If you ever have flown a foreign airline and compared it to an American airline, you noticed a marked difference.

Foreign air carriers like ANA, Japan Airlines, Singapore Airlines, Emirates, and Qatar Airways offer better food options, and more comfortable seating, better in-flight entertainment, and superior amenities.

Many foreign airlines operate newer and more modern aircraft with lie-flat seats in business class, advanced in-flight entertainment systems, and luxurious first-class suites.

Why the difference?

I ask because of a recent experience my daughter had flying United Airlines, first class, from Chicago to Denver.

It was a two-hour and 43-minute flight that took off at 11:02AM Central time and landed at 12:45PM Mountain time.

Here is a photo of the “meal” she was served in First Class during that 2 hours and 45 minutes (Coach got nothing):

This is United Airlines’s lunch in first class.

Yes, that’s right. In “First Class,” i.e. United Airlines version of “First Class,” this nearly three-hour flight warranted a 1 oz. bag of gummies for lunch.

The “explanation,” if you can call it that, was “We don’t offer meals on all our flights.”

I guess that sitting in a plane for nearly three hours during lunchtime doesn’t qualify for a meal on United Airlines, not even when you pay sky-high First Class rates.

And if that isn’t a disgusting enough example of United Airlines service, my daughter, who had a round-trip First Class ticket, was bumped from the return flight and had to take a later coach flight.

(Did I mention that my daughter is a transplant recipient who flies first class because her immune system is compromised, so she tries to keep whatever seating distance she can from other travelers?)

So, aside from the inconvenience of being bumped and the tighter seating,

Eventually she will get her $500+ refund for the difference between coach and First Class if she files paperwork, argues on the phone, and jumps through whatever other hoops United demands.

How does United Airlines get away with this awful service? Government restrictions on competition:

Once other air travelers have experienced the impressive service some foreign airlines offer, they often wonder: Why can’t they do business in the USA?

Of course, international airlines do operate in this country, but the government forbids them from flying point-to-point destinations domestically.

These laws, meant to protect American consumers and jobs, are having the exact opposite effect. Eliminating — or at least partially lifting — outdated restrictions could significantly increase competition and improve customer service.

Industry watchers say that banning foreign carriers from offering domestic flights might have made sense a generation ago when the American airline industry was tightly regulated by the federal government. But today, with only a few megacarriers remaining and the security concerns of the Cold War a distant memory, it’s harder to justify the laws.

“Foreign airline competition and capital investment in U.S. airlines could quickly improve passenger service, lower fares, result in new start-up airlines, and relieve overcrowding,” says Paul Hudson, president of FlyersRights.org.

When trying to protect U.S. businesses, the federal government has two alternatives: Supportthe domestic industry to provide better quality and service or punish and restrict the foreign business so it can’t provide better quality and service.

Emirates, Qatar Airways, and Singapore Airlines are examples of the former approach. These airlines benefit from significant state backing, enabling them to offer high-end services.

The result is a better overall flying experience for those who can access these airlines.

Our Monetarily Sovereign government could do the same.

Levying import duties and restricting foreign businesses are examples of the “punish-and-restrict” approach.

This results in higher prices and poorer quality of service for Americans.

Expressing fear of federal deficits and so-called “socialism.” the U.S. government invariably uses the “punish and restrict” foreigners, so Americans are the ones punished and restricted.

The U.S. federal government is not like state/local governments, not like euro governments, not like businesses, and not like you and me.

It is uniquely Monetarily Sovereign. It cannot, unwillingly, run short of its own sovereign currency, the U.S. dollar. As real experts have said:

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Press Conference: Mario Draghi, President of the Monetarily Sovereign ECB, 9 January 2014 Question: can the ECB ever run out of money? Mario Draghi: Technically, no. We cannot run out of money.

Because the U.S. federal government has the infinite ability to create its sovereign currency, the U.S. dollar, it never borrows dollars.

Contrary to popular wisdom, T-bills, T-notes, and T-bonds do not represent borrowing. They simply are deposits, the purpose of which is to provide a safe place to store unused dollars and to help the Fed control interest rates.

The government never touches those dollars, which remain the property of the depositors. Not only can our Monetarily Sovereign government not run short of dollars, but federal deficits are necessary to grow the economy, as evidenced by the formula: GDP = Federal Spending + Nonfederal Spending + Net Exports.

When we don’t have sufficient federal deficits, we have depressions and recessions:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Periodically, we publish yet another shrieking claim that the U.S. federal debt is “unsustainable”and a “ticking time bomb.”

This lie has been told to you every year (really, almost every day) since 1940, and that bomb has never exploded, nor will it.

Rather than repeat the entire list of the thousands of lies to which you have been subject, I will list samples here as a reference and add periodically, at the end, new “federal debt is a ticking time bomb“ lies as I encounter them.

Read these and see that even respected economists replace facts with intuition:

September 26, 1940, New York Times: The federal budget was a “ticking time-bomb which can eventually destroy the American system,” said Robert M. Hanes, president of the American Bankers Association.

By 1960, the debt was “threatening the country’s fiscal future,” said Secretary of Commerce Frederick H. Mueller. (“The enormous cost of various Federal programs is a time-bomb threatening the country’s fiscal future, Secretary of Commerce Frederick H. Mueller warned here yesterday.”)

In 1984: AFL-CIO President Lane Kirkland said. “It’s a time bomb ticking away.”

In 1985: “The federal deficit is a ticking time bomb, and it’s about to blow up,” U.S. Sen. Mitch McConnell. (Remember him?)

Later in 1985: Los Angeles Times: “We labeled the deficit a ‘ticking time bomb‘ that threatens to permanently undermine the strength and vitality of the American economy.”

In 1987: Richmond Times-Dispatch – Richmond, VA: “100TH CONGRESS FACING U.S. DEFICIT’ TIME BOMB‘”

Later in 1987: The Dallas Morning News: “A fiscal time bombis slowly ticking that, if not defused, could explode into a financial crisis within the next few years for the federal government.”

In 1989: FORTUNE Magazine: “A TIME BOMB FOR U.S. TAXPAYERS“

In 1992: The Pantagraph – Bloomington, Illinois: “I have seen where politicians in Washington have expressed little or no concern about this ticking time bomb they have helped to create, that being the enormous federal budget deficit, approaching $4 trillion.“

Later in 1992, Ross Perot said, “Our great nation is sitting right on top of a ticking time bomb. We have a national debt of $4 trillion.”

In 1995: Kansas City Star: “Concerned citizens. . . regard the national debt as a ticking time bombpoised to explode with devastating consequences at some future date.”

In 2004: Bradenton Herald: “A NATION AT RISK: TWIN DEFICIT A TICKING TIME BOMB“

In 2005: Providence Journal: “Some lawmakers see the Medicare drug benefit for what it is: a ticking time bomb.”

In 2006: NewsMax.com, “We have to worry about the deficit . . . when we combine it with the trade deficit, we have a real ticking time bomb in our economy,” said Mrs. Clinton.

In 2007: USA Today: “Like a ticking time bomb, the national debt is an explosion waiting to happen.“

In 2010: Heritage Foundation: “Why the National Debt is a Ticking Time Bomb. Interest rates on government bonds are virtually guaranteed to jump over the next few years.

In 2010: Reason Alert: “. . . the time bomb that’s ticking under the federal budget like a Guy Fawkes’ powder keg.”

In 2011: Washington Post, Lori Montgomery:”. . . defuse the biggest budgetary time bombs that are set to explode.”

June 19, 2013: Chamber of Commerce: Safety net spending is a ‘time bomb’, By Jim Tankersley: The U.S. Chamber of Commerce is worried that not enough Americans are worried about social safety net spending. The nation’s largest business lobbying group launched a renewed effort Wednesday to reduce projected federal spending on safety-net programs, labeling them a “ticking time bomb” that, left unchanged, “will bankrupt this nation.”

On June 15, 2014: CBN News: “The United States of Debt: A Ticking Time Bomb“

On January 27, 2017: America’s “debt bomb is going to explode.” That’s according to financial strategist Peter Schiff. Schiff said that while low interest rates had helped keep a lid on U.S. debt, it couldn’t be contained for much longer. Interest rates and inflation are rising, creditors will demand higher premiums, and the country is headed “off the edge of a cliff.”

February 16, 2018 America’s Debt Bomb By Andrew Soergel, Senior Reporter: Conservatives and deficit hawks are hurling criticism at Washington for deepening America’s debt hole.

April 10, 2019,The National Debt: America’s Ticking Time Bomb. TIL Journal. Entire nations can go bankrupt. One prominent example was the *nation of Greece which was threatened with insolvency a decade ago. Greece survived the economic crisis because the European Union and the IMF bailed the nation out.

SEP 12, 2019, Our national ticking time bomb, By BILL YEARGIN SPECIAL TO THE SUN SENTINEL | At some point, investors will become concerned about lending to a debt-riddled U.S., which will result in having to offer higher interest rates to attract the money. Even with rates low today, interest expense is the federal government’s third-highest expenditure following the elderly and military. The U.S. already borrows all the money it uses to pay its interest expense, sort of like a Ponzi scheme. Lack of investor confidence will only make this problem worse.

JANUARY 06, 2020, National debt is a time bomb, BY MARK MANSPERGER, Tri City Herald | The increase in the U.S. deficit last year was about $1.1 trillion, bringing our total national debt to more than $23 trillion! This fiscal year, the deficit is forecasted to be even higher, and when the economy eventually slows down, our annual deficits could be pushing $2 trillion a year! This is financial madness. there’s not going to be a drastic cut in federal expenditures — that is, until we go broke — nor are we going to “grow our way” out of this predicament. Therefore, to gain control of this looming debt, we’re going to have to raise taxes.

February 14, 2020, OMG! It’s February 14, 2020, and the national debt is still a ticking time bomb! The national debt: A ticking time bomb?America is “headed toward a crisis,” said Tiana Lowe in WashingonExaminer.com. The Treasury Department reported last week that the federal deficit swelled to more than $1 trillion in 2019 for the first time since 2012. Even more alarming was the report from the bipartisan Congressional Budget Office (CBO) predicting that $1 trillion deficits will continue for the next 10 years, eventually reaching $1.7 trillion in 2030

August 29, 2020, LOS ANGELES, California: America’s mountain of debt is a ticking time bomb The United States not only looks ill, but also dead broke. To offset the pandemic-induced “Great Cessation,” the U.S. Federal Reserve and Congress have marshalled staggering sums of stimulus spending out of fear that the economy would otherwise plunge to 1930s soup kitchen levels. Assuming that America eventually defeats COVID-19 and does not devolve into a Terminator-like dystopia, how will it avoid the approaching fiscal cliff and national bankruptcy?

April 16, 2021, NATIONAL POLICY: ECONOMY AND TAXES / MARK ALEXANDER / The National Debt Clock: A Ticking Time Bomb: At the moment, our national debt exceeds $28 TRILLION — about 80% held as public debt and the rest as intragovernmental debt. That is $225,000 per taxpayer. Federal annual spending this year is almost $8 trillion, and more than half of that is deficit spending — piling on the national debt.

Now, the national debt is approaching $31 trillion,which is $12 trillion more than when Donald Trump took office in 2017 and more than half of that debt was tacked on in his final year. Then we’ve had the disastrous year and a half of Joe Biden.

Now, the Fed is now hiking its rates and that spells even more trouble for the national debt and the economy at large.

December 4, 2022 America’s ticking time bomb: $66 trillion in debt that could crash the economy By Stephen Moore, The national debt is $31 trillion when including Social Security’s and Medicare’s unfunded liabilities. Wake up, America.

That ticking sound you’re hearing is the American debt time bomb that with each passing day is getting precariously close to detonatingand crashing the US economy.

With the U.S. reaching its debt limit of $31.4 trillion on Jan. 19, Treasury Secretary Janet Yellen urged lawmakers to increase or suspend the debt ceiling.

April 22, 2023The Debt Ceiling Debate Is About More Than Debt, Jim Tankersley, WASHINGTON — Speaker Kevin McCarthy of California has repeatedly said that he and his fellow House Republicans are refusing to raise the nation’s borrowing limit,and risking economic catastrophe, to force a reckoning on America’s $31 trillion national debt. “Without exaggeration, America’s debt is a ticking time bomb that will detonate unless we take serious, responsible action,” he said this week.

November 3, 2023 The Fuse on America’s Debt Bomb Just Got Shorter,J Antoni Heritage Organization. The Treasury is now on track to borrow almost as much in just six months as it did in the previous 12 months. That’s nearly a doubling of the deficit. Because the federal debt is $33.7 trillion, just a 1 percent increase in yields adds $337 billion to the annual cost of servicing the debt over time. Absent spending reform, eventually no one will be willing to hold the bomb anymore, and the yields on U.S. debt will begin to resemble those in Argentina.

February 2, 2024How Florida can help defuse the nation’s debt bomb By BARRY W. POULSON,professor emeritus of economics at the University of Colorado Boulder and DAVID M. WALKER,former comptroller general of the United States. Washington’s out-of-control spending, combined with fiscal and monetary policies have resulted in trillion-dollar-plus annual deficits, over $34 trillion in federal debt, over $125 trillion in total federal liabilities and unfunded obligations, and excess inflation. Excessive spending and loose monetary policy increase inflation in the short term, and mounting debt burdens serve to reduce future economic growth and shift the economic burden and consequences of mounting debt burdens to future generations.

February 8, 2024Legendary investor Paul Tudor Jones says a ‘debt bomb’ is about to go off in the U.S.: ‘We’re fast-pouring consumption like crazy’. The U.S. economy may seem like it’s firing on all cylinders, but underneath the surface, a “debt bomb” could be on the verge of exploding, according to billionaire hedge fund manager Paul Tudor Jones. The esteemed investor said in an interview with CNBC that he couldn’t deny the economy was strong, but that it was actually “on steroids” due to massive government spending and borrowing.

Jones is not the only one to call attention to the growing deficit issue in the U.S. On Sunday, Federal Reserve Chairman Jerome Powell took a rare dive into politics, telling CBS’s 60 Minutes that the national debt was “growing faster than the economy,” and calling for lawmakers to get the federal government “back on a sustainable fiscal path.” Meanwhile, U.S. Treasury Secretary Janet Yellen has said she is not yet worried about the increasing national debt as long as the government keeps in check the net payments it makes on its debt relative to GDP.

Those payments are projected to rise from 2.5% last year to 2.9% next year, according to the Office of Management and Budget—below their level in the early 1990s. Jones told CNBC that the strong economy could postpone the effects of the government’s deficit spending, but only for a little while. “The only question is … when does that manifest itself in markets?” he added.

“It could be this year, it could be next year. Productivity may mask and it might be three or four years from now. But clearly, clearly we’re on an unsustainable path.”

June 21, 2024 My Weekly Column: Our debt crisis is a ticking time bomb by Randy Feenstra: On June 18th, the nonpartisan Congressional Budget Office (CBO) – the government agency tasked with monitoring our nation’s fiscal health – confirmed my serious concerns with President Biden’s reckless spending agenda.

His administration’s fiscal policies have not only caused cumulative inflation to skyrocket by over 20% since he took office, but they have also accelerated our accumulation of debt to levels that are beyond unsustainable. Instead of changing course, he recently released his budget for Fiscal Year 2025, which has a $ 7.3 trillion price tag and looks to raise taxes on our families, farmers, and businesses to the tune of $5.5 trillion.

The CBO estimates that his debt “cancelation” policies will cost taxpayers nearly $400 billion over the next ten years. I strongly oppose these bailouts. Iowans who never attended college entered the workforce early or helped put their kids through school should not be forced to pick up the tab for President Biden’s costly and unfair executive orders.

July 22, 2024Federal debt is the ticking bomb in your wallet By E.J. Antoni a public finance economist and the Richard F. Aster fellow at the Heritage Foundation, and a senior fellow at Unleash. The federal government is already running $2 trillion annual deficits, driving up interest on the debt exponentially. The time bomb of federal finance has already started ticking down.

———————–//———————–

The above articles contain the same old lies (“unsustainable,” “cost taxpayers”) that they’ve been telling since 1940. To buttress their lies, they make false comparisons to family finances or the finances of other monetarily nonsovereign entities like businesses or euro nations.

They have been wrong, repeatedly wrong, for all those years. If we wait long enough, something will happen to prove them right, perhaps in a thousand years?

Today, this makes “only” 84 years of the debt nuts’ ignorance.

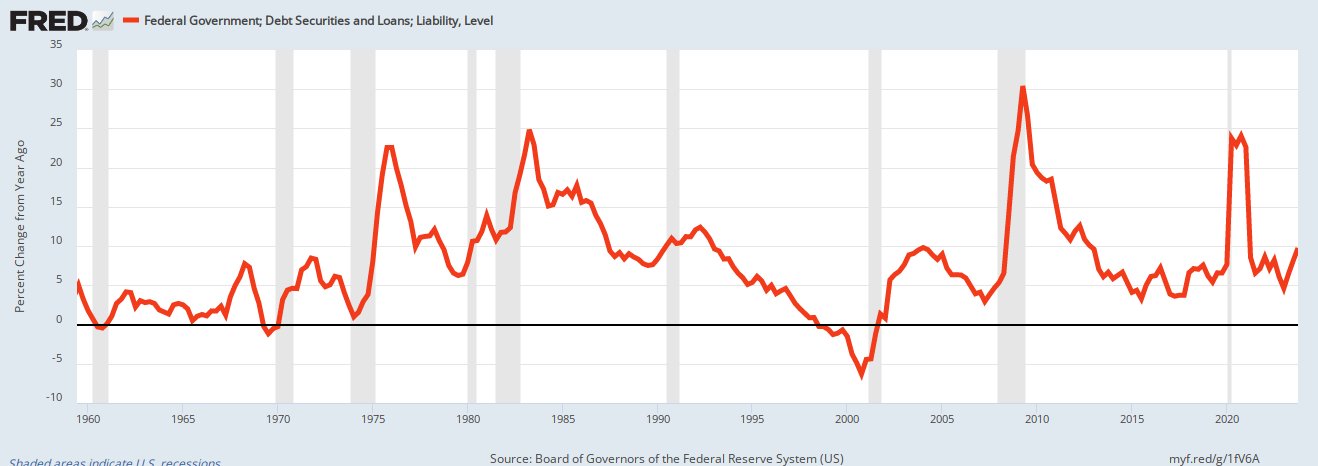

The federal deficit yields economic growth year after year. When deficits are insufficient, we have had recessions, which were cured by increased deficits.

When deficits decline, we have recessions (vertical gray bars), which are cured by increased deficits.

If respected economists keep predicting something terrible is imminent year after year, yet exactly the opposite happens, at what point do they reexamine their beliefs?

At what point does the public say, “Fool me once; shame on you. Fool me repeatedly for 84 years; shame on me”?

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

(Ever wonder why federal spending cuts demanded by debt nuts are designed to widen the income/wealth/power Gap between the rich and the rest, while the few federal spending increases they want are designed to reward and protect the rich?)

There are other examples, but listing them would be wasteful — of your time and mine.

I looked online for claims about federal government wasteful spending. Here are a few of the hundreds I found:

Camo Uniforms for the Afghan Army: The Pentagon spent $28 million on camouflage uniforms for the Afghan National Army that were unsuitable for the desert environment.

Hipster Anti-Smoking Campaign: The National Institutes of Health spent $5 million on a campaign targeting hipsters to stop smoking, including paying them to blog about quitting.

Quail Cocaine Study: Over $500,000 was spent to study how cocaine affects the sexual behavior of Japanese quails.

Hamster Fights: More than $3 million was spent on research involving hamster fights to study aggression1.

Solar Panels for Veterans Affairs: The Department of Veterans Affairs spent $8 million on solar panels that were never used.

The Federal Register–every member of Congress automatically receives a new copy every day, at a $1 million annual cost, even though the contents are available for free online.

I could waste time listing dozens more, but these alone “waste” about $45.5 million a year, which is sufficient to outrage a Congress that voted for these expenditures and the media, which wasted time writing about them, but only on slow news days.

Before I comment further, perhaps we should try to agree on something fundamental: What is “waste”?

I suggest waste is anything that costs significantly more than its benefits over any agreed-upon period.

For instance, let me start with the gross basics: When a bear poops in the woods, is that poop considered waste?

No, because it costs the bear nothing and benefits the forest by providing growth nutrients.

Based on that definition, are the above examples of waste truly waste, or are they more like that cost-free, beneficial bear poop?

This is not a dollar. It is a bearer instrument saying the bearer owns a dollar. The dollar itself is just a number in an account.

Let’s assume there was no benefit to those cameo uniforms, anti-smoking campaigns, quail cocaine studies, etc.

Did they fall under the costs-more-than-its-benefits criterion for waste?

I say, “No.”

Every one of them took dollars from a federal government that has the infinite ability to create unlimited dollars at the touch of a computer key.

So the cost was negligible — perhaps similar to the bear’s cost in expending the effort to squat.

As former Fed Chairman Ben Bernanke said, “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

But what was the benefit? Every one of those endeavors added dollars to the Gross Domestic Product.

Not only did they grow the economy as a whole, but they benefitted specific individuals. Businesses employed people to create those uniforms, the solar panels, and the printed federal register.

People were paid dollars to run the hamster and cocaine studies.

Those people used their newly earned dollars to buy things from other businesses with employees. The new money flowed through the economy, benefiting thousands and then thousands more.

It is quite possible that down the line, you yourself might have received dollars that began with the quail cocaine study.

Should he be afraid to waste sand?

One might object, “Taxpayer dollars were spent. The money came from somewhere.”

In reality, not one dollar, not even one cent, of taxpayer money was spent.

The federal government (unlike state and local governments) pays all its bills with newly created dollars.

Like the first U.S. dollars, created from thin air in 1794, and all subsequent trillions of dollars, the dollars that paid for “wasteful” federal spending were created at no cost, from thin air.

Here’s how it’s done now:

To pay an invoice, the federal government creates instructions (not dollars) from thin air. The instructions are in the form of a check or wire.

The instructions tell the creditor’s bank to increase the balance in the creditor’s checking account (“Pay to the order of _____.”)

The bank obeys those instructions by pressing computer keys. The instant the bank presses those keys, new dollars appear out of thin air and are added to the M2 money supply.

The instructions then are passed to the Federal Reserve which first “clears” them by tallying them against the government’s checking account ( Treasury General Account).

Finally, the creditor’s bank is informed that the check has cleared so it can balance its books.

Everything is just numbers in accounts based on instructions and laws. So long as the federal government can create laws, it can create instructions and dollars. The government has no limits other than the self-imposed.

Many people don’t understand that all dollars are just numbers in accounts. There are no physical dollars. Even a dollar bill is not a dollar. It is the title to a dollar. Just as a house title is not a house, and a car title is not a car, a dollar bill is not a dollar. It is a bearer instrument saying, in essence, “The bearer of this bill is the owner of a dollar.”

Eventually, that paper instrument will be shredded, but dollars, having been created from thin air, are immortal until someone pays off a debt somewhere in the world, at which time dollars will be destroyed.

In summary, all dollars are digital entries—numbers, nothing else. There are no physical dollars. The federal government controls all those entries by passing laws.

To talk about federal waste is akin to saying that the federal government wastes numbers. It’s like worrying that the federal government will run short of the number “seven.”

The federal government can pass a law saying that the Social Security “Trust Fund” now has an additional ten trillion dollars, and those dollars would instantly exist.

It is illogical to claim that the federal government wastes the dollars it has the infinite ability to create. You cannot waste what is available in unlimited quantities.

The real federal waste comes not from faulty spending but from failure to use resources infinitely available.The real waste comes from statements like these:

The Social Security Trust Fund will run out of money in (year).

FICA funds Social Security and Medicare.

Federal trust funds pay for (program).

The Medicare Trust Fund will run out of money in (year).

The debt ceiling is a prudent way to (_____).

The federal government should live within its means.

The federal debt is too high.

The federal deficit is too high.

The federal debt or deficit is unsustainable.

Government spending causes inflation

The federal government can’t afford to pay for (program).

Federal taxes fund federal spending.

Federal funding of (program) is a waste of money

Federal funding of (program) is a waste of taxpayer money.

Federal benefits for (program) must be cut or taxes increased.

The federal government should lend, not give, money to (anyone or anything).

Federal finances are like personal, business, or local government finances

Not one of these commonly heard statements is correct. Not one.

They all mark the writer or speaker as ignorant about our government’s Monetary Sovereignty or as wanting to widen the income/wealth/power Gap between the rich and the rest.

When you read about federal government waste, remember this: When a Monetarily Sovereign government, having unlimited funds, doesn’t spend to feed the hungry, house the poor, or protect its people, that is the worst possible waste, the waste of the government’s power to do good.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell;MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell; https://www.academia.edu/

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

A reader of this blog is concerned about some people’s difficulty understanding Monetary Sovereignty (MS) and asks whether there is some way to present it so that the public can more readily understand it.

Of course, I’ve been attempting to do this for the past twenty-five years, with statements so simple that some economists tell me, “It’s not that simple.”

One risks omitting important details when they simplify an inherently complex subject.

The federal government can be viewed as a combination of Congress, the President, and the Federal Reserve. That combination can be compared to the Bank in the Game MONOPOLY, which, by rule and like the government, cannot run short of dollars.

If you skim through this blog, you will find repeated attempts at simplification.

I have concluded that any failures may be due to different ways of believing.

When I am contacted by someone who understands MS, the communication is cool and data-based. By contrast, I generally receive heat when I receive word from someone who doesn’t get it.

That’s natural, I thought. What is there to be angry about when you agree?

Months ago, I had another thought. It seemed to me that compassion is soft-spoken, while bigotry is angry.

Followers of Biden and now Harris seem to deal thoughtfully with facts, while followers of Trump seem to focus on passion, anger, and conspiracy theories.

Why?

Partly because bigotry is fear and fear is hatred, and those emotions lead to anger.

There is no calm reasoning with a bigoted MAGA who is shouting Fox News and QAnon lies

But I now believe it’s something even more than that. It is because admitting you have been wrong is too painful, even when the admission is secretly in your own mind.

It isn’t that Monetary Sovereignty is complex. It’s dead simple:

The federal government never can run short of its own sovereign currency.

Prices increase when products become scarce.

Raising interest rates increases business costs, which are reflected in price increases.

Deficit spending adds growth dollars to the economy.

Is that too complex for the average person? I think not.

Why do some people feel Monetary Sovereign is difficult to understand? It’s easy to understand, but it’s difficult to believe when you have been subject to many years of brainwashing.

And therein lies the difference.

I’ve spent years trying to help people understand Monetary Sovereignty when their problem is not one of understanding but of believing. That is a much more difficult problem; Reciting the facts won’t solve it.

The MAGAs despise facts. They love conspiracy theories.

When you know you have truth and facts on your side, you might be frustrated by those who blindly accept “alternative facts,” as right-winger Kellyanne Conway famously expressed in defending Sean Spicer’s lies.

You may be frustrated, but not spit-in-your-face, physically-attack-Congress frustrated.

The gun-toting, hate-mongering MAGAs spew vitriol because they know they are wrong. They know Trump is lying to them, taking them for suckers, using them for his own personal gain, and secretly sneering at their ignorance when he’s not on stage.

(“I could shoot someone on 5th Ave. and not lose any followers.” Are those the words of a man who respects his followers’ intelligence?)

So they are angry at being seen as dupes, especially in their own eyes.

They will double down against the obvious and do anything to build a barrier between reality and their foolishness.

They will cover their gullibility with bluster and blindness.

“Wha, wha, I won’t listen to you. I cover my eyes and ears. Your words can’t hurt me.”

To maintain their belief in what they know to be nonsense, they join a mob, scream loudly or even silently, and let the noise in their head cover the truth and their emotion to cover their shame.

Thus, they allow pure belief and worship to wash over them without the burden of honest evaluation.

Hatred and anger are their only defense.

But it is exhausting. As the harsh glare of reality reveals, Trump’s armor is rusty. Each day, more people see the emperor has no clothes.

There stands before them is a befuddled, pitiful, failing old man, mouthing the same lies and insults that no longer fool even the most naive,

He is an often bankrupt business failure, an often losing political failure, an often adulterous marriage failure, an often indicted and convicted moral failure, and a son not even respected by his own late father.

The thrill is gone.

The crowds thin.

Those few who remain look around in embarrassment at their own naivete.

At last, it ends, not with a bang but with a whimper.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell;MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell; https://www.academia.edu/

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

So they are angry at being seen as dupes, especially in their own eyes.

They will double down against the obvious and do anything to build a barrier between reality and their foolishness.

They will cover their gullibility with bluster and blindness.

“Wha, wha, I won’t listen to you. I cover my eyes and ears. Your words can’t hurt me.”

To maintain their belief in what they know to be nonsense, they join a mob, scream loudly or even silently, and let the noise in their head cover the truth and their emotion to cover their shame.

Thus, they allow pure belief and worship to wash over them without the burden of honest evaluation.

Hatred and anger are their only defense.

But it is exhausting. As the harsh glare of reality reveals, Trump’s armor is rusty. Each day, more people see the emperor has no clothes.

So they are angry at being seen as dupes, especially in their own eyes.

They will double down against the obvious and do anything to build a barrier between reality and their foolishness.

They will cover their gullibility with bluster and blindness.

“Wha, wha, I won’t listen to you. I cover my eyes and ears. Your words can’t hurt me.”

To maintain their belief in what they know to be nonsense, they join a mob, scream loudly or even silently, and let the noise in their head cover the truth and their emotion to cover their shame.

Thus, they allow pure belief and worship to wash over them without the burden of honest evaluation.

Hatred and anger are their only defense.

But it is exhausting. As the harsh glare of reality reveals, Trump’s armor is rusty. Each day, more people see the emperor has no clothes. There stands before them is a befuddled, pitiful, failing old man, mouthing the same lies and insults that no longer fool even the most naive,

He is an often bankrupt business failure, an often losing political failure, an often adulterous marriage failure, an often indicted and convicted moral failure, and a son not even respected by his own late father.

The thrill is gone.

The crowds thin.

Those few who remain look around in embarrassment at their own naivete.

At last, it ends, not with a bang but with a whimper.

Rodger Malcolm Mitchell

There stands before them is a befuddled, pitiful, failing old man, mouthing the same lies and insults that no longer fool even the most naive,

He is an often bankrupt business failure, an often losing political failure, an often adulterous marriage failure, an often indicted and convicted moral failure, and a son not even respected by his own late father.

The thrill is gone.

The crowds thin.

Those few who remain look around in embarrassment at their own naivete.

At last, it ends, not with a bang but with a whimper.

Rodger Malcolm Mitchell