Admirably, President Bident wishes to narrow the income/wealth/power Gap between the rich and the rest of us. I agree with this sentiment because the current Gap, very simply, is bad economics and bad for humanity.

Wide Gaps negatively affect health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, GDP, international relations, scientific advancement, the environment, human motivation and well-being, freedom, and virtually every other issue in economics and the human condition.

To narrow the Gaps, Biden proposes changes to federal law. In broad strokes, he has just three options:

Increase taxes on the rich (“rich” by any arbitrary measure).

Reduce taxes on those who are not rich.

Provide supplementary income and benefits to those who are not rich.

All three would narrow the Gap, though in different ways. From the standpoint of the U.S. economy, as measured by Gross Domestic Product, #1 would have a dramatically different effect than #2 and #3.

Increasing taxes on the rich (if the rich actually paid those increased tax levels) would take dollars out of the economy. #2 and #3 would add dollars to the economy). In short, #1 is recessive, and #s 2 and 3, would grow the economy.

This is demonstrated by the formula:

GDP = Federal Spending + Nonfederal Spending – Net Imports.

If the rich paid more taxes (#1), Nonfederal Spending would decline. The amount of the decline would be determined by various factors, most having to do with how much the rich actually pay.

History indicates that payment would be less than anticipated because of existing loopholes and/or new loopholes the rich would bribe Congress to enact.

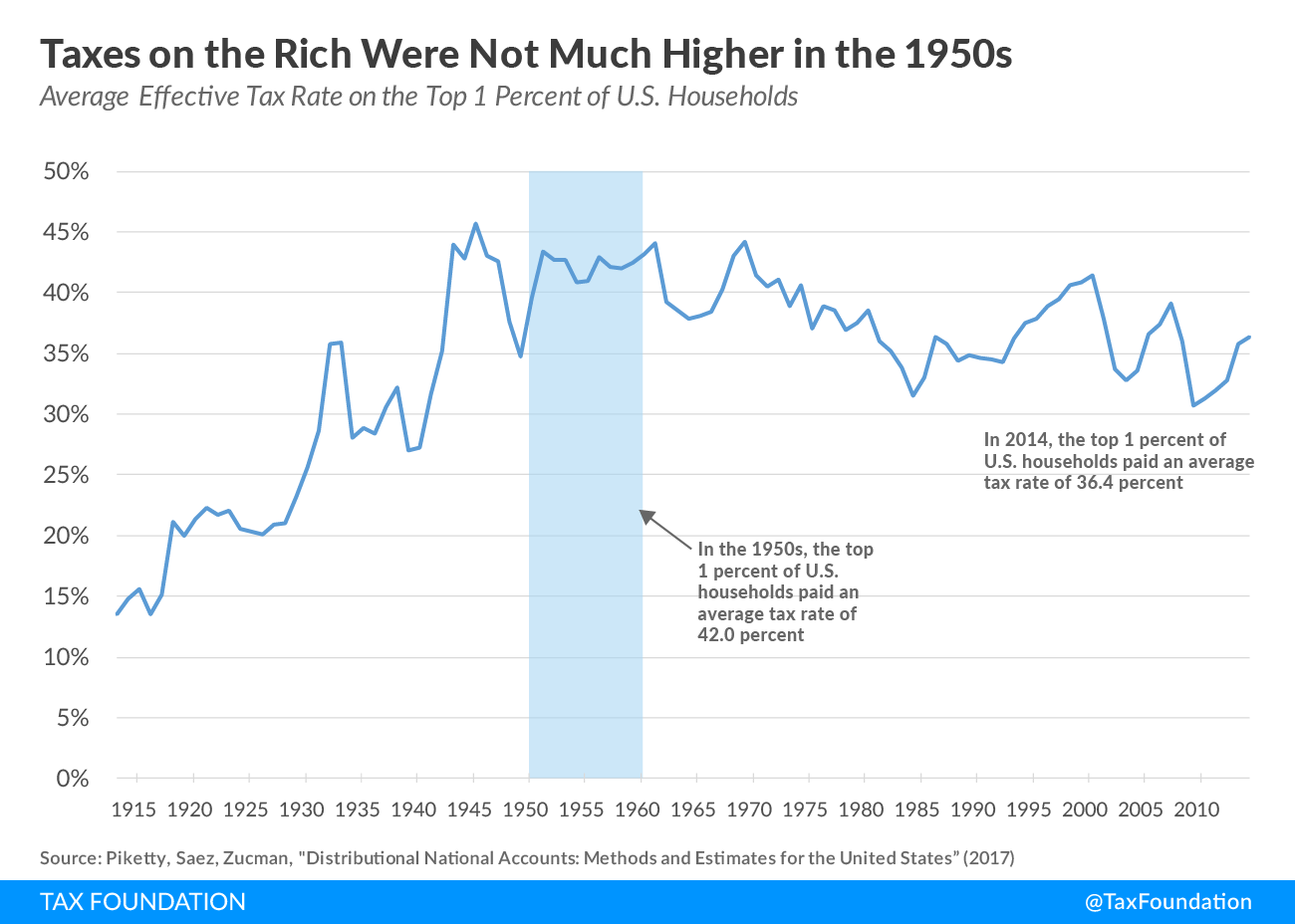

Considering that the top tax rate in the 1950s was 90%, the rich did not pay much more in that period than they do now. And some of the richest among us pay little if anything.

For example, Donald Trump paid no income taxes at all, during ten of the fifteen years, 2000-2015, despite being a billionaire. Tax laws, favorable to the rich, gave him the ability to claim losses on investments that an ordinary taxpayer may not look at as “losing” money.

In summary, using federal taxation of the rich to narrow the Gap is bad economics. History shows the rich would find ways to avoid paying higher rates.

But, even if the rich were forced to pay more, the higher rates would take dollars out of the economy and recess the economy. Option #1 is a “heads-you-lose (the rich don’t pay more), tails-you-lose” (GDP falls) plan.

Sadly, that is the plan Biden seems to have chosen, and it will cost him the November election.

The electorate may be ignorant about economics, but the rich would make sure the voters understood that raising taxes — anyone’s taxes — would hurt the economy.

It’s simple math. The more the federal government takes out of the economy, the less the economy (GDP) has.

Reducing federal taxes and/or providing supplementary benefits to those who are not rich, (#2 and #3) are the sole economically sensible ways to narrow the income/wealth/power Gap.

Sadly this sensible approach is blocked by the non-sensible belief that federal deficit spending is “unsustainable.”

That’s associated with the equally wrong belief that “excessive” federal spending or an “overheated” economy cause inflation. The fact: Inflation is not caused by “heat” (whatever that is) or by federal spending.

All inflations are caused by shortages of critical goods and services, most often oil and food. Inflation can be cured by additional federal spending to acquire and distribute the scarce goods and services.

Here is what the right-leaning Tax Foundation thinks:Details and Analysis of President Biden’s Fiscal Year 2025 Budget Proposal

March 22, 2024, By: Garrett Watson, Erica York, William McBride, Alex Muresianu, Huaquin Li, Alex Durante

11-Year Revenue (Trillions)

Long-run GDP

Long-Run Wages

Long-Run FTE Jobs

+$2.2T

-2.2%

-1.6%

-788k

In plain English, the government would remove from the economy, an additional $2,2 Trillion. This would cause GDP to fall by 2.2%, wages to fall by 1.6%, and Full-Time Equivalent Jobs to shrink by 788 thousand.

Because the Tax Foundation has a right-wing agenda, one may doubt the specifics of their calculations, but I believe they are on the right track. When the federal government collects more taxes, the economy loses money.

When the economy loses money, the GDP, wages, and jobs all shrink. It’s straightforward math.

The tax changes Biden proposes fall under three main categories: additional taxes on high earners, higher taxes on U.S. businesses—including increasing taxes that Biden enacted with the Inflation Reduction Act (IRA)—and more tax credits for a variety of taxpayers and activities.

The combination of policies would move the tax code further away from simplicity, transparency, and neutrality while making the U.S. economy less competitive.

The increase in the corporate tax rate and the additional taxes on top earners would result in U.S. top marginal tax rates on income that are among the highest in the developed world.

The federal government is running short of money while the private sector has too much money.

The middle- and lower-income taxpayers will not understand that taking dollars from the economy is recessive, and instead will happily vote for a “soak-the-rich” administration.

The ignorance and cynicism of these beliefs cannot be overstated. Biden seems to believe that taking the populist approach will gain him votes.

But, it is such government deceit that keeps you from:

The end of the FICA tax deduction from your salary

Comprehensive, no deductible Medicare for every adult and child.

Social Security benefits for everyone of all ages

Food cost aid

Free college for those who want it

Free public transportation

Housing aid

And a myriad of other benefits our Monetarily Sovereign government easily could afford, while preventing recessions and inflations.

Biden could beat Trump in a “truth vs. lies” competition, but he will not be able to out-lie Trump.

If he tries, he will lose.

Narrowing the Gap is good economics, but doing it by taxing businesses and the rich is a lie.

It may be a good time to repeat a few facts:

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money.

•The more federal budgets are cut and taxes increased, the weaker an economy becomes.

•Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

•The single most important problem in economics isthe Gap between rich and poor.

•Austerity is the government’s method for widening the Gap between rich and poor.

•Until the lower 99% understand the need for federal deficits, the upper 1% will continue to rule.

•Everything in economics devolves into motive, and the motive is the Gap between the rich and the rest.

Inflation is not an increase in one commodity’s price. It is a general increase in prices. Inflations tend to begin quickly and end slowly.

Fiscal policy is enacted by the legislative branch of government and deals with tax policy and government spending.

Monetary policy is enacted by a government’s central bank and deals with changes in the money supply by adjusting interest rates, reserve requirements, and open market operations.

Monetary policy involves changing interest rates and influencing the money supply.

Fiscal policy involves changing tax rates and levels of government spending to influence aggregate demand in the economy.

Congress and the President have given the Federal Reserve a mandate for maximum employment and price stability.

Given the Fed’s limited control over consumer and business pricing, this is akin to giving the shortstop a mandate for the team to win the World Series.

Any single business will raise its prices based on several factors, which include:

Increased costs

Reduced competition

Product improvements

New markets open up

Fed Chair Jerome Powell

The Federal Reserve, being a monetary organization, views inflation as being a monetary problem. So, it attempts to fight inflation with a monetary solution: Increased interest rates.

The Fed’s hypothesis is that increasing interest rates will discourage buyers, thus reducing demand. The demand reduction supposedly forces businesses to reduce prices to capture the remaining customers.

This, in turn, forces a reduction in business profits available to spend on employment, marketing, production, and research/development.

The formula for Gross Domestic Product (GDP), one of the most important measures of our economy is:

GDP = Federal Spending + Non-federal Spending – Net Imports

The United States is a huge consumer of goods and services so it tends to import more than it exports.

Thus, for real (inflation-adjusted) GDP to grow, either Federal Spending or Non-federal Spending must grow enough to overcome inflation and Net Imports.

However, if the Fed’s interest rate increases are successful in reducing demand, two things will happen:

Non-federal Spending will decline and

Business costs will rise

The first will cause a recession unless Federal Spending increases enough to overcome inflation and the dollar losses from Net Imports.

The second will exacerbate inflation.

However, the consensus among economic pundits — including the Fed — is that increased Federal Spending causes inflation.

No matter what the Fed’s interest rate hikes do — raise business costs or cut consumer spending — the result will be inflation and/or recession.

Only if the Fed’s rate cuts don’t work will we be spared inflation and/or recession — unless Congress and the President keep pumping growth dollars into the economy.

To cure inflation, without recession, the economy needs more growth dollars that address the true cause of inflation: Shortages of critical goods and services.The Fed’s website says, “The Federal Reserve The Federal Open Market Committee (FOMC) judges that an annual increase in inflation of 2 percent in the price index for personal consumption expenditures (PCE), produced by the Department of Commerce, is most consistent over the longer run with the Federal Reserve’s mandate.”

Two inflation measures, the Consumer Price Index (CPE-red), and Personal Consumption Expenditures (PCE-blue) track similarly. It’s not clear why the blue line is more “consistent with the Federal Reserve’s mandate.”

Another strange comment from the Fed: “Although food and energy make up an important part of the budget for most households–and policymakers ultimately seek to stabilize overall consumer prices–core inflation measures that leave out items with volatile prices can be useful in assessing inflation trends.”

Really? Look at this graph and see if you can see why so-called “core inflation” is useful.

The red line is Personal Consumption Expenditures. The blue line is “Core” Personal Consumption Expenditures.

Does anyone believe the Fed’s predictions are so precise that the blue line is more “useful in assessing inflation trends”? I mention this only to demonstrate how the Fed’s historical beliefs sometimes ignore facts.

No matter which measure the Fed leans toward, one thing is clear: To succeed, the Fed must fail.

Its interest rate increases must fail to increase business costs (or prices will increase).

Its interest rate increases must fail to reduce Non-federal Spending (or GDP will decrease).

Its cajoling of Congress to reduce Federal Spending must fail to cause a recessionary reduction in GDP

In short, the Fed must fail in everything it does, and if it fails, and the recession ends despite what the Fed does, Chairman Powell will boast that he took the economy to a “soft landing.”

Powell is the player who after he strikes out, the catcher drops the ball, and the winning run scores. So he brags about his winning the game.

The facts:

The best way to cure a problem is to cure the cause of the problem.

The cure for shortages is Federal Spending to encourage the production of, and/or access to, the scarcities that cause inflation.

Federal deficit Spending adds growth dollars to GDP, thereby curing inflation while preventing recession.

Oil shortages are the most common cause of inflation. Oil supply changes quickly. OPEC can affect supply in a day, Oil demand changes slowly. Oil prices (green) parallel inflation (purple), which generally comes on quickly, but can leave slowly if oil shortages are not cured. Oil prices affect the prices of nearly every other product.

No “soft landing” was necessary. No “landing” at all was needed. Congress and the President control the fiscal policy that controls supply.

The economy does not need or want increased interest rates. The federal government should:

Increase Federal Spending to support oil drilling and refining. and increase support for research, development, production, and distribution of such renewables as wind, solar, geothermal, tidal, and nuclear fusion (not fission).

Increase Federal support for businesses raising wages by making hiring cheaper. Federal funding of all health care insurance by instituting comprehensive, no-deductible Medicare for every adult and child in America. This would relieve businesses of the payroll cost and reduce the expense of illness-related absences.

Reduce payroll costs by eliminating FICA and funding more generous Social Security benefits for every American. This also would reduce the payroll cost of employer-funded retirement plans.

Stop fobbing off the responsibility for inflation on the Fed. Instead, take responsibility for preventing/curing the shortages that cause inflation.

Stop pretending that the federal government “can’t afford” to pay for benefits or that the federal deficits and debt are dangers to our Monetarily Sovereign economy.

Federal deficit spending is necessary to prevent/cure inflations and for economic growth. The Fed’s interest rate increases must fail to succeed.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell;MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

If you are a regular reader of this blog you may be familiar with this post: Historical claims the Federal Debt is a “ticking time bomb.” It describes the ongoing, relentless claims that the federal debt is “unsustainable and a “ticking time bomb.

The first entry was in 1940, when the so-called “federal debt” was about $40 Billion. Today, it is about $30 Trillion, a monstrous 74,900% increase.

Apparently the “time bomb” still is ticking in the minds of the debt fear mongers.

In the late 1780s, the finances of the United States were in disarray. Revolutionary War debts incurred by the Continental Congress and former colonies were defaulting, and the democratic experiment in the New World was on the brink of failure.

But the nation caught a break when President George Washington appointed Alexander Hamilton as the first secretary of the Treasury.

In 1790 and 1791, Hamilton persuaded a reluctant Congress to establish the nation’s first central bank and consolidate all outstanding state and federal debt.

The federal debt burden after this action was just 30% of gross domestic product. A few years later, President Washington reinforced in his farewell address the need to avoid excessive debt.

We repeatedly have shown that the Debt/GDP ratio signifies nothing. It predicts nothing. It says nothing about a nation’s ability to pay its financial debts. It has no meaning whatsoever.

Yet it is quoted, again and again, by pundits who use it as evidence of . . . whatever they are trying to prove.

What next, Annual Rainfall/Number of Children named “Tom”? Here is the nonsense being peddled by Investopedia:

By comparing what a country owes with what it produces, the debt-to-GDP ratio reliably indicates that particular country’s ability to pay back its debts.

Often expressed as a percentage, this ratio can also be interpreted as the number of years needed to pay back debt if GDP is dedicated entirely to debt repayment.

Oh, really? The ratio “reliably indicates”?

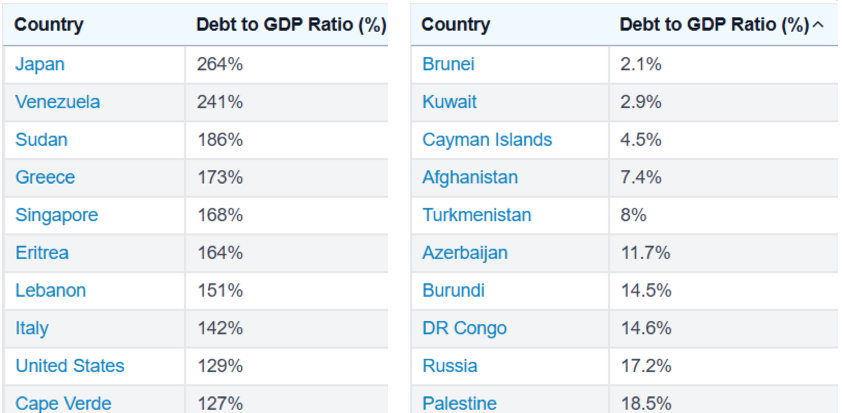

Here are some sample ratios. The nations with the ten highest ratios are shown to the left. The nations with the ten lowest ratios are shown to the right. According to the debt fear-mongers, the most financially secure nations are listed in the right-hand column:

According to the infamous Debt/GDP formula, the U.S. government has less ability to pay its debts than Cape Verde, and every one of the nations in the right-hand column.

And Japan supposedly has less ability to pay its debts than any other nation in the world. Does anyone really believe this nonsense?

But wait. Buried deep in the Investopedia article is this little paragraph:

Economists who adhere to modern monetary theory (MMT) argue that sovereign nations capable of printing their own money cannot ever go bankrupt, because they can simply produce more fiat currency to service debts; however, this rule does not apply to countries that do not control their monetary policies, such as European Union (EU) nations, who must rely on the European Central Bank (ECB) to issue euros.

Thus, the Debt/GDP “rule” does not apply to the United States, Canada, Mexico, China, Australia, the UK, Switzerland, Sweden, Norway, India, South Africa and others. The “rule” doesn’t apply to most of the world’s largest, most significant economies.

Yet, pundits in America insist on using the useless — no harmful — Debt/GDP ratio as a cudgel to ram debt reduction into financial planning.

Never mind that debt reduction causes depressions and recessions:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Why does that happen? Simple algebra. The formula for Gross Domestic Product is:

GDP = Federal Spending + Nonfederal Spending + Net Exports.

To reduce the so-called federal debt, one must decrease Federal Spending and/or increase federal taxes, which decreases Nonfederal Spending.

To increase real (inflation-adjusted) economic growth, a nation must do the opposite: Increase Federal Spending and/or decrease federal taxes, both of which add to the so-called “federal debt.”

Mathematically, there is no way to grow real GDP without growing “federal debt” enough to overcome inflation. So, if inflation is say, 2% (the Fed’s goal), the debt increase must overcome an annual 2% inflation handicap for GDP just to stay even.

Add to that, the need to overcome a net export figure (which America almost always has) and largeannual deficits become vital.

When we have deficits that are too small, we have recessions, which the following graph demonstrates:

When federal debt declines, we experience recessions (vertical gray bars), which are cured by federal debt increases.

Strangely, the “science” of economics, which seems to love mathematical formulas and graphs, ignores the obvious. Growing an economy requires a growing supply of money.

Federal deficits add money to the economy. Federal taxes take money from the economy.

Continuing with the ticking time bomb article:

Over the next 175 years, politicians across the political spectrum largely adhered to Hamiltonian principles to preserve the integrity of the public credit.

The most important principle was that debt should be issued primarily to address emergencies – especially those involving foreign wars – and that debt burdens should be reduced during times of peace.

This changed completely in the 1970’s when President Nixon mandated the end of the dollar “backing” (actually the convertibility) to gold, and made the federal government Monetarily Sovereign in full.

Until then, the federal government’s ability to create dollars was limited by its inventory of gold. When the inventory did not keep up with GDP growth needs, recessions resulted.

Now, with gold no longer a factor, the government’s ability to grow the nation’s money supply also gave the government the ability to grow GDP.

This discipline enabled America to establish and maintain its excellent credit record, which provided ample lending capacity during periodic crises.

As Hamilton predicted, the ability of the nation to borrow proved critical during the War of 1812, the Civil War, World War I and World War II.

The nation now has no need to borrow, a far superior situation. It can create, at will, the growth dollars it needs.

After World War II, fiscal discipline was temporarily restored, and debt/GDP was reduced by growing the economy much faster than the debt even though the federal government continued to run budget deficits during most years.

Again, there is no magic. GDP still = Federal Spending + Nonfederal Spending + Net Exports.

If the Federal debt is reduced, the growth dollars must come from somewhere. In this case, growth came from Net Exports.

Subsequently, our wealthy economy began buying, buying, buying, which is a good thing. We were exchanging dollars that cost us nothing (We created them by pressing computer keys) for valuable goods and services.

Because the American government has access to infinite dollars, importing goods and services makes economic sense.

The U.S. is the world’s most massive consumer economy. Our Net Exports fell while GDP grew only because of massive federal deficit spending.

The one exception was in 1998-2001, when the federal government ran budget surpluses and even paid down debt in two of these years.

That exception proves the debt reduction is an economic disaster. Here is what happened when we paid down debt: 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Reduced deficit spending morphed into a surplus in 1998. The result: A recession in 2001, which was cured by increased federal deficit spending.

Since then, the Hamiltonian principle has been decisively abandoned, and the federal government now routinely runs large deficits, resulting in ever-increasing debt burdens. This behavior is projected to worsen in the future.

Translation: The federal government now routinely runs large deficits, which pump growth dollars into the economy, thus growing GDP.

Mounting federal debt burdens now represent the greatest threat to the U.S. economy, national security and social stability.

The federal debt/GDP ratio is 123%. The nonpartisan Congressional Budget Office projects that, under current law, it will increase to 192% by 2053.

The federal government has the infinite ability to create dollars. The major threat to the U.S. economy (i.e. to GDP) is a reduction in federal money creation.

Clearly this is irresponsible, unsustainable and in sharp contrast to Hamilton’s founding principle.

There it is, the word “unsustainable,” to describe what we have been sustaining since 1940. Hamilton did not anticipate the post-1973, Monetarily Sovereign America.

National debt has topped $34 trillion.Does anyone actually have the guts to fix it?

The fastest way to “fix” the national debt would be to stop accepting deposits into T-security accounts (T-bills, T-notes, and T-bonds).

The government doesn’t use those dollars. They remain the property of the depositors. The problem is that those deposits do have two functions (neither of which is to supply the government with dollars):

To provide a safer place to store dollars than bank savings accounts

To help the Fed control interest rates by providing a floor for rates.

Why does the United States continue to behave so irresponsibly? One reason is that U.S. politicians routinely avoid spending cuts and tax increases because they may threaten their reelection prospects.

Voters rightfully don’t want tax increases and they don’t want federal benefit reductions, both of which take money out of voters’ pockets and lead to recessions.

Another is that, as the issuer of the world’s dominant reserve currency, the United States can run fiscal deficits so long as surplus countries, such as China and Saudi Arabia, continue to purchase U.S. Treasuries.

The U.S. does not need anyone to purchase U.S. Treasuries. The federal government creates all the dollars it needs simply by pressing computer keys. The government does not use the dollars in T-security accounts. They are the property of the depositors.

In fact, proponents of the flawed and failed Modern Monetary Theory implicitly argue that the dollar’s reserve currency status is permanent, which allows deficit spending to continue indefinitely.

The dollar is the world’s leading reserve currency, which is a currency banks keep on reserve to facilitate international commerce. But, other currencies — the British pound, the euro, the Chinese renminbi — also are reserve currencies.

Being a reserve currency has nothing to do with the federal government’s ability to spend indefinitely.

Yikes, there it is again, the silly “time bomb” analogy. It’s the time bomb that never explodes.

A debt crisis is not imminent in 2024, but one will occur in the future if the nation’s addiction to deficits and debt persists.

Translation: A debt crisis is not imminent in 2024. We have no idea when if ever it will occur, but it makes us sound smart to threaten it.

The greatest risk is the one that Alexander Hamilton feared most: One day, the United States could face a threat to its very existence – perhaps in the form of a foreign war – and Americans will lack the debt capacity to fund an adequate response.

Obviously, the government never can run short of dollars. I wonder why they don’t understand that.

Lack the capacity to fund? Utter nonsense. Here are the facts:

Former Fed Chairman, Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debtit has because we can always print the money to do that.”

Former Fed Chairman, Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

That’s the real capacity.

Fortunately, the future is far from hopeless. America sits on a huge reservoir of natural resources and remains the world’s technological innovation engine.

It also possesses sufficient time to enact fiscal reforms and reestablish fiscal discipline.

Because the authors, David M. Walker and Mark J. Higgins, don’t understand Monetary Sovereignty, they think federal government fiscal discipline is the same a personal fiscal discipline.

Federal finance is so unlike personal finance that not understanding the difference is like not understanding the difference between butter and a butterfly.

The challenge for Americans today is that the longer we wait to reinstate this principle, the more pain that will be incurred. It is our belief that the solution is in the hands of “We the People.”

The math doesn’t lie.Republicans and Democrats own every missing dollar of our growing national debt crisis.

Politicians have powerful incentives to respond to short-term demands, and if Americans collectively demand that short-term desires must be satisfied at the expense of the nation’s long-term prosperity and solvency, that is what politicians will deliver.

Heaven forbid that Americans demand increases in taxes and cuts to federal spending. The result would be a depression.

On the other hand, if Americans place equal value on the longevity of their country and the prosperity of their children and grandchildren, they will demand that politicians take steps to defuse America’s fiscal “time bomb.”

Oops, more time bomb that never explodes.

Ever notice that the debt worriers never come up with evidence? They say “debt is bad,” but they don’t say,”Here is a graph of what has happened to the economy when federal debt increased and decreased.

Here is one such graph:

As federal debt (red) has grown, the economy (GDP, blue) has grown.

As you can see, there is no sign of a “debt crisis.”

History suggests that Americans will eventually pursue the correct course of action. Our hope is that they embrace it quickly to ensure that America’s future is brighter than its past.

David M. Walker, a former U.S. comptroller general, is also a recipient of the Alexander Hamilton Award for economic and fiscal policy leadership from the Center for the Study of the Presidency and the Congress.

Mark J. Higgins is author of “Investing in U.S. Financial History: Understanding the Past to Forecast the Future,” coming Feb. 27. Connect with Mark on LinkedIn.

It is frightening that a former U.S. comptroller general and recipient of an award for policy leadership, and the author of a book about U.S. finances can be so clueless about U.S. federal finances. No wonder the public is so ill-informed.

If you owned a legal, money-printing press, would you borrow money? Think about it.

The U.S. government has the infinite ability to create (aka “print”) U.S. dollars. So why would it ever borrowdollars?

It doesn’t.

The same “bark”?

Despite what “learned” pundits tell you, the U.S. government never, never, ever borrows U.S. dollars.

The government issues U.S. Treasury bonds, which are totally unlike the private sector bonds that corporations issue.

The fact that the same words — “bills,” “notes,” and “bonds” — are used to describe completely different things, has confused people who should know better — politicians, economists, and the media — for decades.

It’s as though a professional botanist told you dogs are like trees because they both have “bark.”

In the same vein, the so-called federal “debt” is not debt. It’s not even federal.

Here are Warren Buffett’s comments. He gets it about 95% right.

The U.S. Treasury is borrowing $3 trillion in three months to pay for the pandemic response, a record sum that dwarfs the $1.8 trillion borrowed in 2009 during the financial crisis.

The debt will be sold in bonds to a variety of foreign and domestic investors.

Sorry, Mr. Wolff-Mann, but because the federal government is Monetarily Sovereign, the U.S. Treasury has the infinite ability to create dollars (at the behest of Congress).

If Congress voted for the Treasury to create $3 trillion, or $300 trillion, or $3,000 trillion, the Treasury could do it at the touch of a computer key.

Clearly, it has no reason to borrow dollars.

So it doesn’t.

The so-called, misnamed “debt” is two separate things that have been merged for obsolete reasons:

1. The “debt” is the net total of all deficitsthrough history. Deficits are the difference between taxes received and financial obligations (aka “bills”) paid.

The government doesn’t owe deficits. They already have been paid for. That is what makes them “deficits.”

2. The “debt” also is the total of deposits into Treasury Security accounts, those T-bills, T-notes, and T-bonds that are nothing whatsoever like private sector bills, notes, and bonds.

The government accepts deposits into Treasury Security accounts to provide a safe storage place for unused dollars. This stabilizes the dollar and is partly responsible for the U.S. dollar being the most popular currency in the world.

Rather than putting unused dollars into risky private bank accounts, foreign governments and private investors prefer the safety of U.S. Treasury accounts.

The accounts resemble safe deposit boxesin that the money in these accounts is wholly owned by the depositors, not by the U.S. government, which never touches those dollars.

To pay off these accounts, the government simply returns the contents of the accounts to the owners, i.e. the depositors.

At the 2020 Berkshire Hathaway Annual Shareholders Meeting on Saturday, billionaire investor Warren Buffett carefully explained in simple terms why the U.S. will never default on its debt.

When a concerned shareholder asked him whether there was a risk, he didn’t prevaricate, but started with a “no.”

“If you print bonds in your own currency, what happens to the currency will be the question,” said Buffett. “But you don’t default. The U.S. has been smart to issue its debt in its own currency.”

A U.S. dollar bill actually is a zero-interest, Treasury bond. It is evidence that the bearer owns a U.S. dollar.

Other countries don’t do this, Buffett pointed out.

“Argentina is now having a problem because the debt isn’t in their own currency, and lots of countries have had that problem,” he said.

“And lots of competent countries will have that problem in the future.”

Similarly, U.S. state and local government and euro nation debt isn’t in their own currency. State and local governments use the dollar. Euro nations use the euro, which is the currency of the European Union (EU).

France, Germany, Italy et al have problems with their debt (which is real debt) because they do not issue the euro. The EU does.

Over the years, many have worried about the growing national debt as tax cuts and spending have created an ever-widening gap between revenue and outflows.

But in his explanation, Buffett highlighted the distinctions that make the U.S. Treasury much different than your personal checkbook.

Mainly, the government owns the printing press to pay the money to the holders of its debt.

Close, but that’s not precisely what happens. The money already exists in the accounts. The depositors put it there.

Paying off the “debt” merely involves returning the depositors’ dollars. The only function of the metaphorical “printing press” is to add interest dollars to the accounts.

“It is very painful to owe money in somebody else’s currency,” said Buffett. “If I could issue a currency Buffett bucks, and I had a printing press and I could borrow money, I would never default.”

If he could print Buffet bucks, that would be widely accepted, he never would borrow money, just as the U.S. federal government never borrows dollars.

This is a common refrain of Modern Monetary Theory as well as longtime Fed Chair Alan Greenspan, who once said something similar: “The United States can pay any debt it has because we can always print money to do that. So there is zero probability of default.”

The chief worry about just printing money to pay obligations is inflation.

That is another widespread, false belief. Creating (aka “printing”) dollars doesn’t cause inflation. Shortages of critical goods and services — mostly oil and food — cause inflation. (See: Inflation: Why the Fed is confused)

“What you end up getting in terms of purchasing power can be in doubt,” Buffett said.

But whether the U.S. can pay the dollars that it owes is not in doubt. The Oracle of Omaha noted back to when Standard & Poor’s downgraded the U.S.’s credit rating in 2011.

The U.S. government does not “owe” any dollars. It already has paid for what it has purchased. That is the “deficit.”

And the dollars in Treasury Security accounts — the T-bills, notes, and bonds — are owned by the depositors. The government doesn’t owe them just as your bank doesn’t owe you the contents of your safe deposit box.

“To me that did not make sense,” he said. “How you can regard any corporation as stronger than a person who can print the money to pay you, I just don’t understand. So don’t worry about the government defaulting.”

Buffett then addressed the frequent government shut-downs that happen over partisan arguments about raising the debt ceiling.

“I think it’s kind of crazy incidentally…to have these limits on the debt,” he said. “And then [the] stopped government, arguing about whether it’s going to increase the limits. We’re going to increase the limits on the debt.”

Buffett pointed out that the debt “isn’t going to be paid, it’s going to be refunded,” and referenced the period in the 1990s when the debt came down and the country simply created more.

“When the debts come down a little bit, the country’s going to print more debt. The country is going to grow in terms of its debt-paying capacity,” he said. “But the trick is to keep borrowing in your own currency.”

Ethan Wolff-Mann is a writer at Yahoo Finance focusing on consumer issues, personal finance, retail, airlines, and more. Follow him on Twitter @ewolffmann.

Paul Krugman

That was Warren Buffett. Now, here is Paul Krugman, winner of the economics version of the Nobel Prize. He too gets it about 95% right.

The US doesn’t actually have to pay off its $31 trillion mountain of debt, according to top economist Paul Krugman, hitting back at the idea that government finances can be compared to household balance sheets.

Though individual borrowers are expected to pay off debts, the same isn’t true for governments, Krugman argued in a column for the New York Times on Friday.

That’s because unlike people, governments don’t die, and they gain more revenue with each passing generation.

Not quite right. State and local governments are expected to pay off debts. Euro governments are expected to pay off debts.

But the Monetarily Sovereign U.S. federal government always pays what it owes to vendors, on time. It does not accumulate debt.

The reason is notthat “governments don’t die and gain more revenue.” Monetarily nonsovereign governments do borrow and must pay off loans, and may not gain enough revenue to pay off those loans.

Our Monetarily Sovereign government is a different animal, altogether. It does not borrow, it does not have loans to pay off, and its tax revenue does not pay for anything.

Its tax revenue is destroyed upon receipt. (See: “Does the U.S. Treasury Really Destroy Your Tax Dollars?”)

“Governments, then, must service their debts – pay interest and repay principal when bonds come due – but they don’t necessarily have to pay them off; they can issue new bonds to pay principal on old bonds and even borrow to pay interest as long as overall debt doesn’t rise too much faster than revenue,” he added.

Treasury bonds don’t supply the federal government with spending money. The government never touches those dollars. The government doesn’t use bond deposits to pay anything.

Treasury securities provide two main functions:

They help the Federal Reserve control interest rates by providing a “base” rate.

They help stabilize the dollar by providing a safe haven for unused dollars.

They do not help the federal government fund any thing.

The debt-to-GDP ratio is oft-quoted, but completely meaningless. The federal government can pay all its financial obligations whether the ratio was 10%, 100%, or 1,000%. (See: Enough Already, With The Debt/GDP ratio)

Federal purchases are part of GDP, but are not paid for with GDP. All federal financial obligations are funded by newly created ad hoc dollars.

Historically, it’s also unusual for governments to pay off large debts, Krugman said. Such was the case for Great Britain, which has largely held onto the debt it incurred as far back as the Napoleonic wars.

It’s more irrelevance from the Nobel winner. Deadbeat governments may not pay creditors, but the Great Britain “debt” is not owed to creditors. It’s an accounting myth for describing the total of deficit spending, which is funded by money creation.

Krugman’s argument comes amid growing contention over the US debt level, with policymakers still sparring over the conditions they want to raise the country’s borrowing limit.

House Speaker Kevin McCarthy has said he would reject a short-term debt ceiling increase unless spending cuts are negotiated, having proposed a bill that would slash around $4.5 trillion on spending.

This is purely a political ploy, having absolutely nothing to do with the realities of federal funding. The formula for GDP is:

GDP = Federal Spending + Nonfederal Spending + Net Exports

Slashing $4.5 trillion for federal spending would, by formula, slash at least $4.5 trillion from GDP (Probably more, because federal spending begets private sector, nonfederal spending.)

In short, Republican McCarthy wanted to trash the economy, because a Democrat was President.

Congress now has less than two weeks to raise the borrowing limit before the government could potentially run out of cash, US Treasury Secretary Janet Yellen warned.

Sadly, Yellen is too cowardly (or ignorant?) to tell the truth. The so-called “borrowing limit” is the ultimate fraud. It’s not a borrowing limit, because the U.S. doesn’t borrow.

It’s a limit on deposits into T-security accounts, which do nothing to change the federal government’s ability to fund its spending.

A default on the country’s obligations could result in catastrophe for financial markets, experts have warned.

Krugman is correct. The debt ceiling is a fraud being committed on naive American voters. It’s a bit of meaningless, though harmful, political chicanery, designed to pretend financial frugality.

All those who think the debt ceiling is a good idea either are liars or ignorant.There is no alternative.

Period.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Considering that the top tax rate in the 1950s was 90%, the rich did not pay much more in that period than they do now. And some of the richest among us pay little if anything.

For example, Donald Trump paid no income taxes at all, during ten of the fifteen years, 2000-2015, despite being a billionaire. Tax laws, favorable to the rich, gave him the ability to claim losses on investments that an ordinary taxpayer may not look at as “losing” money.

In summary, using federal taxation of the rich to narrow the Gap is bad economics. History shows the rich would find ways to avoid paying higher rates.

But, even if the rich were forced to pay more, the higher rates would take dollars out of the economy and recess the economy. Option #1 is a “heads-you-lose (the rich don’t pay more), tails-you-lose” (GDP falls) plan.

Sadly, that is the plan Biden seems to have chosen, and it will cost him the November election.

The electorate may be ignorant about economics, but the rich would make sure the voters understood that raising taxes — anyone’s taxes — would hurt the economy.

It’s simple math. The more the federal government takes out of the economy, the less the economy (GDP) has.

Reducing federal taxes and/or providing supplementary benefits to those who are not rich, (#2 and #3) are the sole economically sensible ways to narrow the income/wealth/power Gap.

Sadly this sensible approach is blocked by the non-sensible belief that federal deficit spending is “unsustainable.”

That’s associated with the equally wrong belief that “excessive” federal spending or an “overheated” economy cause inflation. The fact: Inflation is not caused by “heat” (whatever that is) or by federal spending.

All inflations are caused by shortages of critical goods and services, most often oil and food. Inflation can be cured by additional federal spending to acquire and distribute the scarce goods and services.

Here is what the right-leaning Tax Foundation thinks:Details and Analysis of President Biden’s Fiscal Year 2025 Budget Proposal

Considering that the top tax rate in the 1950s was 90%, the rich did not pay much more in that period than they do now. And some of the richest among us pay little if anything.

For example, Donald Trump paid no income taxes at all, during ten of the fifteen years, 2000-2015, despite being a billionaire. Tax laws, favorable to the rich, gave him the ability to claim losses on investments that an ordinary taxpayer may not look at as “losing” money.

In summary, using federal taxation of the rich to narrow the Gap is bad economics. History shows the rich would find ways to avoid paying higher rates.

But, even if the rich were forced to pay more, the higher rates would take dollars out of the economy and recess the economy. Option #1 is a “heads-you-lose (the rich don’t pay more), tails-you-lose” (GDP falls) plan.

Sadly, that is the plan Biden seems to have chosen, and it will cost him the November election.

The electorate may be ignorant about economics, but the rich would make sure the voters understood that raising taxes — anyone’s taxes — would hurt the economy.

It’s simple math. The more the federal government takes out of the economy, the less the economy (GDP) has.

Reducing federal taxes and/or providing supplementary benefits to those who are not rich, (#2 and #3) are the sole economically sensible ways to narrow the income/wealth/power Gap.

Sadly this sensible approach is blocked by the non-sensible belief that federal deficit spending is “unsustainable.”

That’s associated with the equally wrong belief that “excessive” federal spending or an “overheated” economy cause inflation. The fact: Inflation is not caused by “heat” (whatever that is) or by federal spending.

All inflations are caused by shortages of critical goods and services, most often oil and food. Inflation can be cured by additional federal spending to acquire and distribute the scarce goods and services.

Here is what the right-leaning Tax Foundation thinks:Details and Analysis of President Biden’s Fiscal Year 2025 Budget Proposal

Another strange comment from the Fed: “Although food and energy make up an important part of the budget for most households–and policymakers ultimately seek to stabilize overall consumer prices–core inflation measures that leave out items with volatile prices can be useful in assessing inflation trends.”

Really? Look at this graph and see if you can see why so-called “core inflation” is useful.

Another strange comment from the Fed: “Although food and energy make up an important part of the budget for most households–and policymakers ultimately seek to stabilize overall consumer prices–core inflation measures that leave out items with volatile prices can be useful in assessing inflation trends.”

Really? Look at this graph and see if you can see why so-called “core inflation” is useful.