Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

============================================================================================================================================================================================================================================================

In the previous chapter, “The Dollar,” we saw how the US dollar is not a physical entity, but rather is nothing more than an accounting notation — i.e. numbers in an account. Unlike physical objects, numbers have no limit. The government never can run short of numbers.

We also saw that dollars are debts of the US and that the value of any debt is supported by its collateral. While gold and silver often have been part of the collateral for the US dollar, today (as of August 15, 1971) the collateral for the dollar solely is the full faith and credit of the US government.

The word “debt” has powerful, yet ambiguous emotional connotations. For most people, “owing debt” seems financially dangerous, while “paying off debt” seems financially prudent. Yet, among house mortgages, auto payments and credit cards, the vast majority of us “owe debt,” and this includes even the richest 1% of us.

If you are a lender, you own debt. If you own a bank savings or checking account, or a bank CD, or a T-bill, T-bond or T-note you are a lender.

Your bank owes you the dollars deposited into your savings or checking account or CD. They are debts of your bank. They are the way banks do business.

Though deposits are bank debts, banks boast about the amounts of their deposits. As a rule, the bigger the bank, the greater the deposits, the more debt. You seldom will read or hear any concerns about the amount of debt (i.e. deposits) a bank has, and in fact, the term “debt” seldom is used.

One way to lend to your bank is by making a deposit in your checking, savings or CD account. The total amount deposited in US banks is $12 trillion. This is the amount banks owe to their depositors.

Though these accounts constitute bank “debt,” no one other than an accountant calls it “debt.” Everyone refers to it as “deposits.”

As a depositor, you continue to own the dollars you deposited (Otherwise, they would be a gift, not a debt.) And the bank owns those dollars, too, which it invests for profit. By depositing, i.e. by lending to the bank, you increase the supply of dollars in the economy.

The evidence for your ownership of those dollars might be your passbook or online numbers in your account.

To lend to the US, you can buy a T-bond, T-note or T-bill, that is, you can make a deposit in your T-security account at the Federal Reserve Bank. The total of those deposits is $19 trillion, or said another way, the total US debt is $19 trillion.

In short, the US debt is nothing more than the total of deposits in the FRB.

Buying a T-bond is much like buying a bank CD, and having your T-bond “paid off” is much like having your bank CD paid off. In both cases, a bank (FRB or private bank) debits your bank account and credits your checking account. NO ADDITIONAL DOLLARS NEEDED

Knowing that federal “debt” is simply the total of deposits in T-security accounts at the world’s safest bank, the FRB, what do you make of this web site: fixthedebt

The Era of Declining Deficits is Over

January 27th 2016The Already Unsustainable Debt Path Is Now Much Worse

The official budget and economic forecast from the nonpartisan Congressional Budget Office shows that the era of declining deficits is over.

–The deficit will stop declining this year and start growing again.

–Trillion-dollar deficits will return by 2022.

–The national debt will grow by more than $10 trillion over the next decade.Irresponsibility in Washington Is a Chief Culprit in the Worsened Outlook

–Last year, Congress added over $1 trillion to the projected debt in 2026 by passing unpaid-for tax breaks and Medicare spending increases.

–Failure to follow the “pay-as-you-go” law that requires paying for new policies is responsible for roughly half of the deterioration of the country’s fiscal outlook from last year.

–If policymakers continue to act irresponsibly, instead of taking positive action to get the debt under control, the debt projections will be much worse. This could add an additional $1.4 trillion to the debt, making it reach 91 percent of the economy by 2026.

Well, that’s pretty ominous: “Unsustainable, act irresponsibility, deterioration of the country’s fiscal outlook, 91 percent of the economy.”

Before we analyze the validity of these warnings, consider the two luminaries who founded fixthedebt: The notorious Erskine Bowles and Sen. Alan Simpson, Co-Chairs of the National Commission on Fiscal Responsibility and Reform

They suggested balancing the federal budget by taking huge cuts out of Social Security and Medicare, while “broadening the tax base” (i.e. taxing the lower income groups more.) The upper 1% income groups loved it, as did the media, economists and politicians.

The ominous warnings are not new. We published a post showing how, as far back as 1940, and undoubtedly further back than that, the federal debt was referred to as a “Ticking Time Bomb.”

Seventy-five years have passed since that warning. The federal debt has risen from just $42 billion to an astounding $14 trillion — and the “time bomb” still is ticking.

At what point do we begin to understand that the warnings are bogus? Personally, I would be embarrassed to predict disaster for 75 years, only to be proven wrong again and again. Apparently, the fixthedebt folks don’t feel shame.

They use the word “unsustainable” to describe the federal debt and deficit, but they never explain what they mean.

Do they mean the federal government will run short of dollars to service its so-called “debt”? No, I’ve never seen them write that; they know our Monetarily Sovereign, federal government is not like state, county, city and euro nation governments.

Those governments can run short of the currency they use. The federal government cannot run short of its own sovereign currency.

What evidence is provided by “fixthedebt? I found these statements on their website:

The long-term growth in the debt will be largely driven by rising health care costs and an aging population. Nearly half of the projected increase in total spending from 2016 to 2026 is for Social Security and Medicare.

Rising debt will impede economic growth and impair the standard of living for Americans.

Ever-growing levels of debt threaten citizens’ and families’ economic well-being in a number of ways. A large debt:

–Hurts wages and jobs

–Makes borrowing more expensive for important investments

–Harms our children

–Threatens the safety net

–Risks a real crisis

–Prevents us from growing the economy

With the proposed “cure”: Cut Social Security and Medicare benefits, you are supposed to believe this will not “impair the standard of living for Americans.”

Actually, it won’t impair the standard of living for rich Americans.

Here’s a bit more:

As the government continues to issue more and more debt, the debt “crowds out” productive investments in people, machinery, technology, and new ventures.

This is the old, nonsensical, “crowds-out,” mantra. Federal deficit spending adds dollars to the economy. How can adding dollars by purchasing goods and services from the economy and by putting more dollars into people’s pockets “crowd out” investments?

Quite the opposite, federal deficit spending is stimulative. It is the method by which the federal government frees us from recessions and depressions. The Great Depression was cured with the deficit spending of WWII. The recent Great Recession was ended with stimulative deficit spending.

Growing national debt can drive up interest rates throughout the economy, leading to higher interest payments on mortgages, car loans, student loans, and credit card debt. Although rates are currently low—due mainly to the weak economy and temporary efforts by the Federal Reserve to keep them down — they will most certainly rise as the economy recovers, and they will rise much higher if debt continues to grow.

Completely backwards. The national debt has been growing for 75+ years and until recently, interest rates began at zero.

They have gone up a bit now, not because of the debt, but because the Fed increased them. Even fixthedebt admits the Fed, not the debt, controls interest rates.

And note that phrase, “as the economy recovers.” Fixthedebt predicts terrible effects from a rising debt, while simultaneously predicting the economy will recover!

Growing national debt means that the government must pay higher interest payments to service that debt. The nonpartisan Congressional Budget Office projects interest costs will more than triple from about $250 billion in 2016 to more than $800 billion in ten years.

By 2030, 100 percent of the revenue we collect will go toward interest payments and mandatory spending. That leaves little room for important priorities and investments such as national defense, education, infrastructure, low-income support, and basic research.

This is based on the false premise that federal taxes pay for federal spending. If taxes paid for spending, there would be no deficit. So what fixthedebt seems to be saying is, the sale of T-securities (i.e. debt) limits the government’s ability to spend on priority items.

Of course, we know that isn’t true, because the federal government pays its bills by creating dollars ad hoc, and never can run short of dollars. So its ability to spend cannot be limited.

Further, do you remember the Fed’s Quantitative Easing (QE) program? It was a program in which the Fed purchased securities from the private sector.

During QE, the Fed purchased $3.5 TRILLION worth of debt, and now owns close to $4.5 TRILLION in debt.

Where did the Fed get the $4.5 trillion to take that much debt off the market? It’s the government’s bank. As such, it’s ability to create dollars is limited only by its ability to press computer keys. That is the meaning of Monetary Sovereignty.

And those T-securities continued to earn interest; the Fed paid the U.S. Treasury nearly $500 million in interest over the past six years.

Because dollars are infinitely available to the federal government, money freely moves from the left-hand pocket (the Fed) to the right-hand pocket (the Treasury) and back again.

The trustees who oversee Social Security and Medicare estimate both are on a road to insolvency. Social Security’s Disability Insurance trust fund will become exhausted in 2022, and Medicare’s Hospital Insurance trust fund will be exhausted in 2030.

Here again, fixthedebt pretends the US is not Monetarily Sovereign and can run short of its own sovereign currency — the basic element of the Big Lie. Because Social Security and Medicare are federal agencies, they can run short of dollars only if Congress and the President will it.

Failure to get the national debt under control could precipitate a crisis where investors are no longer willing to loan money to the government at affordable rates.

Two lies in one sentence: First, when it comes to the federal government all rates are “affordable.” Second, because the government cannot run short of dollars, it never needs to borrow or rely on investors.

Finally, fixthedebt describes itself as “nonpartisan.” This is a popular ploy, to give legitimacy to a questionable group. Fixthe debt is about as nonpartisan as the Republican National Committee, and about as truthful.

In short, concerns about a non-existent, but never-ending, imaginary debt crisis, constitute a pack of lies and misleading statements, which together form the Big Lie.

We discussed the lies, misstatements and misleading comments found on the fixthedebt website, but there are dozens of such sites, mostly supported the by the richest .1% of us.

Most of them confuse federal deficits (the difference between taxes and spending) with federal debt (the total of T-security accounts at the Federal Reserve Bank). It is possible to have federal deficits without federal debt (Don’t sell T-securities), and it is possible to have federal debt without federal deficits (Sell T-securities even when taxes equal spending).

———————————-//————————————————

Next, we will discuss the question of motive: Why do so many politicians, media and university economists tell the Big Lie.

Rodger Malcolm Mitchell

Monetary Sovereignty

===================================================================================

Ten Steps to Prosperity:

1. Eliminate FICA (Click here)

2. Federally funded Medicare — parts A, B & D plus long term nursing care — for everyone (Click here)

3. Provide an Economic Bonus to every man, woman and child in America, and/or every state a per capita Economic Bonus. (Click here) Or institute a reverse income tax.

4. Free education (including post-grad) for everyone. Click here

5. Salary for attending school (Click here)

6. Eliminate corporate taxes (Click here)

7. Increase the standard income tax deduction annually Click here

8. Tax the very rich (.1%) more, with higher, progressive tax rates on all forms of income. (Click here)

9. Federal ownership of all banks (Click here and here)

10. Increase federal spending on the myriad initiatives that benefit America’s 99% (Click here)

The Ten Steps will grow the economy, and narrow the income/wealth/power Gap between the rich and you.

——————————————————————————————————————————————

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

![]()

No nation can tax itself into prosperity, nor grow without money growth. Monetary Sovereignty: Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

1. A growing economy requires a growing supply of dollars (GDP=Federal Spending + Non-federal Spending + Net Exports)

2. All deficit spending grows the supply of dollars

3. The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

4. The limit to non-federal deficit spending is the ability to borrow.

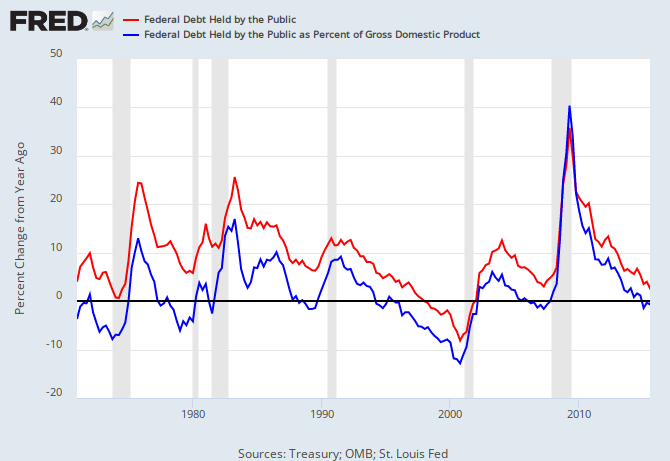

THE RECESSION CLOCK

Recessions begin an average of 2 years after the blue line first dips below zero. There was a dip below zero in 2015. Recessions are cured by a rising red line.

Vertical gray bars mark recessions.

As the federal deficit growth lines drop, we approach recession, which will be cured only when the growth lines rise. Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

Mitchell’s laws:

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money.

•The more federal budgets are cut and taxes increased, the weaker an economy becomes..

•Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

•The single most important problem in economics is the Gap between rich and the rest..

•Austerity is the government’s method for widening the Gap between rich and poor.

•Until the 99% understand the need for federal deficits, the upper 1% will rule.

•Everything in economics devolves to motive, and the motive is the Gap between the rich and the rest..

MONETARY SOVEREIGNTY