OMG! I never thought I would be forced to say this, but the Editorial Board of the Washington Post may even be more ignorant and/or dishonest than the leaders of Fox News.

We’ve published some excerpts from an article that ran today, October 7, 2023, in the Washington Post. It was written by the Post’s “Editorial Board.”

First, here is what the Post says about its Editorial Board:

David Shipley

The Post’s View | About the Editorial BoardEditorials represent the views of The Post as an institution, as determined through discussion among members of the Editorial Board, based in the Opinions section and separate from the newsroom.

Members of the Editorial Board: Opinion Editor David Shipley, Deputy Opinion Editor Charles Lane, and Deputy Opinion Editor Stephen Stromberg, as well as writers Mary Duenwald, Shadi Hamid, David E. Hoffman, James Hohmann, Heather Long, Mili Mitra, Keith B. Richburg, and Molly Roberts.

Now that you know who is responsible, here comes the epitome of misinformation, or dare I say, disinformation.

Opinion Higher interest rates mean greater danger for U.S. debtBy the Editorial BoardOctober 7, 2023, at 7:00 a.m. EDT

Borrowing is expensive again, as anyone who has tried to buy a car or home lately can tell you. The interest rate on 10-year Treasury bonds, the benchmark for home loans, is hovering around 4.75 percent, a nearly two-decade high.

This will significantly add to the federal government’s expenses and raise the urgency to lower the deficit.

Immediately, you see the incredibly ignorant (intentional or otherwise) parallel between personal and federal government finances.

This is Economics 101, folks. You and I are “monetarily non-sovereign. We didn’t create a sovereign currency. We use the currency created by the Monetarily Sovereign U.S. government.

Get it? They are the creators; we are just the users. Huge difference.

As the Monetarily Sovereign creator of the U.S. dollar, the federal government cannot unintentionally run short of dollars.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debtit has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes: Scott Pelley: Is that tax money that the Fed is spending? Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the (checking) account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

This is true of all major currencies created by a Monetarily Sovereign entity like Japan, China, England, the European Union, etc.:

Press Conference: Mario Draghi, President of the ECB, 9 January 2014 Question: I am wondering: can the ECB ever run out of money? Mario Draghi: Technically, no. We cannot run out of money.

The abovementioned Washington Post Editorial Board geniuses presumably have not taken Economics 101; if they took it, they flunked.

Despite its being able to “pay any debt” denominated in dollars, “produce as many dollars as it wishes.” and “simply using the computer to mark up its accounts, the U.S. government’s ability to pay the interest on its T-securities is questioned by the Post editors.

I am stunned by their ignorance, real or feigned.

Interest costs are already the fastest-growing part of the budget. Net interest costs — a nonnegotiable expense — nearly doubled as a share of federal outlays between 2020 and 2023, going from $345 billion, or 5 percent, to $660 billion, or 10 percent. (Defense, by comparison, cost $815 billion, or 13 percent of spending in 2023.)

The higher rates partly reflect the Federal Reserve’s necessary campaign against inflation, but they also mean that the miracle of compounding is now working against the country’s fiscal stability.

The country’s fiscal stability is infinite. If faced with a billion-dollar, a trillion-dollar, or a thousand trillion-dollar invoice, the U.S. federal government could simply “use the computer to mark up the size of the (checking) account” and pay the invoice.

Thus, interest rates do not mean greater danger for U.S. “debt.”

Barring policy changes, recent interest rate increases could add $3 trillion over the next decade to interest costs, according to Marc Goldwein, senior policy director for the Committee for a Responsible Federal Budget.

If the government pays $3 trillion in interest to U.S. security owners over the next decade, that means the government will add $3 trillion growth dollars to Gross Domestic Product.

If some of those dollars go to foreign security holders, that will simply increase foreign citizens’ ability to buy U.S. products.

And all of this will not cost American federal taxpayers one cent. The federal government creates new dollars, ad hoc, every time it makes an interest payment.

It is beyond my belief that the Washington Post’s editors do not understand this fundamental fact about federal finances.

The Department of Health and Human Services announced more than $103 million in funding to address the maternal health crisis.

The money will boost access to mental health services, help states train more maternal health providers, and bolster nurse midwifery programs.

The $103 million will circulate through the U.S. economy, further adding to economic growth.

The doctors, nurses, hospitals, and other health workers will buy products, enriching their sources. Then, those companies that supply doctors, nurses, and hospitals will spend the dollars to enrich their sources.

These initiatives are an encouraging step toward tackling significant maternal health and well-being gaps. In August, the Editorial Board wrote about how the United States can address its maternal mortality crisis.

In addition to financial danger, there’s irony here: While millions of Americans bought or refinanced homes at mortgage rates below 4 percent in recent years and locked those cheap rates for 30 years, the U.S. government failed to do so.

What is the phony “financial danger”? Unlike monetarily non-sovereign state and local governments, the federal government cannot run out of money.

Even if the government did not collect a single penny in taxes, it could continue spending forever.

Top Democratic economists such as Janet L. Yellen and Lawrence H. Summers urged a government borrowing spree during a period of seemingly permanent low-interest rates before 2020.

They argued it was wise to borrow long-term and invest in productivity-enhancing infrastructure, education, and the green transition.

The government borrowed massively in 2020 to keep businesses and consumers solvent during the pandemic.

Think about it. The federal government has the infinite ability to create dollarsby “simply using the computer.” So why would it borrow dollars? It makes no sense at all.

And indeed, the U.S. government never borrows dollars. Never, ever, never.

People borrow to obtain spending or investing money. However, the federal government is “not dependent on credit markets to remain operational.”

Federal T-bills, T-notes, and T-bonds are nothing like private sector notes, bills, and bonds. When you buy a T-security, you are not lending to the federal government. The government does not spend those dollars.

Instead, your dollars go into your account at the Federal Reserve. There, they stay, with interest additions, until maturity, when the federal government returns the balance to you.

There never is a time when the government uses your dollars to pay its bills.

The Biden administration and Congress have subsequently made investments but could not lock in low rates for decades.

There is no reason for the federal government to “lock in low rates.” The more it spends, the healthier the U.S. economy.

That fact is proven by the formula for Gross Domestic Product:

GDP = Federal Spending+ Non-federal Spending + Net Exports

The more the federal government spends, the greater GDP growth is. Locking in low rates would mean the government would pump fewer growth dollars into the economy, the economy would grow more slowly or even shrink, and the federal government would be no healthier than it already is.

The average maturity in the federal debt portfolio is about six years, meaning a huge chunk of government debt must soon be refinanced at high rates.

If the government offers T-securities at high rates, that is good for economic growth (though high interest rates hurt private sector business.)

Consider the three-month Treasury bill. The yield on that was almost zero in 2021. Now, it’s over 5 percent.

That means the government will pump much more growth dollars into the economy. The downside is that businesses and consumers also will pay more interest, so prices will rise.

The irony is that the Federal Reserve increases interest rates to fight inflation, while high-interest costs increase the prices of everything.

Inflation is caused by shortages of vital goods and services and by high-interest rates.

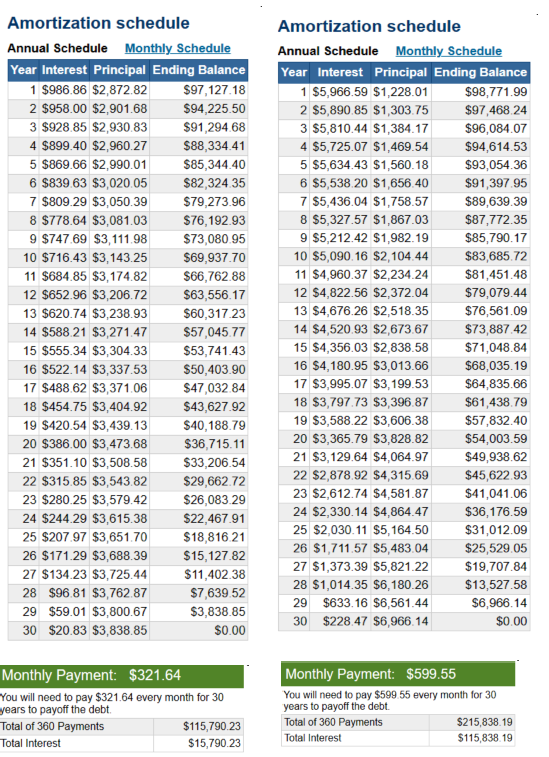

To show you how high-interest rates cause inflation, here is a comparison between two mortgages:

Your house costs you $200,000, so you take out a $100,000, 30-year mortgage. Here are your payments if interest payments are at 1% (left) or if they are at 6% (right.)

With a 1% mortgage, your $100,000 house costs you $115,790. With a 6% mortgage, the same house costs you 215 838.

Now, Chairman Powell, tell me again how your interest rate increases to fight inflation without being recessionary.

Inflation is caused by shortages.The way to fight inflation is for the government to spend more to obtain and distribute the scarce goods and services.

Today’s inflation is caused by shortages of oil, food, computer chips, metals, lumber, labor and other assets. The way to fight this inflation is not to raise interest rates but for Congress to spend more money to obtain and distribute oil, food, computer chips, metals, lumber, labor, and other assets.

There was already a critical need for Congress and President Biden to start addressing the long-term fiscal situation through higher taxes, moderate expense cuts, and adjustments to Social Security and Medicare.

You have just read the most ignorant sentence you will ever encounter.

All three of those suggestions will take dollars out of the economy (which needs a continual flow of dollars for growth or maintenance) while giving those dollars to the federal government, which has infinite dollars.

Higher taxes take dollars out of your pocket, the same effect as inflation has. Federal expense (i.e., spending) cuts cause recessions, taking dollars out of your pocket. And don’t get me started on what cuts to Social Security and Medicare do to your pocket.

Has the Washington Post now become Breitbart?

The Washington Post wants to cut GDP so that the Monetarily Sovereign government won’t run short of the dollars it has the infinite ability to create.

And they want to cut Social Security and Medicare, which should be expanded, not cut. Have they now become a right-wing newspaper akin to Breitbart?

Cutting federal spending to grow the economy is like applying leeches to cure anemia.

We laid out a plan earlier this year to stabilize the debt.

Mathematically, when the so-called debt is stabilized (i.e., doesn’t grow), the economy can’t grow.

The esteemed editors of the Washington Post are calling for a recession, the definition of which is a lack of GDP growth.

The sobering new interest-rate reality makes it even more pressing. Indeed, the infamous crowding-out effect from large federal debts might start making a comeback.

The so-called “crowding-out” effect does not exist. The theory is that if you invest in T-securities, you won’t have enough dollars to invest in private debt.

This never ever has happened in the history of the universe,but economists repeatedly bring it up.

Increases in so-called federal “debt” are caused by increased federal deficit spending, whichputs dollars into your pocket. So, you have more dollars for investing and spending, not fewer.

Instead of providing capital to invest in private business, directly or through the stock market, people with extra cash are likely to choose to earn high rates on less risky government debt.

Again, look at the stock market and tell me whether this has happened. The economists who disseminate the “crowding-out” BS must not own stocks.

This could hurt U.S. growth. One sign that investor caution, and not just Fed policy, is at work: Interest rates on government debt have continued to rise well after the Fed’s last hike, which occurred in July.

The federal government is not market-constrained. It pays whatever interest rates it wishes.

It doesn’t need to sell T-securities. It doesn’t need to set attractive prices for interest rates. As the St. Louis Fed said, the government easily could operate without offering any T-securities.

The purposes of T-securities are:

To stabilize the dollar by providing a safe, interest-paying place to put unused dollars and

To help the Fed control interest rates.

T-securities do not provide the federal government with operating funds. The government never touches the dollars in T-security accounts.

Those accounts are owned by depositors, not by the government. Think of T-security accounts as being like bank-safe deposit boxes. Depositors own the contents of those boxes. The bank never touches them.

With the House of Representatives in chaos, the best hope is for a bipartisan group of senators to launch a debt commission to generate a plan. It might not get taken seriously for a while with the 2024 election looming.

But if interest costs remain high, so will the risks of inaction.

We can only pray that the “bipartisan group of senators” understands economics better than the Editorial Board of the Washington Post.

Here is the Republican solution to student debt, as brought to you by the Libertarian Reason.com

Can Republicans Fix Student Debt?Unlike Democrats, Senate and House Republicans have released proposals that would actually tackle the root causes of increasing student loan debt.Emma Camp | 6.16.2023

As a long-awaited Supreme Court decision on President Joe Biden’s massive student loan forgiveness plan looms, Senate Republicans have unveiled a plan of their own to address the nation’s climbing student loan debt burden.

However, instead of promising blanket forgiveness, the Senate Republicans’ plan aims to reform how student loans are given out in the first place—seeking to direct students toward high-quality programs and limit access to schools that provide a poor return on students’ investment.

As you will see later in this “plan,” the Republicans believe the only purpose of attending college is to make more money. They measure “return on students’ investment” solely by the salaries students will receive after graduation.

The plan is composed of five separate bills. Three of the bills focus on ensuring that prospective borrowers are aware of the financial tradeoffs of taking out student loans and the financial outcomes for alumni of specific institutions.

The last two tackle the federal student loan system itself, cutting down the number of repayment plans and limiting the circumstances in which federal student loans can be given out.

The first bill in the package focuses on increasing transparency from colleges.

The bill seeks to require colleges and universities to provide a wide range of data on student outcomes and enrollment trends to the National Center for Education Statistics, which would create a database of this information aimed at helping prospective students make informed educational decisions.

Transparency is a good thing.

“Student outcomes” might have to do with graduation rates, dropout rates, advanced degrees, and employment after graduation. But they wouldn’t measure what students learn.

And most importantly, it doesn’t address the student loan indebtedness problem.

Can anyone tell me why a nation whose competitiveness relies on its young people to being educated wants to “limit the circumstances in which federal student loans can be given out?”

If the Republicans ran a company, would they want to limit the circumstances in which the company could profit?

It’s absolutely nuts, especially since the U.S. federal government has infinite dollars.

The proposal’s second bill would require colleges and universities to use a standardized financial aid offer form to maximize transparency around the true cost of attending a given institution.

The third bill in the proposal has similar aims, requiring that students applying for federal student loans receive information detailing sample payments for their loans, as well as how long they would expect to be paying off their student loans and what income they can expect to make after graduating from a given school.

These two “solutions” are reasonable in that they provide borrowing information. But they still fall far short of solving the student loan indebtedness problem.

They merely say, “Here’s what it will cost you, and if you can’t afford it, don’t go to college or take out a loan.”

But the purpose of the student loan program is to enable more children to attend college, not to winnow down the number that can afford it.

The fourth bill cuts down on the number of repayment plans available to borrowers.

The bill would consolidate the host of current repayment options down to two—a standard 10-year repayment plan and a Revised Pay As You Earn (REPAYE) repayment plan with minor changes.

The REPAYE plan is an income-driven repayment (IDR) plan, which currently allows borrowers to pay a monthly amount fixed to their income, achieving forgiveness after at least 20 years of payments.

Importantly, the fourth bill also cuts off access to federal student loans for students attending programs that do not result in median earnings higher than those of adults who only have a high school diploma—or a bachelor’s degree, in the case of a graduate program.

To Republican minds, the purpose of attending college is to make more money. Otherwise, it supposedly is a waste of time and money.

The right-wing mentality says that the arts — music, dance, painting, theater, writing, sculpture, etc., — should be measured by how much money you can make from them.

History and philosophy also should be measured by the money you can make, not by their contributions to human culture. Mathematics, too. And teaching. And physics.

To the right-wingers, if your education doesn’t pay you more money, the government shouldn’t help you, no matter how valuable to America it might be. WHY?

Most importantly, the Republicans assume college has no social benefits. But, the 18 through 24 age period is a maturation time, a time to go from childhood to adulthood.

College provides the non-financial benefits of learning about the world along with other young people of like age.

Again, the Republicans measure everything by dollars, while falsely claiming the government doesn’t have enough dollars.

The final bill in the package would eliminate Graduate PLUS Loans—a type of federal student loan whose borrowing cap was removed in 2006.

The removal of this cap has been directly connected to a rapid increase in graduate school tuition, as—unlike for undergraduate programs—graduate students were able to borrow an unlimited amount from the federal government, incentivizing universities to jack up prices.

The function of the student loan program is to help more students afford college. So, of course, colleges have more room to “jack up” prices with more students able to pay. That is a fundamental result of affordability.

The government must pump more growth dollars into the economy when colleges increase prices. That benefits the economy.

Capping loans merely means that fewer students will be able to afford advanced degrees.How does that benefit America? It doesn’t. It simply reduces the number of highly educated Americans and widens the income/wealth/power Gap between the rich and the rest.

Notably, House Republicans have also introduced their own legislation aiming to reform federal student loans.

Their proposal would provide “targeted” student debt relief to those who have consistently made payments but have seen their debt increase anyway.

The GOP (aka, “the party of the rich”) wants to give “targeted” relief to those who were able to afford debt payments, conveniently leaving out those who were financially weaker and unable to make payments.

The proposal would also reform existing income-driven repayment plans and mandate considerable warnings for borrowers before student loan payments resume in October.

“Colleges and universities using the availability of federal loans to increase their tuitions have left too many students drowning in debt without a path for success,” said Sen. Bill Cassidy (R–La.) in a Wednesday statement.

No, Sen. Cassidy, the government has left students drowning in debt by lending them money that should have been given.

Grades K-12 have been government supported for centuries. Grades 13+ also should be government-funded, not just at community schools, but top schools, too.

The more kids who decide to go for advanced degrees, the better off America will be.

“Unlike President Biden’s student loan schemes, this plan addresses the root causes of the student debt crisis. It puts downward pressure on tuition and empowers students to make the educational decisions that put them on track to academically and financially succeed.”

No, it cleverly disempowers poorer students and widens the education gap between the rich and the rest. It does nothing about the “root causes of the student debt crisis.”

The Republicans’ plans offer a constructive solution to the problems that plague the federal student loan system. Rather than focusing on short-term solutions—like Biden’s $400 billion student loan forgiveness boondoggle—Republicans’ plans target the sloppy government policies which directly cause rising student debt.

In particular, the Senate’s attempt to eliminate Graduate PLUS Loans and both plans’ proposals to reform income-driven repayment plans take direct aim at some of the most fiscally irresponsible federal student loan policies.

To Republicans, “fiscally irresponsible” means money going to the poor and middle classes. Notably, it does not mean the tax loopholes given to the rich.

While both bills face an unlikely path toward actually becoming law, they provide a clear template for what a sensible response to the student loan crisis looks like—and policies that are actually likely to lower the cost of college, not raise it.

Except, the bills ignore the fundamental purpose of education in America: To improve America.

The original Colonists understood that. Sadly, today’s inferior crop of politicians is so taken with what’s in it for them that they completely ignore the question, “What’s in it for America.”

THE ROOT CAUSES OF THE STUDENT DEBT CRISIS

Educating young people benefits America. That is why the American colonies mandated free education for our children.

And that came when reading, writing, and arithmetic were much less important to our agrarian society than they are today.

Yet, taxpayers willingly bore the cost of education.

Today, primary education and especially advanced education are far more critical. The world has advanced, and to remain competitive, America must rely on its educated young people.

There are three root causes of the student debt crisis:

Attending college is expensive. Many families find tuition, food and lodging, books, and materials unaffordable.

Not having a job is expensive. Many children can’t afford college because their families need them to stay home and work full-time. Even with a free ride that includes everything in point #1, some kids can’t afford not to work full time.

The federal government, which has infinite dollars, lends rather than giving money to the students.

The latter point is an extension of the false belief that our Monetarily Sovereign government’s finances are like personal finances.

The ignorant idea that the federal government spends too much contradicts the simple formula: Gross Domestic Product (GDP) = Federal Spending + Nonfederal Spending + Net Exports.

GDP is the measure of our economy, so by formula, increased Federal Spending grows our economy, and decreased Federal Spending shrinks our economy. Simple algebra.

Thus, the Federal Government never should lend to Americans; it only should give to Americans.

The student debt crisis results from requiring students to borrow from the government rather than receiving dollars with no payback requirement.

The government neither needs nor even uses the dollars that are paid back. The solution to the student debt crisis is straightforward. Just as local governments fund local schools, the federal government should fund colleges and universities.

In fact, the federal government can do it more easily than can local governments because the federal government uniquely is Monetarily Sovereign; it cannot run short of dollars.

The federal government even should pay students a salary for attending college, so the students’ college attendance does not penalize the student’s family monetarily.

It is beyond stupid for the U.S. government to take dollars from students when America’s competitive position depends on our young people being educated, and the government has infinite money to pay for their education.

Of course, a government that refuses to recognize Monetary Sovereignty and the formula GDP = Federal Spending + Nonfederal Spending + Net Exportsis already beyond stupid, so the extra stupidity is to be expected.

I often listen to the public radio show, “Freakonomics Radio” by Stephen J. Dubner. Today, the story was about insurance and how intractable it is, both from the insurance providers’ and the buyers’ perspectives.

We all have some forms of insurance: Life, health, accident, liability, home, personal property, unemployment, retirement, and many others.

Lloyds of London has a reputation for creating individualized policies to insure anything: An actress’s legs, a quarterback’s arm, a pianist’s fingers.

Among the several insurance problems, the fundamental problem is adverse selection. The insurance company wants to cover people who will not have an immediate claim. The buyer wants to get his money’s worth in claims.

A life insurance seller wants young, healthy customers who will not make claims for many years while paying premiums all those years.

All insurers want the insured to buy as soon as possible, then wait a long time before making a claim (for instance, a health policy) or never make a claim (an auto liability policy),

But the insured ideally would like to purchase his insurance as late as possible — just before making a claim — or never.

To minimize adverse selection, insurers hire actuaries. These people use research and probability formulas to determine the likelihood of a person making a claim and how significant that claim is might be.

This leads to another problem: Adverse denial. Suppose those who will make the fewest and most minor claims are the only people accepted, and all others are denied. In that case, many people will be denied insurance, and the basic premise of insurance — to protect against misfortune — would be lost.

For example, on average, black people get sick and die sooner than white people. If the law allowed, insurance companies would charge blacks higher premiums than whites or refuse insurance to blacks altogether.

However, the law does not allow this, so the premiums charged to white people must be higher than they ordinarily would be to make up the difference.

Any time an insurer accepts something other than the lowest possible risk, the lowest risk people must pay more. Some, but not all, of this can be baked into the premiums. For example, most life insurance policies consider age and prior illness when determining premiums. But no insurer can consider every possible risk category and remain competitive.

So, in general, the lowest-risk people do, in part, fund higher-risk people for all sorts of insurance.

That said, a substantial portion of our population is not financially protected by insurance, either because no company will insure them or because the premium is higher than what people wish to pay.

In short, the risk is too high for any potential insurer, and the premium is too high for potential insureds.

The fact that the problem is considered intractable puzzles me because we already have solved it, not just once, but many times.

Medicare, for instance, solves it for the worst health risks: Older people who already are sick with terminal illnesses cannot be refused when they reach the qualifying age.

More than 18 percent of Americans depend on Medicare for their health coverage, and in 2019 Medicare the enrollment reached over 60 million.

You can start receiving Medicare Part A (hospital insurance) benefits with no premium once you are 65 or older if you or your spouse worked and paid Medicare taxes for a certain period. You can know you are eligible for premium-free Medicare A if one of the following applies to you:

You currently receive or are eligible for Social Security.You currently receive or are eligible for Railroad Retirement Board (RRB) benefits.You or your spouse served in a Medicare-covered government job.

You can purchase Medicare Part B benefits if you are eligible for Medicare Part A. It is a voluntary program that requires you to pay monthly premiums. For 2022, the standard premium is $170.10 (or higher, depending on income).

No matter how sick you are, even on death’s doorstep, you can receive insurance if you meet the above requirements.

How does the government avoid adverse selection? Mostly, it doesn’t. Yes, there are qualifications; adverse selection is not the consideration.

Why can the government afford Medicare when private insurance companies must worry about adverse selection? Contrary to popular belief, people with FICA deducted from their salaries do not fund Medicare.

The federal government, being Monetarily Sovereign, has the infinite ability to create U.S. dollars.

It neither needs nor uses tax dollars to pay for anything. Even if total FICA collections equaled $0, the federal government still has the infinite power to fund something better than our current Medicare.

The government could fund a comprehensive, no-deductible Medicare for every man, woman, and child in America.

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes:Scott Pelley: Is that tax money that the Fed is spending?Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

And that is the solution to the healthcare insurance problem. The federal government should “use the computer to mark up the size of the account” and fund a form of Medicare far better than current Medicare.

I have Medicare, but I also pay for a concierge primary care doctor. I pay her an annual fee in addition to what she receives from Medicare.

My previous primary care doctor, who received Medicare reimbursement, had about 2,500 patients. My concierge doctor self-limits to about 600 patients. This allows her more time to do precisely what she studied for years to do: Treat patients.

She spends time studying my particular needs and discussing my health with me. If I go into the hospital, she has admittance privileges and can oversee my treatment there while discussing my case with all the doctors and nurses.

The federal government has sufficient resources to pay every primary care doctor to be a concierge doctor who can spend the time each patient deserves.

(The federal government also has the resources to provide free medical schooling for all prospective doctors, so there would be plenty of people available to be the abovementioned concierge doctors.)

All drivers need auto liability insurance. The federal government should provide it free. All homeowners and renters need insurance. The federal government should provide it.

There is no logical reason why more affluent people can afford insurance while poorer people cannot. Ironically, it is the poorer who need insurance more than, the richer.

The Freakonomics radio show ignored the fundamental truths about the American economy:

The solution to many of life’s problems stares us in the face, yet disinformation from the top prevents it.

No, federal financing is not the dreaded “socialism” (which is government ownership and direction, not just government funding.)

And no, federal spending does not cause inflation. On the contrary, federal spending can reduce inflation by acquiring goods and services, the scarcity of which is the real cause of inflation.

There is a solution. We need only to recognize it.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

A step in the wrong direction does more than fail to get you to your destination. It takes you farther from your destination.

Smallpox: Evil spirits aren’t what cause smallpox. Any efforts to prevent and cure smallpox via exorcism would have been wasted.

Worse, they would have led us down the wrong path, taking time, effort, and money from finding and addressing the actual cause, a virus. Worse than doing nothing, a false belief does real harm.

Before vaccination was invented, doctors gave smallpox victims “supportive care, ” mainly of fluids to prevent dehydration. The patient was isolated until all scabs had fallen off to prevent disease transmission.

One of the leading theories suggests that Alzheimer’s disease is caused by the abnormal accumulation of two proteins called amyloid beta and tau in the brain, resulting in plaques and tangles.

Despite the huge amount of research that’s happened to date, there’s not been much success in treating and preventing Alzheimer’s disease.

This has led many experts in the field to wonder whether there’s something else we should look at to understand and cure Alzheimer’s disease.

A recent article in New Scientist Magazine highlights an alternative theory: that damage to mitochondria (the energy-producing structures within cells) could actually be the cause of Alzheimer’s.

The focus on ridding the brain of amyloid didn’t work, but actually may have hindered efforts to find the real cause of Alzheimer’s.

—————————————————————

Inflation: Inflation is a general increase in prices. Bing AI says: Inflation is caused by two main factors: demand-pull and cost-push. Demand-pull inflation occurs when demand from consumers pulls prices up.

Cost-push inflation occurs when supply costs force prices higher. Inflation can also occur when prices rise due to increases in production costs, such as raw materials and wages.

“Demand-pull” and “cost-push” are classic descriptions of inflation’s causes. They can be found in many economics textbooks. There are two problems with these supposed causes:

They don’t explain what has happened. They only describe what is. But, inflation is a dynamic process. Something changes to cause inflation. An economy moves from normal pricing to inflation.

Re. Demand pull: What causes a sudden, general increase in consumer demand? Anything? Do you know any examples of sudden increases in the consumer demand for a wide range of products and services?

Re. cost-push. This supposed explanation is a tuatology: In essence it says, prices increases because prices increase. It does not explain what has caused the inflation in supply costs. It merely passes the blame downstream.

Inflation is caused by shortages of crucial goods and services, usually oil, food, and/or labor.

Oil shortages do not come about because of sudden increases in the demand for oil. They are caused by sudden reductions in supply, which may be due to decisions by oil suppliers like OPEC (Organization of the Petroleum Exporting Countries), Canada, and the U.S. itself.

Food shortages do not come about because of sudden increases in the demand for food. Food shortages can be caused by weather, crop disease, and/or government decisions.

Today’s inflation is caused by COVID-related and human-caused shortages, not by sudden increases in demand.

COVID reduced the world’s ability to drill, refine, and ship oil, which affected the prices of nearly every product and service on the planet. COVID impacted the supply of food and labor. COVID isn’t finished with us. The aftereffects still can be felt.

Oil drilling and refining still are down, partly because of COVID and partly because of OPEC and the Russa/Ukraine war. Food shortages result from oil shortages, weather anomalies, COVID-related labor and supply-chain shortages.

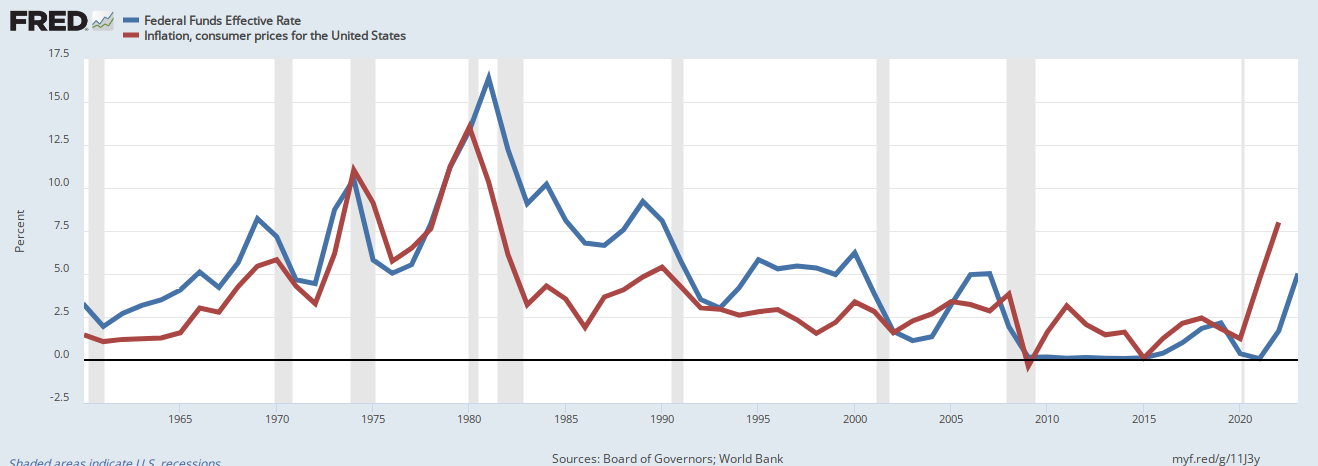

There is no evidence that inflations are caused by interest rates being too low.

The graph demonstrates the Fed’s failed attempts to fight inflation (red line) by raising interest rates (blue line). In the 23 year period, from 1967 through 1990, the Fed raised interest rates to extraordinarily high levels, but inflation also kept rising to high levels, only to fall before or during recessions.

Similarly, in the 12-year period, from 2008 to 2020, interest rates were kept extraordinarily low, while inflation remained low.

Twenty three years of high interest rates did not cure inflation and eight years of low interest rates did not cause inflation.

So what caused inflation and what cured inflation?

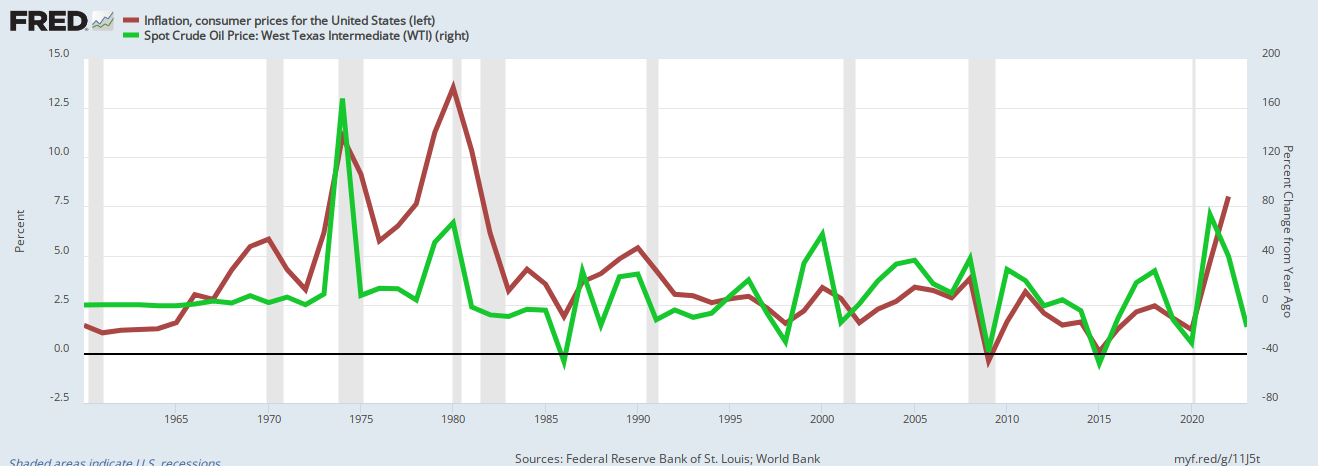

Oil prices (green line) respond to supply and demand. When oil is scarce, prices rise. When oil is plentiful, prices fall.

The graph demonstrates that inflation responds to oil scarcity, because oil availability affects the pricing of most other products and services.

Historically, the primary cause of inflation has been scarcities of oil, which have led to high product and service prices.

Today’s inflation has also been caused by COVID scarcities, not only scarcities of oil but of food, computer chips, supply chain availabilities, construction materials, labor, etc. COVID affected everything.

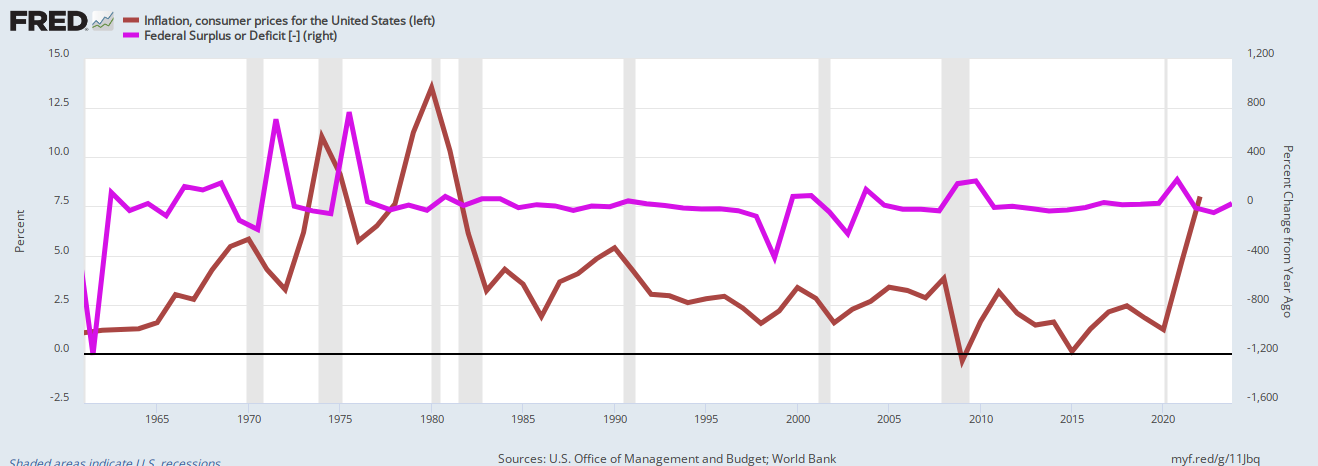

There are those who take the Libertarian view that federal deficit spending causes inflation. History does not support this belief

Changes in federal deficit spending (purple line) bear little relationship to inflation (red line). Increases in federal deficit spending do not correspond to high inflation, nor do decreases in deficit spending correspond to low inflation.

SUMMARYThe prevention and cure for a disease requires the prevention and cure for the cause of the disease.

Evil spirits and lack of fluids did not cause smallpox, so fighting evil spirits/dehydration did not prevent or cure smallpox.

If damage to mitochondria, not the accumulation of amyloids in the brain, proves to be the cause of Alzheimer’s, curing amyloids will not prevent/cure Alzheimers, but preventing/curing damage to mitochondria will.

Low interest rates do not and have not caused inflation, so raising interest rates will not prevent/cure inflation.

Inflation is caused by shortages, most often shortages of oil or food. Today’s inflation is caused by multiple, COVID-related shortages, and curing those shortagesis the only way to cure inflation.

Our Monetarily Sovereign federal government, having the infinite ability to create dollars, should fund efforts to increase availabilities of oil, food, computer chips, construction materials, and labor.

Decreasing in taxes on businesses and employees would be a good place to begin.

For example, the FICA tax, which serves no purpose, raises the price of goods and services, and discourages employment. Eliminating FICA would be a good, easy first step toward reducing inflation.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

If the Republicans ran a company, would they want to limit the circumstances in which the company could profit?

If the Republicans ran a company, would they want to limit the circumstances in which the company could profit? The graph demonstrates the Fed’s failed attempts to fight inflation (

The graph demonstrates the Fed’s failed attempts to fight inflation ( Oil prices (

Oil prices ( Changes in federal deficit spending (

Changes in federal deficit spending (