Liars, fakers, and fear-mongers lurk among us. They masquerade as prudent economics advisors. They sell you their snake oil linament to cure your . . . whatever.

That brings us to one of America’s most prominent snake oil sales groups, the CRFB (Committee for a Responsible Federal Budget).

They have been selling the same nonsense for many years. Their president even testified before Congress, with all those old, sage heads nodding dumbly in agreement at the foolishness she was spouting.

We’ve spoken of the CRFB many times, but they keep selling the same lies.

Here they go again:

New Projection: Federal Debt Will Reach Record Levels Sooner Than Expected NOV 16, 2022 BUDGETS & PROJECTIONS

The nation’s fiscal and economic outlook has deteriorated substantially since the last Congressional Budget Office (CBO) baseline in May, when CBO projected debt would reach a record 110 percent of Gross Domestic Product (GDP) by 2032.

Under an updated current law baseline, we now project debt in 2032 will reach 116 percent of GDP, deficits will reach 6.6 percent of GDP, and interest will reach a record 3.4 percent of GDP.

Under a more pessimistic (and in many ways realistic) scenario, debt in 2032 would reach 138 percent of GDP, deficits would reach 10.1 percent, and interest would total 4.4 percent of GDP.

These projections suggest an unsustainable fiscal trajectory.

Oh, horrors. Federal “debt” will exceed GDP. And federal interest payments will be some “high” percentage of GDP. How awful. Right? WRONG!

The innocent reader would be led to believe there must be some crucial connection between so-called “debt” and GDP. Is it that GDP pays for “debt” so that when “debt” exceeds GDP, the “debt” can’t be paid?

That’s what the liars, fakers, and fear-mongers want you to believe. However, no such connection exists. None. Here’s why:

First: The so-called “federal debt” isn’t a federal debt. The federal government doesn’t owe it.

GDP is the one-year total of national spending (federal + non-federal) + net exports. It’s just the cumulative net difference between federal taxes and federal spending for at least 30 years. So the CRFB is comparing a 30-year (apples) total to a 1-year (oranges) total. Apples and oranges.

What commonly is called “debt” actually equals the total dollars invested into Treasury Security accounts. The vast majority of these accounts are owned by the public and foreign nations.

You first open a T-security account when you invest in a T-bill, T-note, or T-bond. You own that account. The dollars you invest go into your account and stay there until maturity.

Second: The federal government does not touch your dollars. The federal government does not use your dollars to pay its bills. Your dollars just sit there, accumulating interest.

The closest corollary would be a bank safe deposit box. The bank does not owe you the contents of your safe deposit box. The contents belong to you and are unrelated to the bank’s finances.

Similarly, the contents of T-security accounts are unrelated to federal finances. As with safe deposit boxes, the government pays off those accounts simply by returning the contents to you.

Third: The sole purposes of T-bills, T-notes, and T-bonds are to provide a safe storage place for unused dollars and to help the Fed control interest rates. This helps stabilize the dollar.

T-security accounts do not, in any way, help the federal government pay its bills. The federal government could stop accepting deposits into T-security accounts today and still pay all its bills forever. People, businesses, and nations would need to find some other places to store unused dollars, which for nations like China could be inconvenient.

Fourth: Even if the misnamed “federal debt” were actually debt, that still would have nothing to do with Gross Domestic Product. GDP doesn’t pay for any debts, not yours, mine, or the federal government’s.

GDP is not even a measure of federal income. GDP is just a one-year measure of all the spending in the economy, federal and non-federal.

Fifth: Even if the federal government owed the so-called “federal debt,” that would not be a problem. The federal government pays all its debts by creating new dollars ad hoc.

To pay a creditor, the federal government sends instructions, not dollars, to the creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account. When the creditor’s bank obeys those instructions, it creates new dollars, which are added to the money supply measure, M2.

The instructions then are cleared by the Fed, an agency of the U.S. government. Thus, the government approves its own money-creation instructions.

The government doesn’t use tax dollars. It destroys tax dollars upon receipt by the Treasury. To pay you taxes you take M2 money supply dollars from your checking and send them to the Treasury. When your M2 dollars reach the Treasury, they cease to be part of any money supply measure.

Because the U.S. government has infinite dollars, there can be no measure of its dollar supply, so your tax dollars effectively are destroyed.

The U.S. government never borrows dollars. What erroneously is termed “borrowing” merely is the acceptance of deposits into those T-security accounts that the government never touches.

The government doesn’t use any form of income. Even if the federal government collected $0 taxes, it could continue paying its financial obligations forever.

None of the above applies to state and local governments, which are monetarily non-sovereign. They do use tax receipts and other forms of income with which to pay their bills. They do not destroy tax dollars; they store them in bank accounts, just like you do.

Side note: Some European nations are monetarily non-sovereign, and some are Monetarily Sovereign. This difference often is not recognized by economists, the media, and politicians. Often you will read papers that purport to prove U.S. federal debt is dangerous because “look at Greece, Italy, France, et al.”

This is a false comparison, Monetary Sovereignty vs. monetary non-sovereignty. The two are diametrically opposed, which also is why your debt can be overwhelming while the federal government’s never is.

Being Monetarily Sovereign, the federal government has the infinite ability to create dollars just by pressing computer keys.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

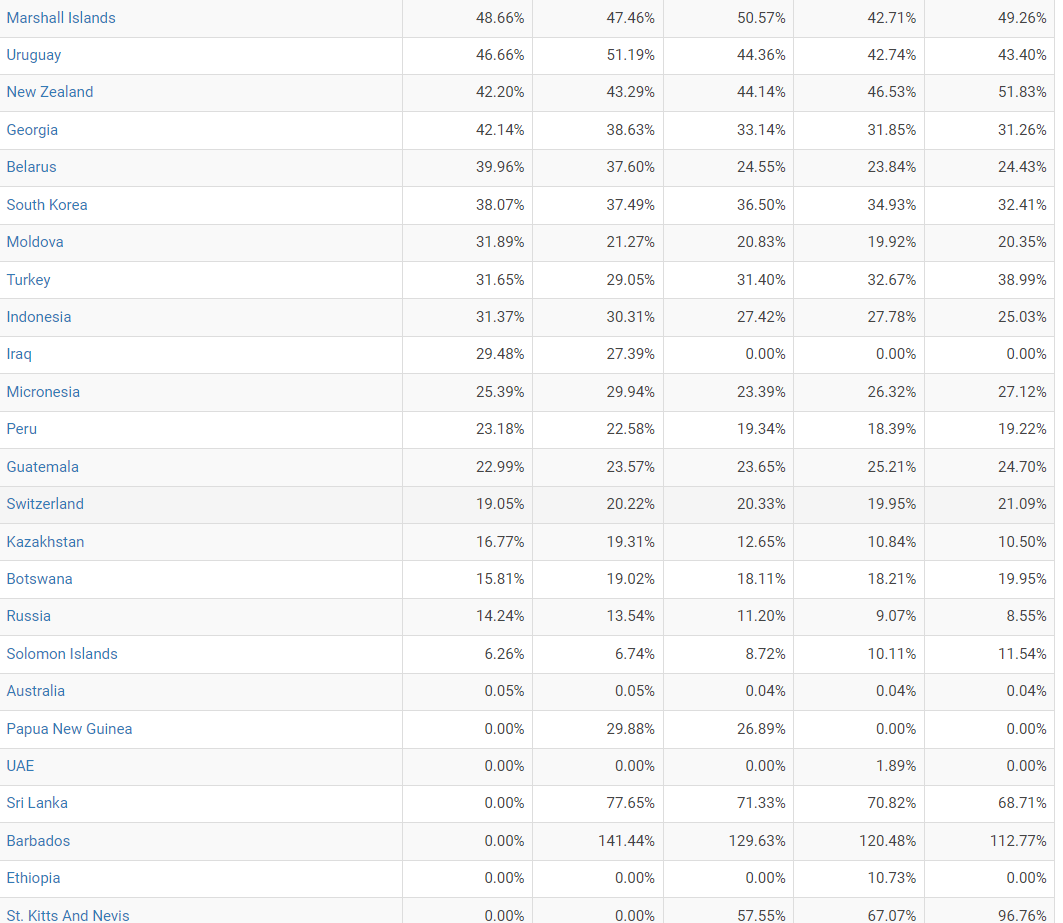

Finally: The proof is in the results. If the CRFB were telling the truth, you would see the nations with the highest Debt/GDP ratio having what the CRFB calls a “financially unstable trajectory,” while the countries with the lowest Debt/GDP ratio would be the most “financially stable.”

Study this list from Macrotrends, and using it as a guide, tell me which nations are more financially stable and which are less financially stable:

Was Jamaica more or less financially stable than Japan and the United Kingdom? What about the United States vs. Russia? South Korea vs. St. Lucia? The U.K. vs. Jordan?

As you can see, Debt/GDP means nothing concerning “financial stability.” The whole concept is a giant lie foisted upon the American public by mouthpieces for the rich.

Those are the facts. The federal “debt” (that isn’t a debt of the federal government) grew eleven thousand percent since 1951. Is today’s America more financially unstable than it was after WWII?

And there’s this:

If a high Debt/GDP ratio caused inflation, one would expect some correspondence between the peaks and valleys of Debt/GDP and inflation. No such parallel exists.

What does cause inflation?

The price of oil, not the Debt/GDP ratio, is the prime driver of inflation. The peaks and valleys of the Oil Price / Inflation ratio correspond.

The RBFB’s B.S. continues:

Perhaps most troubling is the effect of these changes on interest spending.

Under CBO’s baseline, interest costs were already projected to triple from roughly $400 billion in 2022 to $1.2 trillion in 2032.

As a result of higher debt and higher interest rates, we now expect them to rise to $1.3 trillion in our baseline scenario, $1.4 trillion in our intermediate scenario, and $1.6 trillion in our high-cost alternate scenario.

As a share of the economy, interest costs would be in uncharted territory. In all of American history, federal interest costs have never exceeded 3.2 percent of GDP.

We project interest costs will reach 3.4 percent of GDP by 2032 under our baseline scenario, 3.9 percent under the intermediate alternate scenario, and 4.4 percent under the high-cost alternate scenario.

And why is this a problem? It isn’t. The U.S. federal government never, never, never can run short of dollars to pay interest. And those dollars go right into Gross Domestic Product.

Federal interest payments add directly to GDP. They stimulate economic growth. They make the private sector richer.

GDP = FEDERAL SPENDING + NON-FEDERAL SPENDING + NET EXPORTS

Objecting to federal spending is objecting to GDP growth. Why does the CRFB object to that?

There is a reason, which I will get to shortly.

At the same time as inflation is surging and interest rates are rising, our new projections show that the United States faces an unsustainable fiscal outlook.

Liars like the CRFB have called the federal debt “unsustainable” (and a ticking time bomb) every year since the 1940s. Yet, here we are. Sustaining. We are “sustaining” an eleven thousand percent increase in federal “debt” (that isn’t debt) very nicely, thank you.

Year, after year, for 75 years, liars, fakers, and fear-mongers have been wrong. Again. Again. Again. How stupid do we have to be to keep believing the same lie when every scary prediction fails?

We laugh when the Peanuts character Lucy keeps pulling the football away, and Charlie Brown keeps believing. But we are the Charlie Browns, the CRFB, and all the other lying pundits are Lucy. They keep “pulling the football away,” and we keep believing that next time . . . but next time never comes.

And the beat goes on: The lies just keep coming:

The following is a statement from Maya MacGuineas, president of the Committee for a Responsible Federal Budget:

We are asking lawmakers to take one small step towards fiscal responsibility and agree there should be no new borrowing for the remainder of 2022. There is not one single economic justification to borrow rather than pay for any new priorities.

This is only 46 days, and it will be good practice for politicians to break their addiction to debt. Those who are being negatively affected by high levels of inflation – as in, all of us – should ask any policymaker who votes for new borrowing why they are choosing to make inflationary conditions worse rather than better.

The last thing this country needs is a Christmas Tree package full of unpaid-for tax breaks and spending hikes.

Any policymaker who votes for new borrowing instead of paid-for legislation under these economic conditions is not taking the hardships they are creating on working families seriously enough.

What’s wrong with it? It’s all a lie.

First, the U.S. government never borrows dollars. Why should it, given that it can create dollars simply by pressing computer keys.

Statement from the St. Louis Fed:

“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

That thing erroneously called “borrowing” is the acceptance of deposits into T-security accounts, and the federal government never touches those dollars. It’s like accepting deposits into safe deposit boxes. Is that bank borrowing?

Second, tax breaks are nothing more than dollars not taken from the economy. Tax breaks are economically stimulative. Leaving money in the private sector is the only way the economy can grow.

Third, no one ever pays for tax breaks. The only thing paid for is taxes, which take growth dollars out of the economy.

Fourth, all legislation that requires spending dollars is “paid for.” The federal government pays all its bills by creating new dollars ad hoc. It never fails to pay, despite all the hand-wringing about “unsustainability.”

And finally, federal deficit spending never causes inflation. The sole cause of all inflations and hyperinflations throughout history is the scarcity of critical goods and services, usually oil and food, but additionally, computer chips, shipping, rare earths, labor, water, etc.

What caused these shortages? Not federal spending. Federal spending didn’t cause the oil shortage, or the food shortages, or the lumber shortage. Primarily, COVID caused the shortages that caused inflation.

Before COVID, we had massive annual deficit spending and near-zero inflation.

WHY DO THEY LIE, AND WHY DO WE BELIEVE?

Some in the CRFB, the media, economists, and politicians may lie out of ignorance. But many lie because they are bribed by the rich to lie.

The rich bribe the media via advertising dollars and ownership. The rich bribe the politicians via campaign contributions and promises of lucrative employment later. The rich bribe the economists via university contributions and promises of lucrative jobs in think tanks.

The CRFB is supported by rich people who want nothing more than to see benefits to the middle and the poor cut.

Raising taxes or cutting federal spending are recessionary steps that affect middle- and lower-income people. This is particularly true because the cuts always focus on Medicare, Social Security, Medicaid, and other benefits for those who are not rich.

Those cuts widen the Gap between the rich and the rest. Widening the Gap makes the rich richer. The Gap is what makes the rich rich.

In Summary

The Debt/GDP ratio is comparable to a Contents-of-Bank- Safe-Deposit-Boxes / Bank Spending ratio. It’s a meaningless nonsense ratio that predicts nothing, demonstrates nothing, and reveals nothing but the ignorance of those who quote it.

The ratio tells you nothing about the health of a nation’s finances or its ability to pay its obligations. It is a ratio quoted by those who are ignorant of economics or are lying about economics. No other alternatives.

To paraphrase, “There are lies, damned lies, and the Federal Debt / GDP liars, the damnedest liars of all.

May the Debt/GDP liars’ spawn be forever cursed.

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

AS usual, you are spot on Rodger. Thanks for all you do to keep us informed and sane.

LikeLike

I’m still hoping to see the nation’s “aha” moment before I die.

LikeLike

Not sure we will ever have an “aha” moment, as Monetary Sovereignty is not intuitive for most people. At some point we may reach some critical mass of understanding, which will gradually shift the narrative, but I am not holding out for an “aha” moment.

As da Vinci stated: “There are three classes of people: those who see, those who see when they are shown, and those who cannot see. Unfortunately, based on my personal experience in trying to explain Monetary Sovereignty to others, I fear the last class of people represent a majority of the population.

LikeLike

Or perhaps they can see, but they are being influenced by the wrong people.

LikeLike

How much federal taxation is necessary to ‘drive’ our sovereign currency?

LikeLike

Taxes are what “drive” our currency.

LikeLike

I never have found out what “drive” means, though Randy Wray uses that term frequently. I suspect it means, “create demand for.”

Contrary to what some MMTers might tell you, the answer is $0. Bitcoin is one example. Randy Wray and Warren Mosler invented the UMKC Buckaroo, which does charge a quasi-tax in that students must pay 20 buckaroos to get their grades, and buckaroos are paid for community service.

According to Huffpost (https://www.huffpost.com/entry/the-umkc-buckaroo-a-curre_b_970447), Buckaroos are traded for $15 each, which means poor kids labor, and rich kids buy their labor. It’s a realistic, though a sad lesson, that parallels the real world.

In any event, the quasi-tax supposedly “proves” that taxes “drive” money, though there is a catch. The whole purpose of buckaroos is to get students to work for a fixed rate of $15 per hour, no matter what the job. If the Buckaroos were a free currency, like the U.S. dollar, payments would be higher, and a tax would not be necessary.

The article says so: “The students recognize that if the UMKC decided to buy other goods and services with buckaroos from willing sellers, they could do that, but that said purchases would tend to reduce the student labor that the community service providers would attract. The students fully recognize that if the UMKC ends the 20 buckaroo tax, the buckaroo will have no further value.” (Because they only can be used to pay for grades.)

In short, we have an artificial situation in which buckaroos are nothing like dollars, which by law, can be exchanged for anything, and do not need taxes to “drive” them. The ability to buy anything with them (i.e. acceptance which is driven by the full faith and credit of the U.S. government) “drives” them.

LikeLike

In short, MMT would drive the economy by “taking & taxing” forcing a need for employment to pay them. But MS drives the economy from a sense of abundance and responsibility. The reaction, as we already know from conducted experiments, will be in line with human nature. People will give back to the system by finding work or volunteering in spite of what the rich/powerful keep saying about laziness and getting something for nothing. The rich don’t want the truth to be known. They know MS will close the Gap and destroy their commonly accepted argument despite very embarrassing proof to the contrary.

LikeLike