The problem with Libertarians like Eric Boehm . . . where do I begin? They have so many issues.

First, they don’t understand this equation: Gross Domestic Product = Federal Spending + Non-federal Spending + Net Exports.

Gross Domestic Product (GDP) is the most commonly used measure of the economy. The equation tells you that the more the federal government spends, the more the economy grows. But Libertarians don’t like government spending.

How does one reason with such people? Mainly, how does one acquaint them with Monetary Sovereignty, which says, “Federal financing is different from non-federal financing.”

If they can’t understand, or more accurately, refuse to understand, those two concepts—GDP and Monetary Sovereignty—how can their opinions be respected?

Here is the latest “Boehmism,” which, remarkably, may exceed all his previous work in ignorance and/or deception (It’s hard to know which:

The National Debt Is a National Security IssueThe growing debt will “slow economic growth, drive up interest payments,” and “heighten the risk of a fiscal crisis,” the CBO warns.ERIC BOEHM | 3.21.2024 1:50 PM

It’s a dangerously addictive habit that threatens to ruin our children’s lives and undermine America’s national security—and this week, Congress finally acknowledged as much. However, it remains unclear if lawmakers have the guts to do anything substantial.

No, I’m not talking about TikTok. I’m talking about the $34.6 trillion national debt.

The Senate unanimously approved a resolution on Wednesday calling the debt “a threat to the national security of the United States” and calling expected future budget deficits “unsustainable, irresponsible, and dangerous.”

1940 “Debt” was called a “ticking time bomb.”

The Senate votes to please voters, and sadly, most voters believe anything called “debt” should not be large. They don’t understand that federal “Debt” is not federal and it isn’t debt.

“We have more than doubled our national debt in just ten years,” said Sen. Mike Braun (R–Ind.), who sponsored the resolution.

“America is moving down a dangerous and unsustainable path of reckless spending, and the federal government has yet to take it seriously.”

“Unsustainable” is the Libertarian’s favorite word when describing the so-called national (or federal) debt, which is neither national, federal, nor debt.

They use that word because it has no specific meaning. They don’t say precisely what is “unsustainable” about it. The federal government, being uniquely Monetarily Sovereign (Libertarians don’t understand that concept, either), can pay any debt denominated in U.S. dollars.

1950 “Debt” was called a “ticking time bomb.”

Whether a debt is $100 or $100 trillion, the federal government could pay it instantly by pressing computer keys.

The federal government pays all its debts the same way. It creates new dollars ad hoc.

To pay any creditor, the government sends instructions, not dollars, to the creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

Those instructions are electronic or paper (a check), saying, “Pay to the order of _____. ” The instant the bank does as instructed, new dollars are created and added to the M2 money supply measure.

Alan Greenspan: “A government cannot become insolvent concerning obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

That is how the federal government creates dollars and pays its bills. There is no limit to the government’s ability to send instructions, and thus no limit to the government’s ability to create dollars. No debt is “unsustainable.”

1960 “Debt” was called a “ticking time bomb.“

The passage of a nonbinding resolution on the Senate floor is several steps short of addressing the federal government’s addiction to borrowing—but, as they say, recognizing that you have a problem is the first step toward solving it.

The federal (or national) debt is not a debt because the federal government does not borrow.Why would it? Given its infinite ability to create dollars, why would the federal government borrow dollars?

It wouldn’t, and it doesn’t.

Those things called T-bills, T-notes, and T-bonds do not represent borrowing. Although “notes” and “bonds” are evidence of borrowing in the private sector, federal finance is different.

1970 “Debt” was called a “ticking time bomb.“

T-securities are evidence of deposits into savings accounts at the Federal Reserve, the contents of which are wholly owned by the depositors. The government neither needs nor uses those deposits. It merely holds them in safekeeping for the depositors.

The federal government’s main purpose in offering T-security accounts is to provide the public and other nations with a safe, interest-paying place to store unused dollars, which helps stabilize the dollars.

By paying interest, these accounts help the federal government control interest rates.

1980 “Debt” was called a “ticking time bomb.“

The government does not owe the dollars deposited in T-security accounts. The government merely stores them for the depositors.

Upon maturity of any T-security, the government merely gives the dollars, that never had left the account, back to their owner, the depositor.

It’s not a federal debt, just as the contents of a bank safe deposit box are not a bank debt.

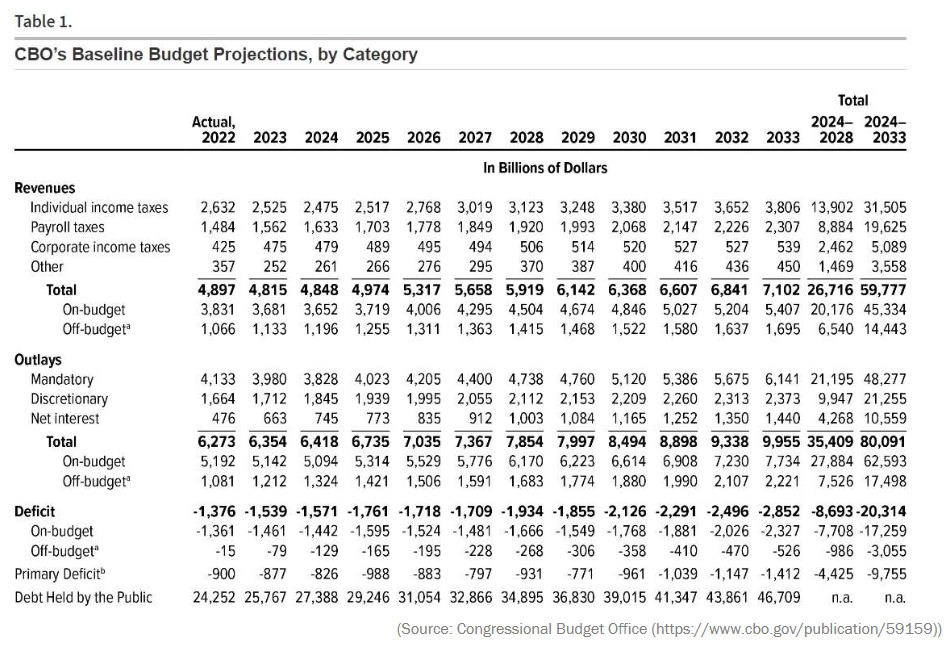

And the approval of that resolution was timely. Later on Wednesday, the Congressional Budget Office (CBO) published its latest long-term budget projections. The report shows that annual budget deficits are on pace to grow from an expected $1.6 trillion this year to $2.6 trillion in 2034, $4.4 trillion in 2044, and $7.3 trillion in 2054.

A federal budget deficit is much different from a personal budget deficit.

1990 “Debt” was called a “ticking time bomb.“

If you or I were to run a budget deficit, we would have to obtain the money to pay our bills, either by borrowing or from our income or savings.

The federal deficit merely is the bookkeeping difference between taxes and spending. The spending has already been paid for by money creation.

Here again, one must understand Monetary Sovereignty. State and local taxes do fund state and local taxes. The state and local governments are monetarily non-sovereign, like you and me.

2000 “Debt” was called a “ticking time bomb.“

So what is the purpose of federal taxes, if not to fund federal spending?

To help the federal government control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward/

To assure demand for the U.S. dollar by requiring federal taxes to be paid in dollars.

To make the public believe that federal benefits are limited by tax receipts or borrowing. (This last is at the behest of the very rich, who get wealthier by widening the income/power Gap between them and the rest of us.)

As a result of those rising budget deficits, the national debt will continue to accelerate upward.

The misnamed “national debt” is not a threat or a burden on anyone- not the government or taxpayers. Even if the “debt” were hundreds of trillions of dollars, the federal government could continue paying its bills without collecting a penny more in taxes, nor borrowing a single dollar.

2010 “Debt” was called a “ticking time bomb.“

The CBO projects that the federal government’s debt will total $114 trillion by 2054. The debt is already roughly the size of the nation’s economy and is expected to surpass the all-time high of 106.4 percent of gross domestic product (GDP) by 2028.

By the end of the 30-year projection, the debt is estimated to reach 166 percent of GDP.

The oft-mentioned “Debt”/GDP ratio is meaningless for several reasons:

The government does not owe or pay the “debt.”

GDP does not owe or pay the “Debt.”

The ratio says nothing about the health of the U.S. economy.

The ratio says nothing about the federal government’s ability to pay its bills.

“Such large and growing debt would have significant economic and financial consequences,” the CBO warns. “

Among its other effects, it would slow economic growth, drive up interest payments to foreign holders of U.S. debt, heighten the risk of a fiscal crisis, increase the likelihood of other adverse outcomes, and make the nation’s fiscal position more vulnerable to an increase in interest rates.”

The above paragraph is wrong in every respect:

2220 “Debt” was called a “ticking time bomb.“

A large and growing “Debt” merely means our Monetarily Sovereign federal government is pumping more growth dollars into the economy. The larger the “Debt,” the more growth dollars and the faster the economic growth. Remember: GDP = Federal Spending + Non-federal Spending + Net Exports. Federal Spending even increases Non-federal Spending

Our Monetarily Sovereign U.S. federal government has the infinite ability to create the dollars that pay foreign holders of U.S. debt. Paying dollars to foreign nations increases foreigners’ ability to purchase our goods and services (Net Exports).

No “fiscal crisis” has been or can be caused by the growing federal debt. The federal government always will be able to pay all its bills.

The large and growing “Debt” causes no “other adverse outcomes. The Debt/GDP ratio is fiscally meaningless for a Monetarily Sovereign nation.

Our Monetarily Sovereign government’s fiscal position is vulnerable only to the ignorance of those who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty. The government can pay any amount of interest simply by pressing computer keys.

In 1940, the federal “Debt” was only $43 billion. Those who are ignorant about federal finances called it a “ticking time bomb.”

Today, the “Debt” totals more than $33 trillion, and that phony time bomb is still a dud—and always will be.

Higher interest rates are already significantly affecting the federal budget. This year, payments on the existing debt will total an estimated $870 billion, which is more than the Pentagon’s budget. Thanks to higher interest rates and a larger debt load, debt payments have jumped by 32 percent since 2023.

Interest payments have indeed had an effect on the federal budget. They have forced the federal government to spend more, which pumps more growth dollars into the economy and increases GDP.

Again, the Libertarians seem to have forgotten: GDP = Federal Spending + Non-federal Spending + Net Exports. Not only does Federal Spending directly lift GDP, but it also lifts Non-federal Spending, which, in turn, lifts GDP

As federal “Debt” has grown, so has the economy (GDP).As federal spending has grown, so has the economy (GDP).

There seems to be no sign that federal spending or federal “Debt” is “unsustainable,” “slows economic growth,” “heightens the risk of a fiscal crisis,” “causes other adverse outcomes,” or makes the nation’s fiscal position more vulnerable to an interest rate increase.”

On the contrary, increases in federal “Debt,” yield all positive outcomes, while decreases in debt cause depressions and recessions:

U.S. depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Deficit reductions (purple line) lead to recessions (vertical gray bars) which are cured by deficit increases.

GDP = Federal Spending + Non-federal Spending + Net Exports. Not only does Federal Spending increase GDP directly, but it also increases Non-federal Spending by providing the private sector with money.

The new CBO report shows that debt payments will be one of the fastest-growing parts of the budget for the foreseeable future, along with the twin old-age entitlement programs of Social Security and Medicare.

By 2051, interest payments will be the single largest line item in the federal budget.

If there’s a sliver of good news to be found in the new CBO projections, it is that the situation looks slightly less dire than it did last year. That improvement is due to higher expected levels of immigration and stronger estimates of future economic growth—not because of anything that policy makers in Washington have done.

(If anything, they seem determined to prevent those improvements from coming to pass, whether by limiting immigration or regulating the economy more strictly.)

This is the ultimate of ignorance. The data stare him in the face, but instead of reevaluating his position, he claims the good news comes despitethe data. In essence, Boehm has two conclusions:

If the data support his belief, he calls attention to that.

If the data do not support his belief, he ignores the data.

Thus, he is incapable of learning.

We should also keep in mind the usual caveats here: The CBO does not account for the possibility of recessions, natural disasters, wars, or other unpredictable events that could cause the federal government to borrow more heavily than current law expects.

The past 30 years have included 9/11, the war on terror, the Great Recession, and the COVID-19 pandemic, so it seems pretty likely that the next three decades will include at least a few emergencies that drive deficits higher.

Boehm doesn’t stop to think about why emergencies drive deficits higher: Emergencies, in of themselves, tend to impede economic growth, so the government increases deficit spending to save the troubled economy.

Why does the government need to wait for emergencies before it stimulates economic growth. Why not stimulate growth during non-emergency times, too?

This is a question the Libertarians and the right wing never asks, because the answer goes against their beliefs.

“There is no way to look at these eye-popping numbers without realizing we need to make a change,” Maya MacGuineas, president of the Committee for a Responsible Federal Budget, which advocates for lower deficits, said in a statement about the CBO report.

“And yet we have lawmakers promising what they won’t do: I won’t raise taxes, I won’t fix Social Security, I won’t pay for all the things I do want to do. And so we continue on this dangerous path.”

MacGuineas has been president of the CRFB for many years. She and her group are bought and paid for by the rich, so they espouse beliefs that would make the rich righer by widening the Gap between the rich and the rest.

“I won’t raise taxes.” That is a good thing. Federal taxes remove growth dollars from the economy.

“I won’t fix Social Security.” To MacGuineas, “fix” means cut benefits or raise taxes, both of which are unnecessary and harmful to the economy. The federal government has infinite money to pay for Social Security.

“I won’t pay for all the things I want to do.” The government is perfectly capable of paying for anything and everything. It’s people like Boehm and MacGuimeas who hinder the government from doing what it was created to do: Protect and improve the lives of the people.

Indeed, on Thursday, Speaker of the House Mike Johnson (R–La.) told reporters that he supports plans for a so-called “fiscal commission”—which could propose some solutions to Congress’ budgeting problems—but only if the agency could not suggest tax increases or cuts to entitlement programs.

Obama had a “fiscal commission.” Its “increase- taxes, cut-spending” recommendations would have sent the economy into a depression. Fortunately, Congress didn’t listen.

That approach guarantees that the federal government will have to continue borrowing heavily to make ends meet.

Again, the U.S. government never borrows its own sovereign currency. Boehm does not recognize the differences between a Monetarily Sovereign entity and a monetarily non-sovereign entity. Either he is paid to act ignorant or he does it without pay.

Despite the Senate’s declaration that the national debt is a national security risk and the CBO’s attempts to sound the alarm about the federal government’s fiscal trajectory, there’s still a major shortage of elected officials who want to take the problem seriously.

He is correct that there’s “a major shortage of elected officials who want to take the problem seriously.” Without that shortage, the government could fund such benefits to America as:

Comprehensive, no-deductible healthcare insurance or every American.

More medical personnel at all levels, plus more hospitals with advanced equipment

Social Security for Americans of all ages.

The reduction of poverty and homelessness in America

With the reduction of poverty, there would be a significant reduction in crime.

A greater ability to accept fully vetted immigrants, whose work and intelligence would help America grow.

Education, including advanced degrees, for all those who want it.

More scientific innovation in disease prevention and cure.

More efforts to reduce global warming.

A dramatic reduction in federal taxes, which do nothing but remove growth dollars from the economy.

Pay students a salary so that families would not need to favor dropping out of school to help support the family.

The government can pay for all of it, without taxes and without inflation. Anyone not want it?

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Some economists, politicians, and media talking heads might tell you it means the airlines are seriously in debt.

OK, that “3 trillion” is not dollars; it’s miles or points. But there is a point (pun intended) to be made.

Frequent flyers, consider yourselves warned: Sitting on a pile of unused airline miles could cost you.

Liabilities tied to the five most valuable airline-loyalty programs in the U.S. soared almost 12% to $27.5 billion last year, according to new analysis by LendingTree Inc.’s consumer-finance website ValuePenguin.

Airlines looking to shore up their balance sheets could reduce the value of those rewards or reinstate policies that allow miles or points to expire, the firm warned.

If the airlines wanted to reduce their mileage “debt,” they arbitrarily could reduce the value of their mileage reward points or allow miles to expire.

They are mileage-points sovereign.As the issuer of mileage points, the airlines can do anything they wish with those points. They can issue as many as they wish, increase or reduce the value, or void them simply by pressing computer keys.

If the Airlines felt generous, they could give you a few million mileage points. Or if they felt stingy, they could “tax” you points by reducing their value. Suddenly, flying to your favorite city would cost you double the number of points you thought. Effectively, that would be a 50% “wealth” tax on your point holdings.

Or they could tell you to use all your points by December 31st at which time the points would be worthless. The effect would be like a tax on you.

The airlines are to mileage points as the U.S. federal government is to U.S. dollars. By giving out more points than they receive, the airlines run “points deficits”; cumulatively, the airlines have “points debt.”

The airlines create points by pressing computer keys. Nothing prevents the airlines from pressing keys, forever. The U.S. government creates dollars by pressing computer keys. nothing stops the U.S. government from pressing keys, forever.

Being points sovereign, the airlines never can run short of mileage points. The U.S. government, being Monetarily Sovereign, never can run short of dollars.

The airlines never borrow points. The government borrows dollars.

“Especially in a time where airlines have gone through such financial issues, it would be easy to see that they would look at some sort of devaluation of the miles and points as a way to make up a little bit of financial ground,” Matt Schulz, LendingTree’s chief credit analyst, said in an interview.

“I would suspect we might see something like that going forward.”

This demonstrates the total control a Monetarily Sovereign entity has over its currency, whether airline points or dollars. The airlines create all the rules re. points. The government creates all the rules (i.e. laws) regarding dollars.

At the height of the Covid-19 pandemic, Delta, American, and United pledged their loyalty programs as collateral for bonds as the virus and resulting government restrictions sapped travel demand. Such deals could prevent any material changes to the programs, said Joe DeNardi, an analyst with Stifel Financial Corp., who follows airline loyalty programs closely.

United, for its part, doesn’t see currency devaluation as a handy tool to lower that accounting liability, said Michael Covey, managing director of the loyalty program at the airline.

Yes, it’s an accountingliability, but not a real liability because the airlines have total control over its value. They arbitrarily can create points by pushing computer keys, or they could eliminate the points altogether. Goodbye, “points debt.”

Does an airline owe someone a billion points? No problem. They can just type 1,000,000,000 into a computer and Voila! Here are the billion points.

Does the federal government owe someone a billion dollars? No problem. Just type the number into a computer and the dollars come into existence.

Think about that the next time someone tells you that Medicare or Social Security are running short of money.

A decade ago, revenue-based airline programs (rather than mileage-based) were fairly uncommon in the U.S. JetBlue was one of the first U.S. airlines to launch a revenue-based program when it revamped its program in 2009. Southwest followed with a program “enhancement” in 2011.

Then, the big airlines jumped on the bandwagon. Delta transitioned to a revenue-based system in 2015, and American Airlines and United quickly followed suit. Now, almost all major U.S. airlines operate a revenue-based program.

There again is that total control a monetary sovereign has over its currency. The airlines arbitrarily went from awarding mileage points to awarding revenue points.

However, programs differ a bit in how they award miles.

For better or worse, the three biggest U.S. airlines have similar mileage earning systems. General members earn 5 miles per dollar of eligible spending on travel with the airline.

Elite members earn a bonus on this base earning, with all three programs topping out at 11 miles per dollar for top-tier elites.

On Dec. 9, 2021, Delta became the first domestic airline to make basic economy fares ineligible for mileage earning. Basic economy flyers will no longer earn SkyMiles or Elite Qualifying Miles, Dollars, or Segments.

Again, the above demonstrates the total control by a monetary sovereign. Delta simply made the change by fiat. The federal government can, and often has, arbitrarily changed the value of the U.S. dollar.

The “Nixon shock” was an arbitrary move by President Nixon to end the convertibility of dollars into gold. Suddenly, the dollar was no longer worth 1/35th of an ounce of gold.

If airlines made the same kind of change, suddenly airline points would no longer be worth 1 cent or 1.5 cents each. The “problem” of the “points debt” would disappear.

Selling frequent-flyer points to banksAirlines make money from loyalty programs by selling frequent-flyer points to banks, which then award them to credit card holders as purchase rewards.

The banks pay airlines 1 to 1.5 cents per mile, plus a bonus when new customers sign up for their branded credit card.

By selling their loyalty program frequent flyer miles to banks, credit card companies, car rental firms, hotels, and supermarkets, the airlines have found an almost guaranteed way to make a profit from their tickets.

In effect, most major airlines have a business model which is more like a bank than a transport company.

No, it’s not more like a bank. It’s more like a Monetarily Sovereignnation— Canada, Mexico, the UK, Australia, Japan, China, and yes, the United States — all of whom can create andvprice their currencies at will (unlike monetarily non-sovereign entities like cities, counties, states, euro nations, businesses, you, and me.)

This is the airline profitability program:

The airlines create points from thin air. They create as many points as they wish at virtually no cost.

Of course, airlines have to offer travel in exchange for points, so that is a cost of the program, but:

Airlines control how many points each flight costs passengers. So, high-demand days cost far more points than other days. This way, the airlines dissuade passengers from using points on those days when they can sell seats for dollars.

This shows you that Monetary Sovereignty is everywhere, though the public is kept in the dark. (See: “The genius of the board game, Monopoly.”)

When a retailer issues coupons, they essentially issue money in lieu of a price reduction. The retailer is sovereign over the coupons and can issue as many coupons as he wishes and make them any value he wishes.

All outstanding coupons could be counted as retailers’ “debt” – -i.e., the value of outstanding coupons—except customers pay for the coupons when they buy the products.

Imagine an airline saying, “We are going to raise the price of a seat from 100 points to 200 points because we are running short of points.”

You would think that’s crazy. How could an airline run short its points, points it creates at will, by clicking computer keys?

But that is exactly what the federal government says when it claims Medicare and Social Security are short on dollars.

You should ask the same question. How can the U.S. federal government run short of its own dollars, dollars it creates at will by clicking computer keys?

The reason you don’t ask is simple. No one questions the airlines’ ability to create their points at will, but your information sources tell you the U.S. government can’t create its dollars at will.

They tell you the federal debt (that neither is federal nor debt) is “unsustainable.” They tell you the government should “ive within its means.” They tell you your taxes must be increased and/or your benefits reduced.

All these statements are deceptive, based on the hope that you don’t understand Monetary Sovereignty. The lie that the federal government can run short is dollars is told so that the rich can become richer while the rest survive in ignorance.

It’s that sort of ignorance someone like Eric Boehm promulgates when he writes an article like this:

The article pretends that the federal government is not Monetarily Sovereign, can’t create dollars at will, needs tax dollars to pay its bills, and in some unexplained way actually could run out of U.S. dollars.

It’s a monstrous lie, aimed at keeping you down and the rich up by widening the income/wealth Gap between the rich and you.

If you ever feel like protesting something, this is what you should protest. The Big Lie in economicsthat the federal government can’t afford to provide certain benefits and/or that taxpayers fund federal spending.

The lie claims the U.S. “debt” is a “ticking time bomb,” to scare you. (It’s a “bomb” that has been “ticking” since 1940, and still no explosion.)

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

This is what passes for “science” in the world of economics:

Raising interest rates increases the prices of everything. Therefore, raise interest rates to cure inflation.

Inflation happens when the economy grows too much (“overheated”). Therefore, to cure inflation, cause a recession or depression.

Any normal scientist would scoff at these beliefs, but economists are neither normal nor scientists. They are believers. They are cultish followers of the standard thinking, as exhibited in the following article.

When a hypothesis doesn’t work, a scientist uses that information to develop a new hypothesis. In economics, when a hypothesis doesn’t work, the economist merely shrugs and continues to claim it works.

Before COVID, the economy was growing massively, with interest rates near zero, massive deficits, and without inflation? Then, during and after COVID, we had inflation, with interest rates at elevated levels.

Did the economists learn anything from these events?

Hmmm. Now, let me think. Why did we have no inflation before COVID and elevated inflation during and after COVID? What changed? Two things”

We had shortages of oil, food, shipping, computer chips, metals, lumber, labor, and almost every other important good and service

The Fed raised interest rates, instantly making every product more expensive.

What didn’t change?

The government still is spending massively with huge deficits.

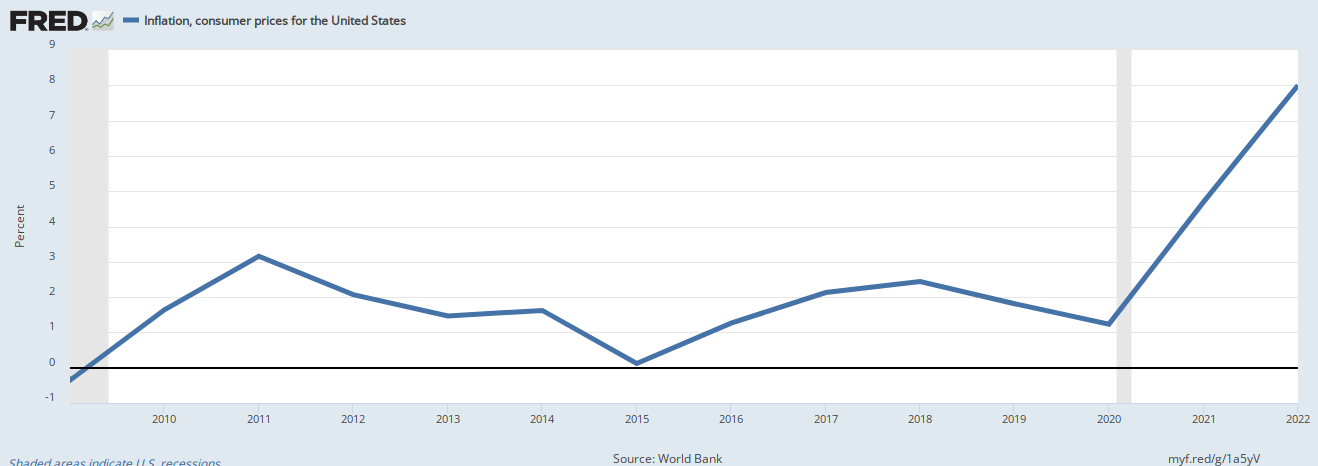

Analyze the following graph:

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.When supply cannot meet demand, prices go up. That’s basic.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.

Inflation has fallen from the shocking highs reached last year, but the Federal Reserve’s efforts have not successfully returned the beast to its cage.

The problem is supply, so what does the Fed do? It tries to control demand.

Why? Because that is the only tool it has. Because Congress is so inept, it has tasked the Fed with preventing and curing inflation. But the Fed can’t do it.

Who can control inflation? Congress and the president can control inflation by controlling shortages.

Oil shortage: Financial rewards to oil companies to find more, pump more, hire more, and lower prices

Food shortage: Financial rewards to farmers, wholesalers, and retailers to reduce risk, reward growth and lower prices

Labor shortage: Eliminate FICA plus Medicare for All to make employment less expensive and to encourage higher net salaries.

Federal rewards to all other industries involved with scarce goods and services.

Do you notice a commonality among the solutions? They all require more deficit spending, not less.

If rising prices are to be fully tamed, it increasingly looks like Congress will have to get the deficit under control first.

Rather than attacking the cause of inflation, scarcity, Boehm attacks the cure for inflation, federal deficit spending to cure shortages.

Prices are up 3.7 percent over the past year, according to new inflation data released by the Bureau of Labor Statistics on Thursday morning. But so-called “core inflation,” which filters out the more volatile categories like food and fuel prices, rang in at 4.1 percent in the newest report.

Oil and food are the “core inflation” goods. Their shortages and resultant price increases cause most inflations, worldwide.

Typical for the pseudo-science of economics, economists filter out the two most common causes of inflation — oil and food scarcity — when measuring inflation.

It’s like a sports team filtering out points scored and allowed when analyzing the team’s won/lost record. Senseless.

To control inflation, the Federal Reserve raised interest rates at 11 consecutive meetings starting in March last year.

Every one of those interest rate increases raised the prices of goods and services. So, surprise! Inflation increased.

Since July, the central bank has left interest rates unchanged—the Fed’s current base rate is 5.5 percent, up from 3.25 percent a year ago.

Higher interest rates seem to have brought inflation down, but prices are rising nearly twice as fast as the Federal Reserve’s target of 2 percent annually.

No, oil, food, labor, metals, shipping, etc. scarcities moderated, so inflation moderated despite continuing interest rate increases.

We may have reached the limit of what the Federal Reserve can accomplish regarding taming inflation through monetary policy.

We reached that limit on the first day. Raising interest rates is inflationary. Period.

The federal government’s $33 trillion national debt and rising budget deficits are creating inflationary pressure in ways that remain underappreciated.

Economists ignore when the national “debt” and deficits rise without inflation (as often happens). But when we have inflation, the “debt” and deficit (which we have almost yearly) are blamed.

The big problem is that higher interest rates are helping curb inflation but worsening the federal government’s deficit.

No, the big problem is that while higher interest rates exacerbate inflation, the federal deficit can be directed toward inflation-curing programs, like Medicare for All and the elimination of FICA — both costs of doing business.

Writing at CNBC, Kelly Evans gets at the heart of this conundrum: “If we don’t quickly close the gap between spending and revenues, the debt load will keep growing, and interest costs will keep on rising, and the deficit will thus stay elevated, which grows the debt load even more.”

de Rugy

There is no debt load. It isn’t even debt. It’s deposits. They are not any sort of burden on the federal government or on the economy.

Those dollars are not owed by the federal government. The creditors all have been paid.

The deposits are owned by the depositors, who are paid off when deposits are returned to them.

So, what does that have to do with inflation?

As Reason contributor Veronique de Rugy, an economist at George Mason University, explains at National Review, there is an assumption built into monetary theory that says fiscal contraction—that is, smaller deficits—will necessarily follow a monetary contraction like the rising interest rates of the past year.

In other words, when central banks make it more expensive to borrow, they assume the politicians in charge of fiscal policy will respond by borrowing less.

But that hasn’t happened, and there is little indication that it will in the near future.

This assumption relies on federal politicians not understanding that spending by our Monetarily Sovereign federal government is not dollar-constrained. The government has the infinite ability to create and spend dollars on interest or anything else.

For that reason, the federal government does not borrow dollars. It does not need to obtain dollars from anyone.

The assumption also relies on the federal government spending less, which is recessionary. It is the false belief that recession is the cure for inflation when there is zero supporting evidence.

The federal budget deficit nearly doubled in the fiscal year that ended on September 30, and bigger deficits are expected in the next few years—in significant part because of the feedback loop between higher interest rates and rising debt costs.

That is not a “feedback loop” it is a tautology. The feedback loop is: Raise interest rates -> inflation –> raise interest rates again –> still higher inflation endlessly.

To fully get inflation under control, de Rugy says the country must experience a period of negative wealth effects—that is, a decline in demand driven by consumers choosing to rein in spending due to declining wealth.

Without her word salad, she says, “The country must experience a recession.” The Libertarians believe recessions cure inflation. Have they never heard of “stagflation”?

That’s hardly something worth cheering for, but it might be the only way to truly tame inflation—and it probably won’t happen until Congress curbs spending, too.

“The only way to get a reduction of total demand, which will ultimately rein in inflation, is for the fiscal authority to implement fiscal consolidation, hence creating a negative wealth effect,” writes de Rugy. “Absent that fiscal contraction, inflation will rise.”

Increased demand did not cause the sudden inflation of 2020. Demand didn’t suddenly appear overnight. But COVID made shortages occur overnight.

Changes to monetary policy have brought inflation down from last year’s near-record highs. Still, the monetary theory upon which that policy is built assumes that fiscal policy will finish the job by reducing deficits.

Congress, so far, doesn’t seem interested in cooperating—so expect prices to keep rising at an annoyingly fast rate.

You have just read the Libertarians’ false excuse for their cure not working. They claim the government’s massive spending (which has been in force for many years) suddenly decided to cause our inflation.

In short, because bleeding the patient with leeches didn’t cure his anemia, it must be that the patient is eating too much good food. Such is the nonsense that permeates economics today.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

The Libertarians (the cruel shills for the Republican Party) have a non-solution for a non-problem.

The non-problem is that the U.S. federal government is running short of its sovereign currency, the U.S. dollar. The non-solution is to take dollars from the poor and middle-income people.

The headline implies at least four lies:

Lie #1. The federal government can’t afford to send money to the poor and middle-income people.

Lie #2. The solution would be for the government to take dollars from Social Security.

Lie #3. Congress doesn’t dare to take Social Security dollars from the poor and middle-income people.

Lie #4. The only recourse is to take welfare dollars from the poor.

Amid the fractious debate over the federal budget, Speaker of the House Kevin McCarthy (R–Calif.) has outlined plans for cutting several prominent welfare programs to save about $150 billion annually.

According to The Washington Post, those cuts would affect a wide range of federal safety net programs, including food stamps and Meals on Wheels, which help feed needy families.

Other cuts would affect Federal Pell Grants for low-income college students, grants that help families afford housing, and a program that helps offset high heating bills.

Notice that none of the Libertarian non-solutions to the non-problem involve taking dollars from the richby eliminating the kind of tax dodges that all people like Donald Trump to pay almost $0 federal taxes.

Regardless of whether you think the federal government should be in the business of funding any of those things in the first place, there’s no denying that sudden cuts to existing welfare programs can be disruptive to the individuals and families that have come to rely upon them.

Here, the Libertarian implies that the federal government should not help low-income college students, families that can’t afford housing, or low-income families that can’t pay their heating bills. This is typical for the heartless Libertarians and Republicans.

They don’t give a damn about people but are concerned with just two things: Saving government money for a government that has infinite money and helping the rich grow richer.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

It’s also true that, as Reason’s Liz Wolfe points out in this morning’s newsletter, the proposed cuts reflect the reality of a government that has been living beyond its means for too long.

You and I can “live beyond our means.” but the federal government cannot. It has infinite “means.”

Alan Greenspan: “The United States can pay any debt it has because we can always print the money to do that.

“It’s not exactly a winning PR move to slash the programs that serve needy toddlers and first-generation college kids, but there’s an important fundamental truth at the heart of the fiscal hawks’ concerns: government spending simply cannot continue at current levels with no consequences,” Wolfe writes.

This lie has been told since at least 1940 and probably beyond. That was the first year I found that the federal debt, or deficit, was called a “ticking time bomb.” The phony bomb still is ticking after eighty-three years.

And precisely what are the “consequences” to which Wolfe refers and Boehm agrees? You never will see that explained in any Libertarian screed. The reason: There are no consequences. Period.

That’s true. But here’s an element of this debate that doesn’t get talked about enough: Cutting welfare programs for needy families is necessary because Congress insists that relatively wealthy senior citizens get paid first.

And here it comes: The theory is that seniors are wealthy, and despite paying the useless FICA tax for their entire lives, they really don’t deserve anything for their investment. So, cut Social Security because that’s where the money — the infinitely available money — goes. And who cares about those old folks, anyway?

Budgeting is always, at its core, an exercise in priority-setting. That’s especially true when your budget is wildly out of whack, and you’ve been borrowing at an unsustainable rate, as Congress has done for years.

What part of budgeting is “wildly out of whack”? Would reducing the money going to the middle and the low be the best way to put the budget in “whack”?

And then for two more lies in just five words (Is that a world record?) “Borrowing at an unsustainable rate.”

Lie #5. The federal government borrows. No, the federal government does not borrow dollars. Why would it borrow when it has the infinite ability to create dollars?

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

The confusion arises because private sector bills, notes, and bonds differ entirely from T-bills, T-notes, and T-bonds

The former have to do with borrowing. The latter have to do with depositing. A borrower receives from a lender money that the borrower uses. But the federal government doesn’t use or even touch the dollars deposited into T-security accounts.

The federal government, unlike state/local governments, is Monetarily Sovereign. It pays all its creditors with newly created dollars, ad hoc.

Despite Monetary Sovereignty being the single most important difference between federal and personal finances, you will never see those words in any discussion of federal budgeting being “unsustainable.”

Lie #6. “Unsustainable rate.” No amount of spending is unsustainable for the federal government. It has the infinite ability to create dollars.

When there’s no longer enough money to go around, you’re faced with a difficult proposition: Who gets paid first, and who has to wait at the back of the line?

The federal government always has enough money to go around. It cannot run short of dollars. Ever. Boehm knows this.

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

In the federal budget, seniors get paid first. Everyone else has to wait.

Lie #7. No, the rich are paid first. They are paid by the tax loopholes that allow them not to pay taxes in the first place.

McCarthy and his fellow Republicans are not proposing any cuts or changes to Social Security and Medicaid, the Post notes. That’s despite the fact that the two major entitlement programs are driving most of the federal government’s long-term deficit.

The federal deficit is the government’s method for pumping growth dollars into the economy. If the government did not run deficits, we would have yearly recessions and depressions.

U.S. depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Over the next decade, discretionary spending—including those welfare programs the GOP aims to cut—is projected to decline relative to the size of the U.S. economy, according to the Congressional Budget Office’s (CBO) projections.

Meanwhile, Social Security and Medicare are growing, fast. By 2030, the CBO expects so-called “mandatory spending” on entitlement programs to consume more than 60 percent of the federal budget.

The federal budget is what Congress wishes it to be. If 60% is too much, the government merely can increase discretionary spending. This would reduce the meaningless percentage and increase the Gross Domestic Product.

Economic growth is both a direct and indirect result of federal spending. GDP=Federal Spending + Nonfederal Spending + Net Exports

Of course, because those programs are funded with a separate revenue stream—payroll taxes—it would be complicated for Congress to cut spending on Social Security to offset cuts on welfare programs.

Unlike state and local governments, the federal government does not fund programs via “revenue streams.” It supports all programs by creating new dollars, ad hoc. Tax dollars are destroyed upon receipt.

Even if all federal tax collections totaled #0, the federal government could continue spending forever.

Even so, the ongoing refusal of either major party to consider any long-term changes to the two major entitlement programs tells you all you need to know about the priorities in Washington.

What tells me all I need to know about priorities in Washington is the failure of either party to get rid of tax dodges by the rich.

There is no shortage of alternative ideas out there.

Congress could fiddle with the specifics of Social Security to make the program less expensive over the long term—raising the retirement age, for example, or changing how contributions and disbursements work.

Yes, soaking the elderly is the Libertarian mantra. But they don’t ask the rich to pay more by closing tax loopholes. That would reduce those luscious political contributions the politicians love so much.

It could (and should) allow younger Americans to opt out of the system retirement.

Boehm exceeds his stupidity allowance by suggesting that younger Americans opt out of Social Security. I can’t even go into how cruel and ignorant that idea is other than saying it does not surprise me coming from Libertarian Eric Boehm.

A pox on him and his descendants ten generations, hence.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.

When supply cannot meet demand, prices go up. That’s basic.

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.

When supply cannot meet demand, prices go up. That’s basic.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.