The federal government has more than a thousand departments and agencies, including The White House, the House of Representatives, the Senate, the Supreme Court, the Central Intelligence Agency (CIA), Medicare (CMS), and the Social Security Administration (SSA).

Contrary to popular myth, all federal agencies and departments are funded in precisely the same way: Congress votes, and dollars are created from thin air.

A few agencies are associated with so-called “trust funds.” According to the Peter G. Peterson Foundation:

A federal trust fund is an accounting mechanism the federal government uses to track earmarked receipts (money designated for a specific purpose or program) and corresponding expenditures.

The largest and best-known trust funds finance Social Security, portions of Medicare, highways and mass transit, and pensions for government employees.

Federal trust funds bear little resemblance to private-sector counterparts; therefore, the name can be misleading.

A “trust fund” implies a secure source of funding. However, a federal trust fund is simply an accounting mechanism that tracks inflows and outflows for specific programs.

In private-sector trust funds, receipts are deposited, and assets are held and invested by trustees on behalf of the stated beneficiaries.

In federal trust funds, the federal government does not set aside the receipts or invest them in private assets.

Instead, the receipts are recorded as accounting credits in the trust funds and combined with other receipts that the Treasury collects and spends.

Further, the federal government owns the accounts and can, by changing the law, unilaterally alter their purposes and raise or lower collections and expenditures.

Read that last sentence carefully, for it is the heart of this discussion. It consists of three truths:

The federal government owns the accounts

The government can change the law and unilaterally change the purposes of the accounts.

The government unilaterally can raise or lower collections and expenditures.

This all adds up to a powerful but little-understood fact. The so-called federal “trust funds” operate entirely at the whim of Congress and the President.

These “trust funds were created and operated according to the laws the Congress and the President control. By adjusting laws, Congress and the President can determine how much money each “trust fund” collects, has, and spends.

Congress and the President arbitrarily can decide that any trust fund has $1, or $1 trillion, or $1,000 trillion, merely by passing laws. There is no limit to what laws Congress and the President pass, nor what those laws say regarding money in the “trust funds.”

Keep this total control in mind as you read excerpts from this article, also by the Peter G. Peterson Foundation:

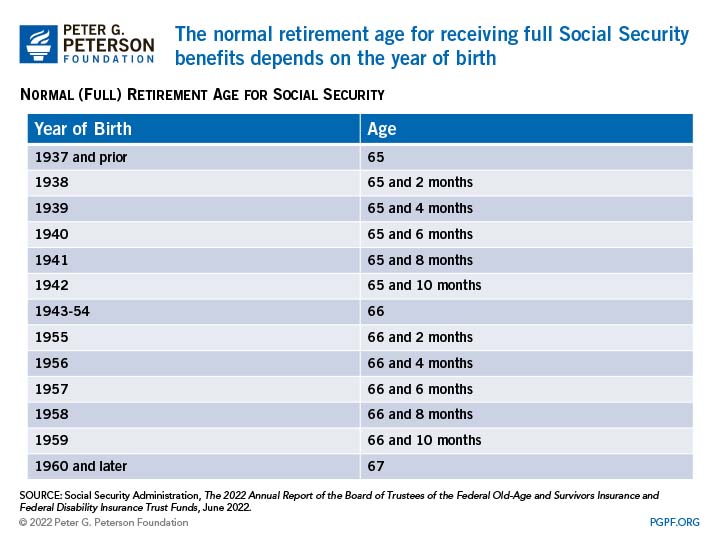

SOCIAL SECURITY REFORM: SHOULD WE RAISE THE RETIREMENT AGE?In their 2022 Annual Report, the Social Security trustees estimate that the program’s primary trust fund — Old Age and Survivors Insurance (OASI) — will spend more on payments to beneficiaries than it collects yearly until it is depleted in 2034.

Driving that impending depletion are the dual demographic trends of retiring baby boomers and lengthening life expectancies, which together have placed considerable strain on Social Security’s finances.

A balanced approach that combined components from each option would likely provide the fairest, most lasting, and least painful adjustment for the future.

Translation: The primary “trust fund” will spend more than it collects –according to current law, which Congress and the President can change at will, but the only law changes being considered are:

Higher taxes

Raising the retirement age, and

Reduced dollar benefits

But here is another, even better approach: Congress and the President should simply vote to give Social Security more money, precisely as they do for the other thousand federal departments and agencies.

There is no need to increase taxes. In fact, FICA should be eliminated. It is unnecessary and a double tax in that it is not deductible, but part of Social Security is taxed. It also punishes lower-income people.

There also is no need to raise the retirement age. Social Security payments can and should be given to every man, woman, and child in America,

Finally, there is no need to reduce dollar benefits. We should even end the faux “trust funds” and simply pay for Social Security the same way the federal government pays for nearly all of its other agencies: By recreating dollars from thin air.

The U.S. federal government is Monetarily Sovereign.It cannot run short of its own sovereign currency.

To pay for your Social Security benefits, the federal government sends instructions (in the form of a wire or check) to your bank or you, instructing your bank to increase the dollar balance in your checking account.

When your bank does as instructed, the balance in your account increases, creating new dollars and adding them to the M2 money supply measure, growing the economy.

Sending instructions to banks is the primary way the federal government creates dollars. The federal government, being Monetarily Sovereign, has the infinite ability to send and clear instructions, thus, the endless ability to create dollars.

(By contrast, everyone who writes a check or sends a wire can sendinstructions but not clear them. Checks that don’t clear are said to “bounce.”)

Your bank then clears the transaction through the Federal Reserve, another federal agency. Thus, the federal government clears its own money-creation transactions, giving it the infinite power to create dollars.

The government also has the infinite power to change Social Security laws, as demonstrated by the 12 benefit changes shown in this chart.

More than half of all Social Security recipients take benefits before the official retirement age when benefits are reduced.

This demonstrates an early need for benefits by those in lower-income groups.

WHAT EFFECT COULD RAISING THE FULL RETIREMENT AGE HAVE ON SOCIAL SECURITY’S LONG-TERM SOLVENCY?Given that more retirees are beginning to collect Social Security benefits earlier in their retirement and that overall life expectancy continues to increase, many policymakers have called for a modification to the program, wherein the full retirement age is gradually raised and ultimately pegged to average life expectancy.

According to an analysis from the Committee for a Responsible Federal Budget (CRFB), gradually increasing the full retirement age by two months per year until it reaches 69 and then indexing it for changes in overall life expectancywould save $90 billion over 10 years,but much more in future decades; CRFB estimates that the change would close over half of the structural mismatch between Social Security’s revenues and spending in the long run.

The above two paragraphs indicate ignorance of the difference between Monetary Sovereignty and monetary non-sovereignty.

If Social Security were private insurance (i.e., monetarily non-sovereign), pegging benefits to life expectancy would be appropriate, even necessary. However, there are zero reasons for the federal government to do this.

There is no fiscal reason why the federal government should try to extract $90 billion from the private sector. If one wishes to grow the U.S. economy, it is the worst possible course of action.

This is what happens when the federal government “closes the mismatch between revenues and spending“(i.e., runs a surplus). Federal surpluses extract dollars from the economy, causing depression or recessions:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Even without surpluses, just reducing federal deficits leads to recessions:

Reduced federal deficits (red line) lead to recessions (vertical gray bars). Recessions are cured by increased federal deficits.

Economic growth requires the federal government to spend more dollars into the economy than it extracts via taxes and fees (i.e., run deficits). Without federal deficits, we have depressions and recessions.

As federal deficits (spending and taxes) increase, the Gross Domestic Product increases—and that includes real (inflation-adjusted) Gross Domestic Product.

Those who argue against federal deficit spending may admit it grows the economy but sometimes claim it causes inflation. However, as the above graph indicates, the economy grows, even when adjusted for inflation.

All evidence indicates that inflation is caused not by federal spending but by scarcities of critical goods and services.

Inflation usually is cured by federal spending to obtain and distribute the scarcities that caused the inflation.

Federal taxes reduce non-federal spending (mostly private sector spending). Thus, no matter how one calculates it, increasing FICA and/or decreasing Social Security benefits will reduce economic growth.

And it’s all unnecessary; the federal government has infinite money. It cannot become insolvent.

Not understanding the differences between a Monetarily Sovereign government and the monetarily non-sovereign state/local governments, businesses and individuals is the single most significant cause of economic misery and self-defeating government spending decisions.

In summary, if the White House, Congress, the Supreme Court, and hundreds of other federal agencies and departments are financially sustainable, so is Social Security and Medicare. There is no need for benefit cuts. There is no need for FICA tax increases. There is no need for FICA at all.

The federal government can provide all its agencies and departments with every dollar they need at the touch of a computer key.

Why Don’t They?

Question: If the government can fund all its agencies and departments without taxes, why doesn’t it just do it?

Answer: The very rich, who run the government, want you to believe the government can’t afford to give you benefits.

“Rich” is a comparative term. A person having $1,000 would be rich if everyone else had only $100. But that person would be poor if everyone else had $10,000.

You can grow richer if the income/wealth/power Gapbelow you widens and the Gap above you narrows. So, one major goal of the rich is to narrow the Gap below them, which requires limiting the benefits you receive from the government.

To keep you from screaming about that, the rich bribe your sources of information — the media, the politicians, and the university economists — to convince you of the Big Liethat federal spending is funded by federal taxes.

It’s a Big Lie because the federal government, being Monetarily Sovereign, creates all the money it uses. The only true purposes of federal taxes are to:

Control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward and

Assure demand for the U.S. dollar by requiring taxes to be paid in dollars.

That’s it. Federal taxes don’t fund anything. In fact, your precious tax dollars are destroyed the moment they are received by the U.S. Treasury.

You pay with dollars that are part of the M2 money-supply measure. When your dollars reach the Treasury, they cease to be part of any money-supply measure and are effectively destroyed. Because the government has the infinite ability to create dollars, there is no point in trying to measure the government’s supply of dollars.

Suppose you are made to believe the federal government is like monetarily non-sovereign state governments, relying on taxes. In that case, you won’t complain when your Social Security, Medicare, poverty aids, college tuition aids, etc. are cut for lack of money.

The less you receive from the government, the richer are the rich. The rich still receive their federal benefits in the form of tax breaks. There never is a complaint about benefits for the rich being “unsustainable,” “unaffordable,” etc. Those terms are reserved for your benefits.

When you read articles telling you the Social Security age requirement must be raised, benefits must be decreased, or the FICA tax must increase, know this: It’s all part of the Big Lie fostered by the rich to make themselves richer.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

In the previous post (“They feed you garbage to improve your health), we addressed some of the usual false claims about the so-called “federal debt.” We showed why “federal debt”:

Isn’t “federal,” and it isn’t “debt.” (It’s non-federal deposits.)

Doesn’t consider the differences between a Monetarily Sovereign government vs. a monetarily non-sovereign government.

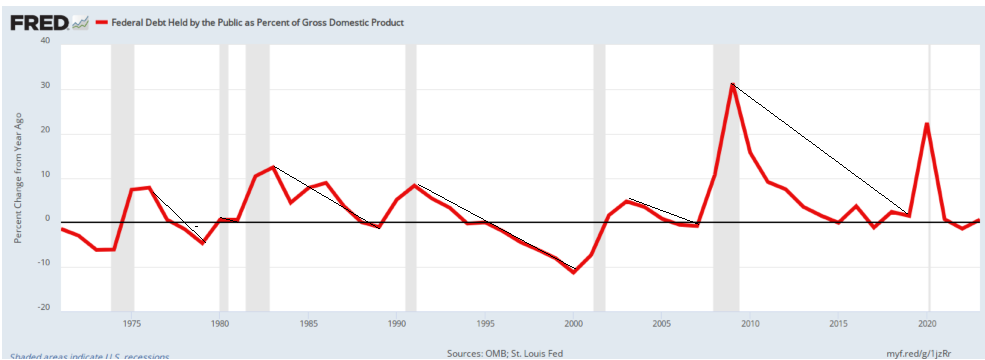

The much-feared Debt/GDP ratio shows a repeated pattern: It declines because debt fear mongers (like J.D. Tuccille) complain about it until it reaches a low point. Then, we have a recession, which is cured by an increase in the ratio, after which the fear-mongers again begin their complaints.

If you are unfamiliar with the above facts, you may wish to read the previous post and rid yourself of the nonsense that J.D. Tuccille spouts in the opening paragraphs of the following article.

J.D. Tuccille

First, his rehash of the old, familiar, wrongheaded, fact-free stuff:

Misery loves company, as they say. But does financial irresponsibility also enjoy spending a little quality time with friends? If so, it’s quite a party.

While the U.S. government is famously running up debt to stratospheric levels, governments worldwide have been spending beyond their means and borrowing to make ends meet.

The likely result: financial markets put at risk by over-extended governments and slow economic growth for pretty much everybody.

“Public debt as a fraction of gross domestic product has increased significantly in recent decades, across advanced, emerging, and middle-income economies,” write Tobias Adrian, Vitor Gaspar, and Pierre-Olivier Gourinchas for the International Monetary Fund (IMF).

“It is expected to reach 120 percent and 80 percent of output respectively by 2028.”

Public debt—money borrowed by governments—has steadily risen, they add, because years of very low interest rates “reduced the pressure for fiscal consolidation and allowed public deficits and public debt to drift upwards.” Then, COVID-19 disrupted the global economy, and governments responded by funding “large emergency support packages” on credit.

Now, with interest rates rising, the cost of servicing debt is going up, too. But governments continue to borrow as if nothing has changed. Of course, riskier governments have to pay higher interest rates.

“On average, African countries pay four times more for borrowing than the United States and eight times more than the wealthiest European economies,” United Nations Secretary-General António Guterres cautioned last summer with the release of A World of Debt: A Growing Burden to Global Prosperity. “A total of 52 countries – almost 40 percent of the developing world – are in serious debt trouble.”

As of 2022, that report revealed, global public debt stood at $92 trillion and rising. Interest payments displaced other expenditures in a growing number of nations, especially developing countries. High public debt crowds out financial room for everything else, including the ability of private parties to borrow to start or expand businesses that create jobs and build wealth.

Then we come to a criticism we didn’t remember to address in the previous post:

Public Debt Crowds Out Private Investment“Households who buy government debt reduce their savings in productive private investments,” Kent Smetters and Marcos Dinerstein wrote in 2021 for the Penn Wharton Budget Model. As the spending is unproductive, the economy is poorer, and total savings are lower due to capital crowding out.”

At first blush, that sounds reasonable. Putting your dollars into a T-security account seems to remove them (temporarily) from the economy.

If you had bought stock or private sector bonds, the dollars would have remained in the economy — except for three facts:

1. You still own those dollars. They are part of your wealth. You can sell them or use them as collateral for loans. Your ownership allows you to borrow more at lower rates than if you didn’t own them. This ability is economically stimulative.

2. They earn net additional dollars in interest. While stock dividends and private-sector bond interest increase your wealth, those dollars come from the private sector.

They do not earn net dollars. They are mere dollar transfers within the private sector. By contrast, federal interest comprises new dollars that add to the private sector’s money supply.

3. That so-called “reduction in savings” is offset by the federal government’s spending into the economy. The dollars you deposit into a T-bill, T-note, or T-bond were derived from the federal government’s deficit spending.

Federal total net deficit spending = Total T-security deposits.

Thus, Tuccille doesn’t realize he is taking both sides of the issue. He dislikes federal deficits, which add dollars to the economy, but criticizes deposits into T-security accounts for taking dollars from the economy.

“Government spending redirects real resources in the economy and can crowd out private capital formation,” they add. “An additional $1 trillion debt this year could decrease GDP by as much as 0.28 percent in 2050.”

How does federal spending crowd out capital formation? Does the government paying your Medical bills crowd out anything? No.

Does paying your Social Security crowd out anything? No.

Does paying private contractors to build a road, bridge, or dam crowd out anything? No.

Does even paying federal employees crowd out anything? No.

Every dollar the federal government spends is a newly created dollar that winds up in the U.S. economy or other nations’ economies. Nothing is crowded out. Capital formation is a result of federal deficit spending.

If you take that insight and apply it to a world of governments on a collective borrowing spree, you end up with a hobbled global economy where prosperity becomes increasingly elusive.

Except for a tiny reality. Prosperity has not become increasingly elusive for the Monetarily Sovereign nations and even for most of the monetarily non-sovereign nations.

The reason: U.S. deficit spending pumps new inflation-adjusted dollars into the world’s economies. We are net importers, meaning we export more dollars than we import.We help the world (and ourselves) become richer.

“Medium-term growth rates are projected to continue declining on the back of mediocre productivity growth, weaker demographics, feeble investment and continued scarring from the pandemic,” note IMF’s Adrian, Gaspar, and Gourinchas.

“Projections for growth five years ahead have fallen to the lowest level in decades.”

First, these are IMF projections, which notoriously are suspect. These folks don’t even say how or whether they include Monetary Sovereignty in their analyses.

Second, it is not reasonable to make a general statement about “medium-term growth rates” without specifying the term and the difference between Monetarily Sovereign nations and monetarily non-sovereign nations.

It is like predicting the growth rate of the world’s children, without specifying their diet and living conditions.

Heavy government borrowing also creates risk for the financial sector by putting banks at the mercy of massive debtors of uncertain creditworthiness.

“The more banks hold of their countries’ sovereign debt, the more exposed their balance sheet is to the sovereign’s fiscal fragility,” note the IMF analysts.

The article supposedly is about U.S. federal debt being too high. But Tuccille drifts off into non-sequiturs.

The U.S. government does not borrow. It creates every dollar it needs ad hoc. This is the process:

1. To pay a bill, the federal government creates instructions (checks, bank wires, currency), not dollars.

2. It sends those instructions (“Pay to the order of . . . ) to each creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

3. At the instant the creditor’s bank does as instructed, dollars are created and added to the M2 money supply measure.

4. The bank then clears its action through the Federal Reserve, a federal agency. One branch of the federal government approves another branch’s instructions.

Thus, in a literal sense, banks create dollars. The notion that banks are “at the mercy of governments” is absolutely true because governments make all the rules by which banks must live.

And yes, banks are at the mercy of a government’s fiscal fragility.

But that begs the question, “Is the U.S. federal government fiscally fragile? The answer is a resounding “No”! (unless Congress, in a moment of MAGA insanity, insists on not paying bills.

Heavily indebted governments also reduce their ability to act as backstops in a financial crisis as they become the likeliest causes of future crises.

As they continue to borrow, they reduce the likelihood that productive private economic activity will grow them out of their financial problems.

Here, Tuccille demonstrates abject ignorance about the difference between Monetary Sovereignty and monetary non-sovereignty. The U.S. federal government is not “heavily indebted” because it could if it chose to, pay all its current and even future bills today.

It simply could send instructions to every creditor’s bank, instructing all those banks to increase the balances in the creditors’ checking accounts. Instantly, all debt, current and future, would disappear.

“Higher government debt implies more state interference in the economy and higher taxes in the future,” The Economist points out in its interactive overview of global government debt.

One would think that a publication titled “The Economist” would understand that while state/local taxes fund state/local spending, federal taxes do not fund federal spending. Even if the federal government didn’t collect a penny in taxes, it could continue spending forever.

The purpose of federal taxes is to:

Control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward, and

Assure demand for the U.S. dollar by requiring the dollar to be used for tax payments.

To make the populace wrongly believe that federal benefits are unaffordable without tax increases, thus reducing the clamor for more benefits.

Also, add the editors, rising debt “creates a recurring popularity test for individual governments,” which often goes poorly regarding fiscal responsibility because paying outstanding bills isn’t popular with voters.

Paying outstand bills isn’t unpopular. It’s collecting taxes that ostensibly are necessary; that’s the unpopular part.

Higher Debt Leads to Lost Prosperity

Well, isn’t that cheerful? It’s also extraordinarily unfortunate. After thousands of years of grindingly slow progress, recent decades saw the human race escaping poverty.

According to the World Bank, even as populations increased, the number of people living below the poverty line, adjusted for inflation, plummeted from 2.01 billion in 1990 to 689 million in 2019.

In 2016, the economist Deirdre N. McCloskey attributed improving prospects for many of the world’s people to “liberalism, in the free-market European sense.”

But that progress reversed in recent years, with poverty blipping back up (712 million people in 2022) amidst slower economic growth and after drastic government interventions during the pandemic.

A future of stumbling economies hobbled by debt-ridden governments that crowd out private investment is one in which more people are poorer than they would have been if the world had stuck with free markets and implemented a modicum of financial responsibility.

Again, Tuccille was supposedly talking about the U.S. government, except he is mixing some monetarily nonsovereign governments into his comments.

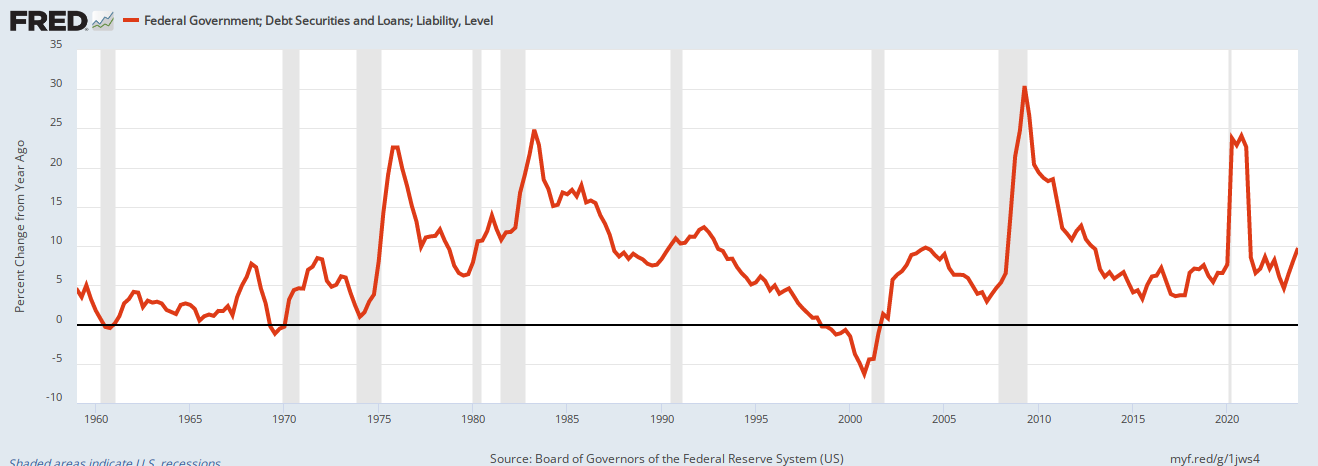

The U.S. “federal debt” has grown from $40 billion in 1940 to $30 trillion in 2024. Where is the crowding out and the poverty he is wringing his hands about? Certainly, not in the U.S., the supposed subject of his article.

I can’t say whether Tuccille is incompetent or dishonest. You decide. Either way, he is wrong, wrong, wrong.

As concerned as the U.N. is about rising public debt, its proposed “solutions” are pretty much what you would expect from that organization. A lot of verbiage about a “more inclusive” system providing “increased liquidity” and “affordable long-term financing” boils down to letting the riskiest governments have a greater say in offering themselves cheap financing. What could possibly go wrong?

The IMF analysts, on the other hand, propose “durable fiscal consolidation” while “financial conditions remain relatively accommodative and labor markets robust.”

I take that as a gentle suggestion that governments need to start paying down their debt to sustainable levels before interest rates and economic conditions deprive them of any options in the matter.

There is only one way for the U.S. government to “pay down its debt.” It has to run surpluses, i.e., to take dollars out of the economy.

That is the worst idea since investing money with Bernie Madoff. Here is what happens every time the federal government pays down its “debt.”

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Recessions (vertical gray bars) are preceded by declines in federal deficits and cured by increases in federal deficits.

It’s not just deficits, but deficit increases that are necessary for economic growth.

Would someone please tell Mr. Tuccille that taking money out of the economy causes recessions if we are lucky and depressions if we aren’t. Remind him that GDP = Federal Spending + Non-federal Spending + Net Exports.

Gentle suggestion or not, governments need to get their fiscal affairs in order before they take us all down with them.

Heavily indebted governments result in burdened economies, leading to a poorer world for everybody.

With its irresponsible borrow-and-spend ways, the U.S. government is, unfortunately, not alone. Most, if not all, world governments are hanging out in very bad company.

Wrong in every regard. Not just wrong but diametrically wrong, pitifully wrong, harmfully wrong.

Is this article about the meaningless Debt/GDP ratio ignorance or malevolence?

I suspect it’s not ignorance. These people should know better. But they keep writing this nonsense. Why?

Bhargavi Sakthivel

I have my suspicions, which I’ll voice later, but first, here are some excerpts from a frightening example.”

A million simulations, one verdict for economy: Debt danger ahead Bhargavi Sakthivel, Maeva Cousin, and David Wilcox, Bloomberg News

In its latest projections, the Congressional Budget Office warned that U.S. federal government debt will increase from 97% of GDP last year to 116% by 2034—higher than in World War II. The actual outlook is likely worse.

“Worse”? Why is an increase in the so-called “federal debt” (that isn’t federal and isn’t debt) bad? When you read the article, you’ll find that they never say. They just assume it.

Rosy assumptions underpin the CBO forecasts released earlier this year, covering everything from tax revenue to defense spending and interest rates. When you factor in the market’s current view on interest rates, the debt-to-GDP ratio rises to 123% in 2034.

Then assume — as most in Washington do — that ex-President Donald Trump’s tax cuts mainly stay in place, increasing the burden.

What “burden”? And on whom is the “burden”? Here are seven reasons why the so-called “federal debt” isn’t federal, isn’t debt, and isn’t a burden on anyone.

1. The federal government is Monetarily Sovereign. It has the infinite ability to pay its bills. Even if the government owed the “federal debt,” it instantly could create the dollars to pay it off.

Statement from the St. Louis Fed:“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes:

Scott Pelley: “Is that tax money the Fed is spending?”

Ben Bernanke: “It’s not tax money… We simply use the computer to mark up the size of the account.”

2. The so-called “federal” debt isn’t federal. It is the total of deposits into Treasury Security accounts, the contents of which are wholly owned by the depositors.

The federal government doesn’t use those deposits for spending. They sit in the account, earning interest, until maturity, when the government transfers them to the owners’ checking accounts.

Because the government doesn’t take ownership of the dollars, the government doesn’t owe the dollars.

These accounts resemble bank safe deposit boxes where the contents are not bank debt. They are merely held for safekeeping. Thus, as with safe deposit boxes, the contents of T-security accounts are neither federal nor debt.

Even if the “debt” (deposits) were trillions of dollars, that would mean trillions were sitting in Treasury Security accounts, waiting to be returned, which could be accomplished by the touch of a computer key.

3. The debt does not burden the government (it has the infinite ability to pay) or taxpayers (who are never asked to pay for those deposits).

4. The deposits have nothing to do with Gross Domestic Product (GDP), a federal plus non-federal spending measure. Even if the “Debt”/GDP ratio were 100, 1000, or 10,000, this would have nothing to do with the government’s ability to return the dollars in T-Security accounts.

If you go to the Debt/GDP ratio by country, you will see a long list of nations and their Debt/GDP ratios. Examine those ratios; you cannot tell anything about the nations’ finances.

The ratio says nothing about a nation’s ability to pay what it owes, its economic safety, or its money. It tells you nothing about the past, the present, or the future. It is a classic Apples/Audis comparison, signifying nothing.

Sadly, even that country comparison website falsely states, “(The ratio) typically determines the stability and health of a nation’s economy and offers an at-a-glance estimate of a country’s ability to pay back its current debts.”

Wrong. The ratio does neither of those things.

For a Monetarily Sovereign nation like the U.S., UK, Canada, China, Japan, et al., the ratio says nothing about the stability and health of a nation’s economy or its ability to pay its current debt. Whether federal “Debt” (that isn’t debt) grows faster or slower than GDP means nothing.

With uncertainty about so many variables, Bloomberg Economics has run a million simulations to assess the fragility of the debt outlook. In 88% of the simulations, the results show the debt-to-GDP ratio is unsustainable — defined as an increase over the next decade.

A normal human being would define “unsustainable” as something that cannot be continued. Apparently, Bloomberg describes it as an increase.

“Unsustainable” is a favorite word for “debt” fear-mongers because it absolves them of the requirement to explain what cannot be sustained.

The U.S. federal debt has increased from about $40 billion in 1940 to about $30 trillion this year (an astounding 75,000% increase), and fear-mongers have told you it’s a “ticking time bomb.”

It has been ticking for 84 years, and still no problems. The prognosticators seem not to learn from failure.

The Biden administration says its budget, which includes a series of tax hikes on corporations and wealthy Americans, will ensure fiscal sustainability and manageable debt-servicing costs.

Our Monetarily Sovereign government has infinite fiscal sustainability and can manage any debt-serving costs. In fact, the more interest the federal government pays, the more GDP increases.

GDP=Federal Spending + Nonfederal Spending + Net Exports.

Economic growth benefits from federal interest payments.

“I believe we need to reduce deficits and stay on a fiscally sustainable path,” Treasury Secretary Janet Yellen told lawmakers in February. Biden administration proposals offer “substantial deficit reduction that would continue to hold interest expense at comfortable levels.

But we would need to work together to achieve those savings,” she said.

I do not know why Janet Yellen would promulgate such ignorance or lies. The U.S. has infinite fiscal sustainability and can comfortably pay any interest.

Alan Greenspan: “A government cannot become insolvent concerning obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

The trouble is that delivering such a plan will require action from a Congress that’s bitterly divided on partisan lines.

Republicans, who control the House, want deep spending cuts to bring down the ballooning deficit without specifying precisely what they’d slash.

Democrats, who oversee the Senate, argue that spending contributes less to debt sustainability deterioration, with interest rates and tax revenues being the key factors.

To paraphrase the old saying, “There are lies, damned lies, and claims about the federal debt.”

Here is what deep spending cuts accomplish:

U.S. depressions to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began in 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began in 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began in 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began in 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began in 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began in 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began in 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Here is what deficit cuts accomplish:

When deficits (red line) decline, we have recessions (vertical gray bars), which are cured by increased federal deficit spending.

Federal surpluses take dollars from the economy. Federal deficits add dollars to the economy. You can review the formula for GDP to see why the above effects occur.

Neither party favors squeezing the benefits provided by significant entitlement programs.

The public understands that federal spending helps the economy. One wonders why the “experts” don’t.

Ultimately, it may take a crisis — perhaps a disorderly rout in the Treasuries market triggered by sovereign U.S. credit-rating downgrades or a panic over the depletion of the Medicare or Social Security trust funds — to force action.

That’s playing with fire.

The credit-rating agencies have downgraded the U.S. credit, not because of high debt but because Congress threatened not to pay its bills with that ridiculous, useless “debt ceiling.”

Congress always has the ability to pay its bills by creating dollars ad hoc. However, credit ratings will fall unnecessarily when Congress threatens creditors due to ignorance or political malevolence.

Last summer provided a miniature foretaste of how a crisis might begin. Over two days in August, a Fitch Ratings downgrade of the U.S. credit rating and an increase of long-term Treasury debt issuance focused investor attention on the risks.

Benchmark 10-year yields climbed by a percentage point, hitting 5% in October — the highest level in over a decade.

The federal government had no trouble pressing those computer keys that paid the interest.

Further, the government didn’t need to pay higher interest; it set the bottom interest rate, and if there was no threat to paying, that will be the rate.

For years following the “Great Recession of 2008, federal deficits increased massively, and interest rates stayed near zero. The government and Federal Reserve have the tools to control spending and interest rates.

The Federal Reserve sets interest rates to control inflation, not to help the government pay interest.

Shaking investor confidence in U.S. Treasury debt as the ultimate safe asset would take a lot.

If it evaporated, though, the erosion of the dollar’s standing would be a watershed moment, with the U.S. losing access to cheap financing and global power and prestige.

Yes, “it would take a lot” — a lot more than deficit spending, which, though massive, has not caused the “unsustainability” that the Henny Pennys fret about.

By law, the CBO is compelled to rely on existing legislation. That means it assumes the 2017 Trump tax cuts will expire in 2025. However, even President Joe Biden wants some of them extended.

According to the Penn Wharton Budget Model, permanently extending the legislation’s revenue provisions would cost about 1.2% of GDP each year starting in the late 2020s.

Hmmm. Extending tax cuts (which allows the private sector to spend more money) would cost 1.2% of GDP each year—strange mathematics.

The CBO also must assume that discretionary spending, which Congress sets each year, will increase with inflation rather than keep pace with GDP.

What?? Discretionary spending will increase with inflation but not keep pace with GDP. If I read that correctly, the author warns that GDP will grow faster than inflation. And that’s a bad thing??

Market participants aren’t buying the benign rates outlook, with forward markets pointing to borrowing costs markedly higher than the CBO assumes.

Borrowing costs are determined by the Fed, which (wrongly) believes raising interest rates (which increases the prices of everything you buy) is a good way to fight inflation! If you can figure that one out, let me know. I can’t.

Bloomberg Economics has built a forecast model using market pricing for future interest rates and data on the maturity profile of bonds. Keeping all the CBO’s other assumptions in place shows debt equaling 123% of GDP for 2034.

Which is meaningless.

Debt at that level would mean servicing costs reach close to 5.4% of GDP — more than 1.5 times as much as the federal government spent on national defense in 2023, comparable to the entire Social Security budget.

All it means is that our Monetarily Sovereign government will create more growth dollars and add them to GDP. Is that supposed to be a problem? Mathematically, increases in federal spending increase economic growth.

Heavyweights from across the political spectrum agree the long-term outlook is unsettling.

Fed Chair Jerome Powell said earlier this year that it was “probably time—or past time” for politicians to start addressing the “unsustainable” path of borrowing.

The federal government does not borrow. T-bills, T-notes, and T-bonds do not represent borrowing. They represent deposits into Treasury Security accounts — money the federal government neither needs nor touches.

The purpose of those accounts is not to provide spending money to a Monetarily Sovereign government but to provide a safe place to store unused dollars. This stabilizes the dollar.

Former Treasury Secretary Robert Rubin said in January that the nation is in a “terrible place” regarding deficits.

From the realm of finance, Citadel founder Ken Griffin told investors in a letter to the hedge fund’s investors Monday that the U.S. national debt is a “growing concern that cannot be overlooked.”

Days earlier, BlackRock Inc. Chief Executive Officer Larry Fink said the U.S. public debt situation “is more urgent than I can ever remember.”

Ex-IMF chief economist Kenneth Rogoff says while an exact “upper limit” for debt is unknowable, challenges will arise as the level keeps going up.

Rogoff’s broader point is well taken: forecasts are uncertain. To mitigate this uncertainty, Bloomberg Economics has run a million simulations on the CBO’s baseline view—an approach economists call stochastic debt sustainability analysis.

Ooooh! “Stochastic sustainability analysis.” And they did it a million times. How many of those times included the fact that the Monetarily Sovereign U.S. government never can run short of dollars to pay its bills and interest? Not yesterday, not today, not tomorrow, not ever?

“stochastic” means: “Having a random probability distribution or pattern that may be analyzed statistically but may not be predicted precisely.”

Each simulation forecasts the debt-to-GDP ratio with a different combination of GDP growth, inflation, budget deficits, and interest rates, with variations based on patterns seen in the historical data.

In the worst 5% of outcomes, the debt-to-GDP ratio ends in 2034 above 139%, which means the U.S. would have a higher debt ratio in 2034 than crisis-prone Italy did last year.

But the ratio means nothing. It tells you nothing about “sustainability.”

More importantly, the proof of abject ignorance comes with those last few words: “crisis-prone Italy.”

OMG. They are too ignorant to understand the differences between a Monetarily Sovereign entity and a monetarily non-sovereign entity.

Italy is monetarily non-sovereign. It can run short of euros. The U.S. is Monetarily Sovereign. It cannot run short of dollars (unless Congress continues with the foolish debt-limit nonsense.)

It’s like claiming that birds can’t fly because elephants can’t fly.

The Treasury chief herself acknowledged in a Feb. 8 hearing that “in an extreme case,” there could be a possibility of borrowing reaching levels that buyers wouldn’t be willing to purchase everything the government sought to sell. She added that she saw no signs of that now.

I assume she’s talking about buyers of T-securities. Surely she knows that:

The federal government doesn’t need to sell T-securities. They don’t provide the government, as a dollar creator, with anything. They provide dollar users with safe storage.

If the government had a yen to sell more T-securities, it could always raise interest rates.

Getting to a sustainable path will require action from Congress. Precedent isn’t promising. Disagreements over government spending came to a head last summer when a standoff over the debt ceiling brought the U.S. to the brink of default.

The deal to halt the havoc suspended the debt ceiling until Jan. 1, 2025, postponing another clash over borrowing until after the presidential election.

This is what ignorance causes. It is an unnecessary battle over a meaningless number to reach a fruitless conclusion. And these are the geniuses we elect to Congress.

It’s hard to imagine a U.S. debt crisis. The dollar remains the global reserve currency. The annual and unseemly spectacle of government shutdown brinksmanship typically leaves barely a ripple on the Treasury market.

A fictional “debt crisis” (the U.S. federal government unable to create dollars?) has nothing to do with the dollar being the leading “reserve currency.” A reserve currency is just money banks keep in reserve to facilitate international trade.

Though the U.S. dollar is a leader, other currencies are reserve currencies, depending on geography: The euro, the Canadian dollar, the Mexican peso, China, Japan, Australia, etc. all produce currencies that banks keep in reserve.

There is no magic in being a reserve currency. And it does nothing to prevent a “debt crisis.

Still, the world is changing. China and other emerging markets are eroding the dollar’s role in trade invoicing, cross-border financing, and foreign exchange reserves.

This has nothing to do with any “debt crisis” or the Debt/GDP ratio.

Foreign buyers make up a steadily shrinking share of the U.S. Treasuries market, testing domestic buyers’ appetite for ever-increasing volumes of federal debt.

It’s not federal; it’s not debt, and it’s not a problem.

And while demand for those securities has lately been supported by expectations for the Fed to lower interest rates, that dynamic won’t always be in play.

The federal government doesn’t need to issue T-securities. It creates all its dollars by spending them. The spending comes first, and then it creates dollars.

Herbert Stein, head of the Council of Economic Advisers in the 1970s, observed that “if something cannot go on forever, it will stop.” If the U.S. doesn’t get its fiscal house in order, a future U.S. president will confirm the truth of that maxim. And if confidence in the world’s safest asset evaporates, everyone will suffer the consequences.

Given that the U.S. government has the infinite ability to create dollars, the endless ability to pay interest, the limitless ability to control interest rates paid by Treasuries, and the infinite ability to pay for anything, anytime, that sounds like the fiscal house is in good order.

Because the debt-GDP ratio is meaningless, the following paragraphs are purely for entertainment purposes and should not be taken seriously.

I have bolded the more humorous parts:

MethodologyBloomberg Economics uses the latest long-term CBO projections’ baseline fiscal and economic outlook—including the effective interest rate, primary budget balance as a percent of GDP, inflation as measured by the GDP deflator, and real GDP growth rate—as a starting point for the analysis.To calculate the debt-to-GDP ratio using market forecasts for rates, we substitute forward rates as of March 25, 2024, and project future effective rates on federal debt based on a detailed bond-by-bond analysis.To forecast the distribution of probabilities around the CBO’s baseline debt-to-GDP view, we conduct a stochastic debt-sustainability analysis:—We estimate a VAR model of short- and long-term interest rates, primary balance-to-GDP ratio, real GDP growth rate, and GDP deflator growth using annual data from 1990 to 2023. The covariance matrix of the estimated residuals is then used to draw one million sequences of shocks.—We use data on the maturities of individual bonds to map short- and long-term interest-rate shocks to the effective interest rate paid on U.S. federal debt.—Using this model, Bloomberg Economics considers two definitions of sustainability. First, we check if the debt-to-GDP ratio increases from 2024 to 2034. Second, we examine if the average inflation-adjusted interest expense, scaled by nominal GDP, over the ten years from 2025-2034 is less than 2%.———(With assistance from Jamie Rush, Phil Kuntz, and Viktoria Dendrinou.)

Jamie, Phil, and Viktoria have invented two definitions of “sustainability.” One is debt/GDP increases, which have been going on for over 80 years and have caused nothing. The other is interest expense, which the government has the endless ability to pay, is controlled by the Fed, and adds to GDP growth.

Apparently, Jamie, Phil, and Viktoria don’t know we’ve passed those road signs, but we are still sustaining.

Folks, you have been fed a steady, 80+ years diet of garbage, the purpose being to convince you the government can’t afford to give you benefits. The rich know better, so they get all the tax benefits.

The media are bribed to feed you garbage by advertising dollars and ownership.

The economists are bribed via contributions to schools and promises of lucrative employment in think tanks.

The politicians are bribed by campaign contributions and employment after they leave office.

Sadly, the public eats the garbage, so the people struggle while the rich laugh. Ignorance is costly.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People..

I long have favored a federal plan in which every man, woman, and child in America would receive a monthly stipend from the federal government. (Some call it UBI—Universal Basic Income. Others call it GI—Guaranteed Income, or Social Security for All.)

A federally funded Social Security for All program was described in a post published seven years ago.

Today, that post was brought to mind by the following article:

An Illinois Senate appropriations committee would review “the landscape of cash supports available to low-income residents” and identify “populations without significant access to cash supports.”

The bill, as filed, says after the board is dissolved at the end of 2027, DHS would administer the program with monthly cash payments of $1,000 to Illinois residents, regardless of immigration status, who provide care for a child or specified dependent, recently gave birth or adopted a child or is enrolled in an educational or vocational program.

By law, the Monetarily Sovereign U.S. government is an infinite horn of plenty, capable of creating an unending stream of dollars at the touch of a computer key without collecting a penny in taxes.

Mike Buehler, an opponent of the measure, said it’s irresponsible to discuss such a program without knowing how much it will cost taxpayers.

You may be surprised that I oppose this and other similar plans.

Here is why:

1. Localgovernments are monetarily non-sovereign (unlike the federal government, which being Monetarily Sovereign, has the infinite ability to create dollars).

With few exceptions, local governments get their spending money from taxpayers.

That is why it can run trillion-dollar deficits with no funding problem at all.

State, county, or city taxpayers pay for local government-funded UBI programs.

Most local tax dollars come from sales taxes and/or local income taxes, most of which are paid by middle—and lower-income residents. Extracting dollars from middle—and lower-income taxpayers is exactly the opposite of the UBI plan’s basic purpose.

2. While the federal government has unlimited access to dollars,local governments have limited abilities to pay for things. So, the benefits must be limited to local governments’ affordability estimates.

This, in turn, requires limiting benefits to specific groups and denying benefits to other groups, which creates two problems:

A. The government must set up a complex and expensive apparatus for monitoring recipients so that people do not cheat.

B. People just outside the limit of qualifications are unjustly deprived of aid, and/or try to find unanticipated ways to qualify.

“I understand that you would have to be a person with a child, or caring for someone in your home or school to be eligible for the benefits.

A local government would have to hire dozens (or thousands?) of people to monitor these qualifications. (Do you have a child? How old? Are you really “caring for” that boarder? Are you still in school, and exactly what is a “school.” How many days or hours do you attend?

Additionally, there would be extensive and expensive paperwork filed, read, and authenticated.

That could be millions of people and the cost could be in the tens of billions of dollars,” Buehler told The Center Square. “And where’s the state going to come up with these funds and the only place to come up with that is to get it from the taxpayers.”

Guaranteed income programs in Chicago and the Metro East St. Louis areas are ongoing, costing taxpayers millions. In 2022, the city of Chicago was in line to spend $31.5 million for $500 a month to go to 5,000 low-income residents.

That same year, Illinois legislators approved a pilot program using state taxpayer fundsworth $3.6 million for the Metro East St. Louis area.

Inevitably, a state-run, money-restricted program would evolve to a “nanny-state,” where the money only could be used for approved purposes. And that would have to be monitored.

Ameya Pawar with the Economic Security Project said there are 150 different programs across the country. He gave examples of people using the money to buy sports goods for their children or even to take a vacation.

There is widespread belief that the poor who receive money from taxpayers, should be told what to do with the money (the poor supposedly being too ignorant to know what is best for them). Buying sports goods and taking vacations is not “good” for the poor.

The nanny preference is only to feedstarving children, not just make them happy with toys and entertainment. Note the hinted outrage Ameya Pewar expresses for recipients buying baseballs to entertain their kids.

“And all of this money that goes into the pockets to stabilize households flows through local businesses,” Pawar told the committee. “So you see some of this money back in sales taxes, and other taxes.”

No buying from Amazon allowed??

Buehler said there could be unintended consequences, like reducing work productivity and more.

“For regardless of immigration status, I think an unintended consequence could be a flood of migrants coming to Illinois looking for benefits and not having to work for it,” he said.

3. If one state, county, city, or village offers better benefits than another, people will tend to go where the money is and the taxpayers will pay. This is true for citizens as well as migrants.

And note the common but false belief that the poor are so lazy and unmotivated, if you give them money, they won’t get jobs.

Pawar said the proposed statewide guaranteed program of “unrestricted cash” should be in addition to other taxpayer-funded safety net programs.

Programs like Supplemental Nutrition Assistance Program funds go to buy food. The Low Income Housing Energy Assistance Program is for heating bills. The Temporary Assistance for Needy Families program provides monthly cash assistance to low-income families with children.

“And to get this income, they may not necessarily spend that in their own best interest or the interest of the citizens at large,” he said.

Again, the taxpayer requirement exacerbated the nanny-state belief that the poor are too stupid to spend in their own best interests. “Why am I, as a taxpayer helping these people to take vacations, if I can’t afford one myself.”

All the above-mentioned problems would be addressed by a federally-funded, Social Security program covering every man, woman, and child in America, regardless of income or wealth.

The rich, poor, citizens, non-citizens, young, old, married, single, renter, homeowner, in or out of school, etc., all would receive the stated benefits — and unlike with state and local government programs, no one would pay a penny.

Federal Social Security payments made to every man, woman, and child, require much less monitoring. Most importantly, affordability would cease to be an issue. The federal government can afford anything, and without collecting taxes.

All of the money spent by the federal government would be addedto the local economy, increasing everyone’s income.

8 Million Have Slipped Into Poverty Since May as Federal Aid Has Dried Up, October 15, 2020. (By Leigh Lynes: New studies show the effect of the emergency $2 trillion package known as the Cares Act and what happened when the money ran out.)

Here are excerpts from another article on the subject.

Actually, there are “strings,” in the form of qualifications.

More than interest — when former US presidential candidate Andrew Yang announced that a UBI program of $1,000 direct payments to citizens every month would be the keystone policy of his platform, he drew an unexpected amount of grassroots support in a crowded primary year.

Guaranteed income programs have been gaining even more traction during the pandemic, which took a particular toll on low-wage workers and threw many Americans into poverty.

At least 11 direct-cash experiments went into effect this year, Bloomberg estimated in January.

Former Stockton, California mayor Michael Tubbs, took the idea to the next level by launching the Mayors for a Guaranteed Income network. As of this year, there are 60 mayors in the program, advocating — and launching pilot programs for — guaranteed income for their residents.

California recently launched the first statewide guaranteed income program in the US, providing up to $1000 per month to qualifying pregnant people and young adults leaving the foster care system.

“Young adults leaving foster care” and “pregnant people” comprise two, very narrow classes, and $1000 a month is a meager amount. The task of verifying qualifications would be costly. (Imagine trying to verify pregnancy for thousands of people, and who monitors when pregnancies end before birth?)

The basic income program that Tubbs launched in Stockton in 2019, the Stockton Economic Empowerment Demonstration, has been considered the model for other cities that have followed in its footsteps, offering low-income residents hundreds of dollars a month and measuring their job prospects, financial stability, and overall well-being afterward.

It seems like a massive and expensive project for just hundreds of dollars’ worth of benefits.

According to SEED, participants improved in all those metrics.

“Guaranteed income makes a case for investing in our undocumented neighbors and formerly incarcerated residents. In doing so, it addresses the reality of the nation’s fragmented, punitive welfare structure.”

Will taxpayers consider this a reward for being undocumented or incarcerated? (Want to make an easy few hundred dollars a month? Go to jail for some minor charge.)

This kind of program isn’t a new idea, however. The Eastern Band of Cherokee Indians Casino Dividend in North Carolina has been giving tribal members annual funds since 1997, for instance. Alaska has been paying residents out of its oil dividends since 1982.

The Eastern Band of Cherokee Indians Casino Dividend in North Carolina gets its money from casino revenue. Alaska gets its dividend money from oil. Neither collects taxes to pay recipients. That is a major consideration.

Here are a few of the 33 examples mentioned in the above article.

Compton, California. Duration: December 2020 to December 2022. Income amount: $1,800 every three months for 2 years. Number of participants: 800

Tacoma, Washington,Duration: December 2021 to December 2o22, Income amount: $500 every month for 1 year, Number of participants: 110

Stockton, California, Duration: February 2019 to February 2021, Income amount: $500 every month for 2 years, Number of participants: 1ount: Based on the annual dividend from state-owned oil companies, ranged from roughly $2,000 per person in 2015 to $800 in years with lower gas prices.

Oakland Resilient Families,Duration: Summer 2020 to present, Income amount: $500 per month for 18 months, Number of participants: 600

Alaska Permanent Fund , Duration: Annual, Income amount: Based on the annual dividend from state-owned oil companies, ranged from roughly $2,000 per person in 2015 to $800 in years with lower gas prices , Number of participants: Alaska residents

North Carolina, Cherokee Tribe, The Eastern Band of Cherokee Indians Casino Dividend pays every tribe member annually, Duration: Annual, Income amount: $4,000 – $6,000 per year, Number of participants: Every tribal member.

The Alaska and Cherokee programs succeed long term because they are not funded by taxpayers. A federally funded program would succeed for the same reason. Federal spending is not taxpayer funded.When state and local taxpayers fund a spending program, the result is that a large group of middle- and low-income people transfers some of their money to a smaller group of middle- and low-income people.

The large group includes all those who pay sales and income taxes. The small group is all those who receive those tax dollars. It’s just dollars rotating within the municipality, enriching some residents at the expense of others. The municipality’s economy receives nothing.

By contrast, when the federal government funds a guaranteed income program the government creates new dollars and sends them to the nation’s recipients. The result is that there is no expense to anyone, but the nation’s economy is enriched with net dollars. (GDP = Federal Spending + Nonfederal Spending + Net Exports).

Guaranteed income programs help narrow the income/wealth/power Gap between the rich and the poorer. While reducing poverty, in of itself, is a worthwhile goal, narrowing the Gap also helps address related, social problems:

Wide Gaps affect not only poverty itself, but health and longevity, education, housing, law and crime, war, ownership, bigotry, taxation, GDP, scientific advancement, the environment, human motivation and well-being, and virtually every other issue related to economics.

The most successful guaranteed income programs share several features:

Funded by a Monetarily Sovereign government or by state owned and controlled businesses. This takes taxpayer costs out of the equation.

Minimal requirements for participants achieve voter support by making the plan fairer.

Significant benefits. Trivial payments, i.e. $100 a month, etc. will not generate positive voter sentiment.

Easy entry and supervision. Difficult entry results in negative feelings by voters. Easy supervision lowers costs.

Easily understood goal.

Many good reasons for, and no good reasons why not.

A national Social Security for All plan, with a minimum benefit if $5,000 per year for each adult (18 and over) and $2,500 a year for a child would begin to address the abovementioned social problems.

The Cost:

The U.S. has about 260 million adults (18+) and about 70 million children.

At the $5,000/2,500 level, the benefit cost of the Social Security for All would be $1.3 trillion for adults and $175 billion for children, totaling somewhat south of only $1.5 trillion.

Why do I say “only”? By comparison:

In 2023, the federal government spent about $6.2 trillion.

The Gross Domestic Product (GDP) for the year 2023 had a current-dollar value of $27.36 trillion.

In 2023, the U.S. federal government collected a total of approximately $4.71 trillion in tax revenue.

In fiscal year 2023, the federal government’s spending exceeded its revenues, resulting in a deficit of $1.70 trillion

By the end of 2023, the cumulative federal deficit was $26.236 trillion.

The U.S. M2 money supply is about $20 trillion.

Given that:

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

and

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

A Monetarily Sovereign government spending $1.7 trillion to send an additional $5,000 to every adult and $2,500 to every child — and at no cost to anyone — would seem to be a bargain price and a great investment for America.

Further, because of the multiplier effect*, that additional $1.7 trillion in federal spending, would increase Gross Domestic Product far more than $1.7 trillion.

*Per Investopedia:A government increases spending or decreases taxes in part to inject more money into the system.

Such fiscal policy has a multiplier effect. That is, every dollar spent can be expected to cause an increase in the gross domestic product (GDP) by more than a dollar.

This is due to the sheer momentum created by the policy. Consumers spend more so businesses produce more goods.

Businesses have to hire more to produce more goods, so more people have more money to spend on goods.

The same phenomenon occurs for both government spending increases and tax cuts. Either tends to increase GDP disproportionately.

A cut in government spending can reduce GDP by a greater degree than the amount saved by the cut.

The expanded Child Tax Credit had a multiplier effect of 1.25 on GDP in the first quarter of 2021, according to an analysis by Moody’s Analytics. The increase in the Supplemental Nutrition Assistance Program boosted GDP by a 1.61 multiplier effect in the same period. Increased defense spending had a 1.24 multiplier effect.

Infinite benefits at no cost to anyone: Can any knowledgeable person object to Social Security for All?

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

The U.S. federal government is Monetarily Sovereign. It cannot run short of its own sovereign currency.

To pay for your Social Security benefits, the federal government sends instructions (in the form of a wire or check) to your bank or you, instructing your bank to increase the dollar balance in your checking account.

When your bank does as instructed, the balance in your account increases, creating new dollars and adding them to the M2 money supply measure, growing the economy.

Sending instructions to banks is the primary way the federal government creates dollars. The federal government, being Monetarily Sovereign, has the infinite ability to send and clear instructions, thus, the endless ability to create dollars.

(By contrast, everyone who writes a check or sends a wire can send instructions but not clear them. Checks that don’t clear are said to “bounce.”)

Your bank then clears the transaction through the Federal Reserve, another federal agency. Thus, the federal government clears its own money-creation transactions, giving it the infinite power to create dollars.

The U.S. federal government is Monetarily Sovereign. It cannot run short of its own sovereign currency.

To pay for your Social Security benefits, the federal government sends instructions (in the form of a wire or check) to your bank or you, instructing your bank to increase the dollar balance in your checking account.

When your bank does as instructed, the balance in your account increases, creating new dollars and adding them to the M2 money supply measure, growing the economy.

Sending instructions to banks is the primary way the federal government creates dollars. The federal government, being Monetarily Sovereign, has the infinite ability to send and clear instructions, thus, the endless ability to create dollars.

(By contrast, everyone who writes a check or sends a wire can send instructions but not clear them. Checks that don’t clear are said to “bounce.”)

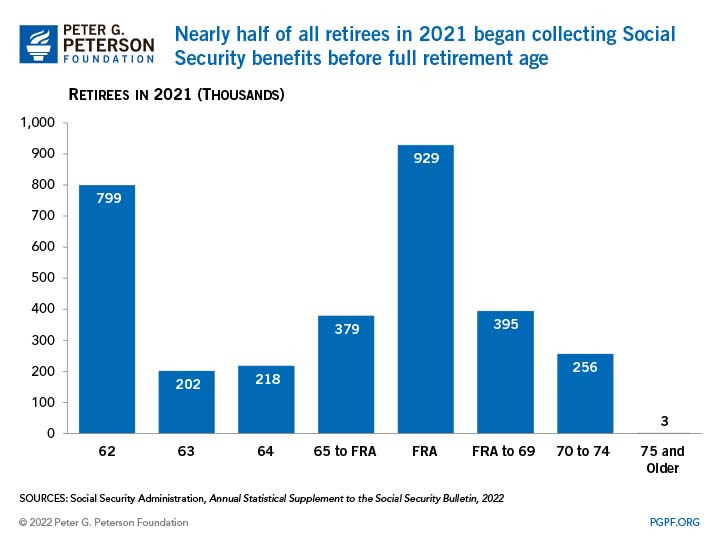

Your bank then clears the transaction through the Federal Reserve, another federal agency. Thus, the federal government clears its own money-creation transactions, giving it the infinite power to create dollars. The government also has the infinite power to change Social Security laws, as demonstrated by the 12 benefit changes shown in this chart.

More than half of all Social Security recipients take benefits before the official retirement age when benefits are reduced.

This demonstrates an early need for benefits by those in lower-income groups.

The government also has the infinite power to change Social Security laws, as demonstrated by the 12 benefit changes shown in this chart.

More than half of all Social Security recipients take benefits before the official retirement age when benefits are reduced.

This demonstrates an early need for benefits by those in lower-income groups.