President Trump may tell more liesthan anyone, even any politician, in U.S. history. Yet his followers don’t seem to mind.

This phenomenon has the rational people of America puzzled and infuriated. “How can they not see or care what a liar he is?”.

My long-time explanation has been:

Trump hates the same people his followers hate.

Trump hates foreigners, especially non-white foreigners who come from “shithole countries: Mexicans, South and Central Americans, and Muslims, blacks, browns, yellows, reds, gays, and anyone who tells the truth about him.

His followers hate the same people, so though Trump lies about virtually everything, his followers remain loyal, as long as he continues to spew bigoted hatred.

So when Trump said, “I will be proud to shut down the government. I will take the mantle. I will not blame you (Democrats) for it” yesterday, and then today wrote, “Democrats own the shutdown,” Trump’s followers were not troubled.

One may ask, “Are these people stupid?” Perhaps they are, but I suspect there is something in addition to the above-mentioned, stupid bigotry going on:

The initial plan was a Cold War classic — brutal yet simple. Two Russian agents would slip onto the property of a turncoat spy in Britain and daub his front door with a rare military-grade poison designed to produce an agonizing and untraceable death.

But when the attempted assassination of Sergei Skripal was botched, the mission quickly shifted. Within hours, according to British and U.S. officials who closely followed the events, a very different kind of intelligence operation was underway — an elaborate fog machine to make the initial crime disappear.

False narratives and conspiracy theories began popping up almost immediately, the first of 46 bogus storylines put out by Russian-controlled media and Twitter accountsand even by senior Russian officials, all of them sowing doubt about Russia’s involvement in the March 4 assassination attempt.

Ranging from the plausible to the fantastical, the stories blamed a toxic spill, Ukrainian activists, the CIA, British Prime Minister Theresa May, and even Skripal himself.

Variations on the technique existed during the Cold War, when the Soviet Union used propaganda to create alternative realities [What Trump’s mouthpiece, Kellyanne Conway, termed, “alternative facts.”]

But the disinformation campaigns now emanating from Russia are of a different breed, said intelligence officials and analysts.

Engineered for the social media age, they fling up swarms of falsehoods, concocted theories, and red herrings, intended not so much to persuade people as to bewilder them.

And that is the secret to the power of Trump’s constant lying. It is done, not so much to persuade his people, but rather to bewilder them.

(After all these months, who would be persuaded by anything Trump says? Who can even remember what he has said?)

Did he say he would or would not take the blame for the shutdown? Did he admit or deny having an affair with Stormy Daniels and numerous other women? Did he, or did he not, claim the purpose of a Russian meeting was to discuss the adoption of Russian children. Is Michael Cohen a “good man” or “a liar”?

The list of lies and contradictions is endless. Like cockroaches, as soon as one is stomped down, ten more appear.

And this doesn’t even include the other criminals that Trump once claimed were “unbelievable,” until they were found to be actually unbelievable: Shulkin, Porter, Manigault-Newman, Price, Bannon, Scaramucci, Yates, Pruitt, et al — all of whom were great until they weren’t.

Can you even remember all those names?

“The mission seems to be to confuse, to muddy the waters,” said Peter Pomerantsev, a former Russian-television producer and author of Nothing Is True and Everything Is Possible, a memoir that describes the Kremlin’s efforts to manipulate the news.

The ultimate aim, he said, is to foster an environment in which “people begin giving up on the facts.”

Most people, even those intelligent enough to see that Trump is both incompetent and untrustworthy, are confused by his lies.

When pro-Russian separatists shot down Malaysia Airlines Flight 17 over eastern Ukraine, killing 298 passengers and crew members, Russian officials and media outlets sought to pin the blame on the Ukrainian government, suggesting at one point that corpses had been trucked to the crash site to make the death toll appear higher.

In October 2015, months after U.S. and European investigators concluded that Flight 17 had been brought down by a Russian missile fired by separatists, then–presidential candidate Donald Trump told CNN that the culprit was “probably Russia” but suggested that the truth was unknowable.

“To be honest with you, you’ll probably never know for sure,” he said.

The effect of Trump’s constant lies is buttressed by his using the old Hitlerian trick of blaming the opposition for his own faults.

Thus, the crooked owner of the scam operation, Trump University, and the criminal head of the illegal Trump Foundation got away with referring to “Crooked Hillary.”

And the unindicted co-conspirator was able to get his followers to chant, “Lock her up! Lock her up! Lock her up!”

And the draft dodger with phony “bone spurs,” was able to convince his followers that Senator John McCain was “no hero” because he was captured.

And the ultimate liar was able to get away with calling Ted Cruz, “Lyin’ Ted,” perhaps assisted by the fact that Cruz really is a liar.

And the crook with multiple bankruptcies of casinos (who could bankrupt a casono) gets away with “Failing NY Times.”

And the man of infinite lies gets away with “Sneaky Dianne Feinstein.”

Putin brought Russia’s privately owned, freewheeling TV networks to heel in one of his first major moves as president.

The Kremlin now controls all of Russia’s main national television channels.

They deliver a strident, conspiratorial, pro-Kremlin message in hours of lavishly produced talk shows and newsmagazine programs every night.

This is what Trump has said he wants to do: Sue and destroy any “fake media” that tell “fake news” he doesn’t like.

Providing further amplification are social media “troll” factories where hundreds of workers are paid to disseminate false stories on the internet, under official direction.

The U.S. version of “troll factories” is Trump himself, aided and abetted by Fox “News,” Rush Limbaugh, and Breitbart.

Russian politicians and diplomats then chime in, often ridiculing any official investigation and denouncing claims of Russian involvement.

The U.S. version of the above is the GOP, who despite repeated indictments and convictions of Trump’s traitorous associates, continue to parrot the claim that Mueller’s investigation is a witchhunt that should end.

“As for who to believe, who you can’t believe, can you believe at all?” Putin mused, before answering his own questions: “You can’t believe anyone.“

Certainly, not Donald J. Trump.

In short, Trump’s firehose stream of lies is designed to exhaust the listener, so that everything blends into a fog. He relies on false equivalences to confuse among “bad” lies, “white” lies, exaggerations, the truth.

When he is accused of lying, his acolytes mention some other person, usually “Hillary, “Obama,” or “the Democrats,” who may or may not have done something bad, and whatever that may be, excuses everything Trump does.

“Trump separates children from their parents” is equated with the myth of “Benghazi.” “Trump has told more than 3,000 lies this year,” is excused by “Well, Obama lied too.” Every Trump failing is excused, most often by a false reference.

And because he has so many failings, nothing stands out, and everything is excused by his followers, with references to “Hillary, Obama, the Democrats.”

That is the genius of the man: Confusing his followers with volume.

The single most important problems in economics involve the excessive income/wealth/power Gaps between the have-mores and the have-less.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps:

Today, Maya MacGuineas, president of the Committee for a Responsible Federal Budget and head of the Campaign to Fix the Debt, told Congress dozens of lies — O.K., “incorrect non-facts.”.

The primary purpose of these “incorrect non-facts” is to support the myth that somehow our Monetarily Sovereignfederal government will run short of dollars to pay its bills, and therefore, spending (especially social benefit spending) must be cut.

This myth is exactly what the rich want you to believe, so they can reduce your Social Security, cut your Medicare, eliminate poverty prevention and cure, worsen education for your children, and destroy many of the other benefits to the middle-income and the poor.

The motive has to do with Gap Psychology, which we previously have discussed many times, including here,here and here. It is the human desire to distance oneself from those below on any scale, and to near those above

The following represent just a few excerpts from her MacGuineas’s speech.

Testimony of Maya MacGuineas

Committee for a Responsible Federal Budget Hearing before the House Financial Services Committee: The Peril of an Ignored National Debt

I will touch on several points today:

1.The national debt is on an unsustainable path.

2.There are many reasons to care about the debt, ranging from detrimental effects on the economy, to interest payments crowding out the rest of the budget, to the economic, political, and security vulnerabilities of such a large debt.

3.There are many approaches Congress can take to fix the debt, but we must stop denying the problem, stop making it worse, and begin to address it.

The so-called national “debt” actually is the total of everyone’s (yours, mine, China’s) deposits into all our Treasury security accounts.

As these deposit accounts mature, the federal government pays them off by returning to our checking accounts the dollars that are in the accounts.

(The dollars remain in our T-security accounts until maturity. The federal government, being Monetarily Sovereign, neither borrows nor uses these dollars. It creates new dollars every time it pays a creditor).

Thus, paying off the so-called debt is no burden on the federal government or on taxpayers. It simply is a money transfer from one (T-security) of our accounts to another (checking) of our accounts. Tax dollars are not involved.

The federal “debt” (deposits) totaled $40 Billion in 1940. Today, the “debt” is $16 Trillion, a 40,000% increase. Every year since then, pundits have claimed the debt is “unsustainable,” “a ticking time bomb,” and/or in some other way, “detrimental to our economy.” See: “From ticking time bomb to looming collapse.”

But, in that same 1940 – 2018 period, the Gross Domestic Product has grown from $102 Billion to more than $20 Trillion. Yet still, we hear the obviously wrong incessant claim that the federal “debt” (deposits) is unsustainable.

To make matters worse, debt is expected to grow drastically in the coming decades. According to the Congressional Budget Office (CBO), debt under current law will grow from 78% of GDP this year to exceed the size of the economy in just 13 years and reach an unprecedented 152% of GDP in 30 years. Our estimates suggest debt under current law will reach 358% of GDP in 75 years.

The federal “debt” / GDP ratio is meaningless. The “debt” is not paid off with GDP. The two are unrelated. Japan, a wealthy nation, had a debt / GDP ratio of 253% in 2017, yet its debt remains “sustainable.

Putting debt on a sustainable path will require significant deficit reduction.

•Simply holding debt at today’s near-record as a share of GDP (78%) would require savings of $4.8 trillion of spending cuts and/or tax hikes over the next decade.

•Balancing the budget in 2028 would require about $7 trillion in savings over ten years.

•Reducing debt to its historical average of 41% of GDP in 30 years would require $7.6 trillion in deficit reduction over ten years.

•And waiting just ten years increases the size of the adjustments by half.

MacGuineas neglected to tell Congress that every depression in U.S. history was caused by a reduction in U.S. debt:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

And recessions begin with reductions in deficit growth.

Blue line = deficit growth. Vertical gray bars = recessions. Recessions are cured by increases in deficit growth.

The reason for this effect is simple: Deficits add dollars to the economy, and these added dollars are necessary for economic growth.

Macguineas’s article continues:

The risks and consequences of high and rising debt include:

•Slower economic and income growth due to debt crowding out private sector investment. As the government issues more debt, investors buy these bonds in place of private investment. Over time, this results in a smaller stock of buildings, machines, and equipment; fewer new ventures and new technologies; and slower wage growth. CBO estimates average income will be $6,000 ( 6%) lower in 2048 if we allow debt to rise rather than reduce it to historical levels.

Completely false. There is no crowding out. Higher debt results from federal deficit spending which adds investment dollarsto the economy.

That is why massive debt growth has paralleled massive economic growth.

MacGuineas ignores these obvious facts.

•Higher interest rates on loans for households and businesses. Rising federal debt tends to put upward pressure on interest rates throughout the economy. This increase trickles into business and consumer loans, making it more expensive for Americans to take out mortgages, car loans, and credit card debt – not to mention small business loans and other borrowing that helps grow the economy.

Interest rates have remained low in past years despite growing debt due to Federal Reserve accommodation and a slow recovery, but there is a very strong risk those conditions will and have started to change as the economy has gotten stronger, the Federal Reserve tightens monetary policy, and we come closer to full employment.

Federal “debt” does not put pressure on interest rates. The Fed sets rates to combat inflation, not to sell federal “debt.”

Further, federal debt does not cause inflation, which instead is caused by shortages. Historically, they have been shortages of food, but more recently, they have been shortages of oil. See: Federal deficit spending doesn’t cause inflation; oil does.

•Higher government interest payments that displace other government priorities. Due to rising interest rates and an increasing stock of debt, interest payments are projected to be the fastest growing part of the federal budget.

Under current law, interest costs will tripleover the next decade. As a result, interest costs will exceed Medicaid spending by 2020, defense spending by 2023, and total discretionary spending by 2045.

We estimate that before 2050, net interest will be the single largest line item in the budget.

In the above comment about “displacing other government priorities,” MacGuineas makes the tacit and false assumption that the federal government can run short of its own sovereign currency, the U.S. dollar.

Because our Monetarily Sovereign federal government has the infinite ability to create dollars, the notion of “displacing” makes no sense.

Clearly, MacGuineas either does not understand Monetary Sovereignty, or she doesn’t want you to understand Monetary Sovereignty.

•Reduced fiscal space for the government to react to wars, recessions, or other emergencies. It is impossible to predict the timing of the next recession. However, the fact that one has not occurred in the last nine years suggests another may be on the horizon.

Unless there is a dramatic reduction in debt, we will enter the next recession with the highest debt in nearly 70 years (and higher than any time prior to World War II). This leads to legitimate concerns about the available “fiscal space” in the U.S., or the federal government’s financial capacity and willingness to respond to emergencies.

While it is impossible to know the precise amount available, the U.S. almost certainly has less fiscal space today than it did a decade ago, and it is projected to have even less in the coming years. The U.S. is less equipped to handle the next recession than it was in handling the Great Recession.

The “precise amount available” is infinite. That is why it’s impossible to know.

The “fiscal space” argument is identical with the “displace other priorities” argument. Again, MacGuineas wants you to believe the federal government can run short of its own sovereign currency.

While you and I, and the cities and states, and even the euro nations can run short of money, the U.S federal government cannot unintentionally run short of dollars.

•Lost opportunities to make thoughtful investments or reforms. Rising debt hinders our abilityto enact good public policy. Whether you care about strengthening the military, developing clean energy, reducing burdensome taxes, or investing in education and infrastructure, rising debt will crowd it out.

Thanks to the increasing debt burden, next year the country will spend more on interest than on children, which means we will be spending more on financing our past than investing in our future.

And there are many new issues on the horizon, from the effects of technology to the future of work to new types of global threats that we are only just developing the capacity to withstand. As time goes on, we will increasingly lose the capability to address our debt situation through thoughtful, gradual, and targeted tax and spending reforms. At some point in the near future, our debt will be so high we will have to forgo new ideas and impose blunt spending cuts and tax hikes.

“Hinders our ability” is another statement of “crowding out,” and “reducing fiscal space.” MacGuineas keeps repeating the same false premise, just using different words

•Risk of an eventual fiscal crisis if changes are not made. The combination of our strong economy, steady monetary policy, and longstanding commitment to pay our debts has allowed us to amass significant debt without severe consequences. This will not last forever. Unsustainable debt may eventually lead some investors to demand higher interest rates, which could set off a chain of events that begins with a small selloff of existing federal bonds and ends with a global financial crisis.

No one knows what level of debt or combination of events would set off such a crisis ; I hope we will never have to find out.

The Fed, not investors, sets interest rates. Unlike with private bonds, demand is not an issue for federal bonds. If no one wished to buy federal bonds, the Federal Reserve could buy them, which is often has. (This is known as “Quantitative Easing.”)

In any event, the Treasury does not need to sell bonds to obtain dollars. It has an infinite supply of dollars.

Instead, the two most important reasons why the Treasury issues T-securities are:

To provide a safe place to “park” unused dollars. This safety helps stabilize the dollar.

To assist the Fed in controlling interest rates, which helps fight inflation.

Thus, the reasons for issuing of federal debt (aka “borrowing”) are quite unlike the reasons why you and I borrow.

Our Monetarily Sovereign federal government could stop issuing debt today — even stop collecting taxes today — and still retain the unlimited ability to pay for goods and services, forever.

Those unconcerned about our rising debt have sometimes pointed to the built- up debt in recent years as evidence that the United States can borrow with little consequence. That’s a mistake.

China owns $1.1 trillion of U.S. debt. Trade and other tensions with them can certainly affect their lending decisions. Moreover, given our unstable political relationship with China, it is less than ideal to be as dependent on them as we are for funds.

Japan, which holds another $1 trillion of our debt, has also halted net purchases – possibly due to its aging population.

As the population continues to age, this nation of savers is likely to draw down its savings to finance retirement and therefore have fewer assets available to purchase U.S. debt.

Currently, foreign investors and governments own about 40% of the publicly traded debt, a percentage that has decreased in recent years as China and Japan have pulled back and forced domestic investors to finance our debt instead.

As we’ve said, the federal government does not need to sell debt to anyone — not to China, not to Japan, not to you or me, not to anyone.

Further, “domestic investors” are not forced to do anything. I know of no “forcing” device the federal government uses to sell T-bonds. It’s all nonsense.

And now we come to the real reason why MacGuineas spreads the Big Lie that the federal government is running short of dollars:

The primary drivers of long-term debt are growing mandatory spending and the lack of revenue to pay for it. Over the next ten years, 82% of spending growth will be due to Social Security, health programs, and interest payments.

Mandatory spending, specifically the costs stemming from an aging population, remains the largest long-term problem to address. Congress should have offset the increased discretionary funding with mandatory cuts and revenues that led to growing deficit reduction over time.

The fastest growing parts of the budget are Social Security, health programs like Medicare and Medicaid, and interest payments on the debt – each of which does not go through the annual appropriations process and is growing faster than the economy.

Mandatory spending and interest have already grown from 61% of the budget in 2010 to 69% today, and they are projected to be at 77% in 2028.

Get it? Her pay comes from the wealthy. So, on behalf of the wealthy, she wants the government to cut Social Security, Medicare, and Medicaid, programs that are vital for the middle classes and the poor, but mean little to the rich.

In short, the rich want to widen the Gap between the rich and the rest, and MacGuineas acts as their mouthpiece.

One of the many reasons this concerns me is the extent to which it has squeezed productive investments.

The best first step our leaders could make is to pledge to not make the debt situation worse(unless there is a smart reason to borrow such as a recession).

“Squeezed productive investments” is yet another synonym for “hinders our ability,” “crowding out,” and “reducing fiscal space.” It’s completely phony when referring to a Monetarily Sovereign government.

And notice she acknowledges that deficit spending is good during a recession (because deficit spending grows the economy), but she doesn’t want to grow the economy unless we have a recession. That’s totally illogical.

Lawmakers should focus on making changes to two of the largest drivers of our long-term debt problem: health care spending and Social Security. Reforms in these areas have the most potential for significant savings, and it would be between difficult and impossible to control our debt problem without making changes to these programs.

The largest driver of future costs is health care. The other major area needing attention is Social Security. The program’s trust fund is on track to exhaust its reserves by 2034, at which point benefits will be cut by 20% to 25% without legislative action to stop it.

Starting this year, the Social Security trust fund is being drawn down to pay benefits, meaning that the government must borrow from elsewhere so that Social Security can redeem its trust fund reserves.

In other words, Social Security is increasing the current deficit and will continue to do so dramatically in the future if the program is not reformed.

We can fix this program by adjusting benefits, raising revenues, or both.

The Supplemental Medical Insurance fund, which pays for Medicare Part B and Part D benefits, is funded by Congress. It doesn’t rely on a “trust fund.” Congress directly authorizes what funds are needed.

So, while Medicare and Social Security supposedly are paid through trust funds, in reality, half of Medicare doesn’t even pretend to go through a “trust fund.”

Second, “raising revenues: means increasing FICA, which is deducted from salaries. The rich, who do not receive most of their income via salaries, don’t care about FICA, and in any event, the salary from which FICA is deducted is a comparatively piddling $100K.

This all demonstrates that the federal government has the unlimited ability to fund Social Security and Medicare forever, with no trust funds and not even a FICA tax.

In Summary:

The rich, who run America, want to widen the Gap between them and the rest of the populace.

It is the Gap that makes them rich. Without the Gap, we all would be the same, and the wider the Gap, the richer they are.

The rich don’t want you to understand that:

1. A growing economy requires a growing supply of money

2. Deficits increase the supply of money

3. Therefore, deficits grow the economy

4. The federal government, being Monetarily Sovereign, never can run short of dollars with which to pay its creditors

They just don’t want you to know it.

They want you to believe the government can’t afford to pay for benefits like Medicare for All, free college for all, and anti-poverty initiatives.

They certainly don’t want you to ask for the Ten Steps to Prosperity (below).

The single most important problems in economics involve the excessive income/wealth/power Gaps between the have-mores and the have-less.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps:

*Between March 23 and July 16, the U.S. collected $1.4 billion from levies on foreign imports of steel and aluminum.

*That figure could reach $7.5 billion this year, based on last year’s import levels.

*Tariff revenue is impacted by Commerce Department exclusions and President Trump’s change of heart.

In less than five months, the Trump administration has collected more than $1.4 billion in new revenue from steel and aluminum tariffs, according to a recent report prepared for members of Congress.

The Congressional Research Service estimated that, between March 23 and July 16, the U.S. reaped $1.1 billion and $344.2 million from levies on foreign steel and aluminum, respectively.

Those earnings are on the rise as trade negotiations with allies linger on and President Donald Trump moves to hike tariff rates on countries like Turkey.

CRS says the new tariffs could reap the U.S. some $7.5 billion — $5.8 billion on steel and $1.7 billion on aluminum– based on last year’s import levels.

Whom do you think will pay that $7.5 billion? Not Turkey. Not Canada. Not China. Not any foreign nation.

The answer: You, the American consumer, will see $7.5 billion taken out of your pockets, and transferred to the U.S. government, where all $7.5 billion will be destroyed.

That’s right, destroyed. As soon as those dollars hit the Treasury, they no longer will exist as part of any money-measure. The government doesn’t need or use those dollars.

To pay creditors, the government creates brand new dollars, ad hoc. Paying creditors is the only method by which the government creates U.S. dollars.

Those federal tariffs constitute a $7.5 billion tax on the American economy, a net loss for the private sector and a net gain for no one.

Just as a tax cut is stimulative, a tariff not only is recessive, but it also is inflationary, as it increases prices.

Trump has suggested the tariffs – originally unveiled as a national security provision – could have the added benefit of reducing the federal deficit, which rose to $77 billion in July, wider than the July 2017 budget deficit of $43 billion.

And the Treasury’s borrowing to fund government operations is set to top $1 trillion this year for the first time ever.

There are only two ways to reduce the deficit: Increase federal taxes and/or cut federal spending. Both are recessionary. They reduce the number of growth dollars coming into the economy.

A growing economy requires a growing supply of money. Reducing the deficit is the worst possible act if one wishes the economy to grow.

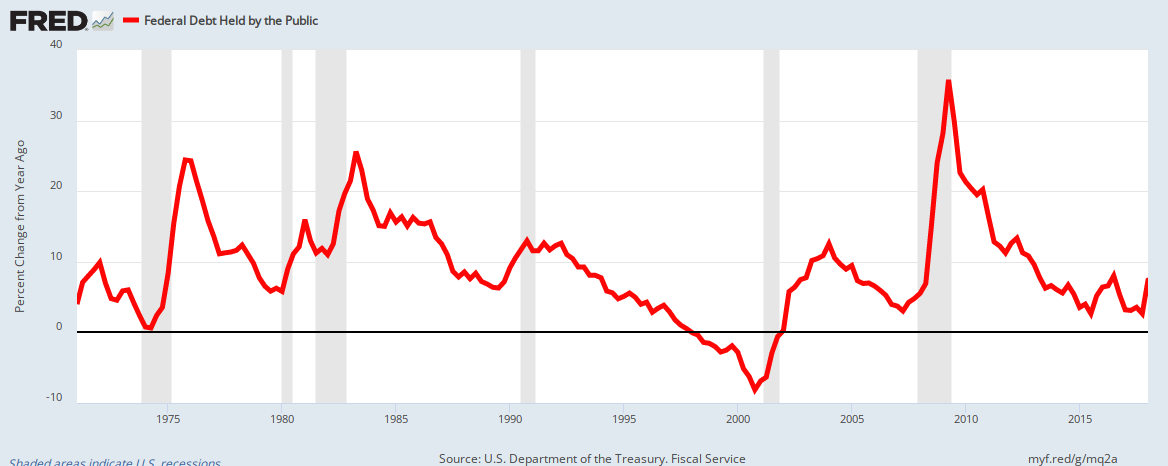

Red line shows changes in federal debt. Reductions in debt growth lead to recessions (vertical gray bars) by taking dollars from the economy. Increases in federal debt growth cure recessions by adding dollars to the economy.

Because of Tariffs we will be able to start paying down large amounts of the $21 Trillion in debt that has been accumulated,” Trump tweeted on Aug. 5. “At minimum, we will make much better Trade Deals for our country!”

As usual with Trump pronouncements, this is false. Tariffs do not in any way help pay down the federal debt.

The debt is paid down by returning the dollars that already exist in Treasury security accounts. No taxes are used for this.

And in any event, paying down debt causes depressions.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

In short, while tariffs may protect a relatively few jobs in a chosen industry, they cost jobs overall by being recessive and inflationary.

Taking $7.5 billion from the economy in an attempt to save jobs is moronic.

Rather than destroying $7.5 billion, the government could, if it wished, support those chosen industries by:

Reducing their taxes

And/or buying from them

And/or giving them money

Though we have come to expect moronic ideas from Trump, we also receive the same moronic ideas from “respected” sources. For instance:

President Trump’s economic choices over the last two years have been terrible. When he wasn’t busy shoveling vast piles of cash into the suppurating maw of the top 1 percent, he busied himself starting a flailing trade war with China and Europe.

So far, so good, but why is that trade war failing? Because all trade wars fail.

However, there have been some accidental side benefits. The tax cuts provided a bit of badly needed fiscal stimulus that jolted the economy half-awake (despite being otherwise monstrous policy).

Right. The tax cuts are stimulative, because they add dollars to the economy. Unfortunately, the primary benefits of Trump’s tax cuts went to Trump and his rich pals.

And, as an Economic Policy Institute report details, his tariffs on aluminum have restored some employment and production in that sector.

Whereas nearly the entire American aluminum industry had vanished between 2010 and 2017, after tariffs went up in March of this year, production is up 67 percent, three smelters have been reopened, and one has been expanded, resulting in 1,000 new jobs and $100 million in new investment.

Taking billions from the economy does not create “new” jobs. It shuffles jobs from one industry to another, while costing the economy money and inflating the price of all things made with aluminum.

Not that tariffs are always and everywhere good, but they can be an important tool for managing trade and the economy.

Tariffs are taxes. Taxes are not a tool for managing the economy; they are a tool for shrinking the economy.

Sure, some tariffs have been pretty lousy or misguided. For instance, the Smoot-Hawley tariffs of 1930 at a minimum utterly failed to cure the Great Depression — and quite possibly enabled a protectionist race to the bottom that ultimately worsened the situation.

Tariffs, being taxes, cannot cure anything. As you have seen from the above data, recessions are caused by reduced money growth, and are cured by increased money growth. Taxes (tariffs) take dollars from the economy.

But, free trade (especially of capital) under a fiat currency regime can fuel devastating financial crises just as it did in the 1920s.

The depression of 1929 was caused by ten years of federal surpluses (taxes exceeding spending).

What the world and America need is a global trade regime that allows poorer nations to get started on the development ladder, but without creating (politically disastrous) severe trade imbalances, or requiring the United States to run a gigantic trade deficit until the end of time so nations can settle their international accounts.

Utter nonsense. “Trade imbalances” (i.e. more money leaving a country than entering it) are no problem for a Monetarily Sovereign government. Such a government creates its own sovereign currency at will, and at no cost.

The U.S. consistently runs trade deficits, which actually are beneficial. Trade deficits allow the federal government to obtain valuable goods and services in exchange for dollars they produce at the touch of a computer key.

Past Federal Reserve Chairman Ben Bernanke: “The U.S. government has a technology that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

A world trade system like Bretton Woods (but better) would be best — but tariffs can absolutely be part of such an effort in the meantime.

Bretton Woods was the last of a series of gold standards which inevitably fail because they tie money creation to the availability of a physical chemical. Nations that are short of gold cannot grow, just as nations that are short of money cannot grow.

For the author, Mr. Cooper, to mention Bretton Woods favorably, demonstrates an abject ignorance of economics.

Trump’s tariffs show they do pretty much exactly what they say on the tin: change the price structure to make domestic production more feasible.

No, tariffs cost both people and nations money, and have zero positive value.

It’s long since time China (and Germany, for that matter) rebalanced its economy to be less export dependent.

Cooper does not even understand that Germany is monetarily non-sovereign. It cannot create its own sovereign currency at will, as it does not have a sovereign currency. So Germany, and all euro nations, must be net exporters (i.e import money) to survive.

The U.S., by contrast, does not need exports in order to import money. It can create its money at will.

As John Maynard Keynes suggested, a trade system favoring neither surpluses nor deficits is a much more sensible way to structure the global economy.

“A trade system favoring neither surpluses nor deficits” would be a zero growth trade system.

Bottom line: A Monetarily Sovereign nation should not levy tariffs, ever. It can encourage any of its industries and their jobs, if it wishes, simply by supporting those industries financially.

A tariff is a tax. Just as a tax cut is stimulative, a tariff not only is recessive because it takes dollars from the private sector, but it also is inflationary because it increases prices.

The single most important problems in economics involve the excessive income/wealth/power Gaps between the have-mores and the have-less.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps:

Quora is a site where people ask questions, and other people answer them. Many people ask about the U.S. federal “debt,” and I’ve tried to illuminate the world, one candle at a time.

Here, for example, is a typical question and answer, with a follow up by one reader. The original question and answer were:

Answer from Rodger Malcolm Mitchell: Contrary to what others are telling you, there is no “debt crisis.”

The federal government, unlike you and me, is Monetarily Sovereign. And unlike you and me, it never can run short of dollars with which to pay its debt. In fact, paying debts is the method by which the federal government creates new dollar.

In fact, the so-called “federal debt” isn’t even debt. It is the total of deposits into Treasury Security accounts, similar to savings accounts.

To “lend” to the federal government, you instruct your bank to send your dollars to your Treasury Security account.

There your dollars remain – they are not used by the federal government. Then when your account matures, your dollars, plus interest are returned to you.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.” Ben Bernanke: “The U.S. government has a technology that allows it to produce as many U.S. dollars as it wishes at essentially no cost.” St. Louis Federal Reserve: “The government is not dependent on credit markets to remain operational.”

It is not a burden on our Monetarily Sovereign government, nor is it a burden on federal taxpayers.

Federal taxing does not fund federal “debt.”

People who worry about the federal debt do not understand Monetary Sovereignty.

The so-called “debt” has increased an astounding 40,000% since 1940, and here we are, with the economy healthy and growing, and inflation near the Federal Reserve target.

Chamchadik

You’re right- being fiat, the us federal reserve can just print as much currency as it wants and settle all debt: I would like to hear your reasoning on why they haven’t done this already?

————————–Reply——————————————-

Rodger Malcolm Mitchell

The so-called federal “debt” is merely the total of outstanding Treasury securities (T-bills, T-notes, T-bonds). It isn’t “debt.” It is “deposits.”

The government does not issue T-securities to obtain dollars. It creates all the dollars it needs.

Issuing T-securities has two primary purposes:

1. To provide a safe, interest-paying, storage place for holders of dollars. This helps stabilize the dollar.

2. To assist the Fed in controlling interest rates. This helps control inflation.

Yes, the government could eliminate all federal “debt” tomorrow, if it wished, simply by returning the dollars in the T-security accounts, back to the owners.

But, there is no reason why the government would want to reduce the “debt.” These T-securities serve valuable functions, and the “debt” is no burden whatsoever on the government, on taxpayers or on anyone else.

The word “debt” confuses people. If instead, it was properly called “deposits,” no one would want it reduced.

Perhaps, the next time someone tells you the federal “debt” should be reduced, you might answer, “Why would the government want fewer deposits into Treasury security accounts? These deposit accounts are valuable to the government and are no burden on anyone.”

The single most important problems in economics involve the excessive income/wealth/power Gaps between the have-mores and the have-less.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps: