It takes only two things to keep people in chains:

The ignorance of the oppressed

and the treachery of their leaders.

——————————————————————————————————————————————————————————————————————————————————————————–

Here is why I agree with Trump and the GOP — almost — even though he and they don’t understand exactly what they are lying about:

Deficit worries complicate path for Republican tax cuts

Reuters, By David MorganWASHINGTON (Reuters) – Unease among Republicans about a massive increase in the federal deficit could complicate passage of two tax-cut bills working their way through the U.S. Congress, endangering President Donald Trump’s top legislative priority.

The Committee for a Responsible Federal Budget (CRFB), a nonpartisan budget watchdog in Washington, on Friday called a Senate Republican tax plan a “fatally flawed budget buster,” likening it to Republican legislation in the House of Representatives that the House tax committee has approved.

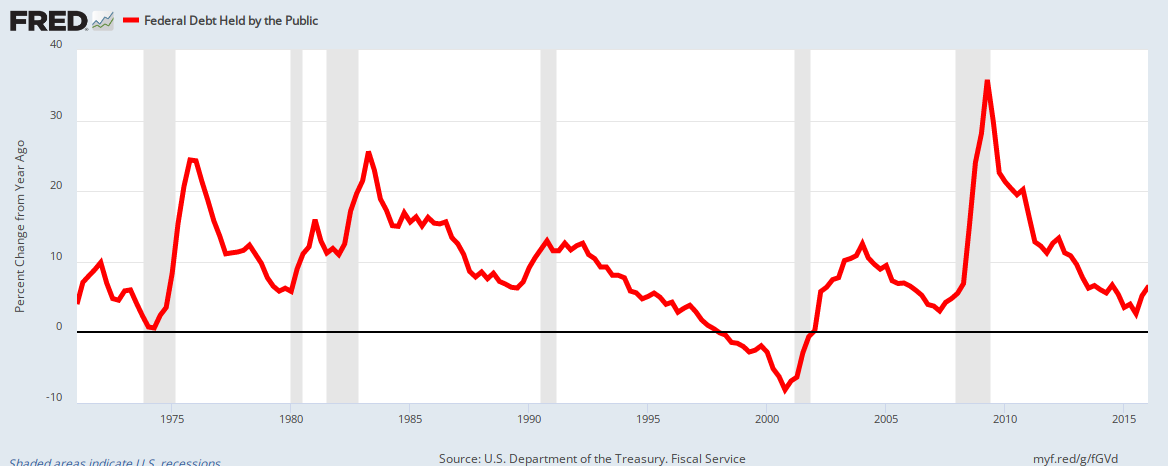

Both measures would add $1.5 trillion over 10 years to the annual budget deficit and the $20 trillion national debt, according to congressional tax analysts.

O.K., immediately you know Trump and the GOP are wrong — for two reasons:

- They are worried about the increase in the economy’s money supply (aka the misnamed “deficit”), the increase that stimulates economic growth

- They are taking advice from the notorious “debt Henny Pennys,“ the CRFB, who have issued the same old warning about the debt “ticking time bomb,” year after year, for more than 35 years. During that period, the federal “debt” has risen an astounding $13 Trillion, from under $1 Trillion to $14 Trillion — and still, we wait for that “time bomb” to explode.

The so-called federal “debt” is the total of deposits in T-security accounts, which are similar to interest-paying savings accounts.

When you deposit your dollars in your bank savings account, they become a debt of your bank.

Your bank owes you the dollars, but does not spend or lend your dollars.

To lend, your bank creates brand new dollars.

Your dollars stay in your account, accumulating interest until you withdraw them. Their only function is to provide legal reserves.

Similarly, when you “lend” to the federal government, you actually make a deposit in your T-security account. The government does not spend or lend your dollars. Your dollars remain in your T-security account, accumulating interest until the government pays it back.

As with a bank savings account, the government does not spend your T-security account dollars. To pay off the “debt,” the government does not use tax dollars. It merely gives you back the dollars that currently exist in your T-security account.

The primary difference between a T-security account and a bank savings account is semantic. We call the former, “debt,” and the latter, “deposits.”

Ironically, we worry about the size of federal “debt” but not the size of bank “deposits,” though the federal government cannot go bankrupt, and banks can.

I know. I know. It makes no sense.

Nearly 10 months into his presidency, with his party in control of the House and the Senate, Trump is still without a major legislative victory.

There are two reasons Trump hasn’t had a victory:

- He can’t comprehend anything much longer than a paragraph. He had no idea what was in the multitude of awful “repeal & replace” Obamacare plans, so he couldn’t give Congress any guidance. Similarly, he has no idea what is in the various tax plans. He only wants to sign something, anything, no matter how terrible, so he can say he did something.

- The voters may be ignorant of the facts, but they are not stupid, and they can see that everything the GOP puts in front of them will take from the 99% and reward the richest 1%.

The Tax Foundation, another nonpartisan group, said the Senate plan would add $1.78 trillion to the deficit over a decade.

Translation: It would add $1.78 million more to the economy over a decade.

It estimated that over the same time frame lower taxes would expand the U.S. economy by 3.7 percent, add 925,000 full-time jobs, raise wages by 2.9 percent and generate enough new tax revenue to erase all but $516 billion of the deficit effect.

Now think very closely about the above two paragraphs. Together they tell you (rightly) that because tax cuts (i.e. deficit increases) will add dollars to the economy, they will grow the economy, add jobs and raise wages.

Those are good things, right? So if deficit spending will accomplish those good things, why is anyone opposed to deficit spending?

Here’s why:

For decades, Republicans positioned themselves as deficit hawks, refusing to raise the debt limit, opposing Democratic spending programs and warning of crushing federal debts being passed on to future generations of Americans.

The deficit Henny Pennys are afraid to admit they have been lying to you and the rest of the voters about the “dangers” of what really benefits you: Federal deficit spending.

Today, they are hung on their own lies, and will try to double-talk you into believing “federal deficits aren’t so bad after all, but anyway, there won’t be deficits” — or something.

In short, they think you’re stupid.

The tax plans now being debated represent a stark reversal, with congressional Republican leadership and tax law writers urging passage of deficit-expanding tax changes. Only a handful of Republican senators already have publicly voiced misgivings.

This is one more demonstration of the Republican Party’s utter bankruptcy. Most of them hate Trump, but are frightened to say it. And most of them know that deficits grow the economy, but are afraid to tell you the truth.

This is disgusting, even for politicians, because their lies directly harm you and the economy.

After the Senate plan was released on Thursday, Republican Senator Jeff Flake said in a statement, “I remain concerned over how the current tax reform proposals will grow the already staggering national debt by opting for short-term fixes, while ignoring long-term problems for taxpayers and the economy.”

Flake repeats the Big Lie that taxpayers will have to pay off the federal “debt” (deposits). They won’t.

Questions:

- Do you consider your bank’s savings account deposits to be “staggering.”

- Do you even know or care what those deposits are?

- Do you think you and your children will have to pay off those deposits?

If your answers rightfully are “No,” “No, and “No,” you similarly should not care about the federal government’s so-called “debt.”

Senator James Lankford said in a statement, “As we work on tax relief, we must also not lose sight of our responsibilities to protect the nation, provide basic government services and confront our federal debt.”

Senator Bob Corker, another Republican and a critic of Trump, did not comment after the Senate bill’s release but signaled fiscal concerns after the House issued its plan, saying he did not want tax cut legislation that added to the deficit.

And then there’s the CRFB, with its usual misstatement:

“The current tax reform debate shows Congress just can’t seem to shake its addiction to debt,” said Maya MacGuineas, president of the Committee for a Responsible Federal Budget.

“If tax cuts paid for by debt are signed into law, Congress will have sent a massive, budget-busting tax bill to our children to pay, and it will result only in a short-term sugar high with little to no economic improvement over the long term,” she said.

May MacGuineas, would you please shut up. Just shut up.

You should be ashamed of yourself. Either you don’t know what you are talking about or, more likely, you have been paid to spread the Big Lie for all these years.

Either way, you will do America a great service if you simply shut up.

I agree with Trump’s and the GOP’s desire to cut taxes, and I agree with the resultant, increased deficit, simply because that would do exactly what The Tax Foundation predicted: Grow the economy, add jobs and raise wages.

What I don’t agree with is the nature of the GOP’s deficits, because as always, they favor the rich, and widen the Gap between the rich and the rest.

Instead, we should increase deficits by instituting The 10 Steps to Prosperity (below).

If Congress and the President merely took Step #1 — eliminate the FICA tax — that alone would go a long way toward growing the economy, adding jobs and raising wages, while narrowing the Gap.

So, enough! Enough with calling deposits in T-security accounts “debt.” Enough with plans that favor the rich and punish the 99%. Enough with widening the Gap between the rich and the rest.

Enough with the Big Lie.

At long last, Congress and the President, forget the political BS and do what you’re paid to do. Do what’s right for the people.

Is that too much to ask?

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………..

The most important problems in economics involve the excessive income/wealth/power Gaps between the have-mores and the have-less.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of The Ten Steps To Prosperity can narrow the Gaps:

Ten Steps To Prosperity:

1. ELIMINATE FICA (Ten Reasons to Eliminate FICA )

Although the article lists 10 reasons to eliminate FICA, there are two fundamental reasons:

*FICA is the most regressive tax in American history, widening the Gap by punishing the low and middle-income groups, while leaving the rich untouched, and

*The federal government, being Monetarily Sovereign, neither needs nor uses FICA to support Social Security and Medicare.

2. FEDERALLY FUNDED MEDICARE — PARTS A, B & D, PLUS LONG TERM CARE — FOR EVERYONE (H.R. 676, Medicare for All )

This article addresses the questions:

*Does the economy benefit when the rich can afford better health care than can the rest of Americans?

*Aside from improved health care, what are the other economic effects of “Medicare for everyone?”

*How much would it cost taxpayers?

*Who opposes it?”

3. PROVIDE A MONTHLY ECONOMIC BONUS TO EVERY MAN, WOMAN AND CHILD IN AMERICA (similar to Social Security for All) (The JG (Jobs Guarantee) vs the GI (Guaranteed Income) vs the EB (Economic Bonus)) Or institute a reverse income tax.

This article is the fifth in a series about direct financial assistance to Americans:

Why Modern Monetary Theory’s Employer of Last Resort is a bad idea. Sunday, Jan 1 2012

MMT’s Job Guarantee (JG) — “Another crazy, rightwing, Austrian nutjob?” Thursday, Jan 12 2012

Why Modern Monetary Theory’s Jobs Guarantee is like the EU’s euro: A beloved solution to the wrong problem. Tuesday, May 29 2012

“You can’t fire me. I’m on JG” Saturday, Jun 2 2012

Economic growth should include the “bottom” 99.9%, not just the .1%, the only question being, how best to accomplish that. Modern Monetary Theory (MMT) favors giving everyone a job. Monetary Sovereignty (MS) favors giving everyone money. The five articles describe the pros and cons of each approach.

4. FREE EDUCATION (INCLUDING POST-GRAD) FOR EVERYONE Five reasons why we should eliminate school loans

Monetarily non-sovereign State and local governments, despite their limited finances, support grades K-12. That level of education may have been sufficient for a largely agrarian economy, but not for our currently more technical economy that demands greater numbers of highly educated workers.

Because state and local funding is so limited, grades K-12 receive short shrift, especially those schools whose populations come from the lowest economic groups. And college is too costly for most families.

An educated populace benefits a nation, and benefitting the nation is the purpose of the federal government, which has the unlimited ability to pay for K-16 and beyond.

5. SALARY FOR ATTENDING SCHOOL

Even were schooling to be completely free, many young people cannot attend, because they and their families cannot afford to support non-workers. In a foundering boat, everyone needs to bail, and no one can take time off for study.

If a young person’s “job” is to learn and be productive, he/she should be paid to do that job, especially since that job is one of America’s most important.

6. ELIMINATE FEDERAL TAXES ON BUSINESS

Businesses are dollar-transferring machines. They transfer dollars from customers to employees, suppliers, shareholders and the federal government (the later having no use for those dollars). Any tax on businesses reduces the amount going to employees, suppliers and shareholders, which diminishes the economy. Ultimately, all business taxes reduce your personal income.

7. INCREASE THE STANDARD INCOME TAX DEDUCTION, ANNUALLY. (Refer to this.) Federal taxes punish taxpayers and harm the economy. The federal government has no need for those punishing and harmful tax dollars. There are several ways to reduce taxes, and we should evaluate and choose the most progressive approaches.

Cutting FICA and business taxes would be a good early step, as both dramatically affect the 99%. Annual increases in the standard income tax deduction, and a reverse income tax also would provide benefits from the bottom up. Both would narrow the Gap.

8. TAX THE VERY RICH (THE “.1%) MORE, WITH HIGHER PROGRESSIVE TAX RATES ON ALL FORMS OF INCOME. (TROPHIC CASCADE)

There was a time when I argued against increasing anyone’s federal taxes. After all, the federal government has no need for tax dollars, and all taxes reduce Gross Domestic Product, thereby negatively affecting the entire economy, including the 99.9%.

But I have come to realize that narrowing the Gap requires trimming the top. It simply would not be possible to provide the 99.9% with enough benefits to narrow the Gap in any meaningful way. Bill Gates reportedly owns $70 billion. To get to that level, he must have been earning $10 billion a year. Pick any acceptable Gap (1000 to 1?), and the lowest paid American would have to receive $10 million a year. Unreasonable.

9. FEDERAL OWNERSHIP OF ALL BANKS (Click The end of private banking and How should America decide “who-gets-money”?)

Banks have created all the dollars that exist. Even dollars created at the direction of the federal government, actually come into being when banks increase the numbers in checking accounts. This gives the banks enormous financial power, and as we all know, power corrupts — especially when multiplied by a profit motive.

Although the federal government also is powerful and corrupted, it does not suffer from a profit motive, the world’s most corrupting influence.

10. INCREASE FEDERAL SPENDING ON THE MYRIAD INITIATIVES THAT BENEFIT AMERICA’S 99.9% (Federal agencies)Browse the agencies. See how many agencies benefit the lower- and middle-income/wealth/ power groups, by adding dollars to the economy and/or by actions more beneficial to the 99.9% than to the .1%.

Save this reference as your primer to current economics. Sadly, much of the material is not being taught in American schools, which is all the more reason for you to use it.

The Ten Steps will grow the economy, and narrow the income/wealth/power Gap between the rich and you.

MONETARY SOVEREIGNTY