This paper comes at a significant moment in our history.

The purpose of government is to improve and protect the lives of a nation’s residents. But here is why the American government can’t do that job:

In his March 1, 2022, State of the Union speech, President Biden promised to reduce the federal deficit and debt.

The audience stood and cheered, not knowing or not caring that what he really told them was, “I’m going to cut the net amount of money the federal government will send into the economy, and if I succeed, we’ll have a recession or depression.”

“Reduce the federal debt” means “take dollars from you Americans and give them to the federal government.” Is that something to cheer about?

Or is the need to cut the federal debt just a Common Myth?

Economics is filled with Common Myths that have no basis in data. For example:

Common Myth: The federal government should handle its finances like you and me.

Reality: In the beginning of the U.S., the federal government created laws from thin air, and some of those laws created the U.S. dollar from thin air.

There was, and remains, no limit to the number of laws the government can create, just as there was, and remains, no limit to the number of dollars the government can create.

This fact is known as “Monetary Sovereignty.“

Unlike state and local governments, unlike businesses, and unlike you, and me, the federal government cannot unintentionally run short of its own sovereign currency, the U.S. dollar. The U.S. federal government has available to it, infinite dollars.

The government creates dollars ad hoc, by paying its bills. The more bills the government pays, the more dollars it creates.

To pay a creditor, the government sends instructions, in the form of checks or wires (“Pay to the order of”), to each creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

The instant the creditor’s bank obeys those instructions, new dollars are created and added to the M1 money-supply measure.

Common Myth: The federal debt should be reduced.

Reality: The federal “debt” is not a debt of the federal government or of taxpayers. It is not even a debt. It is the total of deposits into Treasury security accounts.

These accounts resemble safe-deposit accounts, the contents of which our government, being Monetarily Sovereign and having the infinite ability to create its own sovereign currency, never needs or touches.

Just as the contents of your bank safe deposit box are not your bank’s debt, the contents of T-security accounts are not the government’s debts. They are dollars you own in your T-security account that eventually you will transfer to your checking account.

The notion of the government struggling to reduce the debt is ludicrous. Not only does the federal government have absolute control over the amount of deposits in T-security accounts, but there is no reason to reduce these deposits.

They are not a burden on the government or on future taxpayers.

Common Myth: Taxpayers or your grandchildren will be liable for paying off the debt.

Reality: When you invest in a T-bill, T-note, or T-bond, you take dollars from your checking account and deposit them into your Treasury Security account. There your dollars remain, accumulating interest until account maturity, at which time your dollars are returned to you.

The federal government does not remove those dollars for any purposes.

Returning your dollars is no burden on the government or on future taxpayers. No tax dollars are involved. Your grandchildren will not pay for the federal “debt.”

To pay off the “debt,” (which isn’t a debt) the dollars in your T-security accounts simply are returned to you. It is a simple money transfer from your T-security account to your checking account.

Common Myth: When federal taxes are not sufficient to pay for things, the federal government borrows dollars via T-bills, T-notes, and T-bonds.

Reality: The federal government never borrows. The purpose of T-securities is not to provide spending money. Rather, the sole purposes of T-security accounts are to:

1. Provide a safe, interest-paying place to store unused dollars. This helps stabilize the dollar.

2. Help the Fed control interest rates by setting the rates of interest the government pays into T-security accounts.

Common Myth: Reducing the debt would be fiscally prudent.

Reality: By law, the federal “debt” matches the net total of federal deficit spending. Because federal deficits add dollars to the economy, they are economically stimulative.

Every time the debt has been reduced, we have a depression or recession.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Even when the debt growth rate declines, we have recessions. Recessions are cured by increased deficit spending, i.e. debt growth increases.

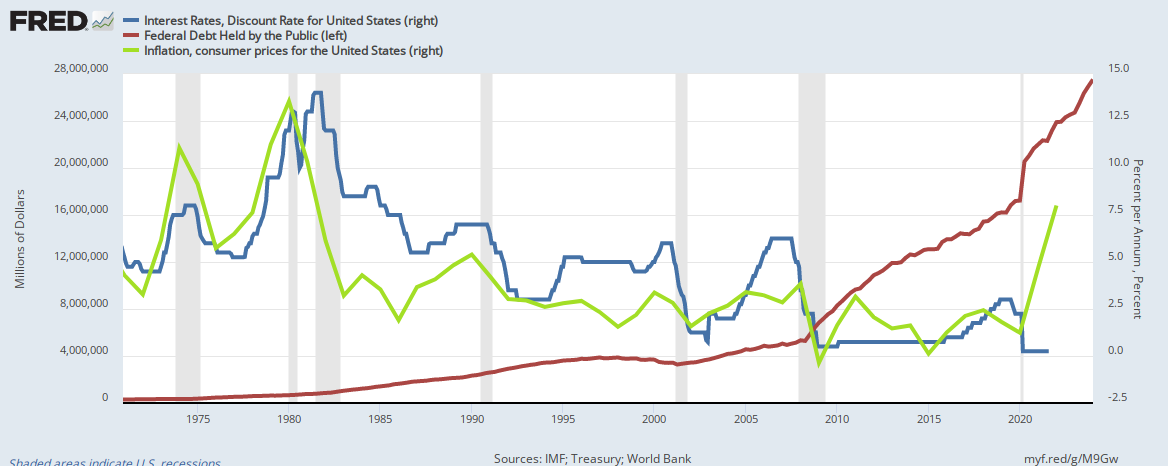

Recessions (vertical gray bars) follow decreases in federal debt growth. Recessions are cured by increases in federal debt growth.Common Myth: Federal deficit spending can lead to inflation

Reality: No inflation in history has been caused by government adding dollars to the economy. All inflations have been caused by shortages of key goods and services.

Inflation (red) is not related to federal debt or deficit(blue).

Massive government spending had been going on for many years without inflation. Yet suddenly, today, we have inflation. Why?

The spending did not cause inflation yesterday, nor did spending cause today’s inflation. Today’s inflation, and all past inflations, are is caused by shortages — in today’s case, shortages of energy, computer ships, shipping, food, labor, etc.

Today’s inflation can be cured by government spending to encourage energy production, computer chip production, shipping, and farming.

Labor can be encouraged by the reduction of the FICA tax and income taxes, both of which make jobs less attractive by reducing net income.

We have recessions (gray bars) when federal debt declines. Recessions are cured by debt increases.

Debt/GDP has no relationship to inflation. There is no historical relationship between changes in federal debt and changes in inflation.

Common Myth: The Debt/Gross Domestic Product fraction is too high.

Reality: The Debt/GDP fraction is meaningless. It neither determines the current, nor the future health of a nation’s economy.

Today, Japan’s ratio is above 200%. The U.S. ratio is near 100%. By contrast, Russia’s, Chile’s, Libya’s, Qatar’s and others are below 10%, all of which tells you nothing about their economies but says a great deal about the meaningless Debt/GDP ratio.

There is no relationship between Debt/GDP and the health of an economy.

The Debt/GDP ratio does not indicate “the country’s ability to pay back its debt.”

Mathematically, the fraction makes no sense. “Debt” is the net total of all federal deficits for the past 250 years. GDP is a one-yearmeasure of all spending by both the public and private sectors.

A 250 year measure cannot be compared to a one-year measure. Further, the whole nation’s spending on goods and services, has no relationship to the federal government’s ability to transfer dollars from T-security accounts at the FRB to checking accounts at private banks.

The fraction also does not take into consideration Monetary Sovereignty. Some nations have it; others don’t. The fraction may have some meaning for monetarily non-sovereign entities, but for Monetarily Sovereign nations it is completely meaningless.

Common Myth: The Social Security and Medicare Trust Funds will run short of dollars unless taxes are increased or benefits are decreased.

Reality: These so-called “trust funds” are not real trust funds and federal taxes do not fund federal spending.

In fact, federal taxes (unlike state/local taxes, are destroyed upon receipt by the Treasury.

(Being Monetarily Sovereign, the government has infinite dollars. When you pay taxes, you take your dollars from your checking account, which is part of the M1 money supply. Because the government has infinite dollars, they are not counted as any part of any money supply, so your federal tax dollars cease to exist in any money measure. They effectively are destroyed. State/local tax dollars continue to exist, however, because those governments are not Monetarily Sovereign.

In summary, the false notion that the federal government must be “prudent” in its creation and distribution of dollars to the private sector has prevented Social Security for All, Medicare for All, Free College for All, repair of our infrastructure, support for science and exploration, and many other programs that would help narrow the Gap between the rich and the rest.

Common economic myths prevent the federal government from using its Monetary Sovereignty to improve and protect the lives of Americans.

The President of the United States lied about basic economics. It simply cannot be due to ignorance. He is surrounded by the most prominent economists in America.

Surely, he knows that what he said was myth. We only can assume:

He is afraid to tell the truth because he feels the American public will not believe the truth, or

He is lying to protect rich donors who do not want the public to know the government has the unlimited ability to provide Gap-narrowing benefits.

Take your pick.

[Why would any sane person take dollars from the economy and give them to a federal government that has the infinite ability to create dollars?]

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

Cameron Craig: “Libertarians are non-interventionists and strong advocates for property rights, free immigration, legalizing all drugs and prostitution.“Libertarians are against taxes, any form of social benefits and believe everyone must pull themselves up by their own bootstraps.“The core tenet of libertarianism is that one’s liberty and right to own property should never be infringed upon.

Reason.com, is a voice of Libertarianism. Read what they say about the National “Debt.”

Immediately, you see that Eric Boehm is spouting ignorance, and I’m not referring to his incorrect use of “are” rather than “is.”

The national “debt” isn’t a priority; it shouldn’t even be a mild concern.

In fact, it’s not “debt.”

It’s the total of deposits into Treasury security accounts, which resemble interest-paying, bank safe-deposit boxes.

When you invest in a T-bill, T-note, or T-bond, you deposit your dollars into your T-security account.

The federal government neither needs, uses, nor touches your dollars, and when your account matures, your dollars are sent back to you.

No tax dollars are involved.

As with the contents of safe-deposit boxes, the government doesn’t owe anyone the deposits in T-security accounts. Neither do you owe them. Nor do your grandchildren owe them. They are not a financial burden on anyone or anything.

So why would a thinking person tell you they are a “priority”?

And as for so-called “deficits,” they represent the net growth dollars our Monetarily Sovereign government pumps into the economy.

The U.S. government hasinfinite dollars to give; the economy needs growth dollars in order to grow. Without federal “deficits” we have recessions and depressions, all of which are cured by “deficits.”

Recessions (vertical bars) follow REDUCTIONS in deficit growth. Recessions are cured by INCREASES in deficit growth.

Mr. Boehm’s article begins with faulty premises, and only goes downhill from there. He asks:

How are we actually going to pay for all this?

“We” (you, and I, and the government) are not going to pay for “all this.” As each T-security account reaches maturity, the dollars that reside in those accounts will be transferred to the owners’ checking accounts, upon request.

It’s a simple dollar transfer. No new dollars are needed.

And even if the federal government did owe the money, it has infinite dollars with which to pay any financial obligation.

Mr. Boehm’s (and the rest of the Libertarians’) deficit/debt concern is based on the Big Lie that federal finances resemble state/local government finances and personal finances.

But the federal government uniquely is Monetarily Sovereign, while you, all local governments and all businesses are monetarily non-sovereign.

The Libertarians don’t want you to understand that a Monetarily Sovereign entity never unintentionally can run short of its own sovereign currency. Even if the federal government collected $0 taxes, it could continue spending, forever.

(The purpose of federal taxes is not to finance spending. The purpose is to control the economy. Taxes discourage what the government doesn’t want, and tax breaks encourage what the government does want.)

The federal government does not borrow dollars. The so-called “national debt” is not a debt to be repaid.

In a letter sent on Tuesday, 24 members of the House of Representatives called on Speaker of the House Nancy Pelosi (D–Calif.) to take some small but important steps to rein in America’s out-of-control national debt.

The misnamed “national debt” (that isn’t a debt), also isn’t “out of control” and doesn’t need to be “reined in.” The federal government controls to the penny, how many T-security dollars to accept from the public.

To prevent the public’s T-security account deposits from growing higher than desired, the federal government can lower interest rates. That discourages further deposits.

Or the Federal Reserve can use its infinite dollar-creation abilities to take the public’s place (what the uninformed would term “borrowing from itself.”)

Similarly, if in its wisdom, the Federal Reserve decides deposits should be higher, it can increase interest rates, or again, the Federal Reserve can increase deposits.

The source of Mr. Boehm’s disinformation is the wrongheaded belief that the federal government borrows when its tax income is insufficient to pay its bills.

That “income vs. borrowing” scenario is true of state and local governments. It also is true of businesses. And it is true of you and me. We borrow when cash at hand is insufficient.

It is not true of our Monetarily Sovereign, U.S. federal government. It has infinite cash at hand.

Here is what knowledgeable people say about Monetary Sovereignty:

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Quote from Ben Bernanke when, as Fed chief, he was on 60 Minutes:Scott Pelley: Is that tax money that the Fed is spending?Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed:“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit marketsto remain operational.”

Press Conference: Mario Draghi, President of the ECB, 9 January 2014Question: I am wondering: can the ECB ever run out of money?Mario Draghi: Technically, no. We cannot run out of money.

Messrs. Greenspan, Bernanke, and Draghi, and the St. Louis Fed, were describing Monetary Sovereignty, the unlimited ability of a Monetarily Sovereign entity to create its own sovereign currency.

The U.S. government not only has this unlimited ability, but it also has the unlimited ability to determine, by fiat, the value of the U.S. dollar, an ability it has exercised many times over the years, when fixing the dollar to varying amounts of silver and gold.

Thus, the U.S. federal government has the absolute power to control inflation.

So why do T-bills, T-notes, and T-bonds even exist?

The federal government’s spending and income are recorded in what is known as the “General Fund.”

It’s not really a “fund.” It’s just a bookkeeping record. But for historical reasons, having to do with a young nation needing acceptance for its money, this record is not allowed to have a negative balance.

It’s an obsolete law. There is no current reason why the General Fund, or any bookkeeping item can’t have a negative balance. But the convoluted workaround for this obsolete law is to pretend to borrow by issuing Treasury securities, and allowing the public to invest in them, with the balance being purchased by the government itself.

It’s all bookkeeping hocus-pocus, to satisfy an obsolete set of rules, originally designed to prevent what mathematically cannot ever happen: Unintended federal insolvency.

Today, the functional purpose for issuing T-securities is to provide a safe interest-paying parking place for unused dollars, which helps to stabilize the value of the U.S. dollar.

The letter highlights the fact that policies enacted during the past five years—including pandemic relief, but also “Congress’ perennially broken budget process and fiscal policies”—have added $13 trillion to the projected levels of debt in 2031, at the end of the 10-year window Congress uses for budgeting.

Mr. Boehm is referring to $13 trillion federal growth dollars, without which the economy would fall into the deepest depression in world history.

“It has been over a decade since Congress enacted any legislation that significantly addressed these longstanding structural problemsor improved the nation’s fiscal outlook,” the lawmakers wrote to Pelosi. “Our national debt should be a top priority for both parties and addressed on a bipartisan basis.”

The misnamed “debt” neither is a structural problem, nor a “priority,” and it has nothing to do with a “fiscal outlook.” It’s all lies.

Yes, the letter represents the view of just 24 of the House’s 435 members. Still, any discussion of the debt and the need to address it is welcome.

It is encouraging that only 24 of the House’s 435 members are misinformed or dishonest enough to sign such a letter.

The Congressional Budget Office (CBO) now forecasts that the debt will be twice the size of the economy by 2051, while the Government Accountability Office (GAO) predicts that the debt will grow to four times the size of America’s economy before the end of the century.

Here, Mr. Boehm referred to the most ridiculous, nonsensical, meaningless ratio in all of economics: The debt/GDP ratio. It is a ratio that says nothing about the health of the economy (see Debt to GDP Ratio by Country 2022). It is a ratio that predicts nothing.

It isn’t even mathematically logical, because it describes different time sequences. “Debt” is the net accumulation of deficits during the past two centuries, while GDP refers to one year.

“U.S. fiscal policy today is not sustainable,” argue Veronique de Rugy and Jack Salmon, researchers at the Mercatus Center, a free market think tank, in a new report published Wednesday. “Not only is our debt ratio at the highest level in peacetime history, but also our future budgetary outlook is even bleaker.”

The two researchers from the Libertarian Mercatus Center imply that the federal government can run short of its own sovereign currency, a fiscal impossibility. And the “not sustainable” trope has been disseminated, without evidence, since at least 1940.

See: “Your periodic reminder. After 80 years, the federal debt still is a ‘ticking time bomb.’

Libertarians were wrong then. They are wrong now. The federal “debt,” far from being a priority, or a problem or a burden on future generations, is an absolute necessity for economic growth — the larger the “debt” (i.e. net deficits), the faster the growth.

Perhaps it was the symbolic $30 trillion debt threshold that has prompted some lawmakers to call on Pelosi to take action. But another factor is the high levels of inflation America is currently experiencing. As Reason has previously explained, inflation and high debt create a trap for policymakers: higher inflation could lead the Federal Reserve raise interest rates, which would increase the payments owed on the debt.

Because Libertarians seem to think that allfederal spending is excessive, the notion that the federal government would pay more interest into the economy upsets them.

In reality however, there is no downside to increased federal interest. The government has infinite dollars, and the economy benefits from additional dollars.

Contrary to the Libertarian philosophy of ignorance, federal spending is stimulative, and also contrary to popular wisdom, not inflationary.

Inflations never are caused by “too much money.” Inflations always are caused by shortagesof key goods and services. Those shortages, and the resultant inflation, can be cured by increased federal spending to encourage the availability of the scarce goods and services.

Today’s inflation is an example: Current shortages of oil, computer chips, food, shipping, and lumber can be cured by federal aid to oil production, computer chips, farming, and lumber.

Current shortages of labor can be cured by the elimination of FICA and income taxes, which serve only to reduce the reward for work.

Fighting inflation with deficit reduction, would lead to recession.

Regardless of the reasons, the 24 lawmakers who signed this week’s letter are asking for two policies that are the lowest of low-hanging fruit.

First, they are seeking the creation of a bipartisan debt commission, similar to one implemented during President Barack Obama’s first term that helped trigger modest reductions in annual budget deficits following the Great Recession.

I’m not sure what economy Mr. Boehm lives in, but the Great Recession was cured by massive increases in federal deficit spending, which then returned to average levels, only to rise again to combat COVID.

Mr. Boehm closes his article with a summary of ignorance and disinformation:

Lawmakers are asking Pelosi to include in the budget changes to how the debt ceiling operates.

The proposed changes would allow the president to unilaterally lift the debt limit as long as Congress has passed a budget resolution that contains certain debt-reduction measures for the current year.

Raising the debt ceiling is not the same as adding to the debt. The debt ceiling merely authorizes the Treasury to borrow funds to pay for spending already approved by Congress.

Objections to increasing the debt ceiling amount to little more than a refusal to pay overdue credit card bills—a temper tantrum that doesn’t address the actual problem of overspending.

Mr. Boehm is correct that the debt ceiling doesn’t address anything, much less the mythical problem of “overspending.” Rather than recommending the end of this laughable anachronism, Mr. Boehm supports Presidential fiddling with the debt ceiling:

“(Deficit cuts) . . . won’t fix America’s fiscal mess, but they are “commonsense ideas” that “would be important steps in the right direction,” according to the Committee for a Responsible Federal Budget, a nonpartisan group that advocates for reducing the deficit.

And they are steps that the country will have to take, sooner or later. “We owe it to our children,”the lawmakers wrote to Pelosi, “to acknowledge our country’s unsustainable fiscal trajectory and work together, across the aisle, to address it over time.”

Yes, Boehm delivers a final dose of utter BS. The ideas neither are “commonsense” nor are they “important steps in the right direction.”

Our children do not owe, nor will they pay for the federal “debt.” Instead, if the debt is reduced our children will be punished by the resultant recessions and depressions.

And, the country’s “fiscal trajectory” (presumably, he means rising “debt”) is not “unsustainable.” It’s necessary. Here is what happens whenever we reduce the “debt.”

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depressionbegan 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recessionbegan 2001.

Libertarians are the kissin’ cousins of Republican conservatives. Birds fly. Fish swim. Libertarians lie. Apparently, those are three constants in nature.

Why do the Libertarians lie about the federal “debt”?

Go back to one of the tenets of Liberalism: “Libertarians are against taxes, any form of social benefits and believe everyone must pull themselves up by their own bootstraps.“

Libertarians want the federal “debt” reduced, and the easiest way to accomplish that is to cut such social benefits as Medicare, Social Security, Medicaid, poverty aids, etc.

Rather than complain about social benefits, which the populace loves (and the government has the infinite ability to provide), Libertarians find it easier to complain about so-called “debt” and deficits.

By convincing the public that “debt” and deficits must be cut, the Libertarians are able to justify cutting benefits to the middle- and lower-income groups.

It’s the backdoor way of making the rich richer by widening the Gap between the rich and the rest.

Thus, Libertarians are Republicans in disguise, pretending to be a middle-ground compromise between liberals and conservatives, but in fact, being as right wing, pro-rich, anti-middle, anti-poor as any Republican, perhaps more so.

[Why would any sane person take dollars from the economy and give them to a federal government that has the infinite ability to create dollars?]

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

[Why would any sane person take dollars from the economy and give them to a federal government that has the infinite ability to create dollars?]

The Committee for a Responsible Federal Budget (CRFB) is a fountain of misinformation, or should we say, “disinformation”?

Clearly, they are providing misinformation, i.e. wrong information, but the real question is, do they know it’s wrong, i.e disinformation?

Because they do extensive data analysis, I believe they simply must know their information is wrong. So why do they promulgate so much nonsense?

Before we answer that question, let’s see what they get wrong. Here are some excerpts from their website.

Gas Tax Holiday Would Take A Wrong TurnFEB 15, 2022 | TAXESThe White House and some in Congress are reportedly considering suspending the 18.3 cent federal gas tax for the remainder of 2022. The Committee for a Responsible Federal Budget recently estimated that such a proposal would reduce gas tax revenues by $20 billion and, without the general revenue transfer proposed in recent legislation, would advance the Highway Trust Fund insolvency date from 2027 to 2026.

Assuming their numbers are correct, what they really are saying is: “The proposal would reduce the amount of money taken out of the private sector (also known as ‘the economy’) by $20 billion.”

Adding dollars to the private sector is stimulative: taking dollars out of the private sector is recessive. In short, the reduced gas tax revenues would be a $20 Billion economic stimulus.

The CRFB seems to hate anything that stimulates the economy, especially if it directly benefits the middle- and lower-income groups as a reduced gas tax would do.

Further, the so-called Highway Trust Fund is not a real trust fund (see “The Phony Trust Fund Controversy”) and it cannot become insolvent unless Congress and the President want it to become insolvent.

The U.S. government, the creator of the U.S. dollar, cannot run short of dollars. Thus, no agency of the U.S. governmentcan become insolvent, unless that is what Congress wants.

(Former Fed Chairman, Alan Greenspan:“A government cannot become insolvent with respect to obligations in its own currency.”)

To prevent the insolvency of any agency, Congress merely passes a law that provides the agency with more dollars. Congress has the infinite ability to pass such laws.

The following is a statement from Maya MacGuineas, president of the Committee for a Responsible Federal Budget:With inflation at a 40-year high, policymakers are appropriately focused on how to bring prices under control. But new tax cuts aren’t going to stop this inflation; after all, excessive tax cuts and spending are part of what caused high inflation.

Contrary to popular wisdom, no inflation in history ever has been caused by excessive tax cuts or spending. All inflations are caused by shortages of key goods and/or services.

Interest rates (blue) and inflation (green) have trended down, while federal debt (red) has increased.

For the past 10 years, federal deficit spending has increased massively, with minimal inflation. Now, suddenly, inflation has increased. Why?

Clearly, the cause is not deficit spending, otherwise it would have happened sooner.

Inflations are caused by shortages of key goods and services..

Today’s inflation is caused by the sudden confluence of several factors, all shortages: Labor, food, gasoline, computer chips, transportation, sand, among others.

(Yes, I said “sand.” U.S. Shale Production Hindered By Sand Supply Crunch.)

While massive federal spending has been with us for at least a decade, what has changed recently to cause the sudden change in inflation from low to high?

The answer: COVID.

The worldwide impact of the disease has caused the shortages that lead to inflation.

The only thing that will cure the inflation is to cure the shortages. And that can be accomplished by more federal spending to obtain the needed goods and services:

More federal spending to encourage oil drilling and/or renewable energy.

More federal spending to support farming

More federal spending to support chip manufacture

More federal spending to support transportation

More federal spending to support hiring (i.e. the elimination of FICA taxes and the reduction of income taxes at the lower end)

Reduced federal deficit spending will lead only to recessions, as it always has.

When federal deficit spending (blue) is reduced, we have recessions (vertical gray bars), which are cured by increases in federal deficit spending.

While a gas tax holiday might provide some temporary relief, much of the benefit may flow through to oil producers or lead to higher prices in other sectors of the economy.

It makes no sense for low gas prices to cause price increases elsewhere. While low gas prices may cause an increase in demand for cars, every industry would see lower production costs, which will ease inflation.

Benefitting oil producers is not something to be avoided. Financially encouraging them to pump more oil will ease the scarcity of oil.

By boosting demand in an already over-stimulated economy, the holiday would likely boost inflation in 2023 once it ends. The holiday will also undercut the Administration’s efforts to address climate change.

The CFRB would like you to believe the economy is “overstimulated.” No one knows what an “overstimulated” economy means, but it sure sounds terrible, doesn’t it?

Presumably, it means companies are making more profits so that they will hire more people and pay more salaries to the lower- and middle income people, thereby narrowing the income/wealth/power Gap between the rich and the rest.

Presumably, it means unemployment is low, so there are fewer impoverished children and their parents, again narrowing the Gap between the rich and the rest.

“Gap Psychology” is the desire to widen the Gap below and to narrow the Gap above. All groups are subject to Gap Psychology, but the very rich are the most expert at effecting it.

As for climate change, yes, encouraging more oil production will increase climate change, in the short term. But financially encouraging more use of renewables will have long-term climate benefits.

Meanwhile, the federal government would be out $20 billion this year alone – and much more if the holiday were extended.

The federal government has infinite money. Infinite minus $20 billion, still is infinite. The federal government always will have the infinite ability to write laws, and those laws have the unlimited ability to create dollars.

The CRFB cries crocodile tears for the infinitely rich U.S. government, but no tears for you. They want you to pay the infinitely rich government more of your scarce dollars.

The Highway Trust Fund is just five years from insolvency, and the last thing we need is to cut its primary revenue source or paper over shortfalls with yet another general revenue transfer.

No, the last thing we need is liars telling us that the federal government is running short of its own sovereign currency, so you poor folks need to pony up more dollars, or receive fewer, benefits.

“Insolvency” is the big, fake bogeyman with which the rich try to scare you.

The Big Lie in economics is: “Federal taxes fund federal spending.” While state and local taxes do fund state and local spending, the federal government, being Monetarily Sovereign, does not rely on, or even use, tax dollars.

In fact, the U.S. Treasury destroys all tax dollars upon receipt. It creates new dollars, ad hoc, every time it pays a creditor.

(How does the Treasuy destroy tax dollars? The dollars in your checking account are part of the M1 money supply. When the Treasury receives those dollars, they disappear. They no longer are part of any money supply measure.They effectively are destroyed.)

Statement from the St. Louis Fed:“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills.

In this sense, the government is not dependent on credit markets to remain operational.”

Thus, the federal government has infinite dollars; it can’t run short; and telling people to give the government more and to accept less is just an example of how the Big Lie works.

As it stands, the gas tax will only cover half of highway and transit spending by the time the trust fund runs out.

In fact, the gas tax covers none of transit spending. Those tax dollars are destroyed. All federal spending, including federal transit spending, is funded by ad hoc, federal money creation.

As inflation subsides, we should either raise that tax or find a new funding source to supplement or replace it.

We don’t need to find a new funding source. And we certainly don’t need to raise taxes. The federal government is the best funding source:

Former Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

As we’ve stated, the CRFB, acts repelled by the fact that federal spending helps narrow the income/wealth/power Gap between the rich and the rest.

A well-designed carbon tax could generate ample tax revenue while substantially reducing carbon emissions and tempering excessive demand.

A well designed carbon tax might be a good idea from an ecological standpoint. But it’s a silly idea if the purpose is to give private sector dollars to a government that has the infinite ability to create dollars.

The pain Americans are feeling at the gas pump – and with rising costs throughout the economy – should be taken seriously and addressed thoughtfully.

The gas price pain will be eased by raising gas taxes??? That’s the utter nonsense the CRFB wants you to believe.

While cutting the gas tax may have political appeal, it would move in exactly the wrong direction, worsening rather than improving our nation’s economic challenges.

The rising costs should be taken seriously, which is why the cost of gasoline should be reduced — by cutting the gas tax.

Inflation takes dollars out of your pocket. The CRFB’s method of taking inflation seriously” is by taking even more dollars out of your pockets via tax increases.

Why does the CRFB act this way?

Because the rich, who run America, also run the CRFB, and support it with donations. The rich and the CRFB want to widen the income/wealth/power Gap between the rich and the rest.

The rich always wish to be richer. The only way to be richer is to widen the Gap. There are two ways the rich can widen the Gap: Obtain more money for themselves and/or make sure you have less money by paying more taxes.

Either one will make the rich richer, and the CRFB seems to be doing everything it can to reach that goal.

In that vein, I just received this Email from CRFB:

Trust Fund SolutionsFeaturing Senators Angus King (I-ME) and Mitt Romney (R-UT)

Maya MacGuineas:Paid by the rich to tell you that the federal government’s trust funds soon will be insolvent.The major government trust funds for Social Security, Medicare, and Highway spending face insolvency in the next decade-and-a-half.Policymakers need to act sooner rather than later to prevent abrupt across-the-board benefit cuts, assure a more sustainable debt path, promote faster economic growth, and achieve a number of important policy goals.

How raising taxes will help “promote faster economic growth” is a mystery the CRFB never really explains.

Trust Fund Solutions will feature opening remarks from Senator Angus King (I-ME) and a discussion between Senator Mitt Romney (R-UT) and Committee for a Responsible Federal Budget president Maya MacGuineas.The event will also feature a panel of experts, one focused on each trust fund. The Committee for a Responsible Federal Budget will also debut its new Trust Fund Solutions website and educational tools.

You can bet that the “solutions” for the mythical “Trust Funds” will involve tax increases (for which the rich will given loopholes) plus benefit decreases, both of which will widen the Gap between the rich and the rest.

Widening the Gap is what the rich pay the CRFB to do.SUMMARY

1. The Big Lie in economics is that the U.S. federal government can run short of its own sovereign currency, the U.S. dollar. Not only does the govarnment itself have access to infinite dollars, but no agency of the government can run short of dollars unless Congress and the President want that.

2. The government neither needs nor uses tax dollars, which are destroyed by the Treasury upon receipt.

3. Federal deficit spending never causes inflations (scarcities are what cause inflations). Federal deficit spending can cure inflations by curing scarcities. Reductions in federal deficit spending lead to recessions or depressions.

4. The rich grow richer by widening the Gap between the rich and the rest. Gap widening has two paths: Gaining more for the rich and/or forcing the rest to accept less.

5. The CRFB is paid to aid the rich by convincing the populace to accept Gap widening.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

Being Monetarily Sovereign, the U.S. government owns infinite dollars.

You reasonably might expect that, of all the newspapers in the world, the Wall Street Journal surely would print articles by only writers who understand federal finances.

Ah, would that it were so.

Unfortunately, some writers published by WSJ either are as ignorant as the general populace or as intentionally ignorant as the bribed-by-the-rich politicians and university economists.

Here is an example saw in a recent WSJ edition (OK, the article printed in several papers, but I read in WSJ, which should know better):

U.S. National Debt Tops $30 Trillion as Borrowing Surged Amid PandemicThe record red ink, fueled by spending to combat the coronavirus, comes as interest rates are expected to rise, which could add to America’s costs.After a protracted standoff last year, Congress agreed in December to raise the nation’s borrowing cap to $31.4 trillion.By Alan Rappeport, Feb. 1, 2022

We can’t even get past the headline and subheads without being subjected to WSJ ignorance.

Federal “debt” is deposits into accounts similar to safe deposit boxes. The federal government never touches those deposits except to return them to the owners.

The so-called “national debt” neither is “red ink,” nor is it debt. It is the total of deposits into Treasury Security accounts.

When you invest in a T-bill, T-note, or T-bond, you do not lend the federal government money. You merely deposit your dollars into your T-security account. It’s an account similar to an interest-paying, safe-deposit box.

As with a safe deposit box, the federal government does not touch your dollars. It merely stores them for you, and allows you to accumulate interest.

Upon the maturity of your account, the government “pays it off” simply by returning to you, the dollars in your account. Since the dollars already exist in your account, and remain yours, this payoff is no burden on you, on the government, or on taxpayers. It’s merely a transfer of your dollars.

If the national “debt” were a real governemnt debt, it would go something like this:

The government needs dollars to pay its bills. Federal taxes are insufficient to pay all the creditors, so the government must borrow dollars, and in return it gives the lenders its IOUs in the form of T-securities (T-bills, T-notes, T-bonds).

Later, to obtain the dollars to pay off the T-securities, the government levies more taxes. This means we taxpayers ultimately are liable for the government’s debts.

You have just read what the Wall Street Journal and the vast majority of Americans believe about the federal debt.

And it is 100% wrong.

Back in the late 1770s, the federal government created the U.S. dollar from thin air. The government simply passed laws (from thin air) that created as many dollars as it wished, and gave those dollars whatever value it wished.

The first U.S. silver dollars were coined on Oct 15,1794. On that day, 1,758 of them were produced, but no more the rest of the year.

In 1794, a new coin called the Draped Bust Dollar, featuring a matronly Liberty of considerable endowment wearing a draped blouse. Over 40,000 Draped Bust dollars were minted in 1795.

Why 1,158 and 40,000? Because the government arbitrarily based its coin on silver. Each coin contained 0.7737 oz of silver. Why 0.7737? Because the government arbitrarily made its dollar similar in weight to the Spanish dollar.

Note the word “arbitrarily.” The government could have produced any numberof dollars, and could have made them equivalent to anything it wished. The base could have been gold, lead, tin, or nothing at all.

Because we were a new country, we tried to create demand for the dollar by making it equivalent to an existing coin. But it was all arbitrary.

The federal government arbitrarily has changedthe metal content of all U.S. coins many, many times over the years.

Today, the vast majority of dollars are nothing more than numbers on spreadsheets, and have no physical existence.

The federal government retains the infinite ability to create laws from thin air, and those laws have the infinite ability to create dollars from thin air.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Quote from Ben Bernanke when, as Fed chief, he was on 60 Minutes:

Scott Pelley: Is that tax money that the Fed is spending?

Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed:

“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Read the above quotes carefully, then ask, what is Alan Rappeport talking about when he refers to the federal “debt” (i.e. deposits) as “red ink?” How can accepting deposits into T-security accounts be considered “borrowing,” when, as Greenspan, Bernanke, and the St. Louis Fed say the federal government has the infinite ability to create dollars? Why would the government ever need to borrow?It wouldn’t and it doesn’t.

WASHINGTON — America’s gross national debt topped $30 trillion for the first time on Tuesday, an ominous fiscal milestone that underscores the fragile nature of the country’s long-term economic health as it grapples with soaring prices and the prospect of higher interest rates.

It’s not “ominous.” On the contrary, it’s a sign of a growing economy. It would be “ominous” if the misnamed national “debt” were declining. That would demonstrate we are in a recession or depression.

In fact, the so-called”debt” isn’t even debt or borrowing. It’s the total of investments in T-securities (T-bills, T-notes, T-bonds).

The government never touches the dollars invested in these securities, and the government pays them off every day, simply by returning the balances in the accounts. No tax dollars are involved. This is not a burden on the government or on taxpayers.

The sole purpose of T-securities is not to provide the federal government with its own dollars, but rather to provide a safe “parking place” for unused dollars. This stabilizes the dollar. It is not borrowing in any sense of the term.

The breach of that threshold, which was revealed in new Treasury Department figures, arrived years earlier than previously projected as a result of trillions in federal spending that the United States has deployed to combat the pandemic. That $5 trillion, which funded expanded jobless benefits, financial support for small businesses and stimulus payments, was financed with borrowed money.

No, no, no. It was NOT financed with borrowed money. Every penny the government pays for anything is created, ad hoc, with the press of a computer key. The federal government never borrows the currency it has the infinite ability to create from thin air. Here is how:

To pay a creditor, the federal government creates instructions. These instructions tell the creditor’s bank to increase the balance in the creditor’s checking account.

At the instant the instructions are obeyed, new dollars are created and added to the money supply measure called “M1.”

That is how the federal government creates money: By using its infinite ability to create instructions telling banks to increase checking account balances.

Why would the federal government borrow, when as Chairman Ben Bernanke said, it can “produce as many U.S. dollars as it wishes at essentially no cost.”

The borrowing binge, which many economists viewed as necessary to help the United States recover from the pandemic, has left the nation with a debt burden so large that the government would need to spend an amount larger than America’s entire annual economy in order to pay it off.

Utter nonsense. The so-called “debt” (that isn’t a debt) is not a debt “burden.” The government pays off all T-securities simply by returning the dollars in T-security accounts. It does this every day.

And the phrase, “entire annual economy” is a non-sequitur based on ignorance. The size of the U.S. economy (i.e. the Gross Domestic Product) does not pay for any part of the “debt.”

That comparison of the so-called “debt” vs. the US. economy — known as the “debt/GDP ratio — often is quoted as a way to shock the reader, though it is a meaningless comparison.

.

.

.

.

.

.

.

.

.

.

Do you see any relationship between the Debt/GDP ratio and the economic strength of the nation? Of course not, because there is no such relationship.

The Debt/GDP relationship is meaningless. So why does Rappeport refer to it? Either he doesn’t understand federal finance or he is trying to scare you.

(The Wall Street Journal is designed for the rich, and the rich want to convince the populace that the government cannot afford to give benefits to the not-rich.)

Some economists contend that the nation’s large debt load is not unhealthy given that the economy is growing, interest rates are low and investors are still willing to buy U.S. Treasury securities, which gives them safe assets to help manage their financial risk. Those securities allow the government to borrow money relatively cheaply and use it to invest in the economy.

More nonsense. The so-called “debt load” is not unhealthy, and low interest rates are not a factor. The federal government, having the unlimited ability to create dollars, has no difficulty paying any amount of interest.Totally painless.

And the federal government doesn’t need investors to buy Treasury securities. These are offered as a benefit to investors, not to the government. And in any event, any unsold T-securities are purchased by the Federal Reserve.

For years, presidents have promised to limit federal borrowingand bring down the nation’s budget deficit, which is the gap between what the nation spends and what it takes in. Under President Bill Clinton, the United States actually ran a budget surplus between 1998 and 2001.

Yes, Presidents have made this promise, and every time they actually kept the promise, we had depression or a recession. Mr. Rappeport fails to mention that Clinton’s surplus led to the recession of 2001.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

But taming deficitshad fallen out of fashion in recent years, including during the Trump administration, when lawmakers blew through budget caps and borrowed money to fund tax cuts and other federal spending.

Deficits don’t need to be “tamed.” Remember what Greenspan, Bernanke, and the St. Louis Fed said about the government’s infinite ability to pay its bills.

Further, the federal government does not borrow its own sovereign dollars, the dollars it has the unlimited ability to create from thin air.

And all federal spending is funded, not by taxes, but by ad hoc creation of new dollars.

Why does the federal government levy taxes? To control the economy. It taxes what it wishes to discourage, and it gives tax breaks to what it wishes to encourage.

Further, taxes give the impression that federal benefits must be limited. The rich, who control Congress and the President, want the Gap between the rich and not-rich to widen. The wider the Gap, the richer are the rich.

It’s called “Gap Psychology“, the human desire to widen the Gap below and to narrow the Gap above.

“Hitting the $30 trillion mark is clearly an important milestone in our dangerous fiscal trajectory,” said Michael A. Peterson, the chief executive officer of the Peter G. Peterson Foundation, which promotes deficit reduction. “For many years before Covid, America had an unsustainable structural fiscal path because the programs we’ve designed are not sufficiently funded by the revenue we take in.”

The Peter G. Peterson Foundation is notorious for crying “wolf” about the deficit and predicting calamity that never happens — until we actually do reduce the deficit, at which time we have the aforementioned depressions or recessions.

Until then, it’s all warnings and hand wringing about the “ticking time bomb of debt.” It’s a “time bomb” that has been ticking since 1940 and still no explosion.

The gross national debt represents debt held by the public, such as individuals, businesses and pension funds, as well as liabilities that one part of the federal government owes to another part.

Right, the so-called debt (T-bills et al) are assets of the private sector. When you own a T-bill, that is one of your assets.

Alan Rappeport doesn’t want you to have that asset. He wants the government, which has infinite assets, to take that asset from you. Smart?

While Republican lawmakers helped run up the nation’s debt load, they have since blamed Mr. Biden for putting the nation on a rocky fiscal path by funding his agenda. After a protracted standoff in which Republicans refused to raise America’s borrowing cap, threatening a first-ever federal default, Congress finally agreed in December to raise the nation’s debt limit to about $31.4 trillion.

It was all political theater — cynical politicians trying to convince the innocent public that they are fiscally prudent. But if they really were prudent, they would spend more on global warming, poverty, healthcare, education, transportation, infrastructure, science, ecology, etc. — not debating about how to spend less.

In January 2020, before the pandemic spread across the United States, the Congressional Budget Office projected that the gross national debt would reach $30 trillion by around the end of 2025. The total debt held by the public outpaced the size of the American economy last year, a decade faster than forecasters projected.

Yes, as usual, the economic forecasters were wrong about the meaningless Debt/GDP ratio. So?

The nonpartisan office warned last year that rising interest costs and growing health spending as the population aged would increase the risk of a “fiscal crisis” and higher inflation, a situation that could undermine confidence in the U.S. dollar.

By “fiscal crisis,” we assume Rappeport means the federal government would be unable to pay its debts — which as we know is impossible for our Monetarily Sovereign government. (It can happen to state/local government, which are monetarily non-sovereign.)

And inflation always is caused by shortages, never by federal deficit spending.

In fact, federal deficit spending is one of the best methods for curing inflation, if the spending is for curing the shortages.

Todays inflation is caused by shortages of oil, food, computer chips, labor, and other needs. The federal government could stop inflation by spending more to support oil drilling, efficient farming, and chip manufacture, and by eliminating FICA (FICA lowers the net income of workers and makes them less willing to accept jobs).

Trillions in federal spending has left the United States approaching levels of red ink not seen since World War II.

Actually, the so-called “debt” is much higher than it was during WWII. And when spending for WWII ended, we had recessions.

The Biden administration has said the $1.9 trillion pandemic relief package the Democrats passed last year was a necessary measure to protect the economy from further damage. Treasury Secretary Janet L. Yellen has argued that such large federal investments are affordable because interest costs as a share of gross domestic product are at historically low levels thanks to persistently low interest rates.

Yes, the $1.9 Trillion in deficit spending did protect the economy, just as cuts to federal spending will injure the economy. So why cut?

Interest costs as a share of GDP are irrelevant, as are low interest rates. In fact, higher interest rates have one advantage: They force the federal government to pump more stimulus dollars into the economy.

What is inflation? Inflation is a loss of purchasing power over time, meaning your dollar will not go as far tomorrow as it did today. It is typically expressed as the annual change in prices for everyday goods and services such as food, furniture, apparel, transportation and toys.What causes inflation? It can be the result of rising consumer demand. But inflation can also rise and fall based on developments that have little to do with economic conditions, such as limited oil production and supply chain problems.

Inflation always is caused by shortages and always is cured by curing the shortages, which the federal government can do by federal deficit spending.

Esther L. George, the president of the Federal Reserve Bank of Kansas City, suggested during a speech this week that the Fed’s big bond holdings might be lowering longer-term interest rates by as much as 1.5 percentage points — nearly cutting the interest rate on 10-year government debt in half. As rates rise, so does the amount that the United States owes to investors who buy its debt. The Congressional Budget Office estimates that if interest rates rise in line with their own forecasts, net interest costs will reach 8.6 percent of gross domestic product in 2051. That would amount to about $60 trillion in total interest payments over three decades.

That’s 60 trillion stimulus dollarspumped into the economy — dollars the federal government easily can create with the touch of a computer key, and dollars the economy uses for growth.

“A larger amount of debt makes the United States’ fiscal position more vulnerable to an increase in interest rates,” the C.B.O. said in its long-term budget outlook.

What does he mean by “vulnerable”? Is he saying that our Monetarily Sovereign government, which has the infinite ability to create dollars, will not be able to pay interest? Nonsensical.

Biden administration officials insist that they view fiscal responsibility as a priority. They have pledged that their economic agenda will be fully paid for through tax increaseson wealthy Americans and corporations and by more rigorous enforcement of the tax code.

Biden wants you to believe that federal taxes fund federal spending. It is a lie. Federal taxes are destroyed upon receipt by the Treasury.

Taxes come out of checking accounts that are part of the M1 money-supply measure. When they reach the Treasury, they cease to be part of any money-supply measure. They effectively disappear.

There is no money supply measure that includes the federal government, because the government has infinite money. No one can answer the question, “How much money does the federal government have?” The only answer is, “Infinite.”

In recent months, the budget deficit has started to shrink as a stronger economy has boosted tax receipts and as government payments of pandemic relief money have slowed.

And this means economic growth will slow. If federal deficits fall enough, we will have a recession or depression.

And some economists argue that a more recent economic phenomenon — inflation — may have a silver lining in that it could chip away at the nation’s debt burden.

The federal “debt” is not a burden on the federal government or on taxpayers or on anyone else. It’s not debt, and even if it were, the federal government has the unlimited ability to pay.

Kenneth Rogoff, a Harvard University economist, said “You would rather have no debt, of course, but compared to other issues at the moment that’s not the principal problem.”

He’s a Harvard economist and he thinks that having no debt (which would require removing $30 trillion from the economy) is something we “would rather have”?? Is this the nonsense they teach at Harvard?

In summary:

A federal deficit is necessary for economic growth. The federal Debt/GDP ratio is meaningless as a measure of economic health.

The federal government creates dollars, ad hoc, by paying creditors, which it can do endlessly.

Unlike state/local governments, the federal government is Monetarily Sovereign. It has the unlimited ability to create its sovereign currency, the U.S. dollar, and instantly can pay any obligation based on dollars.

The government never unintentionally can run short of dollars.

Federal taxes are destroyed upon receipt and do not fund federal spending.

The federal debt is nothing more than the total of deposits in T-security accounts, which are “paid off” by returning the dollars in them. This is not a burden on the federal government or taxpayers.

Federal deficit spending does not cause inflation; shortages cause inflation. A prime way to combat inflation is with federal deficit spending to cure shortages.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

Or is the need to cut the federal debt just a Common Myth?

Economics is filled with Common Myths that have no basis in data. For example:

Common Myth: The federal government should handle its finances like you and me.

Reality: In the beginning of the U.S., the federal government created laws from thin air, and some of those laws created the U.S. dollar from thin air.

There was, and remains, no limit to the number of laws the government can create, just as there was, and remains, no limit to the number of dollars the government can create.

This fact is known as “Monetary Sovereignty.“

Unlike state and local governments, unlike businesses, and unlike you, and me, the federal government cannot unintentionally run short of its own sovereign currency, the U.S. dollar. The U.S. federal government has available to it, infinite dollars.

The government creates dollars ad hoc, by paying its bills. The more bills the government pays, the more dollars it creates.

To pay a creditor, the government sends instructions, in the form of checks or wires (“Pay to the order of”), to each creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

The instant the creditor’s bank obeys those instructions, new dollars are created and added to the M1 money-supply measure.

Common Myth: The federal debt should be reduced.

Reality: The federal “debt” is not a debt of the federal government or of taxpayers. It is not even a debt. It is the total of deposits into Treasury security accounts.

These accounts resemble safe-deposit accounts, the contents of which our government, being Monetarily Sovereign and having the infinite ability to create its own sovereign currency, never needs or touches.

Just as the contents of your bank safe deposit box are not your bank’s debt, the contents of T-security accounts are not the government’s debts. They are dollars you own in your T-security account that eventually you will transfer to your checking account.

The notion of the government struggling to reduce the debt is ludicrous. Not only does the federal government have absolute control over the amount of deposits in T-security accounts, but there is no reason to reduce these deposits.

They are not a burden on the government or on future taxpayers.

Common Myth: Taxpayers or your grandchildren will be liable for paying off the debt.

Reality: When you invest in a T-bill, T-note, or T-bond, you take dollars from your checking account and deposit them into your Treasury Security account. There your dollars remain, accumulating interest until account maturity, at which time your dollars are returned to you.

The federal government does not remove those dollars for any purposes.

Returning your dollars is no burden on the government or on future taxpayers. No tax dollars are involved. Your grandchildren will not pay for the federal “debt.”

To pay off the “debt,” (which isn’t a debt) the dollars in your T-security accounts simply are returned to you. It is a simple money transfer from your T-security account to your checking account.

Common Myth: When federal taxes are not sufficient to pay for things, the federal government borrows dollars via T-bills, T-notes, and T-bonds.

Reality: The federal government never borrows. The purpose of T-securities is not to provide spending money. Rather, the sole purposes of T-security accounts are to:

1. Provide a safe, interest-paying place to store unused dollars. This helps stabilize the dollar.

2. Help the Fed control interest rates by setting the rates of interest the government pays into T-security accounts.

Common Myth: Reducing the debt would be fiscally prudent.

Reality: By law, the federal “debt” matches the net total of federal deficit spending. Because federal deficits add dollars to the economy, they are economically stimulative.

Or is the need to cut the federal debt just a Common Myth?

Economics is filled with Common Myths that have no basis in data. For example:

Common Myth: The federal government should handle its finances like you and me.

Reality: In the beginning of the U.S., the federal government created laws from thin air, and some of those laws created the U.S. dollar from thin air.

There was, and remains, no limit to the number of laws the government can create, just as there was, and remains, no limit to the number of dollars the government can create.

This fact is known as “Monetary Sovereignty.“

Unlike state and local governments, unlike businesses, and unlike you, and me, the federal government cannot unintentionally run short of its own sovereign currency, the U.S. dollar. The U.S. federal government has available to it, infinite dollars.

The government creates dollars ad hoc, by paying its bills. The more bills the government pays, the more dollars it creates.

To pay a creditor, the government sends instructions, in the form of checks or wires (“Pay to the order of”), to each creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

The instant the creditor’s bank obeys those instructions, new dollars are created and added to the M1 money-supply measure.

Common Myth: The federal debt should be reduced.

Reality: The federal “debt” is not a debt of the federal government or of taxpayers. It is not even a debt. It is the total of deposits into Treasury security accounts.

These accounts resemble safe-deposit accounts, the contents of which our government, being Monetarily Sovereign and having the infinite ability to create its own sovereign currency, never needs or touches.

Just as the contents of your bank safe deposit box are not your bank’s debt, the contents of T-security accounts are not the government’s debts. They are dollars you own in your T-security account that eventually you will transfer to your checking account.

The notion of the government struggling to reduce the debt is ludicrous. Not only does the federal government have absolute control over the amount of deposits in T-security accounts, but there is no reason to reduce these deposits.

They are not a burden on the government or on future taxpayers.

Common Myth: Taxpayers or your grandchildren will be liable for paying off the debt.

Reality: When you invest in a T-bill, T-note, or T-bond, you take dollars from your checking account and deposit them into your Treasury Security account. There your dollars remain, accumulating interest until account maturity, at which time your dollars are returned to you.

The federal government does not remove those dollars for any purposes.

Returning your dollars is no burden on the government or on future taxpayers. No tax dollars are involved. Your grandchildren will not pay for the federal “debt.”

To pay off the “debt,” (which isn’t a debt) the dollars in your T-security accounts simply are returned to you. It is a simple money transfer from your T-security account to your checking account.

Common Myth: When federal taxes are not sufficient to pay for things, the federal government borrows dollars via T-bills, T-notes, and T-bonds.

Reality: The federal government never borrows. The purpose of T-securities is not to provide spending money. Rather, the sole purposes of T-security accounts are to:

1. Provide a safe, interest-paying place to store unused dollars. This helps stabilize the dollar.

2. Help the Fed control interest rates by setting the rates of interest the government pays into T-security accounts.

Common Myth: Reducing the debt would be fiscally prudent.

Reality: By law, the federal “debt” matches the net total of federal deficit spending. Because federal deficits add dollars to the economy, they are economically stimulative.