Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

Mitchell’s laws:

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money.

•The more federal budgets are cut and taxes increased, the weaker an economy becomes. .

•Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

•The single most important problem in economics is the Gap between rich and poor.

•Austerity is the government’s method for widening the Gap between rich and poor.

•Until the 99% understand the need for federal deficits, the upper 1% will rule.

•Everything in economics devolves to motive, and the motive is the Gap between the rich and the rest..

===================================================================================================================================================================================================================================================================================

The previous post told you of “stinking liars,” those politicians, media and economists who tell you the federal government’s finances are like your finances, and so the government can run short of dollars and needs to eliminate debt, cut spending and increase taxes, i.e invoke austerity upon us.

The purpose of what we term, the Big Lie is to widen the Gap between the very rich and you, mostly by pushing you down.

Wouldn’t you know it, but shortly after we published that post, the right-wing, Chicago Tribune published an editorial filled with the very Big Lies we had just deplored.

It should have been titled, “The Chicago Tribune’s Big Lies,” but instead it was titled:

The next president’s debts

Federal Reserve Board Chairwoman Janet Yellen testifies in front of a monitor counting the current U.S. national debt while appearing at the House Financial Services Committee hearing on the state of the economy July 15, 2015, in Washington.<

Instantly, we are treated to the specter of Janet Yellen sitting in front of a misleading scare-sign, designed to make you worry about the so-called “debt,” when in fact, it shows nothing more than the total of T-security accounts at the Federal Reserve Bank.

Every single one of those dollars is safely ensconced in T-security accounts (similar to your bank savings account). You own some of those dollars, if you own any T-bills, T-bonds, etc.

And the bank owes you those dollars, but you don’t fret about bank “debt,” do you? (And you certainly wouldn’t fret if your bank had the unlimited ability to create dollars.)

You may have your dollars back in an instant, merely by having them transferred from your T-security account to your checking account. No problem at all, and no burden on the federal government or future taxpayers or your grandchildren or anyone else the liars claim will destoy America.

So there was the Chicago Tribune’s first Big Lie, shamefully aided and abetted by the Chairman of the Federal Reserve.

On the mid-July day Jeb Bush candidly told Sioux City Republicans he wants to curb federal favors to Iowa’s ethanol industry, he got a lucky pick-me-up from the non-partisan group, First Budget: How, asked a member of this ascendant advocacy group, would he balance federal revenue and spending?

Who is “First Budget” and why would anyone want to “balance federal revenue and spending”?

Well, “First Budget” has a website that proudly states, “First Budget is a joint nonpartisan initiative of The Concord Coalition and the Campaign to Fix the Debt. Those are two nefarious right-wing, austerity front groups, whose purpose in life is to tell you that federal support of economic growth is bad for you and for your descendants.

“Nonpartisan”? “NON PARTISAN”???

To give you an idea of how shameless the lies are, the Campaign to Fix the Debt was founded by the notorious duo of Erskine Bowles and Sen. Alan Simpson. Remember them? Yes, these are the guys who brought you the sequester, the disastrous debt-cutting program that set back our recovery from the Great Recession by many years. We still haven’t recovered.

And Fix the Debt is bankrolled by the even more notorious Pete Peterson: [ The Campaign to Fix the Debt is the latest incarnation of a decades-long effort by former Nixon man turned Wall Street billionaire Pete Peterson to slash earned benefit programs such as Social Security and Medicare under the guise of fixing the nation’s “debt problem.”]

Bush, who favors raising the age at which Americans can draw Social Security, said he also backs a federal hiring freeze and not replacing all retirees.

“You are not going to get it to balance immediately, but with high (economic) growth and a focused approach to limiting spending, including entitlements over the long haul, you can get it in balance,” Bush said.

“Without (the economy) growing, it won’t happen. And if we don’t fix the entitlement system, it won’t happen.”

What gibberish! Can anyone explain how fewer people receiving Social Security payments, fewer people receiving employment from the federal government, and more people paying more taxes (to achieve “balanced revenue”) will achieve “high economic growth”?

It’s utter nonsense, sort of like scoring fewer runs and giving up more runs, will help the Cubs win more games. What Bush, Bowles, Simpson, Peterson et al propose, is designed to reduce economic growth, and more specifically, to widen the Gap between the rich and the rest.

And as for balancing revenue (taxes) with spending, that would mean no new dollars entering the economy. If anyone can explain how an economy can grow if its money supply doesn’t’ grow, I’d love to hear it. That would be a miracle of economics, indeed.

With that frankness, a candidate for president paid his respects to First Budget’s pressure over the existential threat that federal debts and entitlements pose to America as we know it.

There, in one sentence, the owned-by-the-rich Tribune expresses the Big Lie: The statement that America cannot exist with those big T-security bank accounts, and that rather than stimulating the economy, Social Security and Medicare payments slow the economy.

Never mind that the bought-and-paid-for media have been saying the federal debt is a “ticking time bomb” for at least 75 years. And here we still are. Still ticking.

In the Tribune’s “black is white, and up is down” Big Lie, adding money to the economy shrinks the economy, while austerity grows the economy.

Yeah sure, austerity works. Just ask Greece.

Looming over these dangers is a current federal debt — that is, a federal taxpayers’ debt — of $18.3 trillion.

There’s another Big Lie.

In reality, Not one taxpayer owes one cent of the federal debt, though millions of taxpayers OWN billions of dollars of the federal debt. They own T-security accounts at the Federal Reserve Bank.

And the bigger the misnamed “federal debt,” the more money taxpayers own in T-security accounts. The more proper name would be “T-security deposits” rather than “debt.” Isn’t “deposits” what you call the money you have in bank accounts?

The Tribune article ends with this revealing question, in which the “stinking liars” accidentally admit why the so-called federal “debt” is necessary:

As for candidates always prattling that they want to “invest” more in schools, or defense, or a hundred other needs: At their events or in your talks with their surrogates, ask the questions First Budget volunteers are forcing politicians to confront.

As two of the group’s officers wrote in a July 19 op-ed for The Cedar Rapids Gazette, “If they promise tax cuts or more spending, how will they pay for them without increasing the debt?

Exactly right. You cannot pay for all the benefits the world’s wealthiest Monetarily Sovereign government should provide, without increasing the so-called “debt.”

The rich don’t want you to have those benefits, so they create a straw man: The “unsustainable” debt. It’s a stinking lie but, that’s the whole point, isn’t it?

Rodger Malcolm Mitchell

Monetary Sovereignty

===================================================================================

Ten Steps to Prosperity:

1. Eliminate FICA (Click here)

2. Federally funded Medicare — parts A, B & D plus long term nursing care — for everyone (Click here)

3. Provide an Economic Bonus to every man, woman and child in America, and/or every state a per capita Economic Bonus. (Click here) Or institute a reverse income tax.

4. Free education (including post-grad) for everyone. Click here

5. Salary for attending school (Click here)

6. Eliminate corporate taxes (Click here)

7. Increase the standard income tax deduction annually

8. Tax the very rich (.1%) more, with higher, progressive tax rates on all forms of income. (Click here)

9. Federal ownership of all banks (Click here and here)

10. Increase federal spending on the myriad initiatives that benefit America’s 99% (Click here)

The Ten Steps will add dollars to the economy, stimulate the economy, and narrow the income/wealth/power Gap between the rich and the rest.

——————————————————————————————————————————————

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

![]()

No nation can tax itself into prosperity, nor grow without money growth. Monetary Sovereignty: Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

1. A growing economy requires a growing supply of dollars (GDP=Federal Spending + Non-federal Spending + Net Exports)

2. All deficit spending grows the supply of dollars

3. The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

4. The limit to non-federal deficit spending is the ability to borrow.

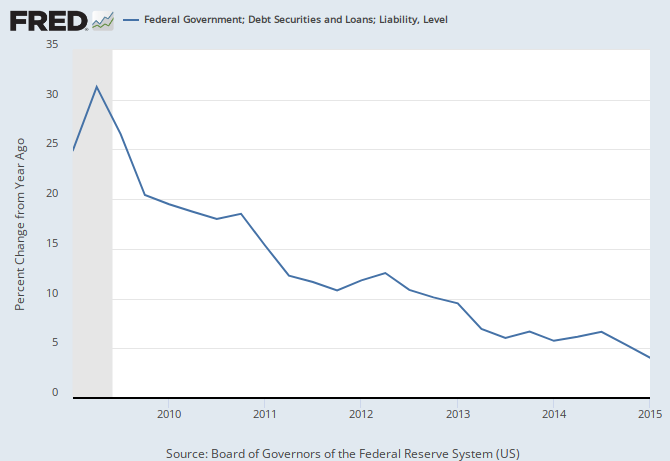

THE RECESSION CLOCK

Vertical gray bars mark recessions.

As the federal deficit growth lines drop, we approach recession, which will be cured only when the growth lines rise. Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

#MONETARYSOVEREIGNTY