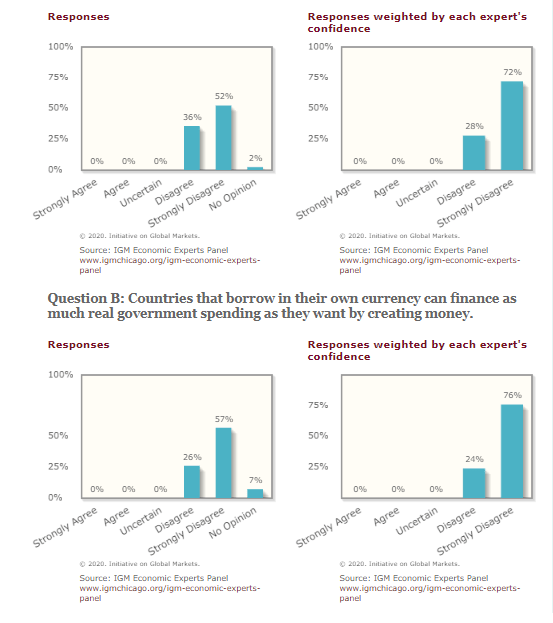

========================================================================================================================================================

Question A: Countries that borrow in their own currency should not worry about government deficits because they can always create money to finance their debt.

========================================================================================================================================================

In the above survey, no economist agrees with the two statements, both of which are provably correct. Those economists who made additional comments to justify their opinions invariably mentioned inflation.

The near-unanimous belief was that creating “too much” money causes inflation, which is widely believed, but factually untrue.

Name any inflation, by country and year, and you will find that the inflation began with a scarcity, most often of food or energy. It was only in response to the scarcity, that a nation begins “printing” money

That is why the illusion of “money creation causes inflation” persists.

Here are examples of clarification comments by those who disagreed with the statements:

Marcus Brunnermeier, Princeton: “see numerous historical examples: Germany in 1920s, Latin America, …”

In every historical example, the inflation is precipitated by a food and/or energy shortage.

Darrell Duffie, Stanford: “The present value of debt issuances is equal to the present value of debt payments. So, borrowing more now means paying more later.”

Duffie provides a mere tautology that neither disproves nor proves the statement.

Ray Fair, Yale: “Surely inflation might be a problem.”

Austan Goolsbie, University of Chicago: “‘Always’ makes an ass out of you and me (reminding for a friend)”

I included this one not only because it is humorously inane — he was trying to be clever about the word “assume,” but got it confused with the word “always” — but it’s an example of an expert quoting something about which he has no knowledge.

Oliver Hart, Harvard: “This kind of behavior can quickly lead to inflation or even hyperinflation once the economy is close to full capacity.”

What will be the symptoms of an economy that is close to full capacity? Right. Shortages. It is shortages that cause inflation.

Kenneth Judd, Stanford: “A government may be able to do this once but doing this systematically will make it impossible to sell bonds in the future.”

Except: 1. If the government decides not to sell bonds or 2. If the central bank buys the bonds. The U.S. government doesn’t need to sell a single bond to acquire U.S. dollars. It creates a dollar, ad hoc, every time it spends a dollar.

Anil Kashyap, Chicago: “Money financing yields some seigniorage, but also inflation and the inflation has costs and there are limits to seigniorage capacity.”

A Monetarily Sovereign government needs no seigniorage (i.e. money creation profits).

Eric Maskin, Harvard: “Printing money causes its own problems, e.g., the risk of inflation”

Same old, same old. And wrong.

Robert Shimer, Chicago: “The real value of the money supply is bounded above. At some point, this must create inflation.”

What does “at some point” mean? He has no idea. The “ticking time bomb” claim has been made for 80 years, and still, we experience no explosion. Now that we are sliding into depression, they still worry about inflation. Insane.

AAron Edin, Berkeley: “There are limits to capacity and no limits to wants.”

So? What does that tell you? There are limits to the universe, too. Where are the limits? Should we stop firing rockets because they may fly out of the universe?

Kenneth Judd, Stanford: “Friedman wrote a book “There’s No Such Thing As a Free Lunch.” He also meant road or bridge or army or school or ANYTHING!”

And exactly what are those limits? The 80-year, 50,000% increase in federal debt hasn’t reached those “limits,” so what are the limits? He has no clue. But there is a “free lunch.”

And here are a few more comments from those whose comments already have been shown:

“. . . lots of countries have proved this to be impossible” Not Monetarily Sovereign countries

“There will come a point where the currency is so debased that further spending becomes difficult if not impossible.” The old “a point” that no one can identify.

“At some point, hyperinflation would break it all apart. However, this is an irrelevant question in an open world.” Some point. A point. Ah, that mysterious point,

“Creating money can finance a great deal of spending, but incidents of hyperinflation, collapse, and other crises indicate there are limits.” Except that every hyperinflation has been caused by shortages, and cured by deficit spending to cure the shortages.

“I don’t like this question. I guess it is true in some sense, but surely inflation looms at some point.” Surely — at some point, somehow, somewhere, maybe.

In summary, the vast majority of economists parrot each other, and the more they hear the same thing, the more believable it is. Herd mentality.

So now, with no evidence of support, they offer two objections to federal money creation:

- The federal government should live within its “means.”

- The federal government doesn’t need to live with its means, but at some unknown point, that would cause inflation.

And those two false statements are the total of economics, today, which is mouthed and printed everywhere.

Meanwhile, the people of the world are starving, because of that drivel.

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell

Search #monetarysovereignty Facebook: Rodger Malcolm Mitchell

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

The most important problems in economics involve:

- Monetary Sovereignty describes money creation and destruction.

- Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

2. Federally funded Medicare — parts A, B & D, plus long-term care — for everyone

3. Provide a monthly economic bonus to every man, woman and child in America (similar to social security for all)

4. Free education (including post-grad) for everyone

5. Salary for attending school

6. Eliminate federal taxes on business

7. Increase the standard income tax deduction, annually.

8. Tax the very rich (the “.1%”) more, with higher progressive tax rates on all forms of income.

9. Federal ownership of all banks

10. Increase federal spending on the myriad initiatives that benefit America’s 99.9%

The Ten Steps will grow the economy and narrow the income/wealth/power Gap between the rich and the rest.

MONETARY SOVEREIGNTY

Ahh, the Chicago Tribune, famous for its headline of “Dewey Defeats Truman” in 1948. FWIW, Dewey was one of the last “R”s to run for president, including Ike, that was worth the powder to blow to hell. And we’re still talking about currency debasement!!

Well, that sent Herbert Hoover down the river to perdition with his insistence on maintaining a gold standard and trying to balance the budget in a recession that turned into a depression; amazing for an intelligent man.

That said, we’d be better off with him in the Oval Office now than the orange-tinted fraud now occupying said space.

LikeLike

The Nobel Prize for economics has been awarded for 50 years and still no real progress on the horizon. Lots of graphs, equations and charts but…zzzzzzz.

Once you get a Ph.D in economics, you’ve got a barb-wire fence around you that can’t be penetrated by ideas that differ from your training.

This Covid virus may prove to be the undoing of traditional economics if no solution is found quickly; government is financially bleeding to death. How do you Fed-feed everything if few are working and insufficient revenue coming in? Won’t this force the MS truth-cat out of the bag?

LikeLike

While some economists are merely shills for the moneyed interests, there are many that are simply fearful that MS/MMT could lead to runaway spending. Paul Samuelson articulated this in this quote that likened deficit concerns to “old time religion”:

“I think there is an element of truth in the superstition that the budget must be balanced at all times. Once it is debunked, that takes away one of the bulwarks that every society must have against expenditure out of control. There must be discipline in the allocation of resources or you will have anarchistic chaos and inefficiency. And one of the functions of old fashioned religion was to scare people by sometimes what might be regarded as myths into behaving in a way that the long-run civilized life requires”

Contrary to the orthodox narrative, MMT argues that deficit spending needs to be in response to specific policy objectives and the fiscal aspects should be designed to minimize risk of inflation or under employment. It’s always been about balancing resources and demand. Stephanie Kelton coined the term “deficit owls” (in contrast to the current hawk and dove species that dominate the conversation). Deficit Owls would:

1) Recognizes that federal deficits are neither good nor bad but merely reflect private sector savings preferences

2) Assigns no arbitrary limit to the size or duration of the deficit

3) Advocates deficits when there is slack (i.e. under utilization of resources) in the economy

4) Supports austerity only as anti-inflation measure

5) Calls it fiscally irresponsible to permit chronic unemployment or high inflation

As Randy Wray recently wrote in the Guardian (link below): No amount of money can deliver more PPE and ventilators if you lack the resources to produce them. Just as in WWII, we are adjusting our manufacturing resources (no thanks to Trump) to produce less of what we don’t currently need (e.g. automobiles) and more of what we do (ventilators and face shields). What we really need at the federal level are better leaders and more rational adults in the room to advise them.

https://www.theguardian.com/commentisfree/2020/apr/17/coronavirus-deficit-american-economy

LikeLike

My response:

1. Deficits are good, never bad, always necessary for an economy to grow. EVERY time we don’t have a federal deficit we have a recession or a depression. Even insufficient deficit growth leads to recessions.

2. Agreed. No arbitrary limit.

3. There always is “slack.” Even during WWII there was “slack,” i.e. room for growth. In human history, there never has been an economy with no “slack.” (Japan has few resources, but plenty of slack.)

4. Austerity is the single worst idea in all of economics. It is a lousy anti-inflation measure. Austerity causes recessions. Recessions are not the opposite of inflations.

Inflation is always caused by scarcities, not by excess money. Scarcities can be cured by federal deficit spending. Thus, counter-intuitively, deficit spending can cure inflation.

5. Agreed. It is fiscally irresponsible to permit chronic unemployment or high inflation, except the MMT “jobs guarantee is a bad way to fight unemployment, and austerity is a bad way to fight inflation.

LikeLiked by 1 person

As for Randy Wray, he simply is wrong. Describe the circumstance in which added money could not create the resources to deliver more PPE and ventilators. Money creates resources.

But then, Randy still is the JG guy, so what can I say?

LikeLike

I agree, more money creates more resources, eventually. It’s often more about how quickly an economy can adapt to sudden changes in supply/demand, including utilization of excess capacity or re-purposing existing capacity depending on needs.

In the U.S. there are probably few if any circumstances, as we have had chronic excess capacity in the economy for quite some time. Industry is now rapidly adjusting to produce more PPE, ventilators, hand sanitizer, treatments, etc., which more money will buy, only because there is abundant excess manufacturing capacity due to collapsed demand for other goods and services. Similar reductions in demand for normal consumer items existed during WWII, which allowed the conversion of industry to support war production.

Example: Tom Bihn, manufacturer of high end travel/business bags in Washington, has converted virtually all of their available manufacturing capacity to produce reusable cloth masks, since demand for backpacks and travel/business cases has fallen to near zero. If we had to build new plants to increase supply of masks or ventilators, no amount of money would deliver those items today or even next month.

We are currently spending millions if not billions of dollars on vaccine and treatment development for covid-19. We could double or triple those amounts, and it wouldn’t make the vaccine come any faster, as we lack the key resource of available technology to do that quickly and safely.

Of course shortages of PPE and ventilators only result in an increase in price for these items (and more unfortunately increased deaths), not general inflation as when you have shortages of key commodities such as energy or food.

When you look at examples of high general inflation or hyperinflation in history, more government spending did not secure more resources, just more inflation, at least over the short term, as the economies were not able to quickly adapt to the shortages.

LikeLiked by 1 person

The only reason why government spending would not cure inflation is if the spending was not directed at the scarce food or energy. All hyperinflation can be cured if the government will use its monetary sovereignty to purchase food and/or energy (whichever is scarce), and distribute it to the populace. You cannot have hyperinflation if both food and energy are in long supply. Simply can’t happen.

Once one accepts that principle, the solution becomes obvious.

LikeLike