This is a challenge to the CRFB.

To: Maya MacGuineas, President;

I recently received an Email from you, which I will quote in its entirety.

Congress has until December 16th to fund the government and avoid a federal shutdown. If they avoid that, they’ll likely have done so with the same tired Washington tactic of promising billions in new deficit-funded spending or tax cuts, driving the national debt even higher.

We have asked Congress not to borrow any new money for the rest of 2022.

With our Debt Fixer interactive tool, you have the opportunity to craft a national budget that puts America on a sustainable fiscal course heading into 2023.

How It Works: The Debt Fixer gives users the opportunity to confront many of the same budget decisions that lawmakers face and to see how those choices affect the debt. You’ll be asked to make decisions on a range of policy options with the goal of stabilizing the debt at 90 percent of Gross Domestic Product (GDP) within ten years and 60 percent of GDP by 2050.

Afterwards, users can share select to share their fiscal choices with Members of Congress and social media. Can you do better than Congress? Give it a try now!

If you’re a teacher and would like to use the Debt Fixer in your class, please let us know by e-mailing debtfixer@crfb.org.

We can provide additional resources for your classroom including guest speakers and a customizable link where you can compare your classes results. If you enjoy Debt Fixer, we encourage you to check out our other interactive resources: Budgeting for the Future, Is It Worth It, and the Social Security Reformer.

Here you’ll be able to test your budget knowledge, compare the costs of proposals and policies, and choose the options to stabilizing the debt at 90 percent of Gross Domestic Product (GDP) for future generations.

I have bolded the following phrases from your Email: “driving the national debt even higher,” “not to borrow,” “not to borrow,” “sustainable fiscal course,” “stabilizing the debt at 90 percent of Gross Domestic Product (GDP), and “stabilizing the debt at 90 percent of Gross Domestic Product (GDP).”

As I suspect you know, the U.S. federal government is Monetarily Sovereign, i.e., it has the infinite ability to create its own sovereign currency, the U.S. dollar. This ability sometimes (incorrectly) is referred to as “printing” dollars.

The infinite ability to “print” dollars means the U.S. government never unintentionally can run short of dollars.

THE CHALLENGE

Given the fact that the U.S. government cannot run short of dollars, I challenge you to answer the following questions:

- DRIVING THE NATIONAL DEBT EVEN HIGHER: Given the federal government’s infinite ability to “print” (create) dollars why should anyone be concerned about the size of the “national debt”?

- NOT TO BORROW: Given the federal government’s infinite ability to create dollars why should the federal government need to borrow dollars?

- DEBT FIXER: Given the federal government’s infinite ability to create dollars, why does the federal debt need fixing?

- SUSTAINABLE FISCAL COURSE: Given the federal government’s infinite ability to create dollars, and the fact that it has sustained its fiscal course for the past 80+ years while the federal debt has increased 62,500%, why do you believe it’s current fiscal course suddenly has become unsustainable?

- STABILIZING THE FEDERAL DEBT AT 90 PERCENT OF GROSS DOMESTIC PRODUCT (GDP): In what way does the ratio of federal debt / GDP affect the economy?

I have followed your Emails for several years, during which time you repeatedly have voiced the same concerns about federal deficit spending. Yet, you never have answered the above questions.

Here are the facts you continually ignore:

- The government’s infinite ability to create dollars means it never needs to be concerned about any debt. It has a greater ability to pay its debts than Elon Musk’s ability to pay a 1 cent debt.

- The federal government does not borrow, nor will it ever need to. As the St. Louis Fed reported: ““As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

The U.S. government provides T-security accounts into which other governments and private citizens are allowed to deposit dollars for safekeeping.

The purpose of these accounts is not to provide the federal government with dollars, but rather to provide the world with a safe place to store unused dollars. This helps stabilize the dollar.

To pay off these deposits, the federal government merely returns the dollars that are in those accounts. Returning existing dollars is no burden on the federal government or on U.S. taxpayers. - The federal debt is not a real debt. It is deposits that are owned by other governments and private citizens. It does not need “fixing.” If the federal government stopped issuing T-securities tomorrow, that would have no effect on the government’s ability to spend dollars and to pay its bills.

- The federal government has proved, year after year, that its course is sustainable. Despite a massive increase in the so-called “debt,” the government has no difficulty funding every expenditure.

- The ratio of federal “debt” to GDP is economically meaningless. It has no effect on the government’s ability to spend or on inflation, or on any aspect of economic health. GDP dollars do not pay for federal debt.

The ratio also is ludicrous because it compares a multiyear figure (debt) to a one-year figure (GDP). One easily could ask, “Why not compare debt to the six-month GDP or the one-month GDP, or even the ten-year GDP?”

U.S. depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

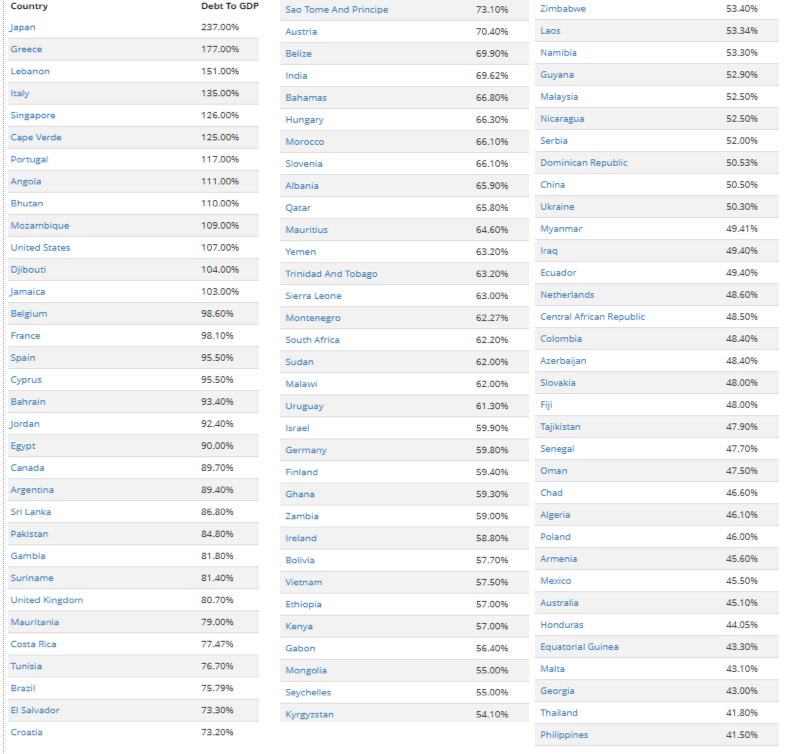

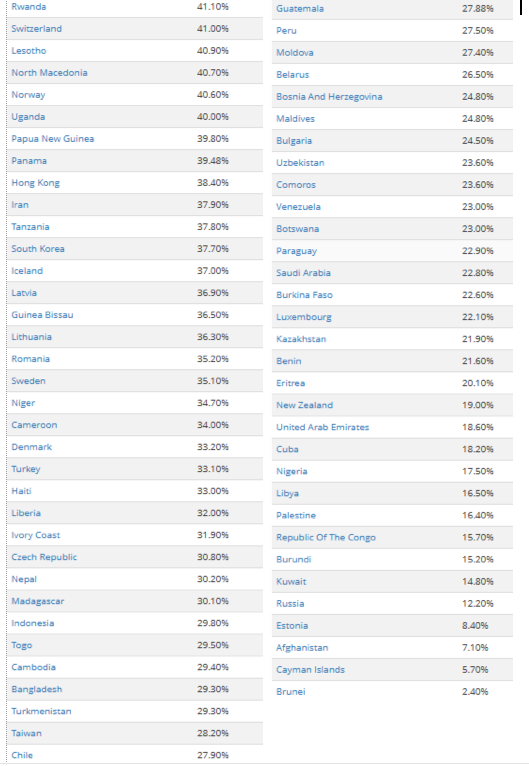

Using the tables below, see if you can determine which economies are “healthiest.”

(You won’t succeed, because the debt/GDP ratios tell you nothing about the health of a nation’s economy:

SUMMARY The CRFB never has and never will accept my challenge. They never will answer the questions, because the true answers would eliminate their reason for existence.

The CRFB is worse than useless. It is harmful to America. I believe they know they are harmful, in which case that would make them traitors.

I believe they are paid by the rich in America to widen the income/wealth/power Gap between the rich and the rest of us, in which case that would make them paid traitors.

I am angry at them. They hurt America.

If you believe they have answers and can meet the challenge, feel free to contact them. I’d be interested in seeing how they try to squirm out of this. Contact Maya MacGuineas at MacGuineas@crfb.org and find her on Twitter @MayaMacGuineas.

If you think I am angry at the CRFB, you’re right. I believe they have done, and continue to do, irreparable harm to America by giving aid and comfort to politicians who vote against benefits.

The claim that Medicare and Social Security can run short of money is absurd, especially so when the federal government, at the touch of a computer key, can provide all the money these agencies need.

The claim that the federal debt is too high also is absurd, when it isn’t even debt and it could be paid off entirely simply by returning the dollars in storage.

Even more absurd is to worry about the debt/GDP ratio, which compares a multi-year figure to a one-year figure, and is indicative or predictive of nothing.

Good luck.

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

BRAVO — Thank you. Sheila Smith

LikeLike

While looking at the chart of debt/GDP versus inflation I noticed that although there is almost no correlation, there are quite a few areas where they go in opposite directions. I would take this to mean that a higher/lower debt to GDP ratio is sometimes associated with a lower/higher inflation rate. Hmmm.

I hope you have a Happy Christmas/Chanukah and a Merry New Year.

LikeLike

Good call, John. It’s simple arithmetic.

Since federal debt and the debt/GDP graphs generally parallel (https://fred.stlouisfed.org/graph/fredgraph.png?g=XHwS), one could say that higher / lower inflation is associated with lower/higher debt, and that is precisely what we see (https://fred.stlouisfed.org/graph/fredgraph.png?g=XHxb)

So, the question is, why?

1. We previously have shown that inflation is associated with shortages, especially oil and food shortages.

2. Shortages cause slow economic growth, even recessions.

3. How is economic growth measured? By GDP, which is the nation’s measure of SPENDING. And an essential part of GDP is FEDERAL spending.

4. When federal spending growth declines, GDP growth must decrease. That’s arithmetic.

5. When GDP growth declines, the federal government reflexively spends more to prevent/cure recessions.

6. That increase in spending mathematically increases GDP.

The tendencies go like this:

Shortages —> Recessions

Recessions —> Lower prices

Recessions also —>Increased federal deficit spending

Increased federal deficit spending —> Increased GDP

Increased GDP —> Prices begin to rise

Increased GDP also—>oil and food prices rise.

Several other factors are involved, so the trail is not so neat. Fundamentally, though, federal deficits are part of GDP, so reducing deficit growth mathematically reduces economic growth.

The more gas you put in your car, the farther it will go. The debt nuts wish to reduce the amount of gas in the tank and are surprised when the car won’t go as far.

LikeLike

I’m just reading this article at The Intercept:

https://theintercept.com/2022/12/12/inflation-covid-war-joseph-stiglitz-ira-regmi/

This is the paper they refer to:

Click to access RI_CausesofandResponsestoTodaysInflation_Report_202212.pdf

It totally supports your eternal contention that inflation, particularly this one is caused by shortages of food and fuel.

LikeLike

Japan’s public sector debt problem is an illusion. If I buy back my own mortgage, I don’t have a mortgage.

Firstly, net debt, not gross debt matters for solvency. BoJ holdings are part of the consolidated government balance sheet. So its holdings are in fact the accounting equivalent of a debt cancellation.

In 2017 when BOJ owned 40% of outstanding Japanese government debt someone told me that the correctly measured net debt of Japan (net of public sector financial assets and bonds held by the BoJ) was then around 65% of GDP and falling.

https://asia.nikkei.com/Economy/Inflation/Bank-of-Japan-s-government-bond-holdings-exceed-50-of-total June 2022 Likely going to 60% in the coming years after the present inflation blip evaporates

LikeLike