Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

============================================================================================================================================================================================================================================================

Before I go on a short vacation — the purpose of which is to demonstrate how we in the upper 10% income group are (per the Republicans) hard working “makers,” sweating and straining at a Margaritaville poolside, while you “takers” in the lower 10% income group are living in crime-ridden comfort and royalty on your $147 per month food stamps — I will leave you with a few more comments by a fake Nobel prize winner.

(Bernie) Sanders has made restoring Glass-Steagal and breaking up the big banks the be-all and end-all of his program.

That sounds good, but it’s nowhere near solving the real problems.

The core of what went wrong in 2008 was the rise of shadow banking; too big to fail was at best marginal, and as Mike Konczal notes, pushing the big banks out of shadow banking, on its own, could make the problem worse by causing the risky stuff to “migrate elsewhere, often to places where there is less regulatory infrastructure.”

Funny how, soon after ideology is expressed, nasty facts get in the way:

Wells Fargo to Pay $1.2 Billion to Settle Lending Practices Claims

The Justice Department argued that Wells Fargo had lent recklessly and relied on the federal government to pick up the tab when lessees defaulted.

“The $1.2 billion settlement with Wells Fargo is the largest recovery for loan origination violations,” said Housing and Urban Development Secretary Julián Castro. “This monetary figure can never truly make up for the countless families that lost homes as a result of poor lending practices.”

Potential claims go back as far as 15 years in some cases.

And then there’s this as listed in the British Paper, the Times:

$1.9bn –HSBC, money-laundering lapses $1.5bn –UBS, Libor rigging $920m –JPMorgan, trading scandal $780m –UBS, aiding tax fraud $667m –Standard Chartered, breaching sanctions $619m –ING, breaching sanctions $612m –RBS, Libor manipulation $550m –Goldman, misleading investors $536m –Credit Suisse, breaching sanctions $500m –ABN Amro, breaching sanctions $451m –Barclays, Libor manipulation

And this:

Biggest Bank Settlements

The settlement by BNP Paribas in the U.S. sanctions case for nearly $9 billion ranks among the biggest ever among banks since the early 2000s. It is the biggest-ever fine levied against a bank for violating U.S. economic sanctions.

And this:

Bank of America Offers U.S. Biggest Settlement in History Over Toxic Mortgage Loans — more than $16 billion

After months of lowball offers and heels dug in, it took only 24 hours for Bank of America to suddenly cave in to the government, agreeing to the largest single federal settlement in the history of corporate America.

Strange that those TBTF banks, while agreeing to ginormous settlements for their nefarious activities, were only “marginal” as Krugman claims.

(One can only wonder how many billions the banks would have had to pay if their misdeeds had not been “marginal.”)

But of all the nutty Krugman comments, this is my favorite:

“(Breaking up the TBTF) banks could make the problem worse by causing the risky stuff to “migrate elsewhere, often to places where there is less regulatory infrastructure.

Get it? You don’t want to pass or enforce any laws against criminality, because then criminals will go where there is less regulation.

Is Krugman too thick to realize that statement could be made about every law that ever has been passed?

No, don’t be fooled by his writing. He’s no dummy. He is just so pro-Clinton, anti-Sanders, he has lost all sense of shame.

Let’s be clear: I believe Hillary is far superior to the defectives now being offered by the Republicans. She could turn out to be one of the most effective Presidents since Lyndon Johnson.

But Krugman apparently will blather any ridiculous notion, idea, or comment to support Hillary over Bernie, let the facts be damned.

My guess: There actually was a time when Krugman cared about his reputation, but that time long has passed.

Rodger Malcolm Mitchell

Monetary Sovereignty

===================================================================================

Ten Steps to Prosperity:

1. Eliminate FICA (Click here)

2. Federally funded Medicare — parts A, B & D plus long term nursing care — for everyone (Click here)

3. Provide an Economic Bonus to every man, woman and child in America, and/or every state a per capita Economic Bonus. (Click here) Or institute a reverse income tax.

4. Free education (including post-grad) for everyone. Click here

5. Salary for attending school (Click here)

6. Eliminate corporate taxes (Click here)

7. Increase the standard income tax deduction annually Click here

8. Tax the very rich (.1%) more, with higher, progressive tax rates on all forms of income. (Click here)

9. Federal ownership of all banks (Click here and here)

10. Increase federal spending on the myriad initiatives that benefit America’s 99% (Click here)

The Ten Steps will grow the economy, and narrow the income/wealth/power Gap between the rich and you.

========================================================================================================================================================================================================================================================================================================

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

![]()

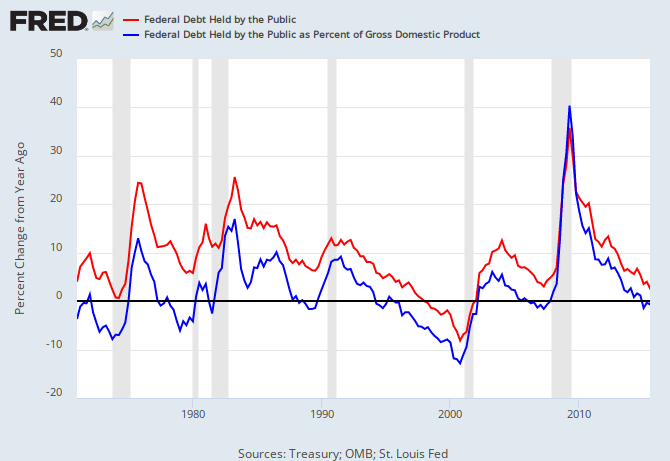

THE RECESSION CLOCK

Recessions begin an average of 2 years after the blue line first dips below zero. A common phenomenon is for the line briefly to dip below zero, then rise above zero, before falling dramatically below zero. There was a brief dip below zero in 2015, followed by another dip – the familiar pre-recession pattern.

Recessions are cured by a rising red line.

Vertical gray bars mark recessions.

As the federal deficit growth lines drop, we approach recession, which will be cured only when the growth lines rise. Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

————————————————————————————————————————————————————————————————————————————————————————————————-

Mitchell’s laws:

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money.

•The more federal budgets are cut and taxes increased, the weaker an economy becomes..

•No nation can tax itself into prosperity, nor grow without money growth.

•Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

•A growing economy requires a growing supply of money (GDP = Federal Spending + Non-federal Spending + Net Exports)

•Deficit spending grows the supply of money

•The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

•The limit to non-federal deficit spending is the ability to borrow.

•Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

•The single most important problem in economics is the Gap between rich and the rest..

•Austerity is the government’s method for widening the Gap between rich and poor.

•Until the 99% understand the need for federal deficits, the upper 1% will rule.

•Everything in economics devolves to motive, and the motive is the Gap between the rich and the rest..

MONETARY SOVEREIGNTY