- Drinking water during physical activity causes cramps.

- Applying heat to sore muscles prevents stiffness.

- Swimming in the summer causes polio.

Associated Press Treasury warns of need to deal with national debt limit By MARTIN CRUTSINGER, AP Economics WriterWe see that the article was written, not by some uninformed amateur, but by the Associated Press’s Economics Writer.

WASHINGTON (AP) — The Treasury Department says it will employ measures to avoid an unprecedented default on the national debt this summer, but officials say those measures could be exhausted “much more quickly” than normal given the unusual circumstances of the global pandemic.The national “debt” is the total of deposits into Treasury Security accounts. When you invest in a T-bill, T-note, or T-bond, you open a T-security account. This account most closely resembles a bank safe-deposit box into which you deposit money. The money never leaves your box until you take it, just as the dollars never leave your T-security account until you take them.

The Treasury will continue to initiate the types of bookkeeping maneuvers it has used in the past to keep the government from breaching a level that would trigger a default on the massive national debt.The Treasury, the Federal Reserve, and Congress all are agencies of the federal government. Among them, they have created all the rules regarding federal finances. Those “bookkeeping maneuvers” are under the absolute control of the federal government. Nothing can “trigger a default” unless the federal government wishes it.

“In light of the substantial COVID-related uncertainty about receipts and outlays in the coming month, it is very difficult to predict how long extraordinary measures might last,” Brian Smith, Treasury’s deputy assistant secretary for federal finance said.They are not “extraordinary” measures. They simply would be bookkeeping adjustments. The federal government created its byzantine bookkeeping system to suit its unique needs, and this system arbitrarily is changed whenever the federal government wishes to change it. No set of circumstances ever can force the federal government to “default” on any of its financial obligations.

The government has been able to borrow enormous sums of money to finance trillions of dollars of support during the pandemic because the limit on borrowing has been suspended. But after July 31, the limit will return to whatever debt level exists at that time.The federal government has the infinite ability to create its own sovereign currency, the U.S. dollar. In the 1780s, the federal government created from thin air, an arbitrary number of U.S. dollars and gave each dollar an arbitrary value. Since then, the government arbitrarily has created trillions of U.S. dollars, and has given those dollars arbitrary values. Having this infinite ability eliminates any need to borrow dollars. And indeed, the U.S. federal government does not borrow. T-bills, T-notes, and T-bonds do not represent borrowing. They are deposits into accounts, the purposes of which are:

- To provide a safe parking place for unused dollars, which helps stabilize the dollar, and

- To help the Federal Reserve control interest rates which helps to control inflation.

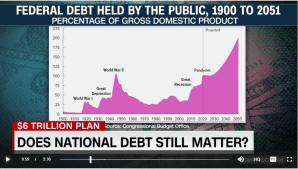

The national debt subject to the limit now stands at a record $28.1 trillion. That amount covers debt the government owes to itself in the form of commitments to Social Security and other government trust funds. The amount of the debt that is held by the public currently totals $22.1 trillion, an amount slightly higher than 100% of the entire economy and heights not seen since the huge borrowing the government did in the 1940s to finance World War II.The fact that deposits into T-security accounts exceed Gross Domestic Product is relevant of nothing. This is known as the Debt/GDP ratio, which though often quoted, has no meaning whatsoever. It predicts nothing, and it evaluates nothing. It does not indicate the past, current, or future health of the economy. It is no better an economic measure than would be the number of runs scored by the Chicago Cubs in the 2nd inning of their next game.

Borrowing has soared in recent years to finance huge budget deficits that reflected increased spending on domestic and military programs in budget deals then-President Donald Trump reached with Congress and also to cover the costs of Trump’s $1.5 trillion tax cut approved by Congress in December 2017.The federal government does not borrow, and so called “borrowing” does not finance federal spending. The federal government finances its spending by creating dollars, ad hoc. The more it spends, the more dollars it creates. Spending is the federal government’s method for creating dollars. In its infinite wisdom, Congress created rules that require the issuance of T-securities to equal in value the net total of federal government deficits (the excess of spending vs. income). Because these rules are obsolete (if they ever had any value), the government, rather than eliminating the rules, instituted a “cheat.” One branch of the government (the Federal Reserve) creates from thin air, dollars to deposit into T-security accounts, to satisfy the needs of a useless rule. Thus, the Federal Reserve owns about $6 trillion of U.S. “debt.” If need be, the Federal Reserve could own all of U.S. “debt,” or the entire “debt” system could be eliminated.

Over the past year, the higher deficits have reflected the trillions of dollars the government has spent to provide support during the pandemic-triggered recession. In the latest package, President Joe Biden got Congress to approve $1.9 trillion in March to provide $1,400 payments to individuals and other types of support for individuals and small businesses.The President and Congress simply passed laws that create spending. No law was made regarding the funding of this spending, because no law was necessary. Federal spending creates its own funding.

Treasury officials did not specify what measures it will employ if Congress has not acted by the July 31 deadline to either raise the borrowing limit or simply suspend the limit for a period of time. What Treasury essentially uses book-keeping maneuvers to avoid a debt default. They basically entail withdrawing money invested in government accounts such as the fund that covers government pensions. The money is always replaced with any lost interest once the debt limit standoff is resolved.There is no real “debt.” There is no real burden on the government or on taxpayers. It’s all arbitrary juggling of the books. The government owns the books and all the laws. It can do whatever it wishes.

Congress has never railed to deal with the debt limit by the deadline although in 2011 the standoff between Republicans and the Obama administration was so prolonged that Standard & Poor’s, the credit rating agency, downgraded a portion of the country’s AAA credit rating for the first time in history.Standard & Poors made fools of themselves. At one point several U.S. corporations was given a higher credit rating than the U.S. government. Consider what would have happened to these corporations had the U.S government defaulted. The corporations’ money and their credit rating would have become worthless, or near so. No domestic entity can have better credit than the U.S. government.

Treasury said it expects to borrow $463 billion in the current April-June quarter which will be part of its plans to borrow $2.28 trillion for the full budget year, which ends Sept. 30. The $463 billion represents a significant jump from the government’s initial estimate three months ago that it would need to borrow just $95 billion in the current quarter. The change was attributed to passage of the most recent virus relief bill of $1.9 trillion in March. The government ran up a record $3.1 trillion budget deficit last year, reflecting the COVID relief spending and a drop in revenues caused by the recession. Private economists believe the deficit for the current budget year will be even higher, possibly hitting $3.3 trillion.Those budget deficits are nothing more than the number of dollars the federal government plans to add to GDP.

GDP = Federal Spending + Non-federal Spending + Net Exports

The more the federal government spends, the greater is GDP, the primary measure of the economy. Those who oppose federal spending are knowingly or unknowingly opposing economic growth. Unlike you and me, and unlike your state, county, and city, the federal government does not use revenue. In fact, the federal government destroys all income it receives. To pay its bills, the federal government creates new dollars, ad hoc. Put these facts together:- The only way to cut federal “debt” is to cut federal spending and/or to increase federal taxes.

- By formula, cutting Federal Spending cuts GDP

- Increasing taxes cuts Non-federal Spending, which cuts GDP

- Therefore, the math is absolutely clear: Cutting the federal debt cuts GDP.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

- The federal government is too big

- The Debt/GDP ratio is too high

- Federal spending is “Socialism” (Socialism isn’t federal spending. It’s federal ownership and control over business).

- The deficit or debt should be reduced

- We should have a federal “balanced budget.”

- The federal government is spending beyond its means.

- Federal taxes “pay for” federal spending

- Personal finance or state/local government finance are like federal finance.

- Limits on federal deficit spending are “prudent.”

- We don’t need additional federal spending.

- We can’t afford programs that benefit the middle and lower-income groups (Elimination of FICA, Social Security for All, Medicare for All, Free College for All, Food and Housing supplements).

- The federal government should not “bail out” the state governments.

Looming Budget Catastrophe in Pictures So Simple Even Congress Can Understand Maybe drawings can deter elected officials from their outrageous spending habits where detailed reports have failed to attract their attention.Lord, have mercy. ………………………………………………………………………… Rodger Malcolm Mitchell [ Monetary Sovereignty, Twitter: @rodgermitchell, Search: #monetarysovereignty Facebook: Rodger Malcolm Mitchell ] THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE. The most important problems in economics involve:

- Monetary Sovereignty describes money creation and destruction.

- Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

- Eliminate FICA

- Federally funded Medicare — parts A, B & D, plus long-term care — for everyone

- Social Security for all

- Free education (including post-grad) for everyone

- Salary for attending school

- Eliminate federal taxes on business

- Increase the standard income tax deduction, annually.

- Tax the very rich (the “.1%”) more, with higher progressive tax rates on all forms of income.

- Federal ownership of all banks

- Increase federal spending on the myriad initiatives that benefit America’s 99.9%