The downgrades had nothing to do with the federal government’s ability to pay. They reflected the government’s willingness to pay, as evidenced by the ridiculous debt ceiling laws. Being Monetarily Sovereign, the federal government has the infinite ability to pay for anything. Mr. Poole confuses “ability”with “willingness.” We have written many times about the so-called fiscal “time bomb.” The first mention we noted was in 1940;Endlessly expanded federal borrowing and spending is not a realistic long-term transportation future

By Robert Poole, Director of Transportation Policy, September 12, 2023

(Robert Poole is one of the founders of the Reason Foundation [which publishes Reason Magazine] and served as its president and CEO from 1978 to 2000.He is currently director of transportation policy at the Reason Foundation and frequently writes about issues related to privatization.)

The national debt will affect the future of transportation funding, and the public-private partnership community needs to understand why and what the implications for P3s may be.

The most recent parts of the story began on Aug. 1, when Fitch Ratings downgraded the federal government’s bond rating from AAA to AA+. For a company, that might not be a big deal, but for the government of the world’s largest economy, the downgrade was a shot across the bow.

This was the second time a rating agency took such an action with the federal government’s bond rating, with S&P doing so in 2011.

Headlines in the financial press, such as The Wall Street Journal’s “America’s Fiscal Time Bomb Ticks Louder” and “U.S. Downgrade Flashes Warning Sign.” indicate how seriously the downgrade should be taken.

September 1940, the federal budget was a “ticking time-bomb which can eventually destroy the American system,” said Robert M. Hanes, president of the American Bankers Association.

Subsequently, references to the federal “debt” as a ticking time bomb appeared regularly in all media, from scholarly journals to daily newspapers. The 1940 mention came when the total federal “debt” was approximately $48 Billion. Today, that debt is roughly $26 Trillion, an astounding 54,000% increase.

Despite that increase, the “ticking time bomb” still has yet to explode, but the doomsday preachers, having learned nothing from the many years of experience, continue to fret. Eighty-three consecutive years of wrong predictions, and people still believe? What word comes to mind?No, the reason for the downgrade was the uncertainty caused by the useless debt limit laws. The word “useless” is appropriate. There is no use for a law that limits the federal government’s ability to pay for what it already has purchased. And should anyone believe the law has any purpose whatsoever, they should explain why, since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt limit – 49 times under Republican presidents and 29 times under Democratic presidents. If the law had any value, why is it so easily and often increased without exploding as a “time bomb”? Money is power, so ironically, if one truly believed the power belongs with the people and not with the government, he would favor money flowing to the people and from the government. Yet the exact opposite is stated by the Libertarian writer.As the Journal’s Greg Ip wrote: One reason for Fitch’s downgrade was the absence of any political will to deal with the main drivers of the deficit: spending programs for older Americans, including Social Security and Medicare, and repeated cuts to tax rates for most households.

Mr. Poole doesn’t give examples of those “triple-A” and “double-A” rated countries, probably because they aren’t comparable to the U.S. government. Perhaps, they don’t have a foolish, useless debt-ceiling law. Or perhaps, they are not Monetarily Sovereign nations that can issue their national currency in unlimited amounts, as the U.S. can. It would have been helpful for Mr. Poole to list the nations he refers to, but of course, he never will because that would destroy his argument.Fitch noted how much worse U.S. fiscal metrics are than its peer countries. For example, The U.S. is on track to spend 10% of federal revenue on interest by 2025, compared with just 1% for the average triple-A-rated country and 4.8% for double-A-rated.

Why, then, isn’t the U.S. rating even lower?

First, the U.S. government does not borrow U.S. dollars. It pays for goods and services by creating dollars ad hoc, which it has the unlimited ability to do. The U.S. government never unintentionally can run short of dollars.Because the reserve status of the dollar and the size and safety of Treasury debt gives the U.S. unprecedented borrowing ability.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

“Not dependent on credit markets” means they don’t borrow dollars. Second, “reserve status” merely means that banks keep dollars on reserve to facilitate international trade. Not only does the U.S. dollar have reserve status, but so do numerous other currencies, depending on geography. Though the U.S. dollar is the most common reserve currency, other reserve currencies include: the euro, the Japanese yen, the Mexican peso, the British pound, the Canadian dollar, the Australian dollar, the Indian rupee, the Swiss franc, the Swedish krona, and many other currencies now being held in reserve by banks, worldwide. Being a reserve currency does not bestow special safety on a currency. It does not indicate a nation’s ability to pay its bills. Third, Mr. Poole mentions the size and safety of Treasury debt in the same article about its being a “ticking time bomb.” I suggest he has just exploded his own warning, as well as he should.Interest rates have no meaning for a Monetarily Sovereign nation like the U.S., which has the infinite ability to create its own currency. Whether interest is 1% or 50%, or anything between, the U.S. federal government simply presses computer keys to pay. Further, the U.S. Federal Reserve pays whatever interest rate it wishes. It sets the rate by fiat. Unlike private borrowers, the Fed does not need to set a rate that is attractive to lenders because:Indeed, it was hard to get presidents or Congress to worry about the deficit when interest rates were low. Today, a bond market signaling that the world is no longer safe for debts may be the first step to tackling them.

a. The government does not borrow. The purpose of T-bills, T-notes, and T-bonds is not to provide the government with spending money. The goal is to provide a safe storage place for unused dollars. The federal government never touches the dollars in T-security accounts.

b. If the Treasury wanted to issue T-securities that no one wanted to buy, the Federal Reserve could purchase them.

The debt/GDP ratio is the most misunderstood fraction in all economics. Contrary to widespread ignorance, that ratio has absolutely nothing to do with the ability of the U.S. to pay its bills. The federal government has the infinite ability to create dollars, which it does by pressing computer keys.The long-term consequences of the growing debt were estimated in the latest Congressional Budget Office’s (CBO) 2023 Long-Term Budget Outlook.

Its baseline 30-year projection, which assumes no changes in existing laws and programs, is that by 2053, the national debt will constitute 181% of the U.S. Gross Domestic Product—compared with 98% today.

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

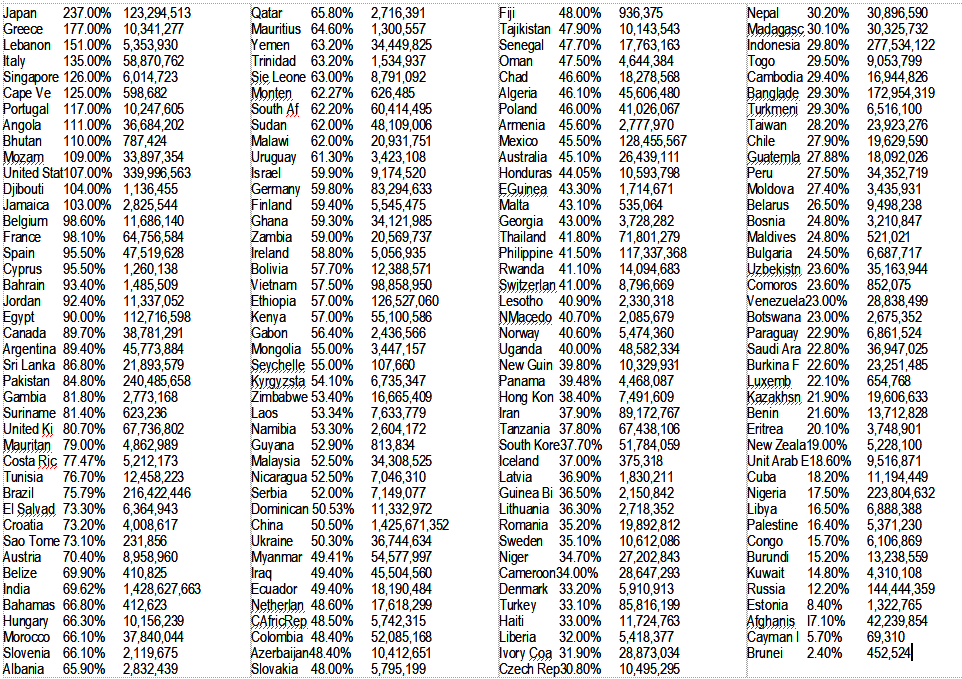

The so-called “debt” is the total of T-security deposits accepted by the federal government. These are dollars in accounts owned by depositors, never touched by the federal government, and paid off simply by returning the dollars in the accounts. The misnamed “debt” consists of net deposits made between yesterday and ten or more years ago. By contrast, GDP (Gross Domestic Product) is a one-year spending measure. So, the debt/GDP fraction compares a multi-year total with a one-year total — mathematically senseless. Imagine your house mortgage being $300,000 and you earning $150,000 a year. That would be a 200% ratio that millions of people support all the time. The debt/GDP is even more senseless than that, because GDP doesn’t pay debt. Of course, you aren’t Monetarily Sovereign — you can’t create dollars at will — and the federal debt isn’t real debt. So, the whole thing is foolish, though no more foolish than current worries about Debt/GDP ratios. If you want to waste time evaluating the world’s most useless ratio, go here. It shows the percentages for dozens of countries. I challenge you to use those ratios to determine the world’s best and worst credit risks.Given that the federal government has the infinite ability to create dollars, why does Mr. Poole stress about paying interest? Ignorance or intent to deceive?And paying interest on that debt will increase from taking 15% of federal revenue today to 35% of federal revenue in 2053 (more than any national budget item except Social Security and Medicare). And that’s just CBO’s baseline estimate.

Whether the debt is 22%, 222%, or 2222% of GDP has zero effect on the federal government’s ability to pay its bills.The Committee for a Responsible Federal Budget estimates that, given likely extensions of tax cuts and expansions of federal programs, the 2053 national debt will likely rise to 222% of GDP.

Here is where we get to Congress’s misunderstanding (intentional or otherwise) of the federal government’s ability to pay for things.Where does transportation fit in the discussion about the national debt?

Well, in July, the House Appropriations Committee, in response to conservative members saying they’re concerned about out-of-control federal borrowing while a Democrat is in the White House—as opposed to mainly supporting massive deficit spending during the Trump administration—proposed trimming Fiscal Year 2024 Department of Transportation (DOT) discretionary grant spending by $5 billion.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Even if the federal government collected zero taxes, it could continue spending forever. There is no reason to cut spending for budgetary reasons. The government has infinite money.Suppose we make the possibly innocent assumption that the Department of Transportation (DOT) had good reasons for its discretionary grant spending. In that case, we now will be forced to do without that spending. The people will be deprived of important transportation improvements, all because of economic ignorance.This relatively minor cut would affect only a few programs in six modal agency discretionary grant programs totaling $22.5 billion last year. Yet a headline in Eno Transportation Weekly read, “FY24 House Funding Bill Has Massive Cuts to DOT Grant Programs.”

This proposal raised similar cries of alarm from highway, transit, and rail organizations, such as the headline “Transportation Funding Under Threat in House of Representatives” by United for Infrastructure, which advocates for more infrastructure investment.

This is an important point. Though the federal government, being Monetarily Sovereign, can create infinite dollars, the states, counties, and cities are monetarily non-sovereign. They can and often do run short of dollars.Let’s think ahead a few years to when massive federal funding in the Infrastructure Investment and Jobs Act, often referred to as the bipartisan infrastructure law, and the Inflation Reduction Act’s budget has been expended.

At that point, state transportation budgets would be expected to revert to their pre-stimulus spending levels.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Why then are states asked to fund what the federal government could easily fund without collecting a penny in taxes? Economic ignorance.Reminder: The federal government does not borrow. It creates dollars at will.But what can we expect transportation organizations and state DOTs to call for?

Based on history, it’s almost certain states will propose the most recent year of those expanded funding levels as their new budget baselines and ask Congress for federal funding.

And if Congress goes along with the calls for that level of infrastructure spending, there will be another massive amount of federal borrowing.

Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes: Scott Pelley: Is that tax money that the Fed is spending? Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Someone, please tell Herb Stein that because the U.S. federal government is Monetarily Sovereign, it can continue to deficit spend forever. It never needs to stop.Since CBO’s dire debt forecasts don’t include this level of increased federal transportation spending, this increase would make all CBO’s 30-year projections seriously underestimating.

Many years ago, a chairman of the Council of Economic Advisers, Herb Stein, propounded what became known as Stein’s Law. “If something cannot go on forever, it will stop.”

But the longer that rude awakening takes to happen, the worse the consequences will be.

Sorry, Mr. Poole, but federal spending has proved to be infinitely sustainable. There is no reason for it ever to stop.America’s transportation leaders should think hard about lobbying for this unsustainable spending to continue.

Because the U.S. government is Monetarily Sovereign, it cannot go bankrupt. For the same reason, no federal government agencies- i.e., Medicare and Social Security- can go bankrupt unless Congress and the President want them to. The federal government could and should eliminate the FICA tax and fund Medicare and Social Security the same way it funds Congress and the White House: By creating dollars. Federal spending is not “out-of-control.” Congress and the President control it. It is exactly what Congress and the President want it to be.The largest contribution to the out-of-control national debt is the impending bankruptcy of Medicare and Social Security.

Does “severe, long-term spending cuts” in transportation sound like “human flourishing,” the Libertarian excuse for the existence of Libertarianism?If, or when, Congress finally gets around to grappling with the costs of those programs, it’s likely that most or all federal discretionary programs, including infrastructure programs, will be in for severe and long-term spending cuts.

Transportation leaders should start planning for that significant change now.

Unnecessary taxes. All federal tax dollars are destroyed upon receipt by the Treasury. Taxes are paid with dollars from the M1 money supply measure. When they reach the Treasury, they cease to be part of any money supply measure. Thus, federal taxes effectively are destroyed upon receipt.One ray of hope for the highway and bridge sector is the opportunity that comes with the urgent need to phase out per-gallon fuel taxes and replace them with per-mile road user charges, also called mileage-based user fees.

This is the usual Libertarian “soak the private sector” (as opposed to “human flourishing,”), though the federal government has infinite money. Ironically, while Libertarians supposedly favor the private sector, they ask the private sector to give the federal government more money. Do these folks even know what they want?If done right, that transition could fully restore the users-pay/users-benefit principles on which the gas tax was based a hundred years ago.

It could even mean converting state highway systems into revenue-financed highway utilities analogous to electric, gas, and water utilities.

Public utilities, which can be government-owned or investor-owned, charge customers based on how much of the service they use. They also issue long-term revenue bonds backed by the projected income from their user charges to fund the costs of maintaining and improving the infrastructure.

It would be even more equitable for the federal government to stop pretending it spends tax dollars. The purpose of federal taxes is not to provide spending dollars to a government that has infinite dollars. The fundamental purposes of federal tax dollars are:Long-time traffic and revenue consultant Ed Regan has suggested that metro areas could add a transit tax to charges in the road user charge (RUC) future.

This would mean only residents of an urban area would pay for its transit subsidies—not rural taxpayers or federal taxpayers in general.

This isn’t ideal, but it would be more equitable than today’s system of diverting nationwide highway user tax revenue to transit in a few hundred metro areas.

- Primarily, to control the economy by taxing what the government wishes to discourage and giving tax breaks to what the government hopes to encourage.

- Secondarily, to create demand for the U.S. dollar by requiring taxes to be paid in dollars.

- In reality, to widen the income/wealth/power Gap between the rich and the rest by claiming that benefits to the poor and middle are “unaffordable” and “unsustainable.”

That is a lie. Federal taxes do not fund federal spending. Period.In the near term, as advocates of more spending point out, thousands of bridges still need refurbishment or replacement across the country.

But there is no way that federal taxpayers, via expanded federal spending, can address that total problem without massive tax increases.

Rather than taking from the private sector, the federal government should fund infrastructure the same way it funds everything else: By simply creating dollars.State and local transportation officials should start planning for a self-help transportation future that requires users to pay for the infrastructure they use and utilizes public-private partnerships to fund and operate significant projects.

SUMMARY Unlike state and local governments, the U.S. federal government is Monetarily Sovereign. Two hundred and sixty years ago, the government created laws from thin air, and some of those laws created dollars from thin air. They created as many laws and dollars as they wished and gave those dollars the value they wished. It all was arbitrary. Today, the federal government retains the infinite right to create as many dollars as it wishes and to give those dollars whatever value it wishes. Thus the U.S. government never can run short of dollars and has absolute control over inflation. It can pay for anything instantly without collecting a penny in taxes. Unlike state/local taxes, federal taxes are destroyed upon receipt by the Treasury. Similarly, no federal government agency runs short of dollars unless Congress and the President want them to. This includes such federal agencies as the Supreme Court, the White House, Congress, all the branches of the military, Social Security, Medicare, Medicaid, and every federal Department. Libertarians claim to believe the federal government has too much power. Yet, to cure federal deficits, they want to cut benefits and increase taxes. Libertarians want to take dollars from the private sector and give them to the federal government — exactly the opposite of the Libertarian stated philosophy. They claim to wish for “human flourishing” and for “freedom,” but it is a freedom to be impoverished and without medical care and transportation, ultimately ending in anarchy. Libertarianism is a fraud that claims to want something noble, but in practice opts for something evil. Rodger Malcolm Mitchell Monetary Sovereignty Twitter: @rodgermitchell Search #monetarysovereignty Facebook: Rodger Malcolm MitchellA version of this column first appeared in Public Works Financing.

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

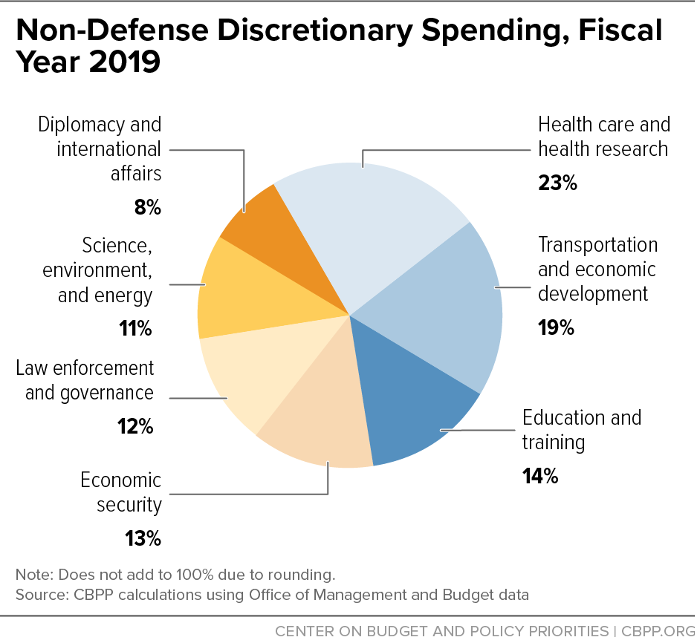

In 2019, non-defense discretionary (NDD) spending totaled $661 billion, or 14 percent of federal spending. That same year, the federal “debt” was $23 Trillion. The entire NND was less than 3% of the so-called “debt.”

Would you be willing to see every dollar cut from health care and health research, diplomacy, science, environment, energy, transportation, economic development, law enforcement and governance, education and training, and economic security?

Oh, but that’s not all.

In 2019, non-defense discretionary (NDD) spending totaled $661 billion, or 14 percent of federal spending. That same year, the federal “debt” was $23 Trillion. The entire NND was less than 3% of the so-called “debt.”

Would you be willing to see every dollar cut from health care and health research, diplomacy, science, environment, energy, transportation, economic development, law enforcement and governance, education and training, and economic security?

Oh, but that’s not all.