I continually am puzzled by the misunderstanding (“disunderstanding”?) of Monetary Sovereignty. It is both simple and obvious, yet many (most?) people have trouble comprehending it.

MS is based on just four simple facts:

In the 1780s, the U.S. federal government created the laws that created the U.S. dollar from thin air — as many dollars as it wished – and gave them the value it wished.

The government’s own laws give it the power to continue creating dollars, infinitely

The government’s own laws give it the power to continue changingthe valueof the dollar — a power it has used many times.

The government can change its laws at will.

Really, what could be simpler, more obvious, and less controversial?

Derived from these simple, obvious facts comes the following:

The U.S. federal government never unintentionally can run short of U.S. dollars.

No agency of the government can run short of dollars unless the government wishes it.

Federal taxes are not used or needed to fund federal spending.

By changing the value of the dollar, the government has absolute control over inflation

And that’s it. Monetary Sovereignty.

Intuition is powerful. Many of us prefer to believe our intuition than believe facts.

Interestingly, where fiction parallels facts, you might not believe the facts about the fiction, while still believing fiction about the facts.

That is, you might read a historical novel of fiction, and not believe the background facts presented. Yet, you might be fooled by a conspiracy theory website presenting fiction as fact.

So here is the explanation that may appeal to intuition as well as to facts.

You probably have played the hugely popular board game, Monopolytm. As a game, it’s fiction, but you believe and understand the facts (i.e. “rules.’)

Here are some of the facts.

The game is played with multiple players plus a Bank. The Bank pays Monopoly dollars to the players for various benefits.The Bank collects taxes, fines, loans and interest from the players.The Bank “never goes broke.” If the Bank needs money, it may issue as many dollars as needed by printing on scraps of paper or simply by creating a bookkeeping tally.

Example of a Monopoly running tally

A sample tally is demonstrated by the illustration at the right.

It reveals three things:

I. Monopoly money is not physical. Those printed $500, $100, $50, $20 $10 $5, and $1 bills aren’t dollars in of themselves.They merely representdollars, just as the numbers on a tally represent dollars.II. The Bank can createan infinite supply of Monopoly dollars.

If needed, the Bank instantly could pay Tom, Dick, Harry, or Bob $1, or $100, or $1,000,000,000 in Monopoly dollars.

In the tally, there is no need to create a column for the Monopoly Bank.

This lack of a column demonstrates the Bank’s ownership of infinite dollars.

It also demonstrates that all dollars sent to the Monopoly Bank are destroyed upon receipt.

If Tom, for instance, sent $100 to the Bank, his $4,400 would be reduced to $4,300. So, what happened to the $100 Tom paid? They simply disappeared. They no longer exist.

Although the Bank can create infinite dollars this creation process does not create Monopoly Bank “debt.” The Monopoly Bank does not borrow dollars nor does it owe any dollars.

Thus, taxes are not levied to “pay off” any Monopoly Bank debt.

By rule, the Monopoly Bank simply creates all the dollars it needs. Although the Bank is not precluded from keeping track of the dollars it receives from players, that record would not indicate how many dollars the Monopoly Bank “owes” or has.

There is no ongoing debt owed by the Monopoly Bank.

All of the above is easily understood by you and by virtually anyone else who has played the game.

Now, in the above paragraphs, substitute the words, “U.S. federal government” for the word “Bank.” And substitute “members of the public” for “players.”

The facts remain essentially the same.

There are multiple members of the public plus the federal government.

The federal government pays dollars to the public for various benefits.

The federal government collects taxes, fines, loans, and interest from the public.

The federal government “never goes broke.” If the federal government needs money, the government may issue as much as needed by printing on paper or simply by creating a bookkeeping tally.

[Former Fed Chairman, Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”]

Continue reading and substituting until you come to the part that some people have difficulty understanding:

The federal government does not borrow dollars nor does it owe any dollars. Taxes are not levied to “pay off” any federal government debt.

[Quote from Ben Bernanke when, as Fed chief, he was on 60 Minutes:

Scott Pelley: Is that tax money that the Fed is spending?

Former Fed Chair, Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.]

The Monopoly Bank and the U.S. federal government both are Monetarily Sovereign. They both are issuers of their dollars. Neither of them can run short of dollars.

Both the Monopoly Bank and the U.S federal government have infinite dollars.

[Former Fed Chair, Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”]

Neither the Monopoly Bank nor the federal government borrows or taxes in order to pay their financial obligations. Spending by the Monopoly Bank or the U.S. federal government does not create future taxpayer obligations.

For that reason, Social Security, an agency of the federal government, cannot run short of dollars, unless that is what the government wants. Even if there were no FICA tax (which contrary to popular myth, does not fund Social Security), that agency need not run short of dollars.

The “debt clock.” You have no share.

Medicare for All, college for all, upgraded infrastructure, good housing for all — every imaginable federal benefit — all are easily affordable. The so-called federal debt is not a burden on future taxpayers or on the government.

The famous “debt clock” implies the lie that somehow the federal “debt” is a danger to you, your children, and the federal government.

It is not a debt, and it is not a danger, to you or anyone.

It is just simple deposits by the public into accounts.

The parallels between the Monopoly game and federal financing are stunning.

Yet, though people tend to understand the rules of Monopoly, too many become hopelessly confused by the same set of facts when applied to real life.

Yes, one is fiction and the other is fact, but that difference is not the source of the confusion.

The confusion is caused by the longtime, ongoing, relentless dissemination of false information about the federal government’s finances and by the misnaming of T-securities as “borrowing” and “debt.” They are neither.

The misinformation is promulgated by agents for the rich, who want to prevent you from asking for the benefits the rich already receive: Retirement benefits, medical care, good housing, safe neighborhoods, college education, spending money for a good life.

Neither the government nor you owes the deposits that sit in T-security accounts. These accounts resemble bank safe deposit boxes, which the bank “pays off” simply by returning the contents. No “debt” or tax liability there.

The Monopoly board game is a good analog for the federal finance system. If you understand one, you should understand the other.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

One definitionof “science” is: A systematic enterprise that builds and organizes knowledge in the form of testable explanations and predictions about the universe.

Economics is a “social science. One wonders whether it can be called a science at all, for it really is an accounting-based branch of psychology, which itself holds to the title, “science,” by its fingertips.

As for “testable explanations” and “testable predictions,” not so good. The psychology role in economics testing is at its best when “predicting” history, but fails repeatedly when trying to predict the future.

Economics approximates religion, which predicts that your following (or not following) certain arbitrary, often illogical and meaningless, rules will be rewarded in some vague way by an omniscient entity.

Accounting

While accounting can have complex and changing rules, it is based on simplicity: The direct relationships among income, saving, and outgo.

Any change in one factor is balanced by a mathematically equal change in the other factors, thus the word “balance” sheet.

Based on its arbitrary rules, accounting strictly is logical and eminently predictable. Adding to the left side of a balance sheet always requires adding to the right side, yesterday and tomorrow.

Though based on arithmetic, and in one sense on algebra (the relationship to the “=” sign), accounting is not a science. Though it organizes knowledge, it doesn’t create testable explanations and predictions about the universe. It simply is a score-keeping method for money-related valuations.

Psychology

This brings us to the other leg of economic’s extremely shaky, two-legged stool, psychology.

In its attempts to rise above religion (the pompous quest to know God’s mind) psychology does run tests and many of these tests provide results that pass for explanations that even are the basis for predictions.

But the economic results seldom are conclusive, while the explanations are subjective, and the predictions often are laughably random — just like with religion.

In real science, testing attempts to change one variable while holding all other variables stable. In psychology, and so in economics, holding all other variables stable generally proves to be impossible. So results vary wildly.

But that impossibility does not deter people known as “chartists.” From Investopedia:

A chartist is an individual who uses charts or graphs of a security’s historicalprices or levels to forecast its future trends.

Chartists generally believe that price movements in a security are not random but can be predicted through a study of past trends and other technical analysis.

Generally, chartists will use a combination of indicators, personal sentiment, and trading psychology to make investment decisions.

Serious chartists can seek to obtain the Chartered Market Technician designation which is sponsored and written by the Market Technicians Association.

Even if charting could predict future prices, it stillcould not predict future prices.

Future stock prices are based on demand. So if charting could predict future prices, everyone would wish to buy or sell according to what the chart indicates.

In that way, charting would affect demand, which in turn would affect charts in an endless helix of price changes, all having little to do with a security’s underlying value.

Thus, charts destroy their own predictions, the “better” the chart, the more the destruction.

Though securities charting doesn’t work as claimed, it does have one value: It establishes a pseudo-scientific, mathematical veneer to its one area of economics.

That is why economics is obsessed with graphs. We economists wish to use mathematics, so to demonstrate our “real science” chops.

That also is why economists love complexification. Read any economics textbook, I dare you. You will discover a convoluted amalgam of graphs, charts, and equations and balance sheets, and difficult wording, all designed to give scientific credence to a non-credible forecasting ability.

How about “Externality,” “Autraky,” “Opportunity set,” “Convexity,” “Dynamic stochastic general equilibrium,” and one of my favorites that often is in the news, “quantitative easing.”)

I too am guilty of graphs and charts, though I use them mostly to disprove economic nonsense. For instance.

Blue line: Gross federal debt. Red line: Gross federal debt/GDP. Green line: GDP

The above graph disputes the “debt-clock” worriers, who falsely claim the federal debt is like personal debt and so is “unsustainable” because of the following myths:

The faux simplicity is the false claim that federal debt is like personal debt. The public understands personal debt, so it is led to believe it understands federal debt.

The effect of complexity is to confuse either the author or the readers, and in that it has done remarkably well. The vast majority of the literate world is confused.

Once we wipe away the faux complexity, we are left with the following simplicity:

I. The U.S. federal government, unlike state, local, and euro governments is Monetarily Sovereign, which means it is sovereign over the U.S. dollar. It never unintentionally can run short of dollars. Even if all federal tax collections fell to $0, the federal government could pay any size debt denominated in dollars. Further, it has absolute control over the relative value of the dollar.

Monetary Sovereignty is fundamentally simple. Anyone who has played the board game, Monopoly, knows the Monopoly Bank is Monetarily Sovereign. By rule, it never can run short of Monopoly dollars and can create all it needs.

III. Inflations are not caused by government currency printing but rather by shortages, usually shortages of food or energy. Counter-intuitively (for many), increased government spending, to reduce food or energy shortages, reduces inflation.

IV. The human side of economics is ruled by Gap Psychycholgy, the desire to distance oneself from those “below” on any social scale and to approach those “above.”

If you understand the above four simplicities, you understand the Ten Steps to Prosperity (below).

You understand why the federal government can eliminate FICA, increase Social Security and Medicare, fund advanced education for all who want it, and reduce poverty, while preventing and curing recessions, depressions, and inflations.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

It takes only two things to keep people in chains:

The ignorance of the oppressed

And the treachery of their leaders

…………………………………………………………………………

I do not understand quantum chromodynamics. Therefore, I do not pretend to understand quantum chromodynamics, and I do not write about the subject.

Would that all the people, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, abstained from writing about the subject. Unfortunately, many (most?) articles about federal finance reveal the authors’ abysmal understanding.

The U.S. government and others (Canada, Japan, the UK, Australia, et al) are Monetarily Sovereign. They create their own sovereign currency and pay their debts using that sovereign currency.

By contrast, cities, counties, states, euro nations, businesses, you, and I are monetarily non-sovereign. We do not have a sovereign currency with which to pay our debts. Unlike the U.S. government, you and I and the other non-sovereign entities can run short of whatever currency we use for bill-paying.

Writers, who do not account for the difference, wrongly seem to believe U.S. government finances are similar to monetarily non-sovereign entities.

Consider President Barack Obama:

“Government has to start living within its means, just like families do. We have to cut the spending we can’t afford so we can put the economy on sounder footing, and give our businesses the confidence they need to grow and create jobs.” —President Barack Obama, weekly radio address, July 2, 2011

He was wrong. The U.S. government is not “just like families.” Federal finances are nothing like family finances. The President spoke out of ignorance or deceit, I don’t know which. Many speakers and writers do the same.

John Steele Gordon is one such writer.

Here are excerpts from his article that appeared in Commentary.

John Steele Gordon is an economic historian and the author of, among other works, An Empire of Wealth:The Epic History of American Economic Power. He was educated at Millbrook School and Vanderbilt University, graduating with a B.A. in history in 1966.

The famous “debt clock” that wrongly implies you owe the federal debt.

Someone in the 19th century said that there are three forms of lying: lies, damned lies, and statistics.

If you would like a beautiful example of the last category of mendacity, check out David Leonhardt’s April 15th column in the New York Times, entitled (try not to laugh) “The Democrats Are the Party of Fiscal Responsibility.”

As you will see, Mr. Gordon will provide excellent examples either of his own mendacity or his pure ignorance of the subject.

In our previous post, “The CRFB myth machine keeps on rolling,“ I assumed the Committee for a Responsible Federal Budget (CRFB) was deliberately deceptive. In today’s post, I wonder whether Mr. Gordon, a Bachelor of Arts in history, simply never learned about federal finance.

Including that notorious and misleading debt clock as a lead to his article, is only the beginning of his article’s wrongheadedness.

He continues:

In it, he compared the deficits run up by each Democratic and Republican administration from Jimmy Carter on to the present with the GDP of that time.

These ratios are presented with the implications that a) the federal government can’t afford to service some level of deficit or debt, and b) that taxpayers will have to bear the burden.

In fact, the U.S. federal government can afford anything, and taxpayers do not pay for federal obligations. To quote some real experts:

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

St. Louis Federal Reserve: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills.

As Greenspan, Bernanke, and the StL Fed say, the federal government can pay any bills by “printing” dollars, not by collecting taxes. Clearly, you taxpayers and your grandchildren will not be burdened (as some pundits claim).

The article continues:

Whatever his methodology, Leonhardt was comparing apples and oranges.

Ah, the irony of the apples/oranges analogy, since there can be a no better example of that fruit salad than Debt and GDP, two unrelated, completely non-comparable figures.

“Debt” equals the deficit total over many years. GDP is a one-year measure of spending in America — federal, non-federal and foreign. A high Debt (or Deficit) / GDP ratio merely implies the financial contribution the federal government makes to our economy. The ratio says nothing about affordability, the need for taxes, economic growth or any other important measure.

Gordon wrote:

It was not Bill Clinton who slew the deficit dragon in the 1990’s but the Congress, which the public transferred to Republican control in 1994 for the first time in 40 years following an outcry over Democratic profligacy.

Gordon refers to the deficit as a “dragon,” not realizing that federal deficits add dollars to the economy, and that without federal deficits it mathematically is impossible for the economy to grow:

GDP = Federal Spending + Non-federal Spending + Net Exports

Federal Spending and Non-federal Spending both rely on the dollars created via federal deficit spending.

Gordon also demonstrates he does not understand the difference between “Total Federal Debt” and “Federal Debt Held By The Public,” when he writes:

The Republican Congress increased spending by a mere 18 percent between 1995 and 2000, while the roaring economy increased tax revenues by 51 percent.

Nor did Leonhardt take into account the phony accounting the federal government uses to obscure reality. Officially, we ran surpluses (meaning, by definition, that income exceeded outgo) in 1998, 1999, 2000, and 2001.

But the national debt went up, not down, in each of those four years.

This graph demonstrates the difference:

The blue line (Total Debt) includes internal debt (dollars federal agencies owe to each other). The red line is the total of T-securities owned by the U.S. and other economies.

The national “debt” went up only if one includes the internal debt that federal agencies owe each other — i.e. what the right pocket owes the left pocket.

Surpluses however, refer only to external debt — dollars flowing from the federal government into the economy. The real federal debt went down from 1997 through 2000.

Predictably, the surpluses beginning in 1997 led to the recession of 2001, which was cured by deficit spending.

(As an aside, every depression in U.S. history, including the “Great Depression,” was introduced by years of federal surpluses, which sucked dollars out of the economy,)

Then comes perhaps the funniest or saddest paragraph in Gordon’s entire article:

Nor did Leonhardt take into account the fact that recessions cause government spending to go up and government revenues to go down—something quite beyond the control of Congress or the President.

Recessions don’t “cause” government spending to go up. Deficit spending, which pumps dollars into the economy, is the primary method governments use to cure recessions.

And to say that government deficit spending is “quite beyond the control of Congress or the President,” goes well beyond ordinary ignorance, into the land of the blind.

Gordon ends his screed, with this misleading, self-defeating conclusion:

But in the last forty years, the only time the federal government made a serious, sustained effort to rein in the deficit was when a Republican Congress was writing the checks.

In fact, Democrat Bill Clinton was President, and though Clinton often boasts about his surpluses, “reining in the deficit” caused a recession, which was cured by deficit spending.

In summary, I don’t know John Steele Gordon. I don’t know whether his wholly wrong article was designed to mislead or merely was written out of ignorance.

Either way, the effect is the same: Deception. A public that already does not understand Monetary Sovereignty and federal finances, is further vaccinated by complete misunderstanding.

The most important problems in economics involve the excessive income/wealth/power Gaps between the have-mores and the have-lesses.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps:

Ten Steps To Prosperity: 1. ELIMINATE FICA (Ten Reasons to Eliminate FICA ) Although the article lists 10 reasons to eliminate FICA, there are two fundamental reasons: *FICA is the most regressive tax in American history, widening the Gap by punishing the low and middle-income groups, while leaving the rich untouched, and *The federal government, being Monetarily Sovereign, neither needs nor uses FICA to support Social Security and Medicare. 2. FEDERALLY FUNDED MEDICARE — PARTS A, B & D, PLUS LONG TERM CARE — FOR EVERYONE (H.R. 676, Medicare for All ) This article addresses the questions:

*Does the economy benefit when the rich can afford better health care than can the rest of Americans?

*Aside from improved health care, what are the other economic effects of “Medicare for everyone?”

*How much would it cost taxpayers?

*Who opposes it?”

3. PROVIDE A MONTHLY ECONOMIC BONUS TO EVERY MAN, WOMAN AND CHILD IN AMERICA (similar to Social Security for All) (The JG (Jobs Guarantee) vs the GI (Guaranteed Income) vs the EB (Economic Bonus)) Or institute a reverse income tax.

This article is the fifth in a series about direct financial assistance to Americans:

Economic growth should include the “bottom” 99.9%, not just the .1%, the only question being, how best to accomplish that. Modern Monetary Theory (MMT) favors giving everyone a job. Monetary Sovereignty (MS) favors giving everyone money. The five articles describe the pros and cons of each approach.

4. FREE EDUCATION (INCLUDING POST-GRAD) FOR EVERYONE Five reasons why we should eliminate school loans

Monetarily non-sovereign State and local governments, despite their limited finances, support grades K-12. That level of education may have been sufficient for a largely agrarian economy, but not for our currently more technical economy that demands greater numbers of highly educated workers.

Because state and local funding is so limited, grades K-12 receive short shrift, especially those schools whose populations come from the lowest economic groups. And college is too costly for most families.

An educated populace benefits a nation, and benefitting the nation is the purpose of the federal government, which has the unlimited ability to pay for K-16 and beyond.

5. SALARY FOR ATTENDING SCHOOL

Even were schooling to be completely free, many young people cannot attend, because they and their families cannot afford to support non-workers. In a foundering boat, everyone needs to bail, and no one can take time off for study.

If a young person’s “job” is to learn and be productive, he/she should be paid to do that job, especially since that job is one of America’s most important.

6. ELIMINATE FEDERAL TAXES ON BUSINESS

Businesses are dollar-transferring machines. They transfer dollars from customers to employees, suppliers, shareholders and the federal government (the later having no use for those dollars). Any tax on businesses reduces the amount going to employees, suppliers and shareholders, which diminishes the economy. Ultimately, all business taxes reduce your personal income.

7. INCREASE THE STANDARD INCOME TAX DEDUCTION, ANNUALLY. (Refer to this.) Federal taxes punish taxpayers and harm the economy. The federal government has no need for those punishing and harmful tax dollars. There are several ways to reduce taxes, and we should evaluate and choose the most progressive approaches.

Cutting FICA and business taxes would be a good early step, as both dramatically affect the 99%. Annual increases in the standard income tax deduction, and a reverse income tax also would provide benefits from the bottom up. Both would narrow the Gap. 8. TAX THE VERY RICH (THE “.1%) MORE, WITH HIGHER PROGRESSIVE TAX RATES ON ALL FORMS OF INCOME. (TROPHIC CASCADE)

There was a time when I argued against increasing anyone’s federal taxes. After all, the federal government has no need for tax dollars, and all taxes reduce Gross Domestic Product, thereby negatively affecting the entire economy, including the 99.9%.

But I have come to realize that narrowing the Gap requires trimming the top. It simply would not be possible to provide the 99.9% with enough benefits to narrow the Gap in any meaningful way. Bill Gates reportedly owns $70 billion. To get to that level, he must have been earning $10 billion a year. Pick any acceptable Gap (1000 to 1?), and the lowest paid American would have to receive $10 million a year. Unreasonable.

9. FEDERAL OWNERSHIP OF ALL BANKS (Click The end of private banking and How should America decide “who-gets-money”?)

Banks have created all the dollars that exist. Even dollars created at the direction of the federal government, actually come into being when banks increase the numbers in checking accounts. This gives the banks enormous financial power, and as we all know, power corrupts — especially when multiplied by a profit motive.

Although the federal government also is powerful and corrupted, it does not suffer from a profit motive, the world’s most corrupting influence.

10. INCREASE FEDERAL SPENDING ON THE MYRIAD INITIATIVES THAT BENEFIT AMERICA’S 99.9% (Federal agencies)Browse the agencies. See how many agencies benefit the lower- and middle-income/wealth/ power groups, by adding dollars to the economy and/or by actions more beneficial to the 99.9% than to the .1%.

Save this reference as your primer to current economics. Sadly, much of the material is not being taught in American schools, which is all the more reason for you to use it.

The Ten Steps will grow the economy, and narrow the income/wealth/power Gap between the rich and you.

Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

===============================================================================================================================================================================================================================

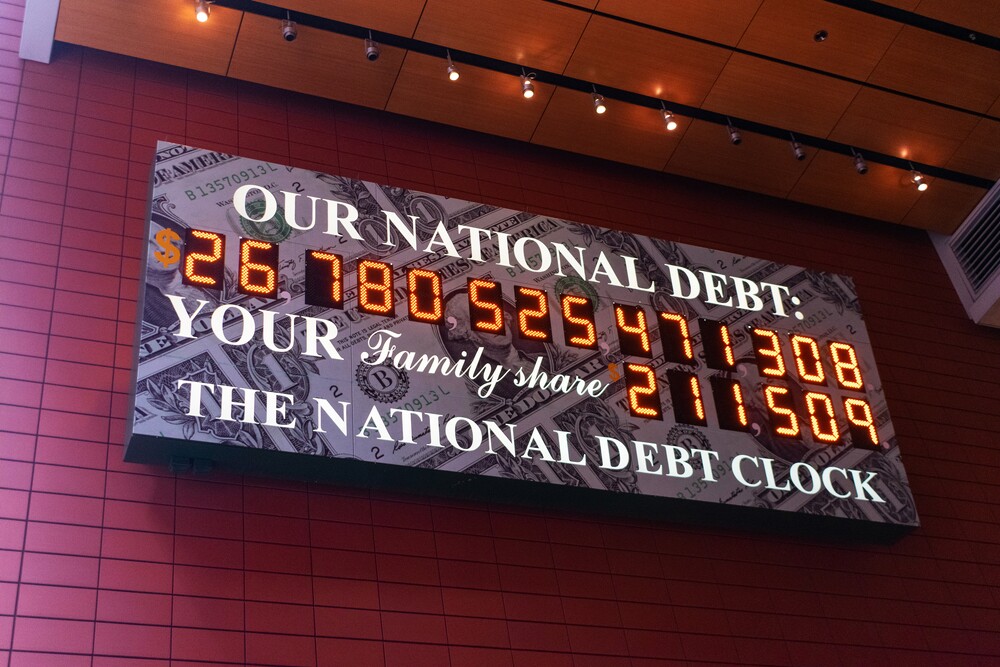

Lately I’ve been seeing this image published more often, in various media.

This surely is the most misleading, downright untruthful sign you ever will have the misfortune to encounter. It’s untruthful because it shows the gross federal debt, which includes money the federal government borrows from itself.

Example: For convenience, my wife and I have separate checking accounts. When we are not together, she can write checks and I can write checks, and it’s easier to balance than if both tried to write checks from the same checkbook. Periodically, if one account is low, we transfer money from one account to the other (the government would call that “borrowing,” but it’s just debiting one account and crediting the other), so both accounts will have positive balances. I don’t feel I’m in debt to my wife, nor she to me. I never would consider these periodic internal transfers to be “debt.”

Similarly, the federal government’s internal “creditors” (i.e. Social Security et al) are not going to dun the federal government for payment of its “debt.”

While the Gross Federal Debt is around $14 trillion, the net debt is only about $8 trillion — well below the debt ceiling (another misleading, untruthful gimmick). Sadly, Congress and the President pretend not to understand that. So they injure our economy about something that isn’t real.

For their own selfish, political reasons, these politicians do more harm to America than al qaeda ever could. (I wish there could be a law precluding these traitors from standing in front of an American flag when they speak.)

The misleading part of the sign has to do with the words, “Your family share.” Most people interpret those words to mean their family owes a share of the gross federal debt, which as we have seen, is a fake number. But worse, your family does not owe a share even of the net federal debt. Your family could more accurately be said to own a share of the debt.

The federal so-called “debt” is the total of outstanding T-securities. When the government “borrows” it debits the “lender’s” checking account and credits the lender’s savings account (aka T-security account) at the Federal Reserve Bank. No dollars are shipped anywhere. It’s just an asset exchange accomplished by a debit and a credit.

When the government pays its “debt,” the process is reversed. The checking account is credited and the savings account is debited. At no time are taxes involved so at no time do you or any other taxpayers owe anything. Whether taxes are $0 or $100 trillion, the federal government’s ability to debit and credit bank accounts does not change.

Buying a T-security is essentially identical with transferring dollars from your checking account to your savings account.

You could be said to own a share of the debt, because federal debt is a measure of money in the economy. You are part of the economy, so that money benefits you. The greater the “debt,” the healthier the economy.

I don’t know whether the Durst family, which owns and maintains the clock, knows what it really means. They may be forerunners of the Tea Party, those clueless folks who hate government but love their Social Security, Medicare and Medicaid checks, their safe food and drugs, their highways, army protection, scientific research, FDIC security, homeland security and the myriad other perks provided by the federal government.

It’s enough you to know that every time you see that sign, you see economic ignorance at work.

Here are some of the facts.

Here are some of the facts.