Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

Mitchell’s laws:

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money.

•The more federal budgets are cut and taxes increased, the weaker an economy becomes..

•Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

•The single most important problem in economics is the Gap between rich and poor.

•Austerity is the government’s method for widening the Gap between rich and poor.

•Until the 99% understand the need for federal deficits, the upper 1% will rule.

•Everything in economics devolves to motive, and the motive is the Gap between the rich and the rest..

============================================================================================================================================================================================================================================================

In your opinion, which scientist is best equipped to understand economics:

- A physicist?

- A mathematician?

- A psychologist?

- A chemist?

Choose one.

Personally, I would choose the psychologist, because economics essentially is psychology.

While physics, mathematics and chemistry rely on specific, proven, reproducible relationships, economics almost wholly is arbitrary and subjective.

I’ll give you a painful example.

Commodity pricing is a function of economics. Years ago, I owned a commodity brokerage, where we employed a prize-winning chartist. (I can’t recall the name of the contest he won, but he and all the other entrants had to use charting techniques to predict various commodity prices.)

When we discussed his system, he spoke very authoritatively of “support levels,” “trend lines,” “resistance,” etc., all under the name, “technical analysis,” and it all sounded quite scientific.

Here is what stockcharts.com says:

Support is the price level at which demand is thought to be strong enough to prevent the price from declining further. The logic dictates that as the price declines towards support and gets cheaper, buyers become more inclined to buy and sellers become less inclined to sell. By the time the price reaches the support level, it is believed that demand will overcome supply and prevent the price from falling below support.

Support does not always hold and a break below support signals that the bears have won out over the bulls.

A decline below support indicates a new willingness to sell and/or a lack of incentive to buy.

Support breaks and new lows signal that sellers have reduced their expectations and are willing sell at even lower prices.

In addition, buyers could not be coerced into buying until prices declined below support or below the previous low. Once support is broken, another support level will have to be established at a lower level.

If you detect the faint aroma of bovine excrement, I don’t blame you. In essence “support” is an arbitrary line, meaning nothing.

Charting, as a means to predict commodity prices, works sometimes and doesn’t work sometimes. In other words: It doesn’t work.

So sadly, our prize-winning chartist later proved spectacularly unsuccessful in predicting prices in the real world, and those of our customers who relied on his prognostications lost money.

Charting still is widely used as a predictive commodity pricing tool.

The use of charts to predict economic events is typical of economics as a science, because we economists have the compulsive urge to prove we are “real scientists,” and as “everyone knows,” real scientists base their hypotheses on mathematics, especially graphs.

I do it. We all do it. But that doesn’t make it smell any better.

The problem, of course, is that economics is a reflection of human psychology. Even worse (i.e. more deceiving) is the fact that economics also is a reflection of real physical processes. It’s a blend.

Consider what might be the most basic equation in all of economics: Value = Demand / Supply.

It says that increased Demand and/or decreased Supply (scarcity) increases Value (as measured by price). Intuitively logical.

Value, though, is complex. What is the price of a TV set? The answer depends on many variables: Size, model, manufacturer, retailer, location, date.

And Supply is equally complex. It too depends on those variables.

But ultimately, one can measure Supply and Price. They are finite. You can walk into a store and see that the store has three of a specific item at a specific price.

But how does one measure Demand?

While Value (price) and Supply can be set arbitrarily, Demand cannot.

Demand is related to motivation, which is buried in the human psyche. How do you measure a population’s motivation to buy a Porche, a pansy or a pickle? You only can do it derivatively and approximately.

That is, when economists know the Price and the Supply, they can derive the approximate Demand. But, if they don’t know both the Price and the Supply, they cannot know or determine the Demand.

The inherent weakness of the equation Value = Demand/Supply, applies to most equations in economics. They are ruled by the variables of human psychology.

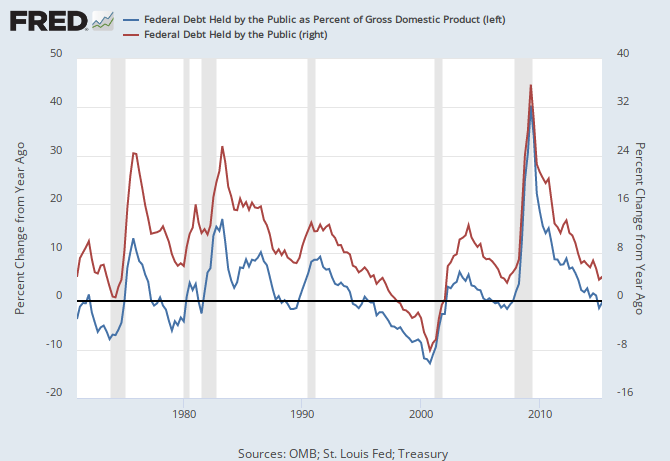

At the bottom of this post is a graph indicating that reductions in federal deficit spending lead to recessions.

It is not like a graph that shows, for instance, the relationships among distance, time and speed (Distance = Time x Speed). They are not functions of psychology. Each can be stated with exact precision.

The graph at the bottom of this page encompasses thousands, no trillions, of human actions and decisions, which unless you believe in determinism and not in free will, are beyond measure and prediction.

Thus, my chartist employee’s efforts to predict commodity prices were doomed from the beginning. Unpredictable and unmeasurable factors affected the outcome.

In most nations, and surely in America, the single biggest unpredictable economics factor is actions by the central government.

Will it create a war? Change interest rates? Deficit spend? Allow or reject immigrants? Allow or prevent the use of resources? Almost anything the central government does affects the economy.

The government is composed of human beings, each of whom is affected by other human beings, as well as being affected by health, weather, threats, anticipated and unanticipated events, fear, hope, greed — the list goes on and on.

The graph (below) indicates we have come dangerously (and unnecessarily) close to recession. But when people ask me, “When will we have the next recession?” my answer always is, “Tell me what the federal government will do, and I’ll tell you when we’ll have the next recession.”

Compare that vague answer with the specific answer a physicist will give you if you ask him how long it will take a photon to travel a mile, or a mathematician will give you if you ask a question about set theory.

I suspect a physicist, a mathematician or a chemist would become exasperated with the pretensions of economists.

Look in any economics textbook and you will see it is loaded with graphs and formulas, almost none of which are more than approximations, and usually less, but appearing to be much more.

If I tell you reductions in federal deficit spending lead to recessions and depressions, that statement is about as accurate as economics can be. There is no formula, no proof, that can improve on that statement for accuracy.

I can show you the many times when reductions in federal deficit spending did, in fact, lead to recessions and depressions. But repetition is not scientific proof. Physicists know that.

I have awakened 30,000 consecutive mornings, but even that massive repetition does not prove I always will awaken.

And if someone presents exceptions showing how at certain times, reductions in federal deficit spending did not lead to recessions and depressions, they merely are expressing the variables of human psychology. They neither have proved nor disproved anything.

That is the point of this blog. Economics tries to be — pretends to be — something it is not, and probably never will be: An exact science.

At best, economics is equal to psychology in its accuracy of prediction.

So where does that leave us? Is all useless? Is it fruitless to predict that A –> B? Are we lost in randomness?

Not at all. We still can learn from facts, logic and experience.

Consider federal debt. The politicians, media and economists stress about it, and claim it is similar to personal debt, and is “unsustainable.” But what are the facts?

Federal debt is the total of T-securities outstanding. That is a fact.

Federal agencies own some T-securities. But most are owned by people, businesses or governments other than U.S. federal government.

To acquire a T-security, one must debit a bank checking account and credit a T-security account at the Federal Reserve Bank. T-securities are bank deposits — deposits in accounts in the FRB.

To “pay off” a T-security, the Federal Reserve Bank debits the appropriate T-security account and credits a checking account. This is identical to what any bank does to pay off any savings account.

Those all are facts.

Logically then, since the Federal Reserve Bank pays off federal debt with dollars that already exist in T-security accounts, the federal debt never can be “unsustainable.”

And, our experience is that the U.S. government never has defaulted (i.e. not “sustained”) on its debts — not through recessions, depressions, wars, inflations, deflations or natural disasters.

Does any of this scientifically prove the federal debt always is and will be sustainable? No.

I can visualize scenarios in which the government might default — for instance, Sen. Ted Cruz becoming President.

Because economics is akin to psychology, strict proof of anything is rare. But using our prime tools — facts, logic and experience — we can approach predictability, the goal of any science.

Unfortunately, economists have shunned facts, logic and experience, in favor of abstruse mathematical formulas, to “prove” the unprovable.

Economics and psychology may never have the accuracy of physics, mathematics or chemistry. In striving for that exactitude, economists peer deeper and deeper into minutia, while losing the big picture and the fundamental facts, logic and experience.

(How else can one explain the widespread misunderstanding, within the economics community, of federal debt, deficits and money creation?)

Economics essentially is a “soft” science, like psychology or philosophy. In trying to be part of a “hard” science, economists have gone astray, and done a great disservice to the public, the nation and themselves.

It’s time to get real, economists.

Rodger Malcolm Mitchell

Monetary Sovereignty

===================================================================================

Ten Steps to Prosperity:

1. Eliminate FICA (Click here)

2. Federally funded Medicare — parts A, B & D plus long term nursing care — for everyone (Click here)

3. Provide an Economic Bonus to every man, woman and child in America, and/or every state a per capita Economic Bonus. (Click here) Or institute a reverse income tax.

4. Free education (including post-grad) for everyone. Click here

5. Salary for attending school (Click here)

6. Eliminate corporate taxes (Click here)

7. Increase the standard income tax deduction annually Click here

8. Tax the very rich (.1%) more, with higher, progressive tax rates on all forms of income. (Click here)

9. Federal ownership of all banks (Click here and here)

10. Increase federal spending on the myriad initiatives that benefit America’s 99% (Click here)

The Ten Steps will add dollars to the economy, stimulate the economy, and narrow the income/wealth/power Gap between the rich and the rest.

——————————————————————————————————————————————

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

![]()

No nation can tax itself into prosperity, nor grow without money growth. Monetary Sovereignty: Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

1. A growing economy requires a growing supply of dollars (GDP=Federal Spending + Non-federal Spending + Net Exports)

2. All deficit spending grows the supply of dollars

3. The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

4. The limit to non-federal deficit spending is the ability to borrow.

THE RECESSION CLOCK

Vertical gray bars mark recessions. Recessions come after the blue line drops below zero and when deficit growth declines.

As the federal deficit growth lines drop, we approach recessions, each of which has been cured only when the growth lines rose.

Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

#MONETARYSOVEREIGNTY

Wow..

All sciences are garbage, the only accurate one is Mitchell’s theory….

Im unsure what you refer to by weakness in the demand equation. You dont think we cant quantify the number of cars that will be introduced 2 months from now? Please…

There is no weakness in that equation. Zero. There is weakness in your theory though. Tons..

LikeLike

Zero,

“All sciences are garbage”

Never said or even implied anything like that. Quite the opposite, in fact. Try reading the post, again.

” . . . weakness in the demand equation. You don’t think we can’t quantify the number of cars that will be introduced 2 months from now?”

You’re talking about Supply, not Demand.

Keep up the good work.

LikeLike

[1] Apologies up front, but it looks like I must one again “mindlessly agree” with Rodger (except that I think we are in a recession right now, which is permanent and intentionally engineered.)

For some people I don’t “mindlessly agree” with Rodger. I am merely a toady who helps Rodger sell his snake oil. (“Monetary Sovereignty cured my warts! Hallelujah! Get yours NOW while supplies last!”)

Anyway I too would choose a psychologist. Economics doesn’t run on facts. Economics runs on psychological factors such as belief, politics, propaganda, vanity, ego, greed, insecurity, selfishness, and so on.

MMT people tend to ignore psychological factors. They ignore Mitchell’s law that: “The single most important problem in economics is the Gap between rich and poor.”

MMT people are like homicide detectives who consider means and opportunity, but who ignore human motives. When we ignore motives, we become vague and confusing. We put everyone to sleep. We never understand even our own babbling. Further, we become gullible suckers. We believe politicians who falsely claim that Social Security, for example is “insolvent,” because we don’t ask whether politicians may be intentionally lying. We don’t ask what their politicians’ motives are.

However, when we consider motives and politics, we have a better understanding of things like Monetary Sovereignty, or things like the “gold standard” gimmick.

[2] On a different note, Rodger writes that, “Charting still is widely used as a predictive commodity pricing tool.”

Yes, and charting is still widely used in the sales pitches of “financial planners” whose job is to con you into giving them your money.

[3] Rodger writes, “If I tell you that reductions in federal deficit spending lead to recessions and depressions, that statement is about as accurate as economics can be. There is no formula, no proof, that can improve on that statement for accuracy.”

I think simple logic is sufficient. When businesses borrow from banks, the businesses build up a debt load. As the debt load grows, businesses must devote more and more of their profits and budgets to debt servicing. This causes the velocity of money to slow down in the general economy. If the government does not increase deficit spending, then the result is a recession. This seems pretty straightforward to me.

But beyond that, the study of Monetary Sovereignty is based on a number of unassailable facts, as Rodger notes farther below. To give one example, if we cannot create money out of thin air, then our income must equal or exceed our expenses, or else we will become financially non-viable.

Ultimately the “economy” consists of what people choose to do (or not do) with the facts.

[4] Rodger writes, “I can show you the many times when reductions in federal deficit spending did, in fact, lead to recessions and depressions. But repetition is not scientific proof. Physicists know that.”

Scientific proof requires an element of falsifiability, verifiability, and predictability. If you assert that austerity leads to recessions, and you are correct in 100 out of 100 cases, then I would say that your assertion is scientific. However most people don’t want science; they want superstition, even when superstition is wrong 100 out of 100 times. They prefer to listen to people who endlessly claim that, “The national debt is a crisis!”

[5] Rodger writes, “I have awakened 30,000 consecutive mornings, but even that massive repetition does not prove I always will awaken.”

If we take things to extremes, then we see than science deals with probability, not certainty. The sun has risen in the east billions of times, but that it not absolute proof that it will rise again tomorrow. Still, we can reasonably predict that it will rise tomorrow. Science can make workable predictions that get aircraft into the air, and cars down the road.

[6] Rodger writes, “And if someone presents exceptions showing how at certain times, reductions in federal deficit spending did not lead to recessions and depressions, they merely are expressing the variables of human psychology. They neither have proved nor disproved anything.”

To me it is analogous to flipping a coin. If a coin is properly flipped, then there is a 50-50 chance that it will come up “heads.” A coin might come up “heads” for thirty times in a row, but the more we keep flipping, the closer we come to a 50-50 outcome. It is the same with austerity and recessions. There may be occasional exceptions, but longer the record we look at, the more we can verify that fiscal austerity does indeed lead to recessions.

[7] Rodger writes, “Logically then, since the Federal Reserve Bank pays off federal debt with dollars that already exist in T-security accounts, the federal debt never can be ‘unsustainable’.”

What about interest? If we deny that a Monetarily Sovereign government can create its own spending money out of thin air (including money to pay interest on T-securities) then we can claim that the federal debt is indeed “unsustainable.”

[8] Rodger writes, “Economics essentially is a ‘soft’ science, like psychology or philosophy. In trying to be part of a ‘hard’ science, economists have gone astray, and done a great disservice to the public, the nation and themselves. It’s time to get real, economists.”

Economists will “get real” when the aggregate amount of human compassion outweighs the aggregate amount of human selfishness.

Until that day comes, most economists will remain charlatans for hire.

LikeLike

THIS WEEK IN CRAZY

LikeLike

Economics is potentially logical, but politicians would have to relinquish their control in favor of science and engineering. Costing, pricing and income are energetically, physically measurable and may be determined as ‘ x amount of work per unit of output ‘ being done primarily by inanimate modern machinery as compared to animate (human) ability acting alone in craft survival.

In short, we actually could find out how much the integrated, electromotive tool complex we call “industry” is capable of when compared to people acting on their own in 1800 A.D. without the aid of mass production.

The real 2015 purchasing power of a dollar -as you might imagine – would be utterly phenomenal in scientific terms when based upon (backed up) by the real cost of a single kilowatt hour of clean, solar, wind or turbine generated hydroelectricity distributed (wheeled) from an all time zones internationally integrated power grid.

This is all off in the future obviously and would, in my estimation, be monetary sovereignty’s follow up phase. By merging economics with science and engineering we would have for the first time in history the unification of ever increasing wealth-as-knowhow underpinning ever increasingly valuable currency. No longer would science and economics be headed in fatally opposite directions. No longer would the words rich and poor and gap have any meaning.

LikeLike

“Look in any economics textbook and you will see it is loaded with graphs and formulas, almost none of which are more than approximations, and usually less, but appearing to be much more.”…… at my “elite” college (in the 90s), the only economics course I took was full of graphs and formulas, the whole semester. a complete waste of time. no wonder it was a favorite of the athletes (and I was an athlete).

“To “pay off” a T-security, the Federal Reserve Bank debits the appropriate T-security account and credits a checking account. This is identical to what any bank does to pay off any savings account.”………. including, of course, the “new” dollars which encompass interest.

LikeLike

The interest dollars are additional, created ad hoc the same way all new spending dollars are created.

That ad hoc money creation is one of the two ways trillions of dollars have been created (the other being bank lending).

LikeLike

just wanted you to say it………..

LikeLike

Actually, Economics CAN and almost was a “Science” until it was deliberately corrupted by the Land-grant universities and their tenured professors in the early part of the last century. Until then, most political economists (economics wasn’t a separate discipline until about this time too) understood there were 3 factors of production, not two as is commonly and wrongly assumed today. In addition to Capital and Labor, there is Land (ALL of nature’s resources, including location). Land is almost the opposite of Capital, which it is wrongly conflated with today.

Land is finite. Capital is infinite, within the constraints of labor and land.

Land is created by nature. Capital is created by Man.

Land appreciates (mostly) due to population growth and commerce growth. Capital wears out, becomes obsolete and depreciates.

There IS a way to predict major economic crashes, and in fact they occur about every 18 years, unless thrown off by major world events like world wars (actually good for the economy if you happen to be on the winning side, because it spurs production and spending…but certainly we can do that without mass slaughter, can’t we?).

Here is a prediction made in 2005 by one of the leading Georgist economic journalists that was right “on the money” http://moneyweek.com/bust-will-follow-boom-but-when/. The next crash will occur in 2019, and the next MAJOR one after that, which will be bigger than 2008-09 will occur in 2026.

Nothing will change this except a broad based land value tax. Not QE, not fiscal stimulus – these just go back in the pockets of land speculators, i.e. rent-seekers, though they can help for a while and even create some infrastructure and jobs.

LikeLike

I will add a 4th factor to go along with land, labor and capital and that would be knowhow as reflected by increased efficiency or doing more with less, such as in nanotechnology and ever more powerful and lighter alloys and materials.

Knowhow (intelligence) is the one and only regenerative factor; all the others wear out as they’re purely physical while knowhow represents Mind over matter, i.e., the META- PHYSICAL.

LikeLike