The Federal Reserve fights inflation by raising interest rates. Here is an amalgam of what several sources say”

The Fed’s primary tool it can use to battle inflation is interest rates. It does so by setting the short-term borrowing rate for commercial banks, and then those banks pass it along to consumers and businesses.

That rate influences everything from interest on credit cards to mortgages and car loans, making borrowing more expensive.

Inflation is a general increase in prices. So, how does making borrowing more expensive affect inflation? Shouldn’t an increase in borrowing costs make products and services more expensive rather than less?

The answer is “Yes.” Interest is a cost that manufacturers, farmers, and services must add to prices, so they can make a profit.

The Fed aims to make borrowing more expensive so that consumers and businesses hold off on investing, thereby cooling off demand and bringing prices back in check.

How does reducing investments “cool off demand”?

Higher interest rates might reduce the demand for large consumer items, like houses and cars. But does reducing investments reduce your demand for food? Does it reduce your need for oil? For clothing?

Think of everything you buy? Which of those things will you buy less because interest rates went up? Probably, none.

The Fed believes that inflation is caused by (in their words) “an overheated economy.” But what is an overheated economy? Here is what the Bing Artificial Intelligence (AI) says:

An overheated economy is when the economy grows too fast. An overheated economy reaches the limits of how much output it can produce to meet the demand from consumers and businesses, as there are minimal unused resources.

In short, inflation is a supply problem. The Fed’s “overheated economy” is one where supply can’t meet demand.

The Fed’s inflation cure is to increase interest rates which reduces business investment and supply.

The Fed hopes that increasing interest rates will reduce demand more than supply, but what do we call reduced demand? Recession.

If the Fed’s approach is correct, we should see two things that we do not see:

We should see that rising interest rates do not cause recessions

We should see that falling interest rates do not cure recessions

We should see that rising interest rates precede (i.e., cause precedes effect) falling inflation.

Look at the graph below, and you will see the opposite. In fact:

Rising interest rates lead to recessions (vertical gray bars).

As for #3, rising inflation precedes interest rate increases because the Fed reacts to inflation increases by raising rates.

Then afterinflation begins to come down, the Fed lowers rates.

While the Fed claims that rising interest rates cause inflation to fall, rising inflation leads to higher interest rates.

Imagine the car going faster causes the driver to press the gas pedal down further. Inflation causes the Fed to increase interest.

What isthe cause and cure for inflation if interest rate increases are recessionary and don’t cure inflation?

The cause and cure for inflation lie in the supply of oil.

The supply of oil is reflected in its price (black line). The shortages of oil parallel inflation (red line).

As opposed to common knowledge, the Fed’s interest rate increases do nothing to reduce inflation, which parallels oil prices and is determined by oil supply.

To the degree interest rate increases may reduce the oil demand, they cause recessions.

Until renewables become a more significant part of our energy supply, a reduced need for oil will signal recession.

Congress and the President have assigned the Fed the task of controlling inflation. But though the Fed doesn’t have the tools to manage inflation, Congress and the President do.

Short term, there should be federal incentives for drilling and refining oil. Longer term, the efforts to reduce oil usage via renewables should be accelerated with federal subsidies and tax credits.

More significant incentives for electric car purchases and usage, incentives for solar, wind, geothermal, and nuclear power production would do far more to reduce inflation, without a recession, than interest rate increases.

Congress and the President don’t want the inflation responsibility. The Fed does want the responsibility because it gives them greater power.

Currently, the Fed is like the child sitting in the back seat, furiously spinning his toy steering wheel. He thinks he steers the car, just as the Fed believes it steers the economy, when Congress, the President, and the world’s oil producers steer it.

The Fed’s money tinkering is but a blip on the screen.

Curing shortages, particularly oil shortages, but also renewable energy, food, computer chips, transportation, vital chemicals, and other shortages are needed to control inflation.

Here’s why: The most crucial question in economics is: “Can the federal government run short of money?”

Most economists will answer something on the order of, “The government always can print more dollars.”

While technically that is not correct — the government prints dollar bills, which are titles to dollars, not dollars in themselves — the concept is correct.

The U.S. federal government cannot unintentionally run short of dollars. With that fundamental truth in mind, logic dictates that:

The U.S. government does not rely on your tax dollars. It simply could “print” all the dollars it spends, and in fact, that is what it does.

Therefore, the U.S. government has no financial need to levy federal taxes.

There is no financial need for the federal government to run a balanced budget.

Federal deficits and debt are not a burden on the federal government or on federal taxpayers

Since the federal government cannot unintentionally run short of dollars, no federal agency can run short of dollars unless the federal government wants that to happen.

Medicare and Social Security are among the hundreds of federal agencies that cannot run short of dollars unless Congress and the President want that result.

The so-called Medicare and Social Security “trust funds” are not real trust funds; they have no financial purpose. The federal government can and does support all federal agencies by creating dollars ad hoc.

Medicare for All, Social Security for All, College Tuition for All, Housing Support for All, Food for All, etc., are well within the federal government’s ability to fund without levying a penny in taxes.

If you can find an error in the above logic, please let me know.

Why, then, does the government collect taxes?

Why does it threaten bankruptcy for Medicare and Social Security?

Why the concern about the federal deficit and debt?

The fundamental financial purpose of federal taxes is to control the economy by taxing what the government wishes to limit and by giving tax breaks to what the government wishes to encourage and reward.

Sadly, the government taxes — i.e., wishes to limit — your income, your healthcare, your retirement, and your other benefits, while it hopes to encourage and reward — i.e., give tax breaks to — the rich and their accumulation of wealth.

That is why the very rich pay a much lower percentage of their income and wealth as taxes than you do.

Donald Trump’s negligible tax payments are but one example.

While the economists generally admit that the federal government cannot become insolvent, they take their lead from the rich, who provide two fallback excuses for not supporting the middle classes and the poor:

Excuse #1: “If we support the middle and the poor by providing health care insurance, retirement insurance, housing aid, food aid, and college aid, the middle and the poor will refuse to work, destroying the economy.”

The tacit claim is that the not-rich are lazy takers who, lacking human aspirations, are not interested in improving their lives via labor but are content to wallow in their own poverty.

Never mind that the poor and middle classes labor much harder than do the rich, who are the real lazy takers.

Excuse #1 is part of the “the poor deserve their poverty, and we rich deserve our wealth” meme.

It is a subset of the white supremacy doctrine — part of the notion that “it was not luck that got us where we are but rather our natural superiority” — part of the “give the poor a few dollars, and they will those dollars to buy drugs and gamble.”

Excuse #2: “Federal spending can cause inflation, which will destroy the economy.”

We can all agree that when something is in short supply, its price rises so that many prices rise when many things are in short supply.

That’s called “inflation.”

Today’s inflation is caused by COVID-related short supplies of oil, food, computer chips, lumber, housing, and labor.

Does federal spending cause these shortages? The reality is that only a very small percentage of federal spending is for the purchase of these things.

The vast majority of federal spending goes to people. Federal dollars for Medicare and other healthcare, Social Security, poverty aids, and even the military comprise nearly all of the federal government’s spending.

Only a tiny percentage goes for the purchase of goods, and even that percentage is largely labor-related.

So, when economists claim that federal spending causes inflation, they really claim that the American people receive too much money.

And further, when people have more money, they spend it on already scarce items, thus causing inflation.

Carried to its logical end, the economists claim that preventing and curing inflation requires impoverishing the middle classes and the poor.

The economists want you to have less money for driving your car, heating your house, buying your food, affording suitable housing, owning a TV, or going to college.

And they want businesses to devote less money to hiring people.

FICA and business-provided healthcare insurance are employment costs discourage hiring whilereducing net wages.

Suppose the government did not require employers and employees to pay FICA and did not encourage companies to provide healthcare insurance (via tax deductions and the lack of Medicare for All). In that case, businesses could hire more people at higher net wages.

The entire anti-inflation argument is based on the poor and middle classes receiving poorer health care, food, housing, education, and net wages.

There can be no argument about the federal government’s unlimited ability to create its own sovereign currency. So, you might think the entire Big Lie about federal deficits being “unsustainable” devolves into inflation.

But that Big Lie is just a cover for a more profound lie, based on Gap Psychology, the human desire to widen the income/wealth/power gap below and to narrow the gap above.

The Gap is what makes one rich. Without the Gap, no one would be rich; we all would be equal. And the wider the Gap, the richer the rich.

A man owning a million dollars would be rich if everyone else owned only a thousand dollars, but he would be poor if everyone else owned ten million dollars.

The richer always wish to be more prosperous. They want the Gap below them to grow wider. So, they bribe our sources of information to convince us that the government should not provide Gap-narrowing benefits.

They bribe the media via ownership and advertising dollars. They bribe the politicians via campaign contributions and promises of future employment.

They bribe university economists via university contributions and employment in think tanks, which is why economists never want poverty to be cured.

They like bribes.

Everyone, from layperson to self-described expert, is fed the same Big Lie: “Federal finances are like personal finances.”

That lie includes misleading statements: The federal government should live within its means and run a balanced budget, deficits and debt are unsustainable, federal taxes fund federal spending, and federal expenditures causes inflations.

The facts are:

The federal government, having the infinite ability to create dollars, has no “means” to live within.

Running a balanced federal budget always leads to recessions and depressions

Federal taxes not only don’t fund federal spending but federal tax dollars are destroyed upon receipt by the Treasury.

All inflations are caused by shortages of critical goods and services, usually oil or food.

Federal spending creates economic growth and even can cure inflations by curing shortages.

Here’s the evidence:

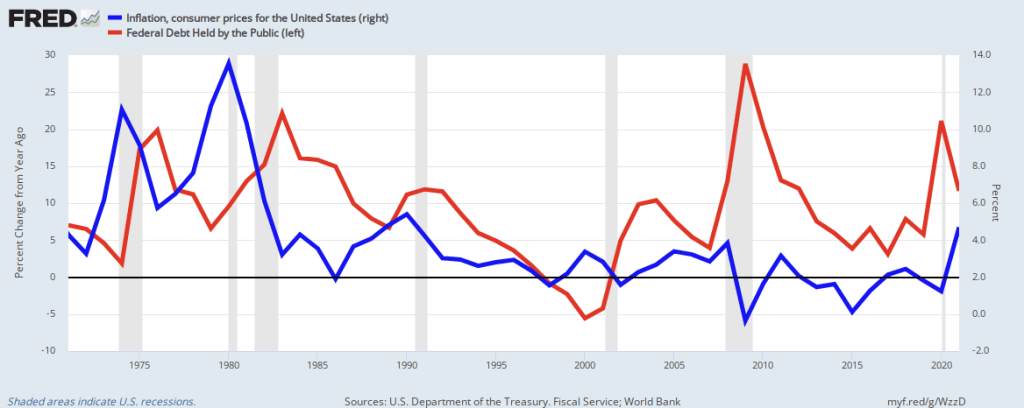

This graph demonstrates that recessions (vertical gray bars) occur not just when federal debt (red) shrinks but even when federal debt doesn’t grow enough.

Here is a list of periods in which the federal debt actually has shrunk:

U.S. depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

A growing economy requires a growing supply of money.

Federal deficits pump money into the private sector, aka “the economy,” and by formula, increase economic growth (GDP=Federal Spending+Non-federal Spending+Net Exports.)

You and everyone else pay federal taxes with dollars taken from the M1 money supply measure , which includes currency in people’s pockets or the M1 money supply measure which includes currency that is in people’s pockets or in checking accounts.

There is no money supply measure for the federal government’s dollars because the government has the infinite ability to create dollars.

It has an infinite supply of money.

Former Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Former Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Quote from Ben Bernanke when he was on 60 Minutes:Scott Pelley: Is that tax money that the Fed is spending?Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Thus, all those M1 money supply tax dollars disappear from any money supply measure. They effectively are destroyed.

The federal government creates ad hoc dollars every time it pays for something. And as for the myth that federal deficit spending causes inflation, look at this graph:

If federal deficit spending caused inflation, the peaks and valleys of the red line (changes in federal debt) would correspond to the peaks and valleys of the blue line (inflation). There is no such correspondence.

If you’re looking for something that does correspond to inflation, look at this graph.

Oil prices (silver) correspond with inflation (blue). Inflations are caused by shortages.

Your major sources of information, the media, politicians, and university economists have been bribed to believe and to disseminate the Big Lie that federal finances resemble personal finances.

In fact, the two could not be more different.

The federal government is Monetarily Sovereign; you, the states, counties, cities, and businesses are monetarily non-sovereign.

The federal government can create unlimited numbers of dollars; you, the states et al, cannot create unlimited dollars

The federal government destroys all the dollars it receives; you do not.

The federal government never unintentionally can be insolvent; you can become insolvent if you do not have sufficient dollars to pay your creditors.

The federal government never borrows dollars; you might have occasion to borrow.

The federal government can cure inflations, not by raising interest rates (which exacerbates shortages), but by spending to alleviate shortages.

For instance: To lower the price of oil, the government could financially support oil exploration and processing, and/or invest in renewable energy.

To lower the price of food, the government could financially support farming and food production R&D.

To ease the price of labor, the government could eliminate the FICA tax while providing Medicare for All (relieving businesses of this financial obligation).

To lower the prices of electronics, the government could invest in computer chips and electronic R&D.

In short, reducing inflation actually requires additional government spending, not less.

Any time you read or hear someone equating federal finances with personal finances, you will know they are lying or ignorant about economics.

Similarly, any time you read or hear someone saying federal debt or deficits are “unsustainable,” they, too are lying or ignorant.

If you have played the board game Monopoly, you know the Bank mimics the federal government in that it cannot run out of money. By rule, the Bank is Monetarily Sovereign.

The players comprise the “economy,” and they do not need to worry about the Bank’s deficits or its debt being “unsustainable.”

The Bank always is able to pay $200 for passing “GO.”

If you find Monetary Sovereignty puzzling, just think of Monopoly. That may help you visualize the reality of the U.S. economy.

The purpose of the Big Lie is to widen the Gaps between richer and poorer, and more specifically, between the very rich and the rest of us.

Economist charlatans never want poverty cured because the cures would reveal their ignorance, deception, and/or their receipt of bribes from the rich.

THE PROBLEM: ECONOMIC MYTHS HINDER ECONOMIC GROWTH

Myth #1: The federal debt and deficits are too high. The fact:

Myth #2: Federal debt as a percentage of Gross Domestic Product is too high and unsustainable. The fact:

The fact: As the percentage of federal debt to GDP rises, real (inflation-adjusted) GDP per person rises. The conclusion: The more “debt” the federal government has, the wealthier are we Americans.

Myth #3: Inflation is too much money chasing too few goods and services. The fact:

Myth #4: Federal deficit spending causes inflation. The fact:

There is no relationship between federal government deficit spending (red) and inflation (blue).

Myth #5: Oil prices aren’t the primary cause of inflation. The fact:

Oil shortages are the primary cause of inflation. When oil prices go up, inflation goes up; when oil prices go down, inflation goes down.

While oil shortages cause oil price increases, which in turn cause price increases in most other goods and services, these price increases are exacerbated by scarcities in the other goods and services.

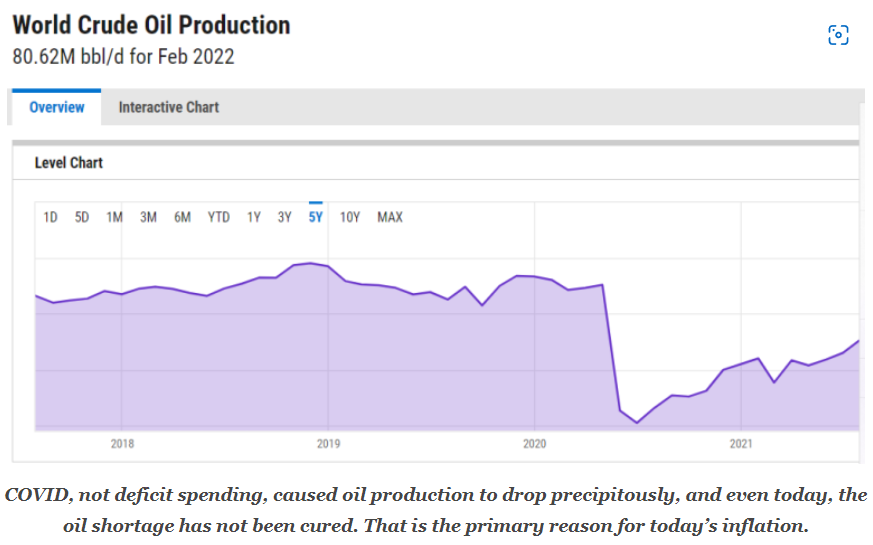

Myth #6: COVID was not an important cause of inflation. The fact:

Oil production dropped dramatically in 2020, at exactly the time when COVID came to be rampant throughout the world.

When oil production drops, the resultant shortage causes prices to rise, which causes virtually all other prices to rise.

COVID-caused scarcities such as computer chips, cars, lumber, homes, food, shipping resources, baby formula, and labor exacerbated these other price increases.

THE SOLUTION: FEDERAL DEFICIT SPENDING TARGETED AT GROWING THE ECONOMY AND CURING INFLATIONS BY ELIMINATING SHORTAGES.

Unlike state and local governments, the federal government is Monetary Sovereign. It has the unlimited ability to create its own sovereign currency, the U.S. dollar.

The federal government never unintentionally can run sort of dollars.

Alan Greenspan:“A government cannot become insolvent with respect to obligations in its own currency.”

Ben Bernanke:“The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Even if all tax collections totaled $0, the federal government could continue spending forever.

The economy, as measured by GDP, is a spending number, a formula for which is:

Federal Spending + Non-federal Spending + Net Exports = GDP

Therefore, by formula, adding dollars to the economy via federal spending increases GDP.

This leads to the question, will this cause inflation?

As we have seen in Myths #4, 5, and 6, inflation is not caused by federal deficit spending but rather by shortages of critical goods and services, most often oil (energy)

To eliminate that shortage, increase federal support for the energy sector.

Oil drilling & refining in the short term

Electric cars, buses, and trains.

Electric homes, factories, farms, and cities

Solar energy

Nuclear energy

Geothermal energy

Wind energy

Hydrogen energy

Research & development of other non-carbon energy sources

Additionally, there should be financial support for other scarce products and services:

Food shortage: Farm aid to increase farm output and the development of more productive crops.

Shipping shortage: Aid for improved ports, workers, trucks, and driver training. Improved national railroad system.

Housing shortage: Aid for housing, the lumber industry, and training for carpenters, electricians, plumbers, etc.

Shortages of cars, trucks, planes, and electric/electronic machines: Support the production of improved computer chips.

Shortage of health providers: Aid for medical training, hospital building, pharmaceutical R&D

Labor shortage: Eliminate FICA, which would help businesses pay more for workers. Also, provide free, comprehensive Medicare for every man, woman, and child in America, thus removing that expense from companies.

Other shortages: Eliminate duties on scarce items.

In summary, all inflations are caused by shortages, and the prevention/cure of inflations is to cure those shortages. Raising interest rates, as the Fed now is doing, will attempt to fix inflation via recession, a poor cure.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps: Ten Steps To Prosperity:

For over a decade, we have experienced powerful economic growth and low inflation, for which the Congress and Presidents Trump’s and Biden’s administrations have taken credit.

Now, COVID has changed everything. Growth has leveled off and inflation has soared.

Economic growth is shown as the Dow Jones Composite Average (blue). Inflation is shown as the Consumer Price Index for All Urban Consumers (red).

So, the bad news has everyone wrongly looking to the Federal Reserve for a solution and to blame.

Solving, for instance, a medical problem, requires dealing with the symptoms or the causes. Dealing with symptoms works when the symptoms are relatively mild, but when symptoms are severe, one must determine the causes, and address them.

The symptom of a mild ache temporarily can be addressed with asperin. But if the pain is severe, and the cause is a broken leg, aspirin may not be the best solution.

In that vein, I submit that slow growth and inflation are not problems in themselves, but rather are symptoms of more serious underlying problems that beg for solutions.

Unfortunately, Congress has stepped back and claimed that the problems must be interest rates that are too low, and money creation that is too high, and therefore the Fed is officially tasked with curing what ails us.

The Federal Reserve has been assigned a task by Congress that is easy to describe, yet fiendishly difficult to achieve. It’s known as the dual mandate: to achieve both price stability and maximum employment.

“Price instability” (in this case, inflation) is a symptom. Inflation is caused by shortages of key goods and services, which are not controlled by the Fed.

“Maximum employment” (a proxy for economic health) also is not under the Fed’s control.

The Fed’s tools are interest rates and to a slight degree, money supply. Neither tool cures shortages. While money supply does affect economic health, the Fed has much less control over money supply than does Congress.

In short, Congress and the President have total control over the Fed’s dual mandate, control the Fed does not have.

Nevertheless, the politicians find the Fed a convenient whipping boy for any financial problems, while claiming credit for any financial successes.

The Fed goes along with the ruse, perhaps because it enjoys the appearance of power the dual mandate provides.

The formal, legal language of the mandate comes from the Federal Reserve Reform Act of 1977, which says the central bank must steer credit and money supply “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.“

The part about “moderate long-term interest rates” hasn’t been a problem in recent decades, which leaves open the question of what counts as “maximum employment” and “stable prices.” The Fed has a great deal of leeway to interpret those goals.

How it works: The central bank now formally defines price stability as an inflation of 2% per year, as measured by the core personal consumption expenditures price index.

This is the part where the Fed is failing. Inflation was up 5.4% over the 12 months ended in February, far overshooting the central bank’s target, though by less of a margin than the more widely covered Consumer Price Index.

The definition of “maximum employment” is more squishy. Median official Fed estimates show the longer-run unemployment rate is 4%, though policymakers also emphasize a lot of uncertainty around how low unemployment can go without sparking excessive inflation.

Though “policymakers” (Congress and the President) recognize that low unemployment, i.e., a shortage of labor, is one of the shortages that lead to inflation, they still insist that the Fed use its interest rate and money-creation tools, rather than curing the shortage.

Our Monetarily Sovereign federal government has neither the need for, nor the use of tax dollars. It creates all the dollars it uses, ad hoc, by paying bills.

So, for example, eliminating the useless and regressive FICA taxwould relieve employers of a significant employment cost while allowing for substantial salary increases at no cost.

Additionally, if the federal government offered Medicare for All, with no deductibles, employers would be relieved of that cost, too, further allowing them to raise salaries at no cost while attracting more employees.

Putting more dollars into employees’ pockets, at no cost to employers, is one good way to encourage more people to go to work, i.e reduce the labor shortage that is one cause of today’s inflation.

The view at the Fed at the moment is that the job market is too hot — “tight to an unhealthy level,” as Chair Jerome Powell put it in his news conference last month.

Between the lines: Powell and his colleagues are hoping the labor market is so robust they can slow demand just enough that labor shortages and inflationary pressures abate — but employers keep hiring, and the jobless rate doesn’t rise much.

“Slow demand” is another term for “start a recession.” It’s based on the belief that the opposite of “inflation” is “recession,” which is just plain ignorant economics.

The opposite of inflation is deflation, which is accomplished by moving away from shortages toward surpluses.

Slowing demand, which the Fed wants to instigate by cutting the money supply, always leads to recessions if we are lucky and depressions if we are not.

Every recession (vertical gray bar) is preceded by reductions (diagonal lines) in federal deficit spending growth (blue line).

Fed President Mary Daly said in a recent speech. “It was critical to assist the economy in recovering the job losses that occurred early in the pandemic, and it is now critical to stem what has been a longer-than-expected run of high inflation.”

Ms. Daly may claim that the Fed assisted the economy to recover from job losses, and now is in a position to stem inflation.

That is like the child sitting in the back seat of a car with his toy steering wheel, and claiming that he is driving the car.

In reality, the economy recovered from job losses because the President and Congress pumped in trillions of stimulus dollars.

The inflation can be stemmed, without starting a recession, only by relieving the COVID-based shortages ofoil, food, computer chips, lumber, labor, and many imported goods.

The shortage of oil can be addressed by federal funding for drilling, drilling materials, labor, solar energy, geothermal energy, wind energy, electric cars, etc.

What’s next: Over the coming months, with supply chains stabilizing, fiscal stimulus fading, and the Fed doing its job of slowing demand, there is good chance inflation will start to come down.

Since when is “slowing demand” (i.e. causing slower economic growth) the Fed’s job? Why is economic growth the devil, when inflation is the real devil? The two are completely different, as we can, and often have had one without the other.

When we have economic growth without inflation, that is termed “a healthy economy.” When we have inflation without economic growth, that is termed “stagflation,” which easily transitions to full blown recession and depression.

Thus, there is a strong chance that the Fed’s “job of slowing demand” will cause a recession.

The question is whether it comes down quickly enough and decisively enough to give the Fed comfort that it doesn’t need to cause an outright crash in the job market to speed things along.

It’s astounding that the Fed’s solution to inflation could cause a “crash in the job market,” (mass unemployment). Is this the best that all those highly paid economists can do?

The solution to inflation is to cure the causes of inflation, i.e. shortages, not to wreck the economy by cutting demand.

The bottom line: The Fed has two jobs, and is currently coming up short at one of them. It is unclear whether it can fix one side without messing up the other.

The real bottom line: This is what the Fed really was designed to do:

Supervise and regulate banks and other important financial institutions to ensure the safety and soundness of the nation’s banking and financial system and to protect the credit rights of consumers.

Maintain the stability of the financial system and contain the systemic riskthat may arise in financial markets.

Provide certain financial services to the U.S. government, U.S. financial institutions, and foreign official institutions, and play a major role in operating and overseeing the nation’s payments systems.Only later did Congress and the President sneak in a fourth responsibility:

Conduct the nation’s monetary policy by influencing money and credit conditions in the economy in pursuit of full employment and stable prices.

Essentially, the Fed was designed to do one job: Control the banking/financial system. Congress and the President are responsible for the economy.

Foisting the inflation, deflation, recession, depression, employment, unemployment, and economic growth jobs on the Fed was an admission by Congress and the President that they are not competent to do exactly what they were elected to do: Improve the lives of the governed.

It’s an admission that our recalcitrant, fractious political system cannot cope with the major problems of the day, and that some politically insulated agency must carry the water when our elected officials are more interested in winning elections than in doing their jobs.

SUMMARY

Today, our economic problems center on inflation and slow growth.

But inflation is a symptom; shortages are the cause.Slow growth is a symptom; lack of money is the cause.

The Fed’s primary tools are limited to interest-rate and a minimal money-supply control, both of which are designed to treat the symptoms, not the shortages.

Sadly, the Fed wrongly believes economic growth causes inflation, so it will use its limited tools to force reduced economic growth, and most likely, recession, while the basic causes of inflation will remain.

So, because of economic ignorance, we will endure stagflation.

Spending to cure the shortages would cure both the inflation and the slow growth, but Congress and the President, which solely have the curative power, have abdicated their responsibility.

So, as always, we will bounce from boom to bust in a neverending cycle of incompetence, while the people suffer.

Historic fertilizer shortages threaten world’s food security Elizabeth Elkin and Samuel Gebre, Bloomberg News For the first time ever, farmers the world over — all at the same time — are testing the limits of how little chemical fertilizer they can apply without devastating their yields come harvest time. Early predictions are bleak.

In Brazil, the world’s biggest soybean producer, a 20% cut in potash use could bring a 14% drop in yields, according to industry consultancy MB Agro.

In Costa Rica, a coffee cooperative representing 1,200 small producers sees output falling as much as 15% next year if the farmers miss even one-third of normal application.

In West Africa, falling fertilizer use will shrink this year’s rice and corn harvest by a third, according to the International Fertilizer Development Center, a food security non-profit group.

Soaring prices for synthetic nutrients will result in lower crop yields and higher grocery-store prices for everything from milk to beef to packaged foods for months or even years to come across the developed world.

More fertilizer use brings more food production. But as costs for synthetic nutrients have skyrocketed — in North America, one gauge of prices is nearly triple where it was at the start of the pandemic — farmers have had to start paring back use, sometimes dramatically.

—//—

Gulf of Mexico drilling makes too-little, too-late comeback Paul Takahashi, Bloomberg News A new wave of oil platforms is sweeping into the U.S. Gulf of Mexico as crude prices are riding historic levels and demand for barrels is higher than ever.

But don’t count on the new production to close the oil-supply gap that has plagued the world’s economies since the pandemic. Even with the new platforms coming online, gulf oil production won’t grow substantially in the coming years as mature fields decline, according to analysts.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics. Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps: