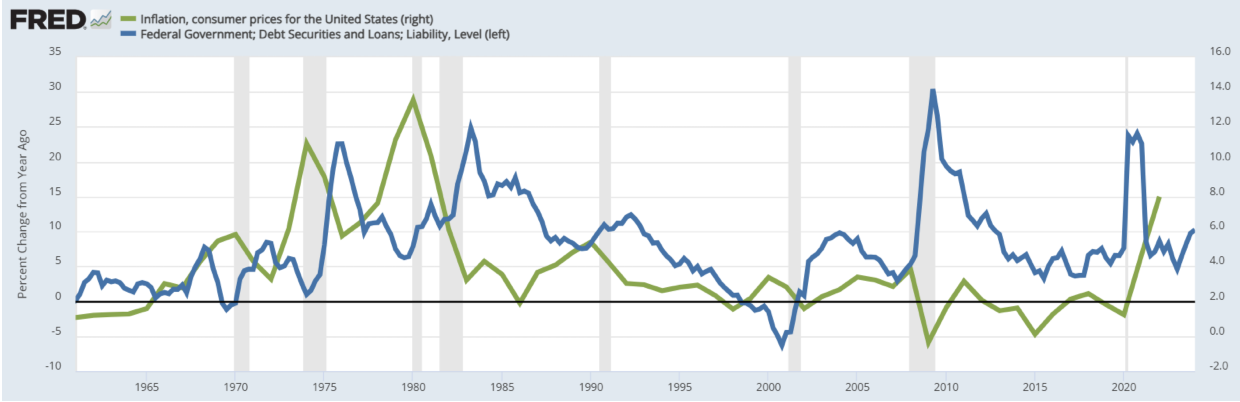

Translation: The US is pumping a record amount of growth dollars into the economy. It’s only going to get better.The US is paying a record amount of interest on its debt. It’s only going to get worse By Tami Luhby, CNN, Tue February 14, 2023

Translation: Powell urges Congress to blame federal “debt” for the inflation, so he doesn’t get blamed. We’ve had massive “debt” (See: The “National Debt” isn’t national, and it isn’t a debt) in the past without inflation. Powell doesn’t tell you that because he is a member of the “Federal Debt is a Ticking Time Bomb” culture.Powell urges Congress to solve growing US debt ‘sooner, rather than later’

Translation: The federal government is nothing “like many Americans.” The federal government is Monetarily Sovereign, while the American people are monetarily non-sovereign. But we want you to believe the government is just like you.Like many Americans, the federal government is shelling out a lot more money to cover interest payments on its debt after a series of Federal Reserve rate hikes over the past year.

Translation: The Treasury Department pumped a record $213 billion growth dollars worth of interest payments in the last quarter of 2022. That is $64 billion added to Gross Domestic Product (GDP)from the same period a year earlier.The Treasury Department paid a record $213 billion in interest payments on the national debt in the last quarter of 2022, up $63 billion from the same period a year earlier.

Translation: The fourth-quarter addition to GDP was nearly $30 billion more than in the prior quarter, the largest stimulus to the economy on record.The fourth-quarter tab was also nearly $30 billion more than in the prior quarter, which is the largest quarterly increase on record, said Jerry Dwyer, an economics professor emeritus at Clemson University.

Translation: The Federal Reserve is raising interest rates by 4.25%, which will increase the price of everything, in its effort to combat increased prices. Think about that.Borrowing costs are expected to become an increasingly heavy burden in coming years. The Congressional Budget Office is set to provide its latest estimate on Wednesday.

The surge is due mainly to the Federal Reserve raising interest rates by 4.25% between March and December. The central bank increased the rate another quarter point in February.

Translation: Until recently, it cost the federal government very little to create the dollars to finance its operations. Just the press of a few computer keys.Until recently, it cost the federal government very little to issue debt to finance its operations.

Translation (courtesy of former Fed Chairman Ben Bernanke): “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.” Translation (courtesy of former Fed Chairman Alan Greenspan): “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.” So, why would the government borrow dollars? It doesn’t.“It was almost free money,” Dwyer said. “You could borrow a trillion dollars, and if you financed it with Treasury bills, you paid almost no interest.”

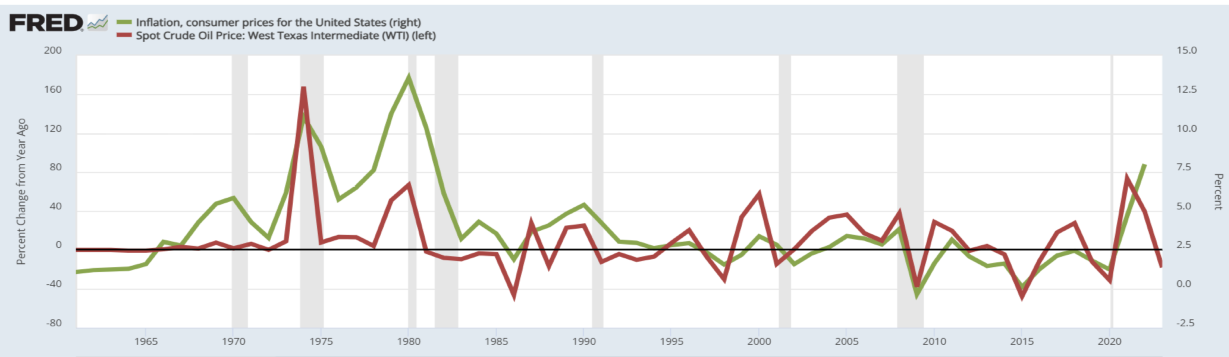

Translation: The Fed raises rates, which increases all prices, i.e., causes inflation, to fight inflation. It’s like a doctor bleeding a patient to cure anemia.“But interest rates weren’t going to stay there forever.”

Translation: The US has hit its $31.4 debt ceiling, which actually isn’t a “debt” ceiling. Everything has already been paid for, and nothing is owed. There is no debt. The dollars exist in T-security accounts. To pay off those accounts, the government merely returns the existing dollars. Congress created the fake “debt” ceiling to make itself look prudent to an ill-informed electorate.The national debt is once again in the spotlight now that the US has hit its $31.4 trillion debt ceiling, forcing Congress to take action or risk a catastrophic default.

Translation (Courtesy of Alan Greenspan): “The United States can pay any debt it has because we can always print the money to do that.” so the “extraordinary measures” are a bunch of hokum. And so is the fake “debt ceiling.”The Treasury Department is taking extraordinary measures to allow the government to continue paying its bills in full and on time, which it expects to last at least until early June.

Translation: The spike in interest payments added growth dollars to GDP much faster. This adds unnecessary pressure on Congress to take dollars out of the economy, thereby causing a recession.The spike in interest payments also contributed to the federal government hitting the debt ceiling that much faster.

And it adds to the pressure on Congress to raise taxes, cut spending or allow the government to borrow more to meet all its obligations.

Translation: As existing Treasury Securities mature, the government will increase the amount of growth dollars it pumps into the economy.Even if the Federal Reserve slows or stops raising rates this year, as many economists expect, the nation’s borrowing costs will continue to increase.

That’s because as the existing debt matures, the government issues new debt with the higher prevailing interest rates.

Translation: The higher rates could increase the amount of growth dollars pumped into GDP to about $9 trillion, according to the Peter B. Peterson Foundation, a right-wing organization that, on behalf of the rich, seeks to spread disinformation about America’s finances.The higher rates could increase the net interest cost on the national debt to about $9 trillion over the next decade, according to estimates by the Peter G. Peterson Foundation, a nonpartisan organization that seeks to raise awareness of America’s long-term fiscal challenges.

Translation: That’s up from a record $8.1 trillion growth dollars the CBO projected in May 2022, and the $5.4 growth dollars it tried to scare you about in July 2021.That’s up from the record $8.1 trillion that the CBO projected in May 2022 and the $5.4 trillion it projected in July 2021.

Translation: (Courtesy of Ben Bernanke) “It’s not tax money… We simply use the computer to mark up the size of the account.” By 2032, growth dollars will triple to more than $3 billion per day, and not costing any household a single penny. The federal government creates ad hoc every dollar it spends by pressing computer keys. No tax dollars are used.By 2032, interest costs will triple to more than $3 billion per day and to at least $9,400 per household, on average, according to the foundation.

Translation: The government justifies paying too little to Social Security and Medicare by pretending it is short of money when, in fact, it has infinite money.They are on track to become the largest federal budget item, surpassing Social Security and Medicare by the middle of the century.

Translation: To keep you from asking for benefits, we pretend that “Having rapidly growing interest makes it much more difficult for the government to fund all the things that are important to our society.” Why do we do that? Because the rich tell us to widen the income/wealth/power Gap between them and you. The wider the Gap, the richer they are. So, they bribe the main information sources to tell you the government can afford tax loopholes for the rich, but not Social Security and Medicare increases for the rest of you. Economists are bribed with university grants and promises of lucrative employment later. The media are bribed with advertising dollars and ownership. Politicians are bribed with political contributions and lucrative jobs in “think tanks.” All are bribed to tell you that increasing your benefits is unaffordable. SUMMARY The rich get richer when the income/wealth/Gap widens. So they promulgate the lie that your taxes pay for benefits, and your federal deficits are unsustainable. Rodger Malcolm Mitchell Monetary Sovereignty Twitter: @rodgermitchell Search #monetarysovereignty Facebook: Rodger Malcolm Mitchell; MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell“Having rapidly growing interest makes it much more difficult for government to fund all the things that are important to our society,” said Michael Peterson, the foundation’s CEO.

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

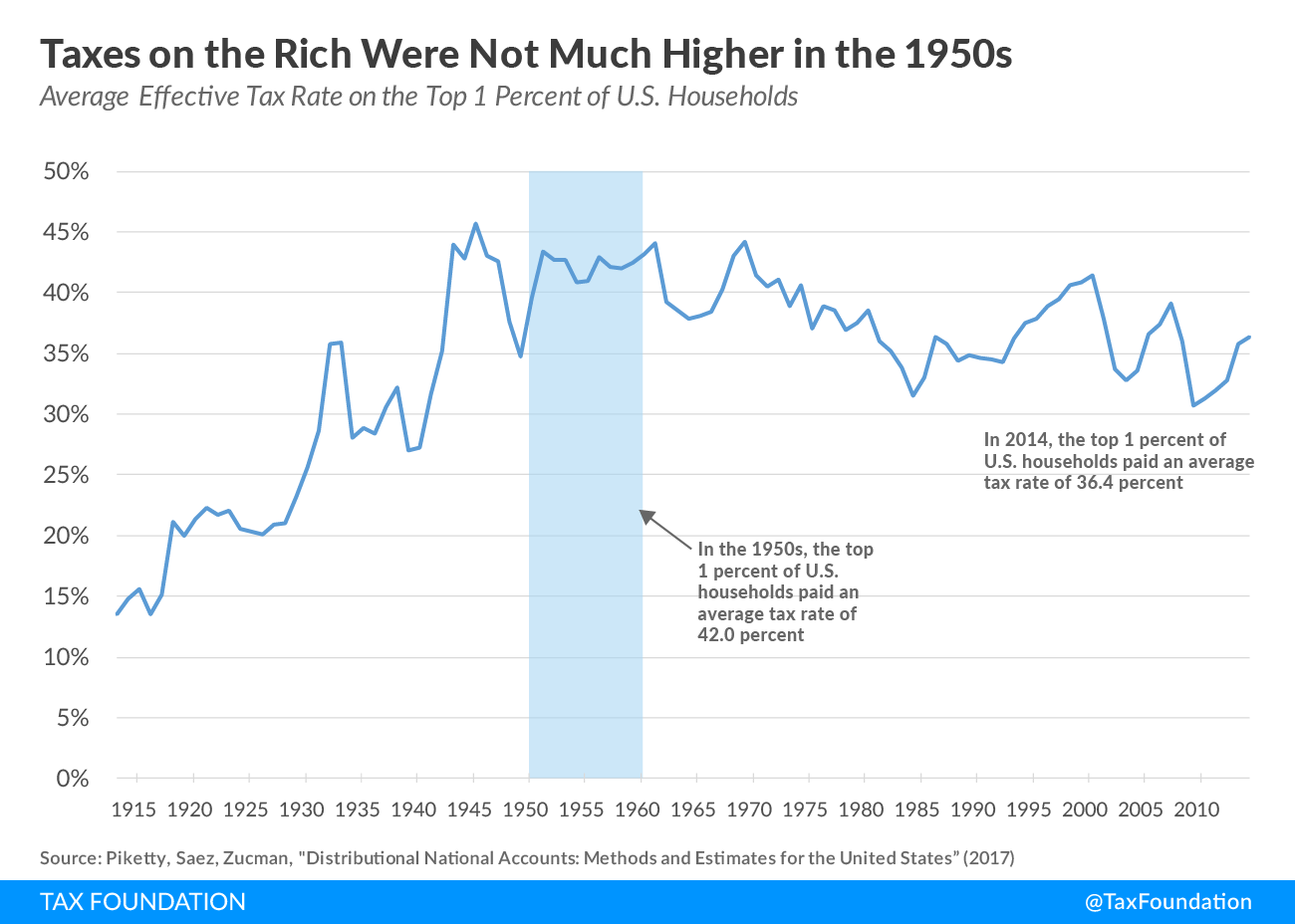

Considering that the top tax rate in the 1950s was 90%, the rich did not pay much more in that period than they do now. And some of the richest among us pay little if anything.

For example, Donald Trump paid no income taxes at all, during ten of the fifteen years, 2000-2015, despite being a billionaire. Tax laws, favorable to the rich, gave him the ability to claim losses on investments that an ordinary taxpayer may not look at as “losing” money.

In summary, using federal taxation of the rich to narrow the Gap is bad economics. History shows the rich would find ways to avoid paying higher rates.

But, even if the rich were forced to pay more, the higher rates would take dollars out of the economy and recess the economy. Option #1 is a “heads-you-lose (the rich don’t pay more), tails-you-lose” (GDP falls) plan.

Sadly, that is the plan Biden seems to have chosen, and it will cost him the November election.

The electorate may be ignorant about economics, but the rich would make sure the voters understood that raising taxes — anyone’s taxes — would hurt the economy.

It’s simple math. The more the federal government takes out of the economy, the less the economy (GDP) has.

Reducing federal taxes and/or providing supplementary benefits to those who are not rich, (#2 and #3) are the sole economically sensible ways to narrow the income/wealth/power Gap.

Sadly this sensible approach is blocked by the non-sensible belief that federal deficit spending is

Considering that the top tax rate in the 1950s was 90%, the rich did not pay much more in that period than they do now. And some of the richest among us pay little if anything.

For example, Donald Trump paid no income taxes at all, during ten of the fifteen years, 2000-2015, despite being a billionaire. Tax laws, favorable to the rich, gave him the ability to claim losses on investments that an ordinary taxpayer may not look at as “losing” money.

In summary, using federal taxation of the rich to narrow the Gap is bad economics. History shows the rich would find ways to avoid paying higher rates.

But, even if the rich were forced to pay more, the higher rates would take dollars out of the economy and recess the economy. Option #1 is a “heads-you-lose (the rich don’t pay more), tails-you-lose” (GDP falls) plan.

Sadly, that is the plan Biden seems to have chosen, and it will cost him the November election.

The electorate may be ignorant about economics, but the rich would make sure the voters understood that raising taxes — anyone’s taxes — would hurt the economy.

It’s simple math. The more the federal government takes out of the economy, the less the economy (GDP) has.

Reducing federal taxes and/or providing supplementary benefits to those who are not rich, (#2 and #3) are the sole economically sensible ways to narrow the income/wealth/power Gap.

Sadly this sensible approach is blocked by the non-sensible belief that federal deficit spending is