I have been reading the Libertarian articles in Reason.com for several years and have noticed something odd. Despite ongoing claims that federal spending should be reduced, no data can support that myth.

Like all other debt Henny Pennys, they focus on telling you how big the so-called debt is and how much will be spent on benefits. OK, we get it. The numbers are significant, but why are they bad?

But there never is data. It is all speculation supported by more speculation.

The following article is no exception:

CBO Projects Huge Deficits, $116 Trillion in New Borrowing Over the Next 30 YearsA new Congressional Budget Office report warns of “significant economic and financial consequences” caused by the federal government’s reckless borrowing.Merely paying the interest costs on the accumulated national debt will require a staggering 35 percent of annual federal revenue by the end of that time frame. | 6.29.2023 11:00 AM

And what will those “significant economic consequences” be? And where is your evidence?

The federal government is on pace to borrow $116 trillion over the next 30 years, and merely paying the interest costs on the accumulated national debt will require a staggering 35 percent of annual federal revenue by the end of that time frame.

And that’s likely an optimistic scenario.

Actually, it is an optimistic scenario. Mathematically, the more the federal government spends, the more the economy grows. Why? Because the economy is measured by Gross Domestic Product (GDP) and:

GDP = Federal Spending + Nonfederal Spending + Net Exports

That $116 trillion in “borrowing” is not borrowing. It is the acceptance of deposits into Treasury Security accounts. The U.S. federal government never borrows dollars.

Why would it? The federal government has the infinite ability to create (aka “print”) dollars, so why would it ever need to borrow what it can create at no cost, especially since borrowing requires paying interest?

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Get it, Libertarians? The U.S. government is not dependent on credit markets. It doesn’t borrow.

Let me rephrase your comment: ” . . . merely paying the interest costs on the accumulated deposits into T-security accounts will require a staggering 35 percent of annual federal revenue by the end of that time frame.

Why is it “staggering” if Greenspan, Bernanke, and the St. Louis Fed say the government never can run out of dollars? Even if annual revenue totaled $0, the federal government could continue spending forever.

Those sobering figures were published Wednesday by the Congressional Budget Office (CBO) as part of the number-crunching agency’s new long-term budget outlook.

The report once again points to an unsustainable fiscal trajectory driven by a federal government that’s addicted to borrowing—even as it becomes readily apparent that the bill is coming due.

It’s Libertarian nonsense. Why is it “unsustainable”? And since the government never borrows, what is the “addiction”? And exactly what bill is “coming due”?

The problem is Eric Boehm, and the rest of the Libertarians do not wish to acknowledge the fundamental difference between personal finance and federal finance.

In short, they don’t seem to understand the difference between Monetary Sovereignty and monetary non-sovereignty. And not understanding those fundamental differences means they don’t understand economics. At all.

Are they being devious or simply ignorant? I don’t know. I vote for devious. In my opinion, they have an agenda and are just pretending to be ignorant.

“Such high and rising debt would have significant economic and financial consequences,” the CBO warns.

Among other things, the mountain of debt will “slow economic growth, drive up interest payments to foreign holders of U.S. debt, elevate the risk of a fiscal crisis, increase the likelihood of other adverse effects that could occur more gradually, and make the nation’s fiscal position more vulnerable to an increase in interest rates.”

In what way does federal deficit spending “slow economic growth” when Federal Spending increases GDP by simple algebraic formula?

As for interest payments, here’s the Libertarian theory: To acquire the dollars to pay its bills, the federal government needs to borrow. And because it needs to borrow so much, it has to raise interest rates to attract lenders.

Wrong. The government never needs to borrow and, indeed, never borrows. The Fed determines the interest it pays on Treasury Securities, not to attract lenders but to regulate the economy.

Example: Of late, interest on T-securities has gone up significantly, not because the Fed wants to attract more depositors, but because the Fed thinks that’s how to reduce inflation. Interest rates have nothing to do with the government needing dollars to pay its bills.

As for foreign holders of U.S. “debt,” that is a convenience for foreigners. The Fed doesn’t give a fig whether Russia or China deposits dollars into Treasury Bill accounts. The purpose of those accounts is not to give America it own dollars. The purpose is to provide the Russians, Chinese et al. a safe place to deposit unused dollars.

Further, what is the “fiscal crisis” the CBO worries about? The government always can pay its bills. If a creditor were to demand that the U.S. federal government pay $100 Trillion tomorrow, a functionary at the Federal Reserve would press a computer key, and the $100 Trillion instantly would be transferred to the creditor’s account.

The CBO’s erroneous claims end with: ” . . . increase the likelihood of other adverse effects that could occur more gradually, and make the nation’s fiscal position more vulnerable to an increase in interest rates.”

We don’t know what the “other adverse effects” supposedly are. We suspect the CBO has no idea, either.

Finally, the federal government’s fiscal position is invulnerable. It can pay any bill of any size at any time it chooses.

The formula for massive deficits and unsustainable levels of borrowing is actually pretty simple: federal spending that far exceeds what the government collects in tax revenue.

Because the federal government has the infinite ability to create U.S. dollars, it neither needs nor even uses tax revenue to pay its bills. So why does it collect taxes at all?

Three reasons:

To control the economy by taxing what it wishes to discourage and giving tax breaks to what it wishes to encourage.

To assure demand for the U.S. dollar and thus stabilize the dollar by requiring taxes to be paid in dollars.

To make the public believe federal spending is limited by taxes and reduce public requests for benefits

As for #3, the rich who run America do not want the non-rich to receive the benefits that would narrow the Gap between the rich and the rest. The Gap makes the rich rich; the wider the Gap, the richer they are.

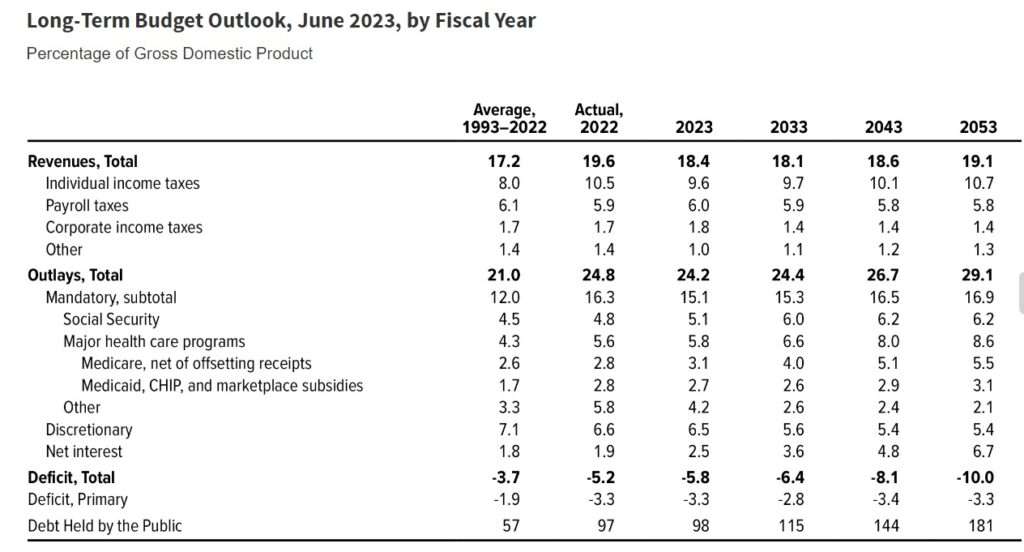

Over the past 30 years, federal spending has averaged 21 percent of gross domestic product (GDP), a rough measure of the size of the whole American economy, while tax revenue has averaged 17.2 percent, the CBO notes. That’s not great, but the future looks much worse.

By 2053, the CBO expects federal spending to grow to 29.1 percent of GDP while revenue climbs to just 19.1 percent.

From being exposed to the above table, you might be led to believe that Federal Spending/GDP or federal taxes/GDP are essential measures. They aren’t.

The first fraction tells you how much the federal government spends vs. the domestic private sector. What can you do with that information? Not much.

You might wish to increase private sector spending, probably requiring federal tax reduction, which is almost always a good idea. And you should increase exports which need federal aid to exporters, though that might run afoul of international agreements.

What you do not want to do is cut federal spending. That will only reduce GDP, which would only make it worse if you are concerned about the Federal Spending/GDP fraction.

As for the Federal Taxes/GDP fraction, the analysis is straightforward. The more significant the fraction, the worse will be economic growth. Sadly, the CBO complains that the fraction will be getting smaller — Federal Spending will grow faster than GDP — and here is the crucial part: GDP is projected to grow.

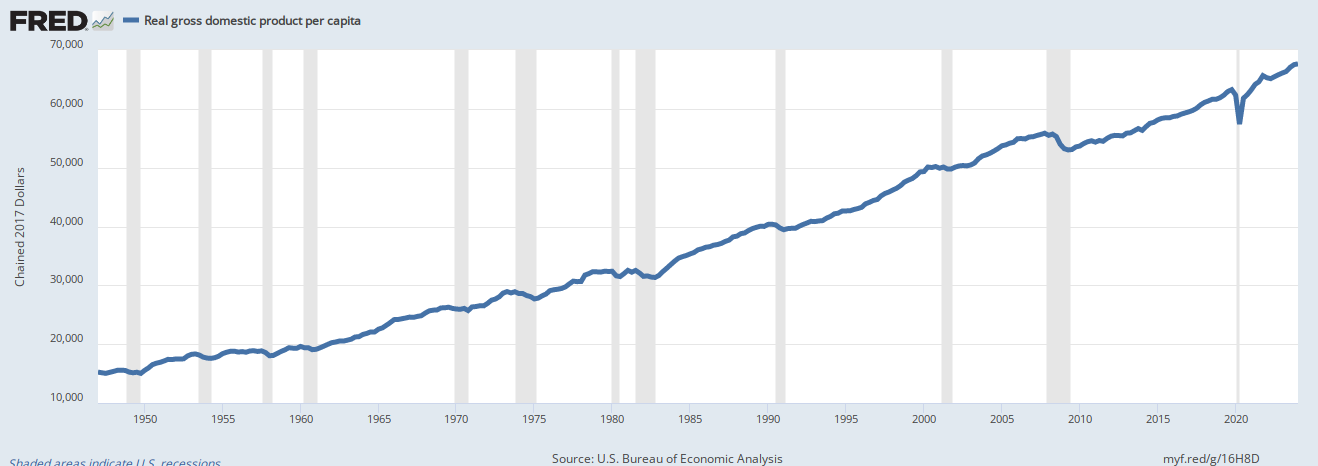

Even more importantly, real(inflation-adjusted) GDP has been growing per capita. That means despite all the moaning and groaning from the Libertarians and the CBO, Americans are getting richer. Here are the data:

Real Per Capita Gross Domestic Product

That, my friends, is a picture of a healthy economy — uh, except for this:

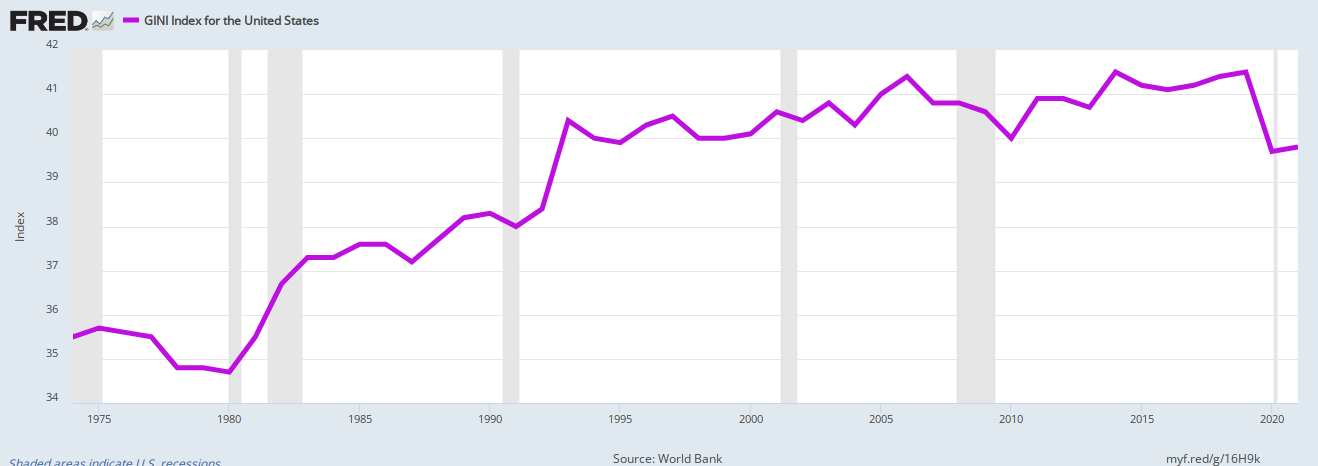

The GINI index shows the distribution of wealth. A level of “0” would mean everyone has the same wealth. A level of “1” would mean one person has all the wealth. The graph shows the rich getting more affluent than the rest of us, with only a small drop from 2019 to 2020.

Keep the GINI index in mind when you read about the Libertarians and the Republicans wanting to cut “Entitlements” (Social Security, Medicare, Medicaid), school lunch programs, and other poverty aids.

The oft-quoted Federal Debt/GDP ratio is equally meaningless. It compares the amount deposited into T-security accounts by foreign nations, domestic companies, and Americans (aka “Federal Debt) vs. the amount spent by Americans and net imports.

This ratio often is cited as something to be concerned about. Yet it has no predictive or analytic value. A low ratio is neither a sign of a healthy nor sick economy. It is not a prediction of the future nor a measure of the past.

GDP doesn’t pay for Federal Debt, and Federal Debt doesn’t pay for GDP. Yet some so-called “economists” wring their hands when the ratio increases.

The only relationship between the two is when Federal Debt increases, which helps GDP increase, though all the bleating about this ratio would make you think otherwise.

Entitlements are the primary driver of that future spending surge. Social Security spending will rise from about 5 percent of GDP to about 6.2 percent over the next 30 years. Costs for Medicare and Medicaid will jump from 5.8 percent of GDP to 8.6 percent by 2053.

And there it is. The right-wing pitch is to reduce Social Security, Medicare, and Medicaid. The purpose is to widen further the Gap between the rich and the rest.

Financing the national debt will become a major share of federal spending in the next few decades. The CBO projects that interest payments on the debt will cost $71 trillion over the next 30 years and consume more than one-third of all federal revenue by the 2050s.

As Greenspan, Bernanke, and the St. Louis Fed reminded us, it costs the U.S. government nothing to create those dollars; that dollar creation has been enriching Americans for decades.

“America’s fiscal outlook is more dangerous and daunting than ever, threatening our economy and the next generation,” Michael A. Peterson, CEO of the Peter G. Peterson Foundation, which advocates for fiscal responsibility, said in a statement.

The group responded to the new CBO report by renewing its calls for a bipartisan fiscal commission to consider plans for stabilizing the debt.

To a rich guy like Michael A. Peterson, “fiscal responsibility” means soaking the poor and middle-income groups while giving tax breaks to the rich.

Stabilizing the debt” means creating recessions and depressions, during which the rich will buy all those low-priced assets to increase domination over the rest of us.

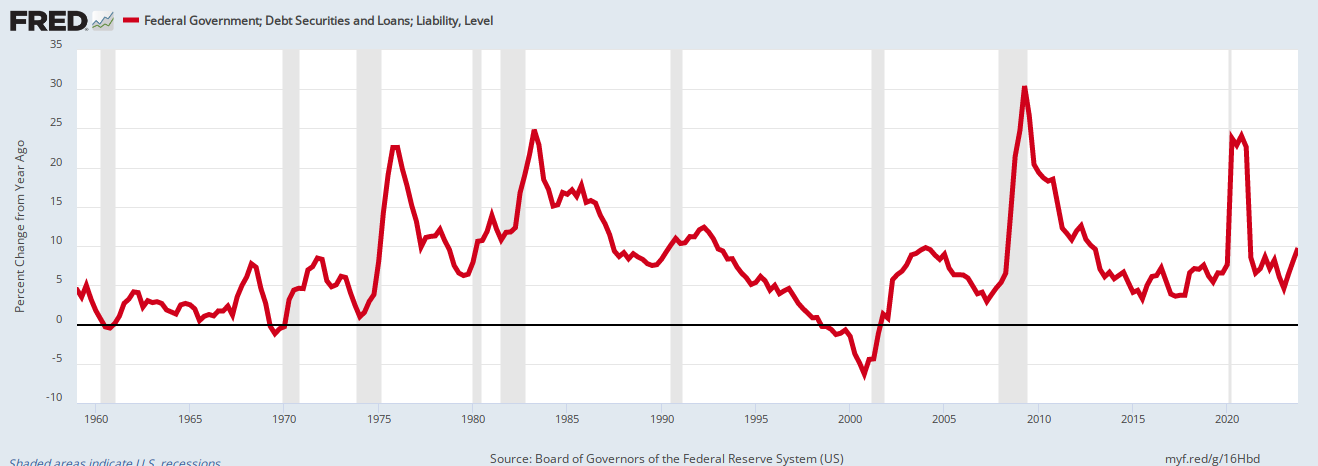

Here is precisely what happens when we “stabilize the debt” as rich Mr. Peterson wishes”

When federal “Debt” growth (red) declines (“Debt” is stabilized), we have recessions (gray bars). To cure recessions, the government increases “Debt.” GDP = Federal Spending + Nonfederal Spending + Net Exports.

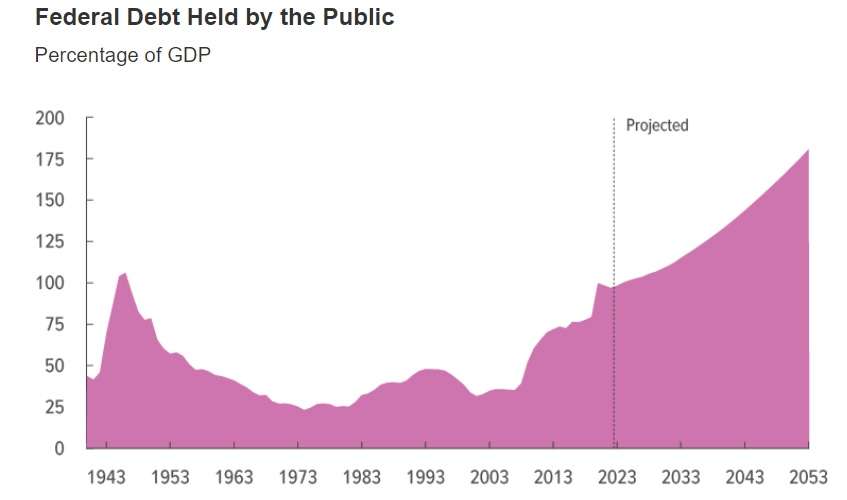

The national debt reached a record high of 106 percent as a share of GDP during World War II. The CBO projects the record to be broken in 2029, and the debt will keep climbing—to 181 percent of GDP by 2053.

A meaningless graph that tells you nothing about the U.S. economy yesterday, today, or tomorrow.

Even something called the “World Population Review” is hypnotized by this meaningless ratio. Here is what they say:

Typically used to determine the stability and health of a nation’s economy, the debt-to-GDP ratio is expressed as a percentage and offers an at-a-glance estimate of a country’s ability to pay back its current debts.

And here are the examples they give:

Top 12 Countries with the Highest Debt-to-GDP Ratios

Venezuela — 350%

Japan — 266%

Sudan — 259%

Greece — 206%

Lebanon — 172%

Cabo Verde — 157%

Italy — 156%

Libya — 155%

Portugal — 134%

Singapore — 131%

Bahrain — 128%

United States — 128%

Top 12 Countries with the Lowest Debt-to-GDP Ratios (%)

Isn’t it nice to know that all these countries — Russia, Afghanistan, Botswana, et al. — supposedly are more stable and healthy and better able to pay back their current debts than the United States and Japan?

It must be true because that is what the Libertarians, the CBO. Michael A. Peterson and the World Population Review are telling you.

So be sure to tell all your creditors not to pay you dollars because you’d rather receive Russian rubles. Right?

The (CBO’s) projections leave out the possibility that Congress will extend the Trump administration’s tax cuts past their planned expiration in 2025—which would add to the deficit and require more borrowing in the future—or the possibility that Social Security’s impending insolvency will be papered over with yet more borrowing.

The United States cannot become insolvent. Per Former Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Because the U.S. can’t become insolvent, Social Security, a federal agency, can only become insolvent if that is what Congress and the President want.

What the author calls “papered over” normal people would call “paying for,” which the government can do simply by pressing a computer key.

And do you really believe that no Congress or president will hike spending without offsetting tax increases in the next three decades?

If Congress and the President increase taxes they will not “offset” anything. Federal taxes do not fund federal spending. They are destroyed upon receipt, and new dollars are created ad hoc to pay for expenditures.

Under an alternative scenario in which the Trump administration’s tax cuts are extended, and federal spending grows at the same rate as the economy (rather than in line with inflation, as the CBO assumes), the Committee for a Responsible Federal Budget projects the debt to hit 222 percent of GDP by 2053.

And that 222 percent will have no meaning.

There’s one shred of good news inside the CBO’s latest report, however. Compared to last year, long-term borrowing is expected to be slightly lower. That resulted from the debt ceiling deal struck last month between Congress and the White House.

The deal included spending caps on nondefense discretionary spending for the next two years, and even that minimal bit of fiscal responsibility can have a measurable impact on future deficits.

This is terrible news. A limit on spending growth is, by definition, a limit on economic growth. Could you remember the formula for measuring the economy?

Still, the modest decline in future deficits mainly illustrates the daunting size of the federal government’s debt problem. By 2053, the debt will more than double the size of America’s economy—and, again, that’s only if you assume borrowing won’t increase for any reason in the next three decades.

“This level of debt would be truly unprecedented,” said Maya MacGuineas, president of the Committee for a Responsible Federal Budget, in a statement. “Time is of the essence; we simply cannot afford to keep borrowing at this unsustainable rate.”

May MacGuineas is another Henny Penny paid by the rich to claim that the middle and poor should receive less money.

Good heavens, one needs to learn only five simple facts, and even that seems to be too much for the economic “experts.”

Gross Domestic Product (the economy) = Federal Spending + Nonfederal Spending + Net Exports

The U.S. government (unlike state/local governments, euro nations, businesses, you, and me) is Monetarily Sovereign. It, and any of its agencies, can only run short of its sovereign currency if Congress and the President will it.

Federal taxes (unlike state/local government taxes) pay for nothing. They are destroyed upon receipt by the Treasury.

Having the infinite ability to create dollars, the government never borrows. The so-called “debt” actually is deposited into T-security accounts. Those dollars remain the depositor’s property, never used by the federal government for anything, and “paid off” by returning them to the owners.

Inflation never is caused by money creation. It always is caused by shortages of crucial goods and services, most often oil and food.

If you understand these five facts, you know more than most economists, politicians, and media writers.

Just five things. Is that so hard?

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Background: The Cato Institute is an American libertarian think tank, founded as the Charles Koch Foundation.

It supports lowering or abolishing most taxes, opposition to the Federal Reserve system, the privatization of numerous government agencies and programs including Social Security, the Affordable Care Act, and the United States Postal Service, along with adhering to a non-interventionist foreign policy.

Reason is an American libertarian monthly magazine published by the Reason Foundation. Peter Suderman works for Reason.

Libertarianism tends toward anarchy; seemingly any level of government ownership or control, no matter how small, is considered too large by libertarians.

The following article perfectly illustrates the libertarian worldview:

The Warren worldview of ill-founded economic pessimism is both bloodless and moralizing.

PETER SUDERMAN | FROM THE OCTOBER 2019 ISSUE OF REASON

At the heart of Elizabeth Warren’s campaign for president—and of her entire career as a politician and public intellectual, are two simple ideas.

The first is that the economy is fundamentally broken. She declared that “millions and millions of American families are also struggling to survive in a system that has been rigged by the wealthy and the well-connected” and in which she insisted that the only response was to fight for “big structural change.”

She inveighed against corporate profits and monopolistic businesses and corrupt lawmakers who have “made this country work much better for those who can make giant contributions, made it work better for those who hire armies of lobbyists and lawyers, and not made it work for the people.”

It was present in the 2007 essay that imagined what would eventually become the Consumer Financial Protection Bureau, a federal agency premised on the notion that American families were being “steered into overpriced credit products, risky subprime mortgages, and misleading insurance plans'”

She proposed an array of economic policies, from a $15 minimum wage to enforcing restrictions on certain bank loans, that she argued could stave off the crisis.

(She issued a) slew of white papers and policy proposals that have poured forth from Warren’s campaign as if she were running a think tank rather than a presidential bid.

It’s her own fault. Don’t ask for government help.

Apparently, libertarian Suderman doesn’t believe that “millions of American families are also struggling to survive in a system that has been rigged by the wealthy and the well-connected” and “this country works much better for those who can make giant contributions, and for those who hire armies of lobbyists and lawyers.”

He is living in a libertarian dream world.

He doesn’t like that Warren has proposed a $15 minimum wage, up from the current federal minimum of $7.25 hour — barely survivable for a single person, and poverty-level for supporting a family.

Libertarian Suderman doesn’t like that Warren wants to restrict the terrible bank loans that contributed to the “Great Recession of 2008.”

Suderman doesn’t like that Warren has issued “white papers and policy proposals,” rather than merely promising generalities and American greatness.

In the space of just a few months this year, Warren released plans for everything from ending drilling on public lands to breaking up Facebook and Amazon.

And she has proposed paying for these costly programs with wealth taxes designed not only to offset the price tag of new government spending but to help reduce economic inequality by shrinking large stores of wealth.

To Suderman, ending drilling on public lands, providing affordable housing, canceling student debt, and offering free college tuitions — i.e. ideas to narrow the Gap between the rich and the rest — are terrible.

Unworkable, because “wealth” is far too easy for the truly wealthy to hide.

Warren’s penchant for wonky policy detail has defined her candidacy: “Elizabeth Warren has a plan for that” has become a rallying cry and a slogan, one her fans have plastered across an array of T-shirts and campaign signs.

Warren has happily embraced this persona, joking with crowds that her focus on the details of federal agencies would turn them all into nerds.

Heaven forbid that a candidate supplies plans and details. To Suderman, it would be far better to offer bland Trump-like generalities, like “Repeal and replace ACA”” and “Build the wall” than to provide specific, people-friendly details.

Warren wants the federal government to be the American economy’s hall monitor, telling individuals and companies what they can and can’t sell or buy and making some of the nation’s most successful businesses answer to her demands.

Being the economy’s “hall monitor,” i.e. preventing miscreants from stealing, is exactly what the federal government should do.

And oh, horrors, telling the nation’s most successful businesses what dishonesty not to commit, is unthinkable to Suderman, who seems to believe that “liberty” means allowing big business to do whatever it pleases.

It seems to be working. During the first six months of 2019, this strategy vaulted Warren into the top tier of Democratic primary contenders, helping her raise more than $19 million during the year’s second quarter and placing her among the top three or four candidates in the party’s crowded field.

Focus groups and political reporting have consistently found that Democratic voters are warming not only to the substance of Warren’s ideas but to the very fact that she has them.

Well yes. Having ideas and detailing them, not only is good politics, but it is good governance. Would that more politicians did it.

Although she has received kudos for the volume and specificity of her plans, Warren has a history of pushing misleading research and cherry-picked data designed to support politicized conclusions.

Warren first rose to prominence as the co-author of a pioneering study of consumer bankruptcy, which was published in book form in 1989 under the title As We Forgive Our Debtors: Bankruptcy and Consumer Credit in America.

Warren and her co-authors based the book on a trove of court data from about 1,500 bankruptcy cases in Pennsylvania, Illinois, and Texas during 1981.

The book relied on real-world case studies. Warren statistically analyzed a trove of unique data. She was telling a story to make an argument about politics and policy.

The story was that rapacious credit card companies, rather than consumer overspending, were primarily responsible for a run-up in consumer debt and the resulting sense that household budgets had grown more precarious.

The book’s authors saw bankruptcy in broadly sympathetic terms, as a financial safety net for struggling families. In the years that followed, Warren would go on to become one of the nation’s most prominent advocates of making bankruptcy easier, more lenient, and more accessible.

But that story had some notable problems. Among others, it was based on cases from 1981, a recession year when consumers would have looked worse off than usual. It was released years later, after a significant reform to the bankruptcy code in 1984 rendered its picture of American bankruptcy somewhat out of date.

Here, Suderman criticizes the currency of Warren’s bankruptcy research, none of which has anything to do with the currency of her above-mentioned economic recommendations.

It’s as though Suderman would hate her ideas for child-rearing because her book on auto repair is out of date. In short, Suderman’s criticism is inane and utter nonsense.

And note the words, “rather than consumer overspending.” They illustrate the libertarian belief that poor people are responsible for their own misfortune.

Warren drew on her bankruptcy research to argue that the middle class had been given a raw deal.

The number of households filing for bankruptcy had shot up dramatically, she said, and it wasn’t because they were spending too much.

Instead, the increasingly high cost of housing, driven heavily by competition for access to good schools, and the pile-up of medical debt were driving families into dire straits.

It is the high cost of living, not just housing, has driven families into dire straights.

Again, Suderman wants to “prove” Warren is completely wrong, by trying to nit-pick a point of data, when her overall conclusion (that the Gap between rich and poor has widened, and many families are in financial trouble and need protection) is correct.

These effects were compounded by the movement of women into the workforce.

Where stay-at-home wives had once served as a safety net—the earners of last resort should a breadwinner husband lose his job—the rise of the working mother had increased financial risk for two-earner families.

The book’s findings were marked by controversy and unanswered questions about the soundness of her methodology. In particular, Warren’s notion that housing prices have been pushed upward by school competition doesn’t fully stand up to scrutiny.

Although research has found that school quality does impact housing prices, the effect is fairly modest. A 2006 study in the Quarterly Journal of Economics found a 2.5 percent increase in home prices for every 5 percent increase in test scores.

And in what way does the so-called “fairly modest” difference in home prices negate Warren’s position on student debt, mortgage supervision, family bankruptcy, the minimum wage, and the prevention of financial cheating by large companies?

It doesn’t, but Suderman tries to make his point by fixating on minutia to distract you from the main point, that middle-class families are struggling, and the very purpose of government is to improve the lives of its citizens.

And then there’s the role of taxes. In the book’s hypothetical comparison budgets, Warren presents taxes as a percentage of household income—24 percent in the 1970s, 33 percent in the 2000s—which the book describes as a 35 percent change.

Yet as George Mason University law professor and consumer finance scholar Todd Zywicki has noted, the choice to render taxes only as a percentage of income has the effect of masking the total dollar value.

Using Warren’s own figures, Zywicki calculated that the tax increase—owing partly to the hypothetical family hitting a new tax bracket and partly to the imposition of additional state, local, and property taxes over time—was by far the largest factor affecting the modern family’s budget.

Warren’s numbers, in other words, showed that families had been strapped not by increased spending on homes or health insurance but by a bigger tax bill.

Yes, taxes on the middle classes are too high. So, how does that eliminate the need to follow Warren’s proposals? Again, it doesn’t. It’s just another Suderman diversion.

Zywicki is among Warren’s most outspoken critics, and he has made this case—that Warren’s data do not show what she claims they do about the plight of the middle class—on multiple occasions over the span of more than a decade.

What Suderman fails to mention is that Zywicki is a senior fellow, paid by the Cato Institute, that aforementioned libertarian think tank, which spends its time and money trying to prove that government not only is unnecessary but a hindrance to America.

Zywick is not exactly an impartial commenter.

Warren co-authored a Health Affairs study purporting to show that at least 46 percent of the nation’s bankruptcies were a result of medical bills, a figure she subsequently updated to 62 percent.

Her research claimed that medically induced bankruptcies had increased a shocking 23-fold since 1981.

President Barack Obama warned that sky-high medical costs had forced many Americans to “live every day just one accident or illness away from bankruptcy.”

One wonders, what is the fundamental point Suderman is trying to demonstrate? That sky-high medical costs are not a serious financial problem for millions of Americans?

The response by Warren and her co-authors was revealing. In one sense, they were engaged in a conventional academic dispute about interpreting bankruptcy data. But what they were really fighting about—what was really at stake—was public policy.

Warren clearly believed that the value of her research was in the story it told and the way that story informed and influenced the real world of politics and public affairs.

Yes, that exactly is the point. What does it matter whether housing prices, or school costs, or medical costs are most responsible for bankruptcies or other forms of financial distress?

The point that Suderman doesn’t want you to understand is that these are problems the federal government can and should address. It has the means, if only it had the will.

Sadly, the Sudermans of the world would rather quibble about differences in data than to solve the clear and obvious problems that plague us.

Yes, some things are more troublesome than others, but that does not mean we should stall. while people suffer, debating how much more troublesome school costs are than medical costs.

But perhaps, stalling is what Suderman wants.

In the aftermath of the 2007–08 financial crisis, Congress, then controlled by Democrats, passed the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was billed as a direct response to the economic meltdown and an attempt to make sure it never happened again.

A centerpiece of the bill was the creation of a new federal agency, the Consumer Financial Protection Bureau (CFPB), which was modeled on Warren’s original proposal.

The bureau, as imagined by Warren, was premised on the notion that consumers did not and in some cases could not understand the financial services they relied on, and that only an army of unusually powerful government bureaucrats could save them from blundering into the tricks and traps set by lenders.

And that is absolutely correct. Left to their own designs, the banks created the most convoluted, complex financial products, that no one, not even Suderman, could understand, then sold them to the public, with disastrous results.

The CFPB’s mission, meanwhile, was far more expansive than its origin story might imply. From payday lenders to cash advance services, many of the financial products it was given the power to regulate had little or nothing to do with the financial crisis.

Suderman’s senseless point seems to be that if a financial scam had nothing to do with the Great Recession, it should be ignored.

The CFPB was the culmination of decades of research and advocacy on Warren’s part. She had imagined it, fought for its creation, and then, from her perch in the administration, ushered it into being.

And yet there was a kind of victory as well, in the simple fact of the CFPB’s creation. Warren would not be its leader—that role would eventually go to former Ohio Attorney General Richard Cordroy, who was given a recess appointment that caused its own controversy—but she had willed it into being and would continue to provide spiritual guidance.

She did not achieve her political ambitions, but on the policy question, she had triumphed.

In the years that followed, something strange happened: Warren, the icon of progressivism whose political brand had proven too toxic to move through the CFPB nomination process, became the object of a strange new respect from the right.

Apparently, being respected by some right-wingers is a curse for Suderman.

Under President Donald Trump, in July, The American Conservative, long a bastion of immigration-skeptical conservative nationalism, ran an essay extolling Warren’s economics, particularly her plans for a new bureaucracy dedicated to “defending good-paying American jobs,” and saying that in some respects, “Warren may be a bigger economic nationalist than even Trump himself.”

A paragraph of utter nonsense, but what else can one expect in political discourse?

Nor is Warren’s popularity limited to small opinion journals.

In June, Fox News’ Tucker Carlson, among the most-watched hosts on cable news and an influence on the Trump administration, opened his show with an extended monologue praising Warren’s domestic jobs plan and its elevation of “economic patriotism,” which calls for, in the senator’s words, “aggressive new government policies to support American workers.”

“Many of Warren’s policy prescriptions make obvious sense,” Carlson said. “She sounds like Donald Trump at his best.” Later, at a conference in July, he praised The Two-Income Trap as “one of the best books I’ve ever read on economics.”

Suderman’s position is if a right-winger likes any of her recommendations that is prima facie evidence she is not a progressive. It’s wrong and a bit goofy, but it’s Suderman.

But then, the quick reversal:

It is hard to imagine the Republican Party ever embracing Elizabeth Warren. Trump frequently mocks her claims of Native American heritage, and the congressional GOP continues to view her with deep hostility. She’ll never be an ally to the party.

But in some increasingly influential corners of the right, her ideas and her outlook are winning.

The rest of Suderman’s long article is a rehash of his “unaffordability” claim about her proposals, and his dislike of the detail with which she presents them.

But “unaffordability” is a false claim concerning federal spending, and quibbling about the details rather than solving the big-picture problems solves nothing.

SUMMARY Government is created by the governed to improve their lives. That is the purpose of government.

Peter Suderman is a classic libertarian, a hater of government. As a libertarian, he wastes more than 6,000 words denying the obvious — that for many people, good schooling, good housing, good food, and good medical care are unaffordable and that the banking industry has cheated millions of innocent people.

Suderman denies that many families are driven into bankruptcy by trying to pay for the abovementioned schooling, housing, food, and medical care, or eschewing bankruptcy, they must forego these life necessities.

Suderman also hints at the libertarian’s “bootstraps” theory, in which the victim is blamed for not earning enough, or being frugal enough, or smart enough to pay for their own needs.

To libertarians, “liberty” means freedom from government help. People should pull themselves up by their bootstraps, rather than depending on the government.

Then he applies the libertarian, “Catch 22” objection to deny people those bootstraps by implying that the $15 minimum wage is a bad idea. “Gotcha!”

In the real world, our “bootstraps” consist of things like a good education, good health, good housing, and money — all of which the federal government can and should provide — and all of which libertarian Suderman would not provide.

Why does libertarian Suderman deny the obvious?

Because to admit it would require him to offer solutions, and those solutions inevitably require federal spending — an anathema to libertarians.

Warren’s proposals are fact-driven and logical, which Suderman dismisses as “bloodless.” Her proposals also benefit the poor and middle classes, which Suderman dismisses as “moralizing.”

Suderman and the libertarians live in a harsh mythical world, where there is no allowance for poverty, people are expected to be born with all they need to succeed, and it only is laziness that prevents them from realizing their dreams.

Asking for help from the government supposedly is a moral and financial imposition on the rest of us who, of course, are self-sufficient.

It is the ultimate expression of Gap Psychology, in which people wish to widen the income/wealth/power Gap below them.

I often have been asked, and I have asked myself, “What is the ongoing, seemingly unshakable appeal of Donald Trump to his followers?”

Given the repeated evidence of his immorality, his ignorance of facts, his compulsive lying, his illiteracy, his cruelty, and his favoring the rich over the middle and poor, one would think that his base – primarily middle-class whites — would be shocked and disillusioned.

His “love” for, and defense of, such murderous dictators as Vladimir Putin, Kim Jong-un, and Rodrigo Duterte.

His, his family’s, and his associates’ secret, unpatriotic, and illegal relationships with Russia, the purpose of which were to enrich Trump at the expense of America. (Example: Trump Had Yet Another Secret Meeting With Putin)

And so many more scandals, any one of which ordinarily would have led to immediate impeachment or at least to loss of backers.

Yet despite all these scandals, Trump sails on, his poll ratings hardly changed.

Why does his base, those self-proclaimed religious, law-and-order folks steadfastly continue to support an irreligious, lying law-breaker?

I believe the answer can be found with the most powerful of all human emotions, “hatred.” Very simply, Trump professes hatred for the same people his base hates.

Hatred is so powerful because it is founded into our primary survival instinct, fear.

Trump’s base hates immigrants, especially brown-skinned immigrants, because of fear.

Trump has tapped into this fear by claiming these men, women, and children are rapists and murderers.

Trump stokes “fear of the other,” and brown-skinned aliens are “the other.”

Atomic-weapon-armed Russia and North Korea, Trump’s latest pals, are far greater threats to America than are Muslims.

But Muslims, too, are “the other.” As are gays, and the media (aside from Fox news) Trump’s other whipping boys.

Trump has taught his base to fear them all, which is why they are so ready to hide behind a Wall.

The notion that huge, powerful America needs a big, strong wall to protect us from families seeking shelter in the storm — that notion is ludicrous and sad.

But, facts don’t matter to blind fear.

Ironically, Russia’s Putin and North Korea’ Kim, whom Trump claims to admire, are the ultimate “socialists.” Yet “socialism is the very epithet Trump uses against Democrats.

Amazingly, Trump’s base supporters, whom he himself derides as, “less educated,” do not seem to see the contradiction.

Things could change, however. In his never-ending effort to take from the poor and give to the rich, Trump continues to propose ending the Affordable Care Act (which has the nickname Trump hates most, “Obamacare,”)

Trump would love nothing more than to replace it with a program that rewards the rich insurance companies, cuts benefits to the poor and middle, and carries the name “Trumpcare.”

A Trumpian home run with the bases loaded.

But his greed may have outweighed his fear-founded plan, because if there is one thing even the densest of his base fears, it’s not having affordable health care for themselves and for their children — the very people Obamacare helps most.

Yes, the entire GOP (the party of the rich) always wants to cut Social Security and Medicare and all poverty-related programs, so as to widen the Gap between the rich and the rest.

And because the Democrats, so far, have gone along with that scam, Trump’s base has too.

But the Dems have awakened to the special place that healthcare occupies on the “fear meter,” especially when combined with the fear of affordability, and belatedly, the Dems have begun to fight.

Now Trump is torn. Does he please the rich, while putting his ego on a government program, or does he help the people of his base by providing them with affordable health care?

So far, he has chosen the rich and his ego over his base, as he wants to destroy Obamacare.

Now he waits for the Supreme Court to save him . . . by ruling against him. If that is the Court’s ruling, Obamacare will survive.

But if the Court rules in favor of Trump, millions of the poor and middle-income men, women, and children, will lose affordable healthcare, and Trump and the GOP will justifiably be destroyed in the next election.

Think of millions of working families who rely on their employer to provide affordable healthcare insurance.

If they get sick and lose their jobs, they also will lose healthcare, and won’t be able to buy it because they now will have a pre-existing condition.

Think of all those children, up to the age of 26, who have affordable healthcare because they are on their parents Obamacare policies. They too, will suffer.

As I sit here, I wonder what I truly wish for. Do I want to see Obamacare saved, and have a criminal President and a compassionless political party survive?

Or do I want to see the Supreme Court destroy Obamacare and have the GOP and Trump meet their deserved end, while millions suffer?

Damn Trump to hell for forcing that decision on my heart.

The most important problems in economics involve the excessive income/wealth/power Gaps between the richer and the poorer.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps:

Each day, Donald Trump demonstrates his character by disparaging some American, while professing love for a murderous dictator. Recently, the focus of his ire has been Senator John McCain, a man deceased for months, unable to fight back — the perfect victim for a coward.

Though some may debate whether Senator John McCain was, or was not, a “war hero,” there is a certain irony in a “bone-spur,” draft dodger claiming that a fighting soldier is not a hero simply because he was captured and tortured for five years.

John McCain

Clearly, neither Trump nor his followers understand that irony nor the irony of Trump’s other reason for hating the long-deceased McCain:

McCain’s decision to vote down the health care bill sponsored by Trump’s friend Sen. Lindsey Graham, R-S.C. That bill, which would have passed had McCain supported it, would have destroyed the Affordable Care Act (ACA), also known as “Obamacare.”

They do not see the irony of Trump’s claim that McCain “. . . was horrible, what he did with repeal and replace (of Obamacare) . . . what he did to the Republican Party and to the nation and to sick people that could have had great healthcare was not good.”

What Trump and his followers neither understand nor will not admit that with that vote, Republican John McCain saved the Republican Party and Trump’s Presidency.

In similar fashion, right-wing, Chief Justice, John Roberts, did the same:

Roberts had left behind a storm in Washington over his opinion upholding President Barack Obama’s health-care overhaul — the Affordable Care Act — a stunning validation of Obama’s signature domestic achievement that transformed public perceptions of the chief justice.Republicans in Congress had been fighting the law dubbed Obamacare at every turn for two years, and all the GOP presidential candidates in 2012 had vowed to repeal it.And now Roberts, a nominee of President George W. Bush, had saved it.

How did these two men save the Republican Party and Trump’s Presidency by voting against the Republican Party and Trump?

Because in their zeal to repeal all things Obama, the Republicans and Trump neglected to develop a “replace” that reduced or eliminated many of the coverages of the ACA. For example (from BBC):

Obamacare: Requires all insurance plans to cover certain health conditions and services, such as emergency room visits, maternity and postnatal care, cancer treatment, annual physical exams, prescription drug costs and mental health counselling.

Republican plan: States may apply for waivers that allow them to end mandatory coverage of certain health conditions, such as vision and dental care for children, hospital care, and outpatient services. States that receive such waivers could allow insurers to set a maximum amount they will pay for an individual’s medical services – a practice that Obamacare had prohibited.

Obamacare: Prohibits insurers from denying coverage or charging more to individuals who have pre-existing medical conditions.

Republican plan: Gives states the ability to opt-out of requirements that insurers charge the same premiums for healthy and sick customers.

Obamacare: Expanded Medicaid health insurance for the poor to cover more low-income individuals.

Republican plan: “Block grants” that are capped based on a state’s population and whose growth is limited. 34 states would see reduced government support for Medicaid and tax subsidies for individuals purchasing health insurance.

Obamacare: Insurers can charge older Americans no more than three times the cost for younger Americans

Republican plan: States can receive waivers to allow them to charge older Americans more.

In short, the Republican plan offered fewer benefits and dumped many of the costs onto the monetarily non-sovereign states, which must increase taxes if they are to afford to improve health care support.

(By contrast, the federal government, being Monetarily Sovereign, has the unlimited ability to create dollars, and can support any health care plan without raising taxes.)

The Republicans actually had years in which to come up with a suitable and superior replacement, and they failed. Trump, of course, did nothing other than to tell the Party that he was waiting “pen in hand.”

Since any replacement would involve more than a single sheet of paper, Trump’s lack of reading, writing, or comprehension skills did not allow him to participate.

So had the Republicans succeeded, they would have failed. That is, by destroying Obamacare, and leaving millions of people without affordable health care, they would have turned the vast majority of the nation against the right-wing.

Today, they are left in the politically enviable political position of being able to stand on the outside and throw rocks, without having done a single positive thing to help the masses receive health care.

And it was the two Johns, McCain and Roberts, who gave them that ironic gift.

Meanwhile, the Democrats failed by succeeding. They receive scant credit for saving Obamacare, and they saved the Republicans from disaster.

Instead, they now must fight the “Medicare for All” battle, and once again the Republicans with throw “socialism” stones without offering a good alternative plan.

The most important problems in economics involve the excessive income/wealth/power Gaps between the richer and the poorer.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps: