The “ticking time bomb” is the federal debt that supposedly is so big as to be “unsustainable.” You remember. It’s the “bomb” that has been sustained for 84 years.

If someone is wrong every year for 84 years, would you believe them? Unfortunately, some still believe the federal debt is “unsustainable,” a “ticking time bomb,” and should be combated with a debt limit.

I have no polite words to describe those people. Sadly, I now must tell you about “the world’s largest Ponzi scheme,” which, by no coincidence, also is the federal debt.

“Ponzi” is the latest term used by people who either don’t understand Monetary Sovereignty or don’t want you to understand Monetary Sovereignty.

‘The world’s largest Ponzi scheme’: Peter Schiff just blasted the US debt ceiling drama. Here are 3 assets he trusts amid major market uncertainty Story by Bethan Moorcraft A ticking time bomb in the U.S. economy is running perilously close to detonation.

With the U.S. reaching its debt limit of $31.4 trillion on Jan. 19, Treasury Secretary Janet Yellen urged lawmakers to increase or suspend the debt ceiling.

Janet Yellen reveals that she knows the debt ceiling is unnecessary, useless, and harmful. Otherwise, she would ask that the debt be paid off.

She knows, however, that federal finance makes that not just unnecessary but impossible simply because the federal government is not the debtor.

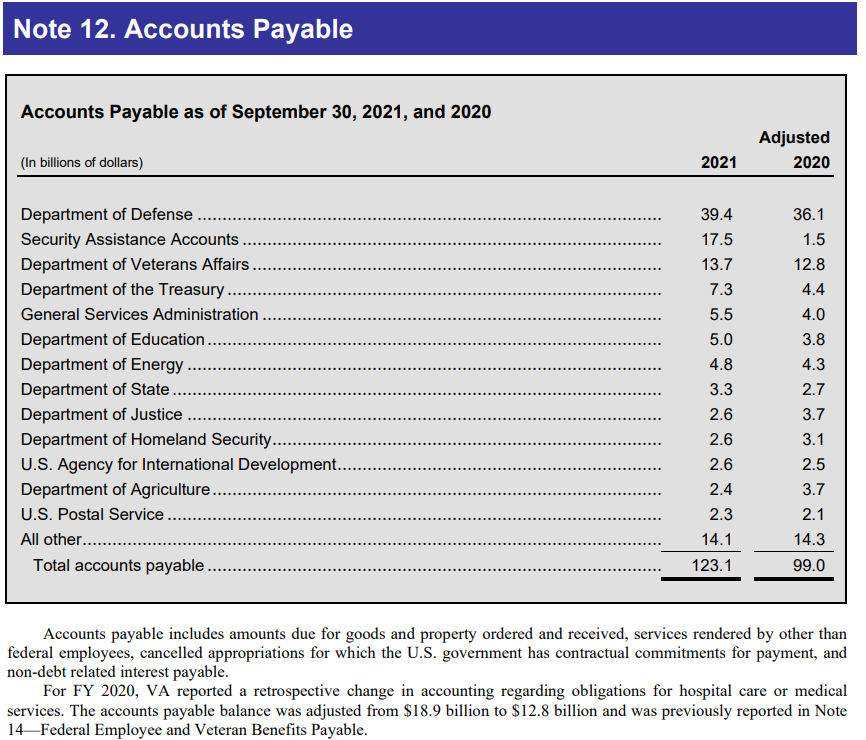

That thing called “federal debt” isn’t federal debt. The actual federal debt is the amount the federal government owes to vendors of goods and services purchased by the federal government but not yet paid for.

In short, the real federal debt also is known as “Accounts Payable” plus Interest Payable.

The actual federal debt is in the billions, not the trillions, and it is paid reliably every day.

Treasury securities, T-bills, T-notes, and T-bonds are deposit accounts, similar to bank safe deposit accounts that the government never touches.

When you invest in a T-security, you put dollars into your account from which only you can withdraw. Just as the contents of your bank safe deposit box are not the debt of your bank, the contents of your T-security account are not the debt of your federal government.

The government didn’t borrow those dollars. It merely holds them separately for safekeeping until you take them back.

Her plea was taken by Peter Schiff, famed investor, and market commentator, as an “official admission that the U.S. is running the world’s largest Ponzi scheme.”

Sadly, Schiff doesn’t seem to know what a “Ponzi scheme is. Quoting from Wikipedia:

A Ponzi scheme is a form of fraud that lures investors and pays profits to earlier investors with funds from more recent investors.

The scheme leads victims to believe that profits come from legitimate business activity (e.g., product sales or successful investments), and they remain unaware that other investors are the source of funds.

A Ponzi scheme can maintain the illusion of a sustainable business if new investors contribute new funds. Most investors do not demand full repayment and still believe in the non-existent assets they purported to own.

Federal T-securities have none of these characteristics.

- They are not fraud.

- Payment does not come from more recent investors but rather from each depositor’s own deposits and the federal government’s infinite ability to create its sovereign currency.

- There is no claim that funds come from any business activity, legitimate or otherwise.

- The government does not rely on new investors, nor does it rely on new depositors. The government does not have to accept deposits. Even if every T-security owner demanded payment, the government could comply today.

Peter Schiff merely is using a scare tactic to fool the public. Rather than being a Ponzi scheme, U.S. T-securities are the safest investments known to the world and will continue to be safe so long as no political party is foolish enough to enforce the ridiculous debt limit (aka the “screw-depositors-to-make-political-points” action).

A political stand-off over the debt ceiling has been raging since Republicans regained control of the House of Representatives in the 2022 midterm elections.

President Joe Biden beseeched Congress not to hold the item hostage, suggesting a default could be “calamitous.”

His warnings hit deaf ears in the case of opposing Republicans who used their votes on an extension as leverage to seek spending cuts.

The debt limit has nothing to do with spending cuts because it deals with past spending, not future spending.

The Republican extortion attempt just as easily could be directed at any federal laws, even those having nothing to do with federal finances.

How about enforcing the debt limit unless women Senators wear long dresses, Trump’s rioters are released from prison, or the Capital is painted purple.

All of those have as much relevance to a debt limit as demanding cuts to future spending. The debt limit is a child’s game of, “I’ll hold my breath until I get my way.”

The Treasury can use “extraordinary measures” in the coming months to cover its many financial obligations, including Social Security and Medicare disbursements, but these emergency funds are limited.

At the end of the day, the U.S. simply must borrow more money, as it has done many times before.

The notion that the creator of the U.S. dollar needs to borrow dollars from the people who use the dollar is obviously ridiculous. Where would the so-called “lenders” get the dollars to “lend” if the creator is precluded from creating dollars?

Congress has set the limit for federal borrowing since 1917, raising it over time as government spending and borrowing needs have increased.

Notice the arbitrariness of the above sentence. It correctly assumes Congress can, at its discretion, increase the “debt limit” without regard to the wishes of so-called lenders.” If it were a real debt, the “borrower” could not, at whim, decide to borrow unlimited amounts.

“The U.S. Treas. Sec. has admitted the only way to avoid a default on the National Debt is to raise the #DebtCeiling so the Govt. can borrow from new lenders to repay existing lenders,” Schiff, CEO and chief global strategist at Euro Pacific Capital tweeted on Jan. 16.

“This is an official admission that the U.S. is running the world’s largest Ponzi scheme.”

Oh, the ignorance! Oh, the lies. The “U.S. Treas. Sec.” admitted no such thing. The real way to avoid default is to eliminate the useless debt ceiling. We didn’t always have a debt ceiling. Why do we have one now? Taken from Wikipedia:

In 1979, noting the potential problems of hitting a default, Dick Gephardt imposed the “Gephardt Rule,” a parliamentary rule that deemed the debt ceiling raised when a budget was passed.

This resolved the contradiction in voting for appropriations but not voting to fund them. The rule stood until it was repealed by Congress in 1995.

Get it? When Congress voted for an appropriation, it also voted to fund them.

So, if Congress said, “We authorize spending a billion dollars on a dam,” that meant a billion dollars immediately became available to build a dam.

Makes sense to any normal person. Apparently, though, it was too logical for Congress.

In 1995, Congress said, “When we authorize spending a billion dollars to build a dam, we really don’t authorize paying a billion dollars to build the dam.”

And if that makes sense to you, you should run for Congress. Since that convulsion of childish illogic, Congress has plagued the nation with repeated debt limit crises.

The US raised its debt ceiling (in some form or other) at least 90 times in the 20th century.

The debt ceiling was raised 74 times from March 1962 to May 2011, including 18 times under Ronald Reagan, eight times under Bill Clinton, seven times under George W. Bush, and five times under Barack Obama.

In practice, the debt ceiling has never been reduced, even though the public debt itself may have been reduced.

It should be noted that never has the arbitrary increase of the debt ceiling caused any sort of financial difficulty. There has been no time bomb explosion, fraud, or Ponzi scheme.

In his podcast, Schiff claimed the U.S. government is in a doom spiral where it cannot pay its current lenders back, so it borrows from new lenders repeatedly.

And, oh yes, no “doom spiral.” Though the so-called “debt” has risen from $40 billion to $26 trillion, a 65,000% increase, the federal government still has no difficulty paying its bills.

“Why do people willingly participate? It’s because they don’t realize it’s a Ponzi scheme,” Schiff says.

It’s not.

“They think they’re going to get paid back. When they realize they’re going to be paid back in monopoly money, they’re not going to want to lend.

“Monopoly money”? Is that a scare term like “Ponzi scheme” and “ticking time bomb”?

“In fact, they’re not going to want to hold on to these Treasuries, and the only buyer is going to be the Federal Reserve. And that’s when the printing press is going to overdrive, and the dollar is going to fall through the floor.”

Gee, Schiff, exactly when is that going to happen. It didn’t happen while the printing press was running every day, every week, every month, and every year for the past 84 years. Why are things different now?

As Congress fights over the debt ceiling extension, U.S. credit rating and financial markets are at risk – but here are three assets that Schiff likes as hedges against economic volatility.

And here it comes, the real reason Schiff is serving up bushels of BS:

Wealthy young Americans have lost confidence in the stock market — and are betting on these assets instead. Get in now for strong long-term tailwinds.

Gold. Schiff has long been a fan of the yellow metal.

“The problem with the dollar is it has no intrinsic value,” he once said. “Gold will store its value, and you’ll always be able to buy more food with your gold.”

Except, Schiff neglects to tell you that gold has very little intrinsic value. Gold has less intrinsic value than aluminum, iron, copper, or paper. Gold isn’t used for much other than decoration.

A few teeth fillings, some electronics, that’s about it. Rather than intrinsic value, gold has demand value. People want the stuff mainly because it’s pretty.

As always, he’s putting his money where his mouth is.

Euro Pacific Asset Management’s latest 13F filing shows that as of Sept. 30, Schiff’s company held 1.655 million shares of Barrick Gold (GOLD), 431,952 shares of Agnico Eagle Mines (AEM), and 317,495 shares of Newmont (NEM).

In fact, Barrick was the firm’s top holding, representing 6.8% of its portfolio. Agnico and Newmont were the third and sixth-largest holdings, respectively.

Right. He’s promoting his holdings, trying to get suckers to buy gold.

Gold can’t be printed out of thin air like fiat money, and its safe-haven status means demand typically increases during times of uncertainty.

Except, we always are in times of uncertainty, and gold can be mined out of thin air.

The biggest problem with gold is it costs money to ship, costs more money to store, and costs even more money to insure. And the stuff pays no interest or dividends.

Gold is the classic “bigger fool” investment. Fools buy it hoping to sell it to bigger fools. If you are looking for absolute safety, with no shipping, storage, or insurance costs, plus income, buy T-securities.

Other than that, your best bet is one of the big stock funds. based on the S&P index or similar. And stop worrying about the misnamed federal “debt.” It’s not federal, and it’s not debt, and it’s not a ticking time bomb.

It’s just privately owned, federally guaranteed depositories of U.S. dollars. The only way the “ticking time bomb” can explode is if the debt nuts push the “debt limit” button.

The cure for the “debt limit crisis:” Simply return to the Gephardt Rule. Simple.

Rodger Malcolm Mitchell Monetary Sovereignty Twitter: @rodgermitchell Search #monetarysovereignty Facebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY