I have been reading the Libertarian articles in Reason.com for several years and have noticed something odd. Despite ongoing claims that federal spending should be reduced, no data can support that myth.

Like all other debt Henny Pennys, they focus on telling you how big the so-called debt is and how much will be spent on benefits. OK, we get it. The numbers are significant, but why are they bad?

But there never is data. It is all speculation supported by more speculation.

The following article is no exception:

CBO Projects Huge Deficits, $116 Trillion in New Borrowing Over the Next 30 YearsA new Congressional Budget Office report warns of “significant economic and financial consequences” caused by the federal government’s reckless borrowing.Merely paying the interest costs on the accumulated national debt will require a staggering 35 percent of annual federal revenue by the end of that time frame. | 6.29.2023 11:00 AM

And what will those “significant economic consequences” be? And where is your evidence?

The federal government is on pace to borrow $116 trillion over the next 30 years, and merely paying the interest costs on the accumulated national debt will require a staggering 35 percent of annual federal revenue by the end of that time frame.

And that’s likely an optimistic scenario.

Actually, it is an optimistic scenario. Mathematically, the more the federal government spends, the more the economy grows. Why? Because the economy is measured by Gross Domestic Product (GDP) and:

GDP = Federal Spending + Nonfederal Spending + Net Exports

That $116 trillion in “borrowing” is not borrowing. It is the acceptance of deposits into Treasury Security accounts. The U.S. federal government never borrows dollars.

Why would it? The federal government has the infinite ability to create (aka “print”) dollars, so why would it ever need to borrow what it can create at no cost, especially since borrowing requires paying interest?

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Get it, Libertarians? The U.S. government is not dependent on credit markets. It doesn’t borrow.

Let me rephrase your comment: ” . . . merely paying the interest costs on the accumulated deposits into T-security accounts will require a staggering 35 percent of annual federal revenue by the end of that time frame.

Why is it “staggering” if Greenspan, Bernanke, and the St. Louis Fed say the government never can run out of dollars? Even if annual revenue totaled $0, the federal government could continue spending forever.

Those sobering figures were published Wednesday by the Congressional Budget Office (CBO) as part of the number-crunching agency’s new long-term budget outlook.

The report once again points to an unsustainable fiscal trajectory driven by a federal government that’s addicted to borrowing—even as it becomes readily apparent that the bill is coming due.

It’s Libertarian nonsense. Why is it “unsustainable”? And since the government never borrows, what is the “addiction”? And exactly what bill is “coming due”?

The problem is Eric Boehm, and the rest of the Libertarians do not wish to acknowledge the fundamental difference between personal finance and federal finance.

In short, they don’t seem to understand the difference between Monetary Sovereignty and monetary non-sovereignty. And not understanding those fundamental differences means they don’t understand economics. At all.

Are they being devious or simply ignorant? I don’t know. I vote for devious. In my opinion, they have an agenda and are just pretending to be ignorant.

“Such high and rising debt would have significant economic and financial consequences,” the CBO warns.

Among other things, the mountain of debt will “slow economic growth, drive up interest payments to foreign holders of U.S. debt, elevate the risk of a fiscal crisis, increase the likelihood of other adverse effects that could occur more gradually, and make the nation’s fiscal position more vulnerable to an increase in interest rates.”

In what way does federal deficit spending “slow economic growth” when Federal Spending increases GDP by simple algebraic formula?

As for interest payments, here’s the Libertarian theory: To acquire the dollars to pay its bills, the federal government needs to borrow. And because it needs to borrow so much, it has to raise interest rates to attract lenders.

Wrong. The government never needs to borrow and, indeed, never borrows. The Fed determines the interest it pays on Treasury Securities, not to attract lenders but to regulate the economy.

Example: Of late, interest on T-securities has gone up significantly, not because the Fed wants to attract more depositors, but because the Fed thinks that’s how to reduce inflation. Interest rates have nothing to do with the government needing dollars to pay its bills.

As for foreign holders of U.S. “debt,” that is a convenience for foreigners. The Fed doesn’t give a fig whether Russia or China deposits dollars into Treasury Bill accounts. The purpose of those accounts is not to give America it own dollars. The purpose is to provide the Russians, Chinese et al. a safe place to deposit unused dollars.

Further, what is the “fiscal crisis” the CBO worries about? The government always can pay its bills. If a creditor were to demand that the U.S. federal government pay $100 Trillion tomorrow, a functionary at the Federal Reserve would press a computer key, and the $100 Trillion instantly would be transferred to the creditor’s account.

The CBO’s erroneous claims end with: ” . . . increase the likelihood of other adverse effects that could occur more gradually, and make the nation’s fiscal position more vulnerable to an increase in interest rates.”

We don’t know what the “other adverse effects” supposedly are. We suspect the CBO has no idea, either.

Finally, the federal government’s fiscal position is invulnerable. It can pay any bill of any size at any time it chooses.

The formula for massive deficits and unsustainable levels of borrowing is actually pretty simple: federal spending that far exceeds what the government collects in tax revenue.

Because the federal government has the infinite ability to create U.S. dollars, it neither needs nor even uses tax revenue to pay its bills. So why does it collect taxes at all?

Three reasons:

To control the economy by taxing what it wishes to discourage and giving tax breaks to what it wishes to encourage.

To assure demand for the U.S. dollar and thus stabilize the dollar by requiring taxes to be paid in dollars.

To make the public believe federal spending is limited by taxes and reduce public requests for benefits

As for #3, the rich who run America do not want the non-rich to receive the benefits that would narrow the Gap between the rich and the rest. The Gap makes the rich rich; the wider the Gap, the richer they are.

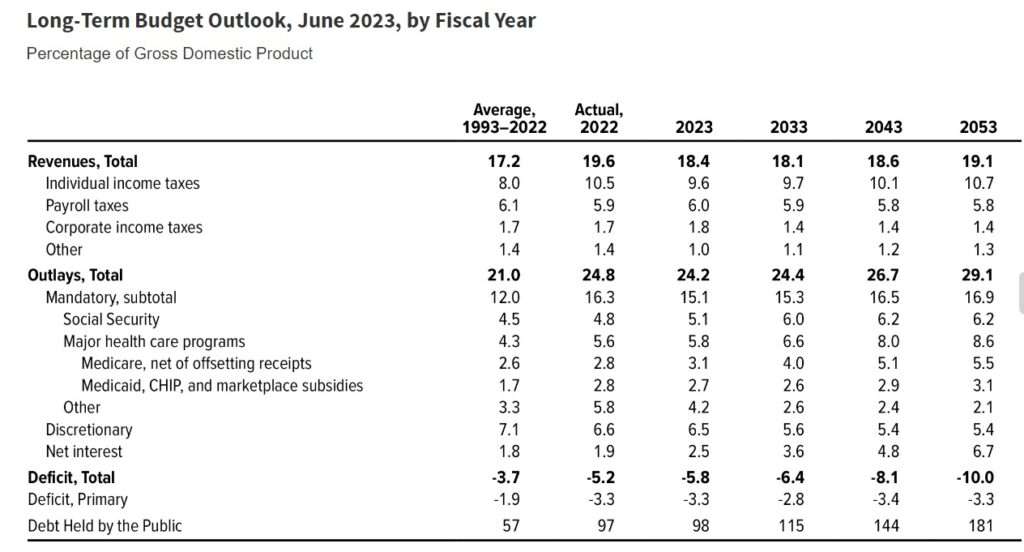

Over the past 30 years, federal spending has averaged 21 percent of gross domestic product (GDP), a rough measure of the size of the whole American economy, while tax revenue has averaged 17.2 percent, the CBO notes. That’s not great, but the future looks much worse.

By 2053, the CBO expects federal spending to grow to 29.1 percent of GDP while revenue climbs to just 19.1 percent.

From being exposed to the above table, you might be led to believe that Federal Spending/GDP or federal taxes/GDP are essential measures. They aren’t.

The first fraction tells you how much the federal government spends vs. the domestic private sector. What can you do with that information? Not much.

You might wish to increase private sector spending, probably requiring federal tax reduction, which is almost always a good idea. And you should increase exports which need federal aid to exporters, though that might run afoul of international agreements.

What you do not want to do is cut federal spending. That will only reduce GDP, which would only make it worse if you are concerned about the Federal Spending/GDP fraction.

As for the Federal Taxes/GDP fraction, the analysis is straightforward. The more significant the fraction, the worse will be economic growth. Sadly, the CBO complains that the fraction will be getting smaller — Federal Spending will grow faster than GDP — and here is the crucial part: GDP is projected to grow.

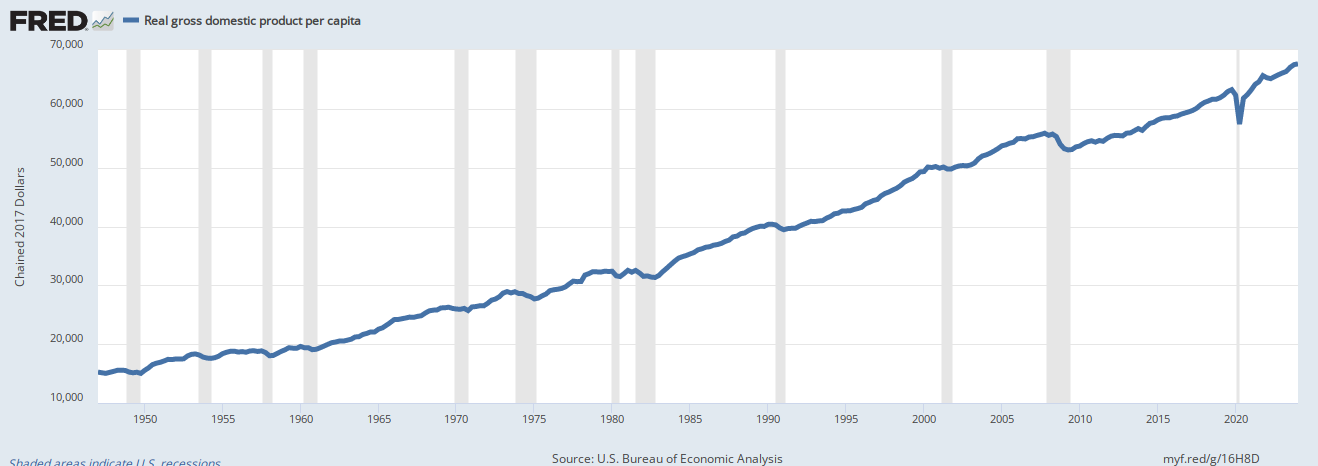

Even more importantly, real(inflation-adjusted) GDP has been growing per capita. That means despite all the moaning and groaning from the Libertarians and the CBO, Americans are getting richer. Here are the data:

Real Per Capita Gross Domestic Product

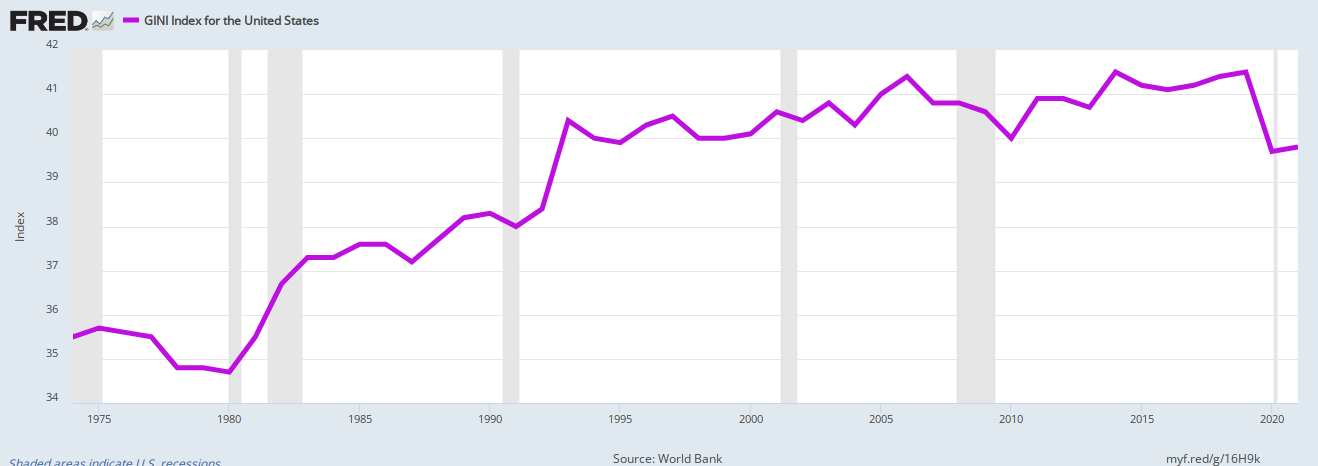

That, my friends, is a picture of a healthy economy — uh, except for this:

The GINI index shows the distribution of wealth. A level of “0” would mean everyone has the same wealth. A level of “1” would mean one person has all the wealth. The graph shows the rich getting more affluent than the rest of us, with only a small drop from 2019 to 2020.

Keep the GINI index in mind when you read about the Libertarians and the Republicans wanting to cut “Entitlements” (Social Security, Medicare, Medicaid), school lunch programs, and other poverty aids.

The oft-quoted Federal Debt/GDP ratio is equally meaningless. It compares the amount deposited into T-security accounts by foreign nations, domestic companies, and Americans (aka “Federal Debt) vs. the amount spent by Americans and net imports.

This ratio often is cited as something to be concerned about. Yet it has no predictive or analytic value. A low ratio is neither a sign of a healthy nor sick economy. It is not a prediction of the future nor a measure of the past.

GDP doesn’t pay for Federal Debt, and Federal Debt doesn’t pay for GDP. Yet some so-called “economists” wring their hands when the ratio increases.

The only relationship between the two is when Federal Debt increases, which helps GDP increase, though all the bleating about this ratio would make you think otherwise.

Entitlements are the primary driver of that future spending surge. Social Security spending will rise from about 5 percent of GDP to about 6.2 percent over the next 30 years. Costs for Medicare and Medicaid will jump from 5.8 percent of GDP to 8.6 percent by 2053.

And there it is. The right-wing pitch is to reduce Social Security, Medicare, and Medicaid. The purpose is to widen further the Gap between the rich and the rest.

Financing the national debt will become a major share of federal spending in the next few decades. The CBO projects that interest payments on the debt will cost $71 trillion over the next 30 years and consume more than one-third of all federal revenue by the 2050s.

As Greenspan, Bernanke, and the St. Louis Fed reminded us, it costs the U.S. government nothing to create those dollars; that dollar creation has been enriching Americans for decades.

“America’s fiscal outlook is more dangerous and daunting than ever, threatening our economy and the next generation,” Michael A. Peterson, CEO of the Peter G. Peterson Foundation, which advocates for fiscal responsibility, said in a statement.

The group responded to the new CBO report by renewing its calls for a bipartisan fiscal commission to consider plans for stabilizing the debt.

To a rich guy like Michael A. Peterson, “fiscal responsibility” means soaking the poor and middle-income groups while giving tax breaks to the rich.

Stabilizing the debt” means creating recessions and depressions, during which the rich will buy all those low-priced assets to increase domination over the rest of us.

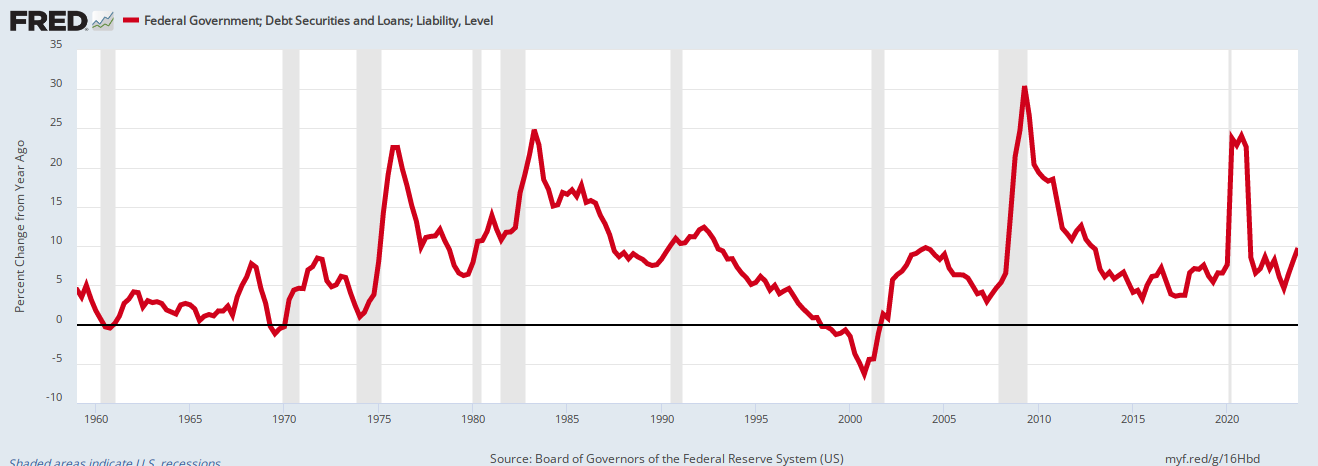

Here is precisely what happens when we “stabilize the debt” as rich Mr. Peterson wishes”

When federal “Debt” growth (red) declines (“Debt” is stabilized), we have recessions (gray bars). To cure recessions, the government increases “Debt.” GDP = Federal Spending + Nonfederal Spending + Net Exports.

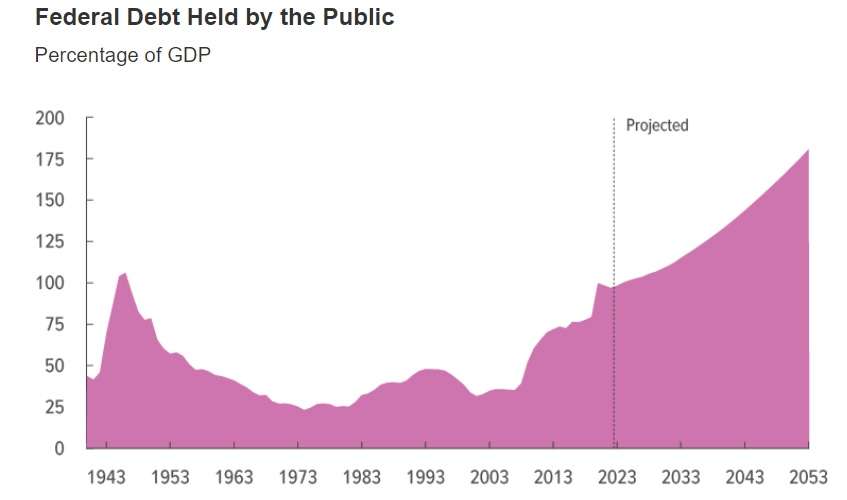

The national debt reached a record high of 106 percent as a share of GDP during World War II. The CBO projects the record to be broken in 2029, and the debt will keep climbing—to 181 percent of GDP by 2053.

A meaningless graph that tells you nothing about the U.S. economy yesterday, today, or tomorrow.

Even something called the “World Population Review” is hypnotized by this meaningless ratio. Here is what they say:

Typically used to determine the stability and health of a nation’s economy, the debt-to-GDP ratio is expressed as a percentage and offers an at-a-glance estimate of a country’s ability to pay back its current debts.

And here are the examples they give:

Top 12 Countries with the Highest Debt-to-GDP Ratios

Venezuela — 350%

Japan — 266%

Sudan — 259%

Greece — 206%

Lebanon — 172%

Cabo Verde — 157%

Italy — 156%

Libya — 155%

Portugal — 134%

Singapore — 131%

Bahrain — 128%

United States — 128%

Top 12 Countries with the Lowest Debt-to-GDP Ratios (%)

Isn’t it nice to know that all these countries — Russia, Afghanistan, Botswana, et al. — supposedly are more stable and healthy and better able to pay back their current debts than the United States and Japan?

It must be true because that is what the Libertarians, the CBO. Michael A. Peterson and the World Population Review are telling you.

So be sure to tell all your creditors not to pay you dollars because you’d rather receive Russian rubles. Right?

The (CBO’s) projections leave out the possibility that Congress will extend the Trump administration’s tax cuts past their planned expiration in 2025—which would add to the deficit and require more borrowing in the future—or the possibility that Social Security’s impending insolvency will be papered over with yet more borrowing.

The United States cannot become insolvent. Per Former Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Because the U.S. can’t become insolvent, Social Security, a federal agency, can only become insolvent if that is what Congress and the President want.

What the author calls “papered over” normal people would call “paying for,” which the government can do simply by pressing a computer key.

And do you really believe that no Congress or president will hike spending without offsetting tax increases in the next three decades?

If Congress and the President increase taxes they will not “offset” anything. Federal taxes do not fund federal spending. They are destroyed upon receipt, and new dollars are created ad hoc to pay for expenditures.

Under an alternative scenario in which the Trump administration’s tax cuts are extended, and federal spending grows at the same rate as the economy (rather than in line with inflation, as the CBO assumes), the Committee for a Responsible Federal Budget projects the debt to hit 222 percent of GDP by 2053.

And that 222 percent will have no meaning.

There’s one shred of good news inside the CBO’s latest report, however. Compared to last year, long-term borrowing is expected to be slightly lower. That resulted from the debt ceiling deal struck last month between Congress and the White House.

The deal included spending caps on nondefense discretionary spending for the next two years, and even that minimal bit of fiscal responsibility can have a measurable impact on future deficits.

This is terrible news. A limit on spending growth is, by definition, a limit on economic growth. Could you remember the formula for measuring the economy?

Still, the modest decline in future deficits mainly illustrates the daunting size of the federal government’s debt problem. By 2053, the debt will more than double the size of America’s economy—and, again, that’s only if you assume borrowing won’t increase for any reason in the next three decades.

“This level of debt would be truly unprecedented,” said Maya MacGuineas, president of the Committee for a Responsible Federal Budget, in a statement. “Time is of the essence; we simply cannot afford to keep borrowing at this unsustainable rate.”

May MacGuineas is another Henny Penny paid by the rich to claim that the middle and poor should receive less money.

Good heavens, one needs to learn only five simple facts, and even that seems to be too much for the economic “experts.”

Gross Domestic Product (the economy) = Federal Spending + Nonfederal Spending + Net Exports

The U.S. government (unlike state/local governments, euro nations, businesses, you, and me) is Monetarily Sovereign. It, and any of its agencies, can only run short of its sovereign currency if Congress and the President will it.

Federal taxes (unlike state/local government taxes) pay for nothing. They are destroyed upon receipt by the Treasury.

Having the infinite ability to create dollars, the government never borrows. The so-called “debt” actually is deposited into T-security accounts. Those dollars remain the depositor’s property, never used by the federal government for anything, and “paid off” by returning them to the owners.

Inflation never is caused by money creation. It always is caused by shortages of crucial goods and services, most often oil and food.

If you understand these five facts, you know more than most economists, politicians, and media writers.

Just five things. Is that so hard?

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

For years, there has been increasing concern about our growing trade deficit, especially with China. But do trade deficits really benefit us?

China creates the goods/services we want and sends them here in exchange for dollars. The goods/services are scarce to China. Time, manpower and physical resources are necessary for their creation. By contrast, dollars are not scarce to the U.S. Our government has the unlimited power and authority to produce dollars, without using any resources, whatsoever. The press of a computer key sends billions of dollars from our government to anywhere. Lately, many have gone into our economy as a stimulus.

A trade deficit is an example of one country devoting great effort to creating scarce materials for another country in exchange for something that requires no effort by the other country. In that sense, China is our servant. They work, sweat and strain and use their valuable resources to create and ship to us the things we want, while we, hardly lifting a finger, ship dollars to them. Who has the better deal?

Obviously, for any given individual, the situation is different. None of us has the unlimited ability to create dollars. We have to work hard for our dollars. Dollars are scarce to each of us. But when we talk about trade deficits, we are talking about governments, and there the situation changes. Dollars are not scarce to the U.S. government.

To satisfy our desires, China could ship us every yard of cloth and every ounce of steel in their country; they could burn all their coal and oil; they could employ every man, woman and child in dismal sweatshops; they could empty their nation of all physical resources, and still we would have plenty of dollars to send to them, simply by touching a computer key.

This may be more easily understood by looking at Saudi Arabia, with whom we also have a trade deficit. One day, the Saudis will have sent us every drop of their oil, leaving their country a hollow, empty sand dune, while we blithely will go on producing dollars. Who has the better deal?

Of course, as monetarily sovereign nations, China and Saudi Arabia are able to create as much of their own money as they wish. They don’t need to work so hard to send us their precious resources in exchange for our money. But that’s a discussion for another posting.

An alternative to popular faith

In the post “Do deficits cure inflation?” we saw that contrary to popular faith, deficit spending (i.e., too much money) has not caused inflation. We also saw that inflation can be cured by increasing the reward for owning money, i.e. by increasing interest rates.

Now we question another piece of popular faith: Is inflation caused by too much money chasing too few goods?

Begin with the notion of “too much money.” We already have seen that federal deficits are not related to inflation. What about another definition of money: M3? Please look at the following graph:

Clearly there is no immediate relationship between money supply and inflation. What about a subsequent relationship. Could “too much money” today, cause inflation later?

The graph indicates no such cause/effect relationship, with M3 peaks preceding inflation peaks by anywhere from 2 years to 10 years. It is difficult to imagine a graph revealing less relationship.

What about “too few goods”? If too few goods caused inflation, this would manifest itself with GDP moving opposite to CPI. Again, that does not seem to happen:

There seems to be no regular pattern, with GDP and CPI sometimes rising together and sometimes separately. In today’s international economy, it is difficult to substantiate the idea of a wide-spectrum commodity shortage when sufficient purchasing power exists.

Individual nations can experience shortages of individual commodities. Individual poor nations can experience shortages of a broad basket of commodities. But can a wealthy nation, with plenty of money to spend, suffer a shortage of a broad basket of commodities, thereby causing inflation? Has it recently happened?

Seems unlikely these days as products are made in multiple nations and shipped to multiple nations, with easy international shipping and instantaneous money convertibility. Your cotton shirt may have been grown in Egypt, woven in India, assembled in China, labeled in Italy and sold in the U.S. Clearly, a cotton shirt shortage would be rare, as any of these steps could occur in various countries, and that’s just one product. A nationwide “too-few-goods” situation, coincident with “too much money,” seems impossible.

There is however, one exception: Oil.

The graph below compares overall inflation with changes in energy prices, which are dominated by oil prices.

Oil is the one commodity that has worldwide usage, affects prices of most products and services, and can be in worldwide shortage. That is why, when oil prices rise or fall steeply, inflation rises and falls in concert.

The large oil price moves “pull” inflation in the same direction. When oil prices increased or decreased the most, inflation came along for the ride.

In summary, inflation is not caused by deficit spending or by “too much money chasing too few goods.” Inflation is caused by a combination of high oil prices and interest rates too low to counter-balance the oil prices.

The high oil prices can be caused by real shortages and/or by price manipulation.

Hyperinflation is a different beast, altogether. Every hyperinflation has been caused by shortages, most often shortages of food.

Zimbabwe, Weimar Republic, and Argentina had food shortages that created hyperinflations.

Just a quick thought: President Barack Obama’s decision to impose trade penalties on Chinese tires has infuriated Beijing. This is eerily reminiscent of Smoot-Hawley. Continued political cave-ins to unions could take us to a depression. At a time like this, the world needs the freest possible trade, not protectionism.