Affordable housing laws are not a solution. They are not even a partial solution. They are, at best, tokenism. They are a symptom.

Some people want the federal government to treat symptoms rather than problems. So:

Local governments try to reduce street crime by hiring more police

Some economists want the government to reduce unemployment by creating make-work, WPA-style jobs

Some politicians try to increase affordable housing by passing Affordable Housing laws.

But street crime, unemployment, and lack of affordable housing are symptoms of a more fundamental problem. It is a problem that easily is cured, not with complex, convoluted laws and more government agencies.

The problem is: Lack of money.

We have discussed why street crime is merely a symptom of poverty. Areas with low, or non-existent poverty rates also have low or non-existent incidents of street crime. We have discussed why unemployment is not in itself a problem., Rather, unemployment is the face of a more fundamental problem: Lack of money.

Similarly, lack of affordable housing is a symptom of lack of money. (Those who have money never lack for affordable housing.)

On August 10, 1965, President Lyndon B. Johnson signed the Housing and Urban Development Act. The Act expanded funding for existing federal housing programs, provided rent subsidies for the elderly and disabled, assisted in the construction of more low-income housing, and provided funds for public works projects.

Four weeks later on September 9, 1965, President Johnson would go on to sign legislation that would establish the U.S. Department of Housing and Urban Development (HUD), a cabinet-level agency, to oversee the newly funded housing programs.

“Improving quality of life.” Public housing projects: Crime, drugs, gangs, misery.

President Johnson thought he was solving a problem — unaffordable housing — but since that wasn’t the real problem, his “solutions” accomplished very little, for very few, and had strong, negative implications.

Although Johnson didn’t create the first public housing projects, that basic philosophy has led to drugs, crime, gangs, and misery.

In essence, Johnson had prescribed aspirin for a brain tumor.

Public housingis a form of housing tenure in which the property is usually owned by a government authority, either central or local.

Social housing is any rental housing that may be owned and managed by the state, by non-profit organizations, or by a combination of the two, usually with the aim of providing affordable housing. Social housing is generally rationed through some form of means-testing or through administrative measures of housing need.

One can regard social housing as a potential remedy for housing inequality.

That is the common, though false, belief, that public or social housing is a potential remedy for housing inequality.

Here is the brief mission statement of the federal Department of Housing and Urban Development:

“HUD’s mission is to create strong, sustainable, inclusive communities and quality affordable homes for all.

“HUD is working to strengthen the housing market to bolster the economy and protect consumers; meet the need for quality affordable rental homes; utilize housing as a platform for improving quality of life; build inclusive and sustainable communities free from discrimination, and transform the way HUD does business.”

Sec. 1. This Act may be cited as the Affordable Housing Planning and Appeal Act. Sec. 5. Findings. The legislature finds and declares that: (1) there exists a shortage of affordable, accessible, safe, and sanitary housing in the State; (2) it is imperative that action be taken to assure the availability of workforce and retirement housing; and (3) local governments in the State that do not have sufficient affordable housing are encouraged to assist in providing affordable housing opportunities to assure the health, safety, and welfare of all citizens of the State. Sec. 10. Purpose. The purpose of this Act is to encourage counties and municipalities to incorporate affordable housing within their housing stock sufficient to meet the needs of their county or community. Sec. 15. Definitions. As used in this Act: “Affordable housing” means housing that has a value or cost or rental amount that is within the means of a household that may occupy moderate-income or low-income housing. In the case of owner-occupied dwelling units, housing that is affordable means housing in which mortgage, amortization, taxes, insurance, and condominium or association fees, if any, constitute no more than 30% of the gross annual household income for a household of the size that may occupy the unit. In the case of dwelling units for rent, housing that is affordable means housing for which the rent and utilities constitute no more than 30% of the gross annual household income for a household of the size that may occupy the unit.

As laws are wont to do, this one goes on and on, in excruciating detail, about who, what, why, when, and how, all invented by politicians who are clueless about the needs of poor people

Worse yet, all laws are generalities, that do not take into consideration the massively different needs of massively different families. It is the ultimate expression of paternalism by uninformed leaders.

My village of Wilmette, IL provides one of many examples of how difficult (impossible?) it is to provide affordable housing through legislation.

Wilmette, IL. Population: 27,087 people, 9,742 households.

Median household income in Wilmette, IL is $148,678 (compared to about $62,000 for the U.S.)

The median home price in Wilmette is $702,660, Zillow)

(There are 2 Low-Income Apartment Communities In all of Wilmette) Gates Manor Apartments, 51 bedroom units. (Section 8 Project-Based Rental Assistance) Shore Line Place, 44 bedroom units. (Section 202 Supportive Housing for the Elderly)

Out of 27 thousand people and nearly 10 thousand households, Wilmette has created 95 “affordable” apartments, of which half are for the elderly. Would anyone consider this a “solution to unaffordable housing”? A better description would be “tokenism.”

Wilmette primarily is composed of upscale, single-family housing. Yet, the political leaders of Wilmette felt a moral (legal?) obligation to provide affordable housing for poor people.

Clearly, the Wilmette government would not pay hundreds of thousands of dollars to purchase a decent Wilmette home to shelter a poor family.

Additionally, merely residing in Wilmette is costly. The school system is costly. Taxes are costly. Upkeep is costly. Even water is costly. So if poor families even were given free houses, they couldn’t support the ongoing costs.

The solution to housing unaffordability, indeed the solution to all unaffordability by the poor, is for the federal government to give people money. The Ten Steps to Prosperity (below) provides one set of solutions.

Rather than having politicians decide what universal percentage of household income counts as “affordable housing,” let each individual and each family make that decision. A 35-year-old man, with three children, surely will have different needs and make a different decision than a 55-year-old widow living alone.

Laws are expensive. At the local level, money spent to create and enforce laws does not benefit the populace. By contrast, federal spending costs people nothing, and it can solve the real problems facing the poor.

They are poor. They are short of money. The federal government has infinite money. The solution is clear. Help people improve their own lives by simply giving them money.

We should replace “affordable housing” laws with the Ten Steps to Prosperity.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

Background: The Cato Institute is an American libertarian think tank, founded as the Charles Koch Foundation.

It supports lowering or abolishing most taxes, opposition to the Federal Reserve system, the privatization of numerous government agencies and programs including Social Security, the Affordable Care Act, and the United States Postal Service, along with adhering to a non-interventionist foreign policy.

Reason is an American libertarian monthly magazine published by the Reason Foundation. Peter Suderman works for Reason.

Libertarianism tends toward anarchy; seemingly any level of government ownership or control, no matter how small, is considered too large by libertarians.

The following article perfectly illustrates the libertarian worldview:

The Warren worldview of ill-founded economic pessimism is both bloodless and moralizing.

PETER SUDERMAN | FROM THE OCTOBER 2019 ISSUE OF REASON

At the heart of Elizabeth Warren’s campaign for president—and of her entire career as a politician and public intellectual, are two simple ideas.

The first is that the economy is fundamentally broken. She declared that “millions and millions of American families are also struggling to survive in a system that has been rigged by the wealthy and the well-connected” and in which she insisted that the only response was to fight for “big structural change.”

She inveighed against corporate profits and monopolistic businesses and corrupt lawmakers who have “made this country work much better for those who can make giant contributions, made it work better for those who hire armies of lobbyists and lawyers, and not made it work for the people.”

It was present in the 2007 essay that imagined what would eventually become the Consumer Financial Protection Bureau, a federal agency premised on the notion that American families were being “steered into overpriced credit products, risky subprime mortgages, and misleading insurance plans'”

She proposed an array of economic policies, from a $15 minimum wage to enforcing restrictions on certain bank loans, that she argued could stave off the crisis.

(She issued a) slew of white papers and policy proposals that have poured forth from Warren’s campaign as if she were running a think tank rather than a presidential bid.

It’s her own fault. Don’t ask for government help.

Apparently, libertarian Suderman doesn’t believe that “millions of American families are also struggling to survive in a system that has been rigged by the wealthy and the well-connected” and “this country works much better for those who can make giant contributions, and for those who hire armies of lobbyists and lawyers.”

He is living in a libertarian dream world.

He doesn’t like that Warren has proposed a $15 minimum wage, up from the current federal minimum of $7.25 hour — barely survivable for a single person, and poverty-level for supporting a family.

Libertarian Suderman doesn’t like that Warren wants to restrict the terrible bank loans that contributed to the “Great Recession of 2008.”

Suderman doesn’t like that Warren has issued “white papers and policy proposals,” rather than merely promising generalities and American greatness.

In the space of just a few months this year, Warren released plans for everything from ending drilling on public lands to breaking up Facebook and Amazon.

And she has proposed paying for these costly programs with wealth taxes designed not only to offset the price tag of new government spending but to help reduce economic inequality by shrinking large stores of wealth.

To Suderman, ending drilling on public lands, providing affordable housing, canceling student debt, and offering free college tuitions — i.e. ideas to narrow the Gap between the rich and the rest — are terrible.

Unworkable, because “wealth” is far too easy for the truly wealthy to hide.

Warren’s penchant for wonky policy detail has defined her candidacy: “Elizabeth Warren has a plan for that” has become a rallying cry and a slogan, one her fans have plastered across an array of T-shirts and campaign signs.

Warren has happily embraced this persona, joking with crowds that her focus on the details of federal agencies would turn them all into nerds.

Heaven forbid that a candidate supplies plans and details. To Suderman, it would be far better to offer bland Trump-like generalities, like “Repeal and replace ACA”” and “Build the wall” than to provide specific, people-friendly details.

Warren wants the federal government to be the American economy’s hall monitor, telling individuals and companies what they can and can’t sell or buy and making some of the nation’s most successful businesses answer to her demands.

Being the economy’s “hall monitor,” i.e. preventing miscreants from stealing, is exactly what the federal government should do.

And oh, horrors, telling the nation’s most successful businesses what dishonesty not to commit, is unthinkable to Suderman, who seems to believe that “liberty” means allowing big business to do whatever it pleases.

It seems to be working. During the first six months of 2019, this strategy vaulted Warren into the top tier of Democratic primary contenders, helping her raise more than $19 million during the year’s second quarter and placing her among the top three or four candidates in the party’s crowded field.

Focus groups and political reporting have consistently found that Democratic voters are warming not only to the substance of Warren’s ideas but to the very fact that she has them.

Well yes. Having ideas and detailing them, not only is good politics, but it is good governance. Would that more politicians did it.

Although she has received kudos for the volume and specificity of her plans, Warren has a history of pushing misleading research and cherry-picked data designed to support politicized conclusions.

Warren first rose to prominence as the co-author of a pioneering study of consumer bankruptcy, which was published in book form in 1989 under the title As We Forgive Our Debtors: Bankruptcy and Consumer Credit in America.

Warren and her co-authors based the book on a trove of court data from about 1,500 bankruptcy cases in Pennsylvania, Illinois, and Texas during 1981.

The book relied on real-world case studies. Warren statistically analyzed a trove of unique data. She was telling a story to make an argument about politics and policy.

The story was that rapacious credit card companies, rather than consumer overspending, were primarily responsible for a run-up in consumer debt and the resulting sense that household budgets had grown more precarious.

The book’s authors saw bankruptcy in broadly sympathetic terms, as a financial safety net for struggling families. In the years that followed, Warren would go on to become one of the nation’s most prominent advocates of making bankruptcy easier, more lenient, and more accessible.

But that story had some notable problems. Among others, it was based on cases from 1981, a recession year when consumers would have looked worse off than usual. It was released years later, after a significant reform to the bankruptcy code in 1984 rendered its picture of American bankruptcy somewhat out of date.

Here, Suderman criticizes the currency of Warren’s bankruptcy research, none of which has anything to do with the currency of her above-mentioned economic recommendations.

It’s as though Suderman would hate her ideas for child-rearing because her book on auto repair is out of date. In short, Suderman’s criticism is inane and utter nonsense.

And note the words, “rather than consumer overspending.” They illustrate the libertarian belief that poor people are responsible for their own misfortune.

Warren drew on her bankruptcy research to argue that the middle class had been given a raw deal.

The number of households filing for bankruptcy had shot up dramatically, she said, and it wasn’t because they were spending too much.

Instead, the increasingly high cost of housing, driven heavily by competition for access to good schools, and the pile-up of medical debt were driving families into dire straits.

It is the high cost of living, not just housing, has driven families into dire straights.

Again, Suderman wants to “prove” Warren is completely wrong, by trying to nit-pick a point of data, when her overall conclusion (that the Gap between rich and poor has widened, and many families are in financial trouble and need protection) is correct.

These effects were compounded by the movement of women into the workforce.

Where stay-at-home wives had once served as a safety net—the earners of last resort should a breadwinner husband lose his job—the rise of the working mother had increased financial risk for two-earner families.

The book’s findings were marked by controversy and unanswered questions about the soundness of her methodology. In particular, Warren’s notion that housing prices have been pushed upward by school competition doesn’t fully stand up to scrutiny.

Although research has found that school quality does impact housing prices, the effect is fairly modest. A 2006 study in the Quarterly Journal of Economics found a 2.5 percent increase in home prices for every 5 percent increase in test scores.

And in what way does the so-called “fairly modest” difference in home prices negate Warren’s position on student debt, mortgage supervision, family bankruptcy, the minimum wage, and the prevention of financial cheating by large companies?

It doesn’t, but Suderman tries to make his point by fixating on minutia to distract you from the main point, that middle-class families are struggling, and the very purpose of government is to improve the lives of its citizens.

And then there’s the role of taxes. In the book’s hypothetical comparison budgets, Warren presents taxes as a percentage of household income—24 percent in the 1970s, 33 percent in the 2000s—which the book describes as a 35 percent change.

Yet as George Mason University law professor and consumer finance scholar Todd Zywicki has noted, the choice to render taxes only as a percentage of income has the effect of masking the total dollar value.

Using Warren’s own figures, Zywicki calculated that the tax increase—owing partly to the hypothetical family hitting a new tax bracket and partly to the imposition of additional state, local, and property taxes over time—was by far the largest factor affecting the modern family’s budget.

Warren’s numbers, in other words, showed that families had been strapped not by increased spending on homes or health insurance but by a bigger tax bill.

Yes, taxes on the middle classes are too high. So, how does that eliminate the need to follow Warren’s proposals? Again, it doesn’t. It’s just another Suderman diversion.

Zywicki is among Warren’s most outspoken critics, and he has made this case—that Warren’s data do not show what she claims they do about the plight of the middle class—on multiple occasions over the span of more than a decade.

What Suderman fails to mention is that Zywicki is a senior fellow, paid by the Cato Institute, that aforementioned libertarian think tank, which spends its time and money trying to prove that government not only is unnecessary but a hindrance to America.

Zywick is not exactly an impartial commenter.

Warren co-authored a Health Affairs study purporting to show that at least 46 percent of the nation’s bankruptcies were a result of medical bills, a figure she subsequently updated to 62 percent.

Her research claimed that medically induced bankruptcies had increased a shocking 23-fold since 1981.

President Barack Obama warned that sky-high medical costs had forced many Americans to “live every day just one accident or illness away from bankruptcy.”

One wonders, what is the fundamental point Suderman is trying to demonstrate? That sky-high medical costs are not a serious financial problem for millions of Americans?

The response by Warren and her co-authors was revealing. In one sense, they were engaged in a conventional academic dispute about interpreting bankruptcy data. But what they were really fighting about—what was really at stake—was public policy.

Warren clearly believed that the value of her research was in the story it told and the way that story informed and influenced the real world of politics and public affairs.

Yes, that exactly is the point. What does it matter whether housing prices, or school costs, or medical costs are most responsible for bankruptcies or other forms of financial distress?

The point that Suderman doesn’t want you to understand is that these are problems the federal government can and should address. It has the means, if only it had the will.

Sadly, the Sudermans of the world would rather quibble about differences in data than to solve the clear and obvious problems that plague us.

Yes, some things are more troublesome than others, but that does not mean we should stall. while people suffer, debating how much more troublesome school costs are than medical costs.

But perhaps, stalling is what Suderman wants.

In the aftermath of the 2007–08 financial crisis, Congress, then controlled by Democrats, passed the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was billed as a direct response to the economic meltdown and an attempt to make sure it never happened again.

A centerpiece of the bill was the creation of a new federal agency, the Consumer Financial Protection Bureau (CFPB), which was modeled on Warren’s original proposal.

The bureau, as imagined by Warren, was premised on the notion that consumers did not and in some cases could not understand the financial services they relied on, and that only an army of unusually powerful government bureaucrats could save them from blundering into the tricks and traps set by lenders.

And that is absolutely correct. Left to their own designs, the banks created the most convoluted, complex financial products, that no one, not even Suderman, could understand, then sold them to the public, with disastrous results.

The CFPB’s mission, meanwhile, was far more expansive than its origin story might imply. From payday lenders to cash advance services, many of the financial products it was given the power to regulate had little or nothing to do with the financial crisis.

Suderman’s senseless point seems to be that if a financial scam had nothing to do with the Great Recession, it should be ignored.

The CFPB was the culmination of decades of research and advocacy on Warren’s part. She had imagined it, fought for its creation, and then, from her perch in the administration, ushered it into being.

And yet there was a kind of victory as well, in the simple fact of the CFPB’s creation. Warren would not be its leader—that role would eventually go to former Ohio Attorney General Richard Cordroy, who was given a recess appointment that caused its own controversy—but she had willed it into being and would continue to provide spiritual guidance.

She did not achieve her political ambitions, but on the policy question, she had triumphed.

In the years that followed, something strange happened: Warren, the icon of progressivism whose political brand had proven too toxic to move through the CFPB nomination process, became the object of a strange new respect from the right.

Apparently, being respected by some right-wingers is a curse for Suderman.

Under President Donald Trump, in July, The American Conservative, long a bastion of immigration-skeptical conservative nationalism, ran an essay extolling Warren’s economics, particularly her plans for a new bureaucracy dedicated to “defending good-paying American jobs,” and saying that in some respects, “Warren may be a bigger economic nationalist than even Trump himself.”

A paragraph of utter nonsense, but what else can one expect in political discourse?

Nor is Warren’s popularity limited to small opinion journals.

In June, Fox News’ Tucker Carlson, among the most-watched hosts on cable news and an influence on the Trump administration, opened his show with an extended monologue praising Warren’s domestic jobs plan and its elevation of “economic patriotism,” which calls for, in the senator’s words, “aggressive new government policies to support American workers.”

“Many of Warren’s policy prescriptions make obvious sense,” Carlson said. “She sounds like Donald Trump at his best.” Later, at a conference in July, he praised The Two-Income Trap as “one of the best books I’ve ever read on economics.”

Suderman’s position is if a right-winger likes any of her recommendations that is prima facie evidence she is not a progressive. It’s wrong and a bit goofy, but it’s Suderman.

But then, the quick reversal:

It is hard to imagine the Republican Party ever embracing Elizabeth Warren. Trump frequently mocks her claims of Native American heritage, and the congressional GOP continues to view her with deep hostility. She’ll never be an ally to the party.

But in some increasingly influential corners of the right, her ideas and her outlook are winning.

The rest of Suderman’s long article is a rehash of his “unaffordability” claim about her proposals, and his dislike of the detail with which she presents them.

But “unaffordability” is a false claim concerning federal spending, and quibbling about the details rather than solving the big-picture problems solves nothing.

SUMMARY Government is created by the governed to improve their lives. That is the purpose of government.

Peter Suderman is a classic libertarian, a hater of government. As a libertarian, he wastes more than 6,000 words denying the obvious — that for many people, good schooling, good housing, good food, and good medical care are unaffordable and that the banking industry has cheated millions of innocent people.

Suderman denies that many families are driven into bankruptcy by trying to pay for the abovementioned schooling, housing, food, and medical care, or eschewing bankruptcy, they must forego these life necessities.

Suderman also hints at the libertarian’s “bootstraps” theory, in which the victim is blamed for not earning enough, or being frugal enough, or smart enough to pay for their own needs.

To libertarians, “liberty” means freedom from government help. People should pull themselves up by their bootstraps, rather than depending on the government.

Then he applies the libertarian, “Catch 22” objection to deny people those bootstraps by implying that the $15 minimum wage is a bad idea. “Gotcha!”

In the real world, our “bootstraps” consist of things like a good education, good health, good housing, and money — all of which the federal government can and should provide — and all of which libertarian Suderman would not provide.

Why does libertarian Suderman deny the obvious?

Because to admit it would require him to offer solutions, and those solutions inevitably require federal spending — an anathema to libertarians.

Warren’s proposals are fact-driven and logical, which Suderman dismisses as “bloodless.” Her proposals also benefit the poor and middle classes, which Suderman dismisses as “moralizing.”

Suderman and the libertarians live in a harsh mythical world, where there is no allowance for poverty, people are expected to be born with all they need to succeed, and it only is laziness that prevents them from realizing their dreams.

Asking for help from the government supposedly is a moral and financial imposition on the rest of us who, of course, are self-sufficient.

It is the ultimate expression of Gap Psychology, in which people wish to widen the income/wealth/power Gap below them.

Slum: a thickly populated, run-down, squalid part of a city, inhabited by poor people.

Few slums were built as slums. Most slums began as ordinary, middle-class housing and evolved to be slums.

The exceptions might be the high-rise, no-rent, warehouses-for-the-poor, erected by city leaders who needed some place to segregate the lowest (and darkest skin) end of the riff-raff.

But even they began new, and were converted to slums by tenants without the means to preserve the buildings, and owners who don’t care.

And that is the formula for creating a slum: Residents with insufficient financial means to pay rent, to repair, or even to clean, plus owners with insufficient financial motivation to repair or clean.

If we don’t want to create slums, we need either to improve residents’ financial means and/or to improve owners’ financial motivation. It’s that simple, but if one doesn’t want a simple solution, he will make it complex.

I thought of this when I read an article in the Chicago Tribune:

The average renter in the Chicago area does not earn enough to comfortably afford a modest apartment, a study by the National Low Income Housing Coalition reported Wednesday.

Higher housing costs are forcing people to skimp on other necessities such as food, child care and transportation, said Andrew Aurand, vice president of research for the coalition.

The average hourly pay for the 1.1 million renters in the Chicago area is just $17.03 an hour, or about $35,422 annually. To afford the typical two-bedroom at $1,176, a renter in the Chicago area would need to be earning $22.62 an hour, or $47,040 annually.

The lowest-income households are especially squeezed, the report said. While there are subsidies for low-income people, only 1 in 4 of those eligible for aid actually receive it because there are waiting lists.

The affordability issue extends throughout the country.

A family depending on a minimum wage of $7.25 per hour would need a single worker to take on 2.8 full-time jobs to afford the average U.S. two-bedroom apartment, said Diane Yentel, president of the housing coalition.

That’s 112 hours per week for all 52 weeks of the year, leaving no time for anything except working and sleeping eight hours a night, she said.

The coalition is urging local and national governments to provide incentives for constructing more affordable housing, and Yentel suggested that some funding would be available if the government cut back the mortgage interest deduction for affluent homeowners.

Let’s return to the formula for a slum: Residents with insufficient financial means + owners with insufficient financial motivation.

Clearly, the long term solution to that problem is to increase residents’ financial means and increase owners’ financial motivation.

Chicago’s high rise “gold coast” has both. The residents are well able to afford the rents and the owners receive enough rents for beautiful upkeep, preventing the buildings from turning into slums.

So these tall buildings, some of which are quite old, are in excellent repair, and the people live very nicely, thank you. Contrast them with the high-rise slums common to American cities.

In Chicago, Bob Palmer, policy director of Housing Action Illinois, said the state should pass an emergency spending bill and provide $9.3 million for homeless shelters and $65 million for building affordable housing through the Illinois Housing Development Authority. Shelters are needed, he said, because “we are a long way from having enough affordable housing.”

Forcing people into shelters or into the street, is disgraceful for our wealthy nation.

The solution to the problem: Make sure no one would have so low an income as to be unable to afford well-maintained housing.

But Illinois, being monetarily non-sovereign, is broke, so the representatives for the working poor must beg for homeless shelters and so-called “affordable housing.”

Since monetarily non-sovereign Illinois can’t do it, then Monetarily Sovereign USA could and should.

During the last couple of decades, the number of affordable units has declined while demand has grown, Aurand said.

Fewer people own homes now than they did before the housing crash.

Millions lost homes and suffered job setbacks, so millions now require rentals at the same time that there has been a population boom of people in their 20s and early 30s — a group that typically rents.

In addition, baby boomers are retiring, and a significant number are interested in renting.

So lets put it all together:

Many people have difficulty finding jobs.

Even many working people make too little to afford apartments in well-maintained buildings and neighborhoods.

Landlords are not motivated to maintain their buildings unless rents are sufficient.

Therefore, forcing landlords to provide so-called “affordable” housing leads to poorly maintained housing.

Poorly maintained housing is contagious, in that one dilapidated building in a neighborhood causes immediate neighbors to flee, nearby surrounding rents to drop, and those lower rent buildings to be less cared for — the beginnings of a slum. This is what happens in previously well-kept neighborhoods, that have turned bad.

Cities, counties and states, all of which are monetarily non-sovereign, and so cannot create dollars at will, cannot afford to provide income to the poor. To provide subsistence, they must levy taxes — sales and property — which invariably are regressive, thereby punishing the poor even more.

The federal government, being Monetarily Sovereign, has the unlimited ability to improve the incomes of the poor.

However, the populace has been trained by the rich to resent the poor receiving money. The resentment is based on two myths:

A. Giving the poor money makes them lazy and satisfied to do nothing

B. *Federal spending is paid for by federal taxes.

These myths are promulgated by the rich, who want:

a. A ready supply of desperate, low-paid servants.

b. To widen the Gap between the rich and the rest

The poor need income and education. Landlords need rent and educated tenants.

The solution is a combination of direct, modest, financial support for the poor, together with the elimination of factors that keep the poor from lifting themselves through work and education.

The solution is the Ten Steps to Prosperity. (See below.)

Returning to the title question, “Who wants to create a slum?” the answer is: The rich.

Nothing happens in America without the urging and complicity of the rich. The rich run America.

The rich bribe the politicians via campaign contributions, even more effectively now that the right wing Supreme Court has decided money is constitutionally protected “free speech.” Thus we have the regressive FICA and sales taxes along with income tax loopholes that benefit only the rich.

The rich bribe the media via ownership, so that media writers indoctrinate the populace into believing falsely that the poor are sloths who deserve their poverty, and that deficit spending is paid for by taxpayers.

The rich bribe the economists, via benefits to universities and “think tanks,” to claim there is a “deficit problem,” which prevents helping the poor.

Slums are no accident. They exist by design. The rich create slums and slum buildings to perpetuate and house the servant class.

=================================================================================== Ten Steps to Prosperity: 1. ELIMINATE FICA (Ten Reasons to Eliminate FICA ) Although the article lists 10 reasons to eliminate FICA, there are two fundamental reasons: *FICA is the most regressive tax in American history, widening the Gap by punishing the low and middle-income groups, while leaving the rich untouched, and *The federal government, being Monetarily Sovereign, neither needs nor uses FICA to support Social Security and Medicare. 2. FEDERALLY FUNDED MEDICARE — PARTS A, B & D, PLUS LONG TERM CARE — FOR EVERYONE (H.R. 676, Medicare for All ) This article addresses the questions:

*Does the economy benefit when the rich afford better health care than the rest of Americans?

*Aside from improved health care, what are the other economic effects of “Medicare for everyone?”

*How much would it cost taxpayers?

*Who opposes it?”

3. PROVIDE AN ECONOMIC BONUS TO EVERY MAN, WOMAN AND CHILD IN AMERICA, AND/OR EVERY STATE, A PER CAPITA ECONOMIC BONUS (The JG (Jobs Guarantee) vs the GI (Guaranteed Income) vs the EB) Or institute a reverse income tax.

This article is the fifth in a series about direct financial assistance to Americans:

Economic growth should include the “bottom” 99.9%, not just the .1%, the only question being, how best to accomplish that. Modern Monetary Theory (MMT) favors giving everyone a job. Monetary Sovereignty (MS) favors giving everyone money. The five articles describe the pros and cons of each approach.

4. FREE EDUCATION (INCLUDING POST-GRAD) FOR EVERYONEFive reasons why we should eliminate school loans

Monetarily non-sovereign State and local governments, despite their limited finances, support grades K-12. That level of education may have been sufficient for a largely agrarian economy, but not for our currently more technical economy that demands greater numbers of highly educated workers.

Because state and local funding is so limited, grades K-12 receive short shrift, especially those schools whose populations come from the lowest economic groups. And college is too costly for most families.

An educated populace benefits a nation, and benefiting the nation is the purpose of the federal government, which has the unlimited ability to pay for K-16 and beyond.

5. SALARY FOR ATTENDING SCHOOL

Even were schooling to be completely free, many young people cannot attend, because they and their families cannot afford to support non-workers. In a foundering boat, everyone needs to bail, and no one can take time off for study.

If a young person’s “job” is to learn and be productive, he/she should be paid to do that job, especially since that job is one of America’s most important.

6. ELIMINATE CORPORATE TAXES

Corporations themselves exist only as legalities. They don’t pay taxes or pay for anything else. They are dollar-tranferring machines. They transfer dollars from customers to employees, suppliers, shareholders and the government (the later having no use for those dollars).

Any tax on corporations reduces the amount going to employees, suppliers and shareholders, which diminishes the economy. Ultimately, all corporate taxes come around and reappear as deductions from your personal income.

7. INCREASE THE STANDARD INCOME TAX DEDUCTION, ANNUALLY. (Refer to this.)

Federal taxes punish taxpayers and harm the economy. The federal government has no need for those punishing and harmful tax dollars. There are several ways to reduce taxes, and we should evaluate and choose the most progressive approaches.

Cutting FICA and corporate taxes would be an good early step, as both dramatically affect the 99%. Annual increases in the standard income tax deduction, and a reverse income tax also would provide benefits from the bottom up. Both would narrow the Gap. 8. TAX THE VERY RICH (THE “.1%) MORE, WITH HIGHER PROGRESSIVE TAX RATES ON ALL FORMS OF INCOME. (TROPHIC CASCADE)

There was a time when I argued against increasing anyone’s federal taxes. After all, the federal government has no need for tax dollars, and all taxes reduce Gross Domestic Product, thereby negatively affecting the entire economy, including the 99.9%.

But I have come to realize that narrowing the Gap requires trimming the top. It simply would not be possible to provide the 99.9% with enough benefits to narrow the Gap in any meaningful way. Bill Gates reportedly owns $70 billion. To get to that level, he must have been earning $10 billion a year. Pick any acceptable Gap (1000 to 1?), and the lowest paid American would have to receive $10 million a year. Unreasonable.

9. FEDERAL OWNERSHIP OF ALL BANKS (Click The end of private banking and How should America decide “who-gets-money”?)

Banks have created all the dollars that exist. Even dollars created at the direction of the federal government, actually come into being when banks increase the numbers in checking accounts. This gives the banks enormous financial power, and as we all know, power corrupts — especially when multiplied by a profit motive.

Although the federal government also is powerful and corrupted, it does not suffer from a profit motive, the world’s most corrupting influence.

10. INCREASE FEDERAL SPENDING ON THE MYRIAD INITIATIVES THAT BENEFIT AMERICA’S 99.9% (Federal agencies)Browse the agencies. See how many agencies benefit the lower- and middle-income/wealth/ power groups, by adding dollars to the economy and/or by actions more beneficial to the 99.9% than to the .1%.

Save this reference as your primer to current economics. Sadly, much of the material is not being taught in American schools, which is all the more reason for you to use it.

The Ten Steps will grow the economy, and narrow the income/wealth/power Gap between the rich and you.

========================================================================================================================================================================================================================================================================================================

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

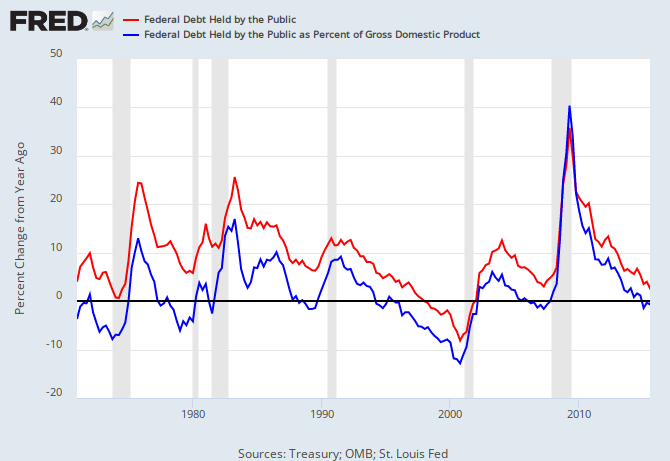

THE RECESSION CLOCK

Recessions begin an average of 2 years after the blue line first dips below zero. A common phenomenon is for the line briefly to dip below zero, then rise above zero, before falling dramatically below zero. There was a brief dip below zero in 2015, followed by another dip – the familiar pre-recession pattern. Recessions are cured by a rising red line.

Vertical gray bars mark recessions.

As the federal deficit growth lines drop, we approach recession, which will be cured only when the growth lines rise. Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

Mitchell’s laws:

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money.

•The more federal budgets are cut and taxes increased, the weaker an economy becomes.. •No nation can tax itself into prosperity, nor grow without money growth.

•Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

•A growing economy requires a growing supply of money (GDP = Federal Spending + Non-federal Spending + Net Exports)

•Deficit spending grows the supply of money

•The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

•The limit to non-federal deficit spending is the ability to borrow.

•Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.