Imagine you being the richest person in the world—the first trillionaire—when your adult daughter comes to you and says, “I have cancer, and my insurance won’t cover the treatments I need to survive. I can’t afford to pay the medical bills.”

” What would you do?

Would you say, “I’m trillionaire; I’ll pay for the cost of your treatment”?

Or would You say, “I don’t care whether you go broke or die. You’ll have to pay because, even though I’m a trillionaire, I don’t want to help you.”

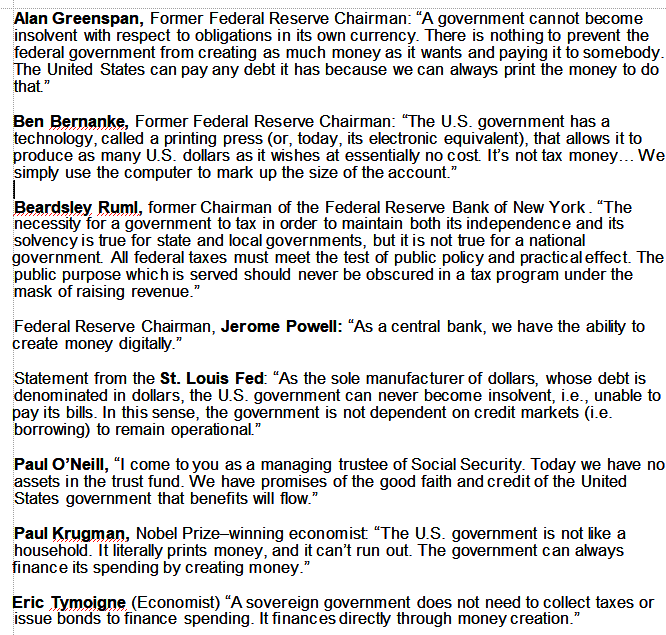

The federal government, being Monetarily Sovereign. Has more money than even a trillionaire. It effectively has infinite money.

Who says so? These experts, listed at the right, and many others.

If four Federal Reserve Chairmen, and many others of similar note, say the government has the infinite ability to pay for anything, without collecting taxes or borrowing, why won’t the government simply pay for a comprehensive, no deductible Medicare for everyone, regardless of age or illness?

This recent article tells the story.

Republicans see high-risk plans as the future of health insurance Story by Kelly Hooper • 20h • 8 min read

The High Deductible PlanHundreds of thousands of Americans have switched to health insurance that covers a lot less of their care this year. Republicans hope a lot more will follow them.

The shift since January was driven by GOP lawmakers’ decision at the end of December to reduce the help the government provides to people who don’t get insurance through work, but instead buy it in the Obamacare marketplace. The reduction in those subsidies sent Obamacare customers searching for plans that cost less.

There’s a catch: The cheaper plans don’t cover the first several thousand dollars in sick visits, drugs and surgeries a patient needs. Nearly 4 in 10 Obamacare enrollees are in these “high-deductible” plans now, compared to 3 in 10 a year ago.

In short, Republicans want to move the financial burden from the government, which can afford it, to lower-income people, who can’t.The reason is that it widens the income, wealth, and power gap between the rich and everyone else. This gap is what makes the rich wealthy—the wider it gets, the richer they become.

Since Republicans are seen as the “party of the rich,” their goal often seems to be helping the rich get richer while the poor get poorer.

President Donald Trump and GOP senators want to encourage more to go that route by shifting remaining Obamacare subsidies, which are now used to reduce monthly premiums, into tax-advantaged savings accounts that come with the high-deductible plans.

That would be very good for some — affluent people in good health who use the savings accounts to accrue wealth — but not so much for others: sicker and poorer people who incur medical bills they can’t afford.

The “Overuse” False ExcuseFor many Republicans, that’s a worthwhile trade-off, considering the plans also reduce overuse of the health care system and put downward pressure on prices.

“The president clearly has said we need to send money to patients rather than insurers in the system, and building out policies that are consistent with that is important,” said Brian Blase, president of the right-leaning Paragon Health Institute and an adviser to Trump in his first term.

Republicans believe that poor Americans tend to “overuse” the healthcare system, whether by visiting the doctor too frequently or undergoing unnecessary surgeries.It’s likely that very few people see a doctor too often or undergo unnecessary surgeries. Regular checkups are encouraged as a cost-seaving and preventive measure, and while some cosmetic procedures might be unnecessary, most of us would rather eat spiders than have surgery we don’t need.

Many high-deductible customers are “chasing after that lower premium, but they actually do need to use care on an ongoing basis, and then they end up with a lot of debt or being terrified to use their insurance or seek care and ignoring symptoms,” said Katherine Hempstead, senior policy adviser at the Robert Wood Johnson Foundation, a progressive health care-focused philanthropy.

The president touted his “Great Health Care Plan” at a Turning Point USA event two weeks ago, promising “to get it done one way or the other.”

The “Save Money” False ExcuseAmong Republicans on Capitol Hill, both Trump allies, like Sen. Rick Scott of Florida, and adversaries, such as Sen. Bill Cassidy of Louisiana, are trying to help.

Cassidy told POLITICO he thought most people would come out ahead given the lower premiums and tax savings. “Your total cost of being insured is less,” he said.

The phrase “being insured” feels like mealy-mouthed double talk. Sure, the overall cost might be lower, but having no insurance at all would be even cheaper. Is that the idea?

Cassidy ignores the fact that deductibles shift costs from the infinitely rich government onto poor sick individuals.

The “Greater Control” False Excuse

For Scott, it’s about giving patients greater control. The change would “radically re-empower the American people and let them dictate more of where their money goes,” he said.

It’s hard to see how deductibles give more “control,” especially when a relatively small federal payment is unlikely to cover the costs of serious illnesses.

One easily could ask, If the Republican proposal offers, better, cheaper insurance, would Senators be willing to use their own proposed plan?

A mass shift to high-deductible plans could leave millions of Americans who recently lost access to Obamacare subsidies vulnerable to unexpectedly high costs, health policy experts said.

“You’re going to have parallel-marketed plans — next to comprehensive ACA plans — that are loosely regulated, that may look attractive at first because they they appear to have lower premiums, but then you come to find out when you actually need to use the plan you’re stuck with much higher out-of-pocket costs and fewer consumer protections,” said Michelle Long, a senior policy manager for the Program on Patient and Consumer Protections at KFF, a health policy research organization.

The “Most People” DoubletalkSen. Bill Cassidy (R-La.) thinks most people would come out ahead under his plan to direct Obamacare subsidies into individuals’ HSA accounts when they enroll in low-premium, high-deductible plans.

In fact, most people would be better off financially if they didn’t buy any insurance at all. That’s what makes insurance companies profitable. If most people came out ahead by purchasing insurance, there wouldn’t be any private insurers.You can be certain that Cassidy knows this.

Cassidy, the Health Committee chair, is leading a bill with the Finance chair, Mike Crapo (R-Idaho), that would direct federal funds used for Obamacare subsidies instead to individuals’ HSA accounts when they enroll in low-premium, high-deductible plans.

If the government were to put $2,000 into enrollees’ health savings accounts, Cassidy said, that would cover the annual medical expenses of the average American.

Scott said his proposal would do more to lower costs by allowing people to save in new Trump Health Freedom Accounts in any type of insurance plan. Currently, only people in high-deductible plans can open HSAs.

Scott’s plan would also let states waive certain ACA requirements, including coverage of essential health benefits, to lower premiums. That could leave enrollees who get sick on the hook for unexpected bills.

The plan is consistent with Trump’s efforts to offer more choices for Obamacare enrollees outside traditional ACA plans, including expanding short-term health plans, which Democrats have derided as “junk insurance.”

No matter how many twists, turns, and fake options the Republicans add to confuse the public, the goal remains the same: Have the government spend less and the people spend more.

The Trump administration has also proposed a marketplace rule that would crack down on fraudulent ACA enrollments and expand several alternative plan options, including catastrophic plans — lower-premium plans that cover Obamacare’s essential health benefits but come with a more than $10,000 deductible for an individual in 2026. Trump also proposes allowing the sale of so-called non-network plans on the ACA marketplace, which typically come with high deductibles but have no networks of doctors or providers, an option some employers currently offer.

If all these options leave you feeling confused, that’s exactly the point: toss in dozens of variations to make you believe you’re paying less, when the real goal is to have you pay more while thinking you’re getting a deal.

If insurers take a financial hit as a result of the policies, they might hike premiums across the market, raising costs for large swaths of Obamacare enrollees regardless of what plans they’re in. And the plans might not provide much protection for an unexpected medical event.

What politicians don’t mention is that while federal spending doesn’t cost taxpayers directly, it actually helps grow the economy. They complain about hospitals, doctors, and pharmaceutical companies charging “too much,” but overlook the fact that this money circulates through the economy and ends up in everyone’s pockets.

Insurers and providers argue the plans would leave consumers vulnerable to high out-of-pocket costs. vers just because they’re armed with pricing data.

“What you might see instead is somebody who gets duped into thinking it’d be better to have a lower-tier plan and $2,000. That could be a really terrible trade-off for them, because that $2,000 won’t last long if something really happens, and they’re just going to have a way more exposure to debt.”

THE REAL SOLUTION

The government exists to protect and enhance the well-being of its people, and in return, we provide it with money and grant it authority over certain aspects of our lives.

Since the U.S. federal government has unlimited funds, it can cover services that would be expensive for individuals, such as military defense, legal protections, and healthcare.

The federal government can afford to fund — without collecting a penny in taxes — a comprehensive, no-deductible Medicare plan for everyone in America, regardless of age or health.

This would not only include all services from doctors, nurses, and hospitals, but also educational programs to train more doctors and nurses, along with funding for pharmaceutical R&D and equipment manufacturers.

A holistic approach to funding America’s health could not only cost taxpayers nothing and boost healthy longevity but also generate billions in economic growth. Cost no longer would be an issue, because the dollars would circulate through the economy and benefit everyone, both economically and physically.

If we ever can educate America on the huge possible benefits of Monetary Sovereignty, we’ll finally become the great nation we’ve always aspired to be.

Rodger Malcolm Mitchell

Twitter: @rodgermitchell

Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell;

MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell;

……………………………………………………………………..

A Government’s Sole Purpose is to Improve and Protect The People’s Lives.

MONETARY SOVEREIGNTY

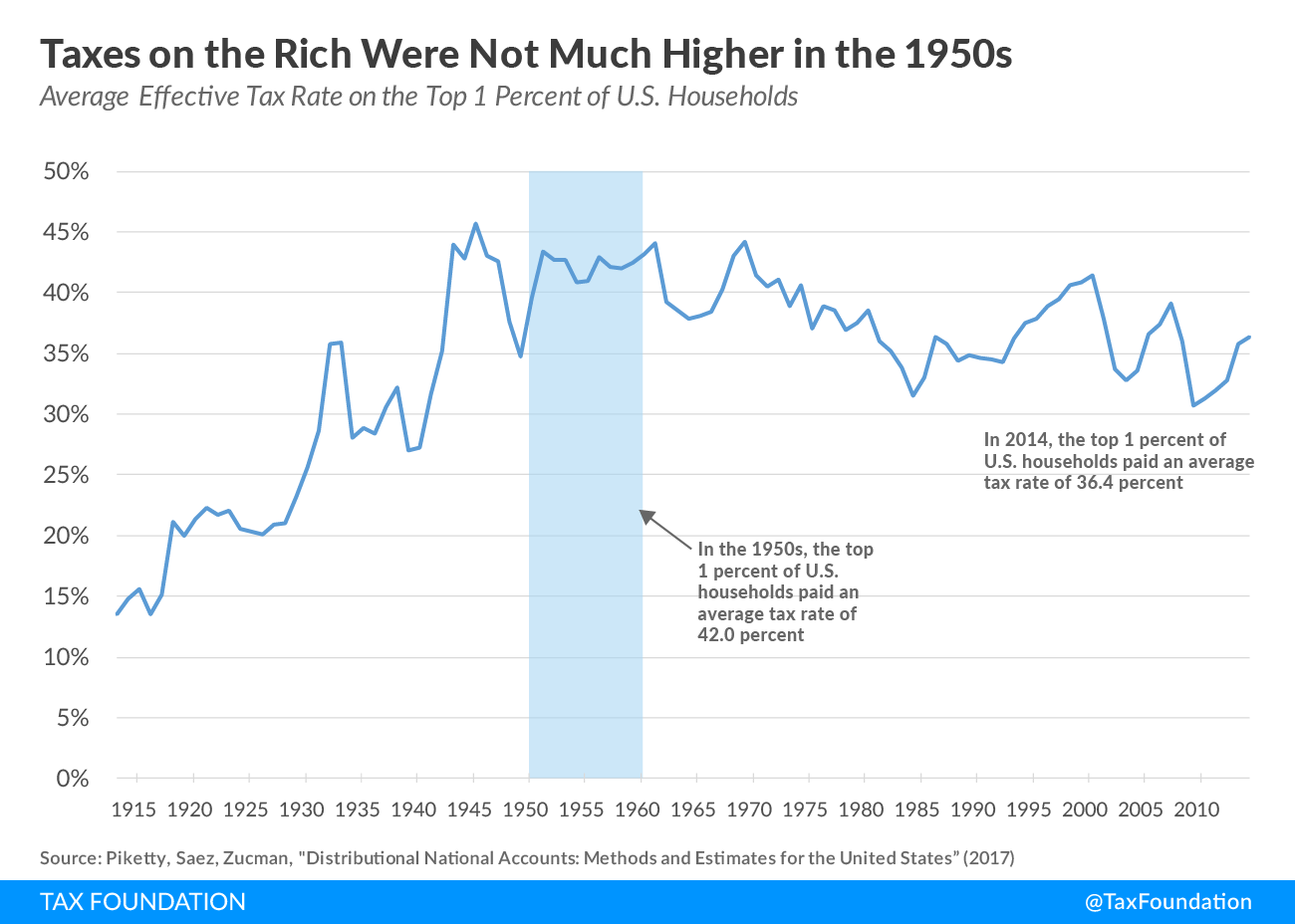

Considering that the top tax rate in the 1950s was 90%, the rich did not pay much more in that period than they do now. And some of the richest among us pay little if anything.

For example, Donald Trump paid no income taxes at all, during ten of the fifteen years, 2000-2015, despite being a billionaire. Tax laws, favorable to the rich, gave him the ability to claim losses on investments that an ordinary taxpayer may not look at as “losing” money.

In summary, using federal taxation of the rich to narrow the Gap is bad economics. History shows the rich would find ways to avoid paying higher rates.

But, even if the rich were forced to pay more, the higher rates would take dollars out of the economy and recess the economy. Option #1 is a “heads-you-lose (the rich don’t pay more), tails-you-lose” (GDP falls) plan.

Sadly, that is the plan Biden seems to have chosen, and it will cost him the November election.

The electorate may be ignorant about economics, but the rich would make sure the voters understood that raising taxes — anyone’s taxes — would hurt the economy.

It’s simple math. The more the federal government takes out of the economy, the less the economy (GDP) has.

Reducing federal taxes and/or providing supplementary benefits to those who are not rich, (#2 and #3) are the sole economically sensible ways to narrow the income/wealth/power Gap.

Sadly this sensible approach is blocked by the non-sensible belief that federal deficit spending is

Considering that the top tax rate in the 1950s was 90%, the rich did not pay much more in that period than they do now. And some of the richest among us pay little if anything.

For example, Donald Trump paid no income taxes at all, during ten of the fifteen years, 2000-2015, despite being a billionaire. Tax laws, favorable to the rich, gave him the ability to claim losses on investments that an ordinary taxpayer may not look at as “losing” money.

In summary, using federal taxation of the rich to narrow the Gap is bad economics. History shows the rich would find ways to avoid paying higher rates.

But, even if the rich were forced to pay more, the higher rates would take dollars out of the economy and recess the economy. Option #1 is a “heads-you-lose (the rich don’t pay more), tails-you-lose” (GDP falls) plan.

Sadly, that is the plan Biden seems to have chosen, and it will cost him the November election.

The electorate may be ignorant about economics, but the rich would make sure the voters understood that raising taxes — anyone’s taxes — would hurt the economy.

It’s simple math. The more the federal government takes out of the economy, the less the economy (GDP) has.

Reducing federal taxes and/or providing supplementary benefits to those who are not rich, (#2 and #3) are the sole economically sensible ways to narrow the income/wealth/power Gap.

Sadly this sensible approach is blocked by the non-sensible belief that federal deficit spending is