What is America’s most dangerous and harmful conspiracy theory?

No, it’s not the idiocy from QAnon. There is no group of Satanists, cannibals, and child sex abusers plotting against Donald Trump.

Only the mentally challenged believe that tripe.

No, it’s not the ages-old, anti-Semitic B.S. that Jews drink children’s blood on holidays. Jews famously love children. Mogen David wine is the preferred imbibement.

And no, it isn’t that Trump was cheated out of the election (though he and the entire GOP already plan to make the same claim if they lose again).

Fifty lawsuits, dozens of judges — some Republican — and numerous recounts have demonstrated the ongoing perfidy of that assertion.

The guy lost by over 7 MILLION individual votes and 74 electoral votes! And still, he whines. What does it take to convince the MAGAs?

Only the bottom segment of America’s intelligence range still believes those ideas.

The single most dangerous and harmful conspiracy theory is believed by the majority of America because it is repeated by the majority of America. Repetition is convincing.

Here is a classic example:

The CRFB Fiscal Blueprint for Reducing Debt and Inflation October 26, 2022

The United States faces numerous economic and fiscal challenges, including surging inflation, rising interest rates, trust funds heading toward insolvency, a broken budget process, and an unsustainably increasing national debt.

The CRFB (Committee for a Responsible Federal Budget) is part of a conspiracy to spread the false theory that these are problems caused by too much federal deficit spending.

The very rich, who support the CRFB, want you to believe that if you would accept less help from Medicare and Social Security while paying more of your salary to FICA, America could survive financially.

You working stiffs who struggle to pay for food, clothing, a car, a few days of vacation, and education for your kids are simply being selfish by asking the government to help you with your medical bills and retirement.

Shame on you, especially when the rich have to scrimp along on the few millions they get from tax loopholes. After all, rich Donald Trump paid minimal taxes in three of the past ten years. What more do you expect?

In order to help the Federal Reserve fight inflation, reduce interest costs, and support economic growth, policymakers should put forward a plan to put the national debt on a sustainable long-term path.

Though there is no one single “correct” fiscal metric, the higher the debt-to-Gross-Domestic-Product (GDP) ratio and its growth trajectory, the more vulnerable the U.S. economy is.

If you believe those two sentences, you have been royally conned. They are lies.

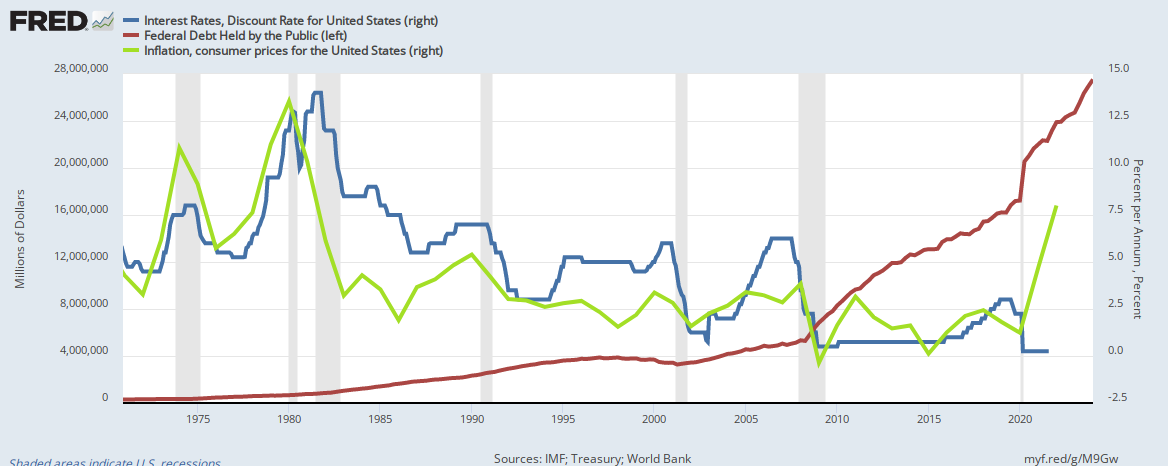

You have been fed the same baloney since at least 1940 when the “debt” first was called a “ticking time bomb.” The so-called “national debt” was only $40 billion back then.

Today, it’s somewhere in the neighborhood of $25 TRILLION, an astounding 62,400% increase. Yet here we are. Still sustaining. How is that possible?

First, the so-called national debt isn’t really a debt; second, it is infinitely sustainable. The federal “debt” is two different things united by an unnecessary law.

I. The so-called “debt” is the net total of federal deficits, i.e., the difference between federal income (mainly tax collections) and federal spending.

But, while state/local government taxes fund state/local government spending, federal taxes do not fund federal spending. The Monetarily Sovereign federal government destroys every tax dollar it receives, and it funds all its spending by creating new dollars, ad hoc, every time it pays a bill. It works like this:

When you pay taxes, you take dollars from your checking account. Those dollars are part of the “M2” money supply measure.

When those dollars reach the U.S. Treasury, they suddenly are not part of any money supply measure. Because the federal government has infinite dollars, there is no measure of the government’s money.

Your tax dollars disappear from existence. They effectively are destroyed.

State/local governments, being monetarily non-sovereign, put tax dollars into banks, where they continue to be part of the M2 money supply measure. While state/local government debt really is debt, the federal government has infinite money, so it has no measurable debt.

II. The so-called “debt” is the total of deposits into Treasury security accounts resembling bank safe deposit boxes. You put money into your T-security account, the government adds some money, and later, when the account matures, the government returns the dollars already in your account — just like your safe deposit box.

The contents of the boxes are yours, from beginning to end. The government doesn’t “owe” them to you because you never lose ownership of them. The government isn’t indebted to you for those dollars any more than the banks are indebted to you for the box’s contents.

In both cases, the bank and the government do not touch the contents of the “account box.” The government and banks simply store them for you.

Another reason why that misnamed “debt-that-isn’t-a-debt” is infinitely sustainable: The federal government, being Monetarily Sovereign, has the infinite ability to create its sovereign currency, the U.S. dollar.

It never, never, never can unintentionally run short of dollars.

Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes: Scott Pelley: Is that tax money the Fed is spending? Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

In plain English, the federal government does not borrow dollars. Nor does it rely on taxes. It creates dollars, at will, by pressing computer keys.

Implant this in your mind: THE U.S. GOVERNMENT CANNOT UNINTENTIONALLY RUN SHORT OF DOLLARS. NOT TODAY. NOT TOMORROW. NOT EVER.

Even if the misnamed “debt” doubled or tripled tomorrow, that would have zero effect on the federal government’s ability to pay its bills.

And what goes for the government as a whole also goes for federal agencies. Medicare cannot run short of dollars unless that is what the President and Congress want.

Similarly, Social Security cannot run short of dollars unless that is what our leaders want.

The next time you hear some Congressperson expressing anguish about the “debt” or the “debt ceiling,” you can be sure he/she is lying or ignorant about federal finances.

And when you hear that the Medicare or Social Security fake “trust funds” are running short of money, you will know you are hearing the most dangerous and harmful conspiracy theory in America.

The conspiracy theory continues:

Ideally, debt should be gradually reduced to its half-century historical average of about 50 percent of GDP.

The “debt”/GDP ratio is 100% meaningless. It has no predictive value. It tells you nothing about the federal government’s ability to pay its bills. “Debt” is a measure that accounts for the full lifetime of America. GDP is a one-year measure.

“Debt” is the difference between federal income and federal spending. GDP is total spending (federal + non-federal) + net exports. They are as comparable as apples vs. Apple computers.

Here are the nations having the lowest Debt/GDP ratios: Suriname, United Kingdom, Mauritania, Costa Rica, Tunisia, Brazil, El Salvador, Croatia, Sao Tome/Prin, Austria, Belize, India, Bahamas, Hungary, Morocco, Slovenia, Albania, Qatar, Mauritius, Yemen, Trinidad/Tobago, Sierra Leone, Montenegro, South Africa, Sudan

Here are the nations having the highest Debt/GDP ratios: Japan, Greece, Lebanon, Italy, Singapore, Cape Verde, Portugal, Angola, Bhutan, Mozambique, United States, Djibouti, Jamaica, Belgium, France, Spain, Cyprus, Bahrain, Jordan, Egypt, Canada, Argentina.

What generalizations can you make about these nations? What does the Debt/GDP ratio tell you about their financial health? Absolutely nothing.

Yet it is quoted frequently by those who either want to fool you or are ignorant about national finances.

Every time you see or hear someone quoting that ratio as having some importance, know this: That person should not be listened to.

Given political constraints, we suggest at least stabilizing the debt at its current level within a decade, requiring roughly $7 trillion in savings.

The CRFB wants to reduce the “debt” by $7 trillion — about 25% — guaranteeing a depression that would make 1929 look like Christmas. What the CRFB doesn’t want you to know is every time we reduce the “debt,” we have a recession or a depression:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

The Great Depression, which some “experts” claim was caused by “excessive speculation” or some other myth, actually was caused by federal surpluses.

The federal surplus President Clinton loves to boast about led to a recession that President Bush had to deal with.

Mathematically, a growing economy requires a growing supply of money, but federal surpluses take dollars out of the economy and destroy them, which leads to reduced economic growth or negative economic growth.

(The CRFB) blueprint puts forward a framework to achieve these goals through a combination of revenue and spending changes – with savings from health care, tax reform, discretionary spending caps, energy reforms, Social Security solvency, and other changes to the budget.

About 40 percent of the deficit reduction comes from revenue and 60 percent from changes in spending.

And virtually all of the deficit reduction comes from the middle classes and the poor.

Translation: The CRFB wants to cut Medicare (“health care”), increase the FICA tax (“tax reform”), reduce aids to the poor (“discretionary spending caps”), ignore global warming (“energy reforms”), and cut Social Security (“Social Security solvency”).

The very rich are laughing all the way to the bank.

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

……………………………………………………………………..

Government’s Sole Purpose is to Improve and Protect the People’s Lives.

MONETARY SOVEREIGNTY