Yes, Mr. Vargas Llosa, it is time to tell the truth about government finances. Some might say, “Well, past time. Sadly, your article does not do it. The purpose of government financing is not to give the government more money. Because the U.S. federal government is Monetarily Sovereign, it already has infinite money.The national debt is over $34 trillion. It’s time to tell the truth about the U.S. government’s finances Story by Libertarian Alvaro Vargas Llosa

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Federal Reserve Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.“

The purpose of the federal government — any government, in fact — is to improve the lives of the people. One measure of the improvement is Gross Domestic Product, the total amount of spending in an economy. Here is what federal deficit spending has done to Gross Domestic Product.

A normal human would say that a “financial mess” is a situation in which a person has difficulty paying his/her financial obligations. But as Messrs. Greenspan and Bernanke explain, the Monetarily Sovereign U.S. government has no such difficulty. It pays all its financial obligations simply by creating more dollars. So what does Mr. Vargas Llosa mean by “financial mess“? Nowhere in his article does he explain. Typical for “debt- truth tellers” who use frightening words to deceive.If anyone living in the United States in the decades immediately after the Second World War had predicted the self-inflicted financial mess the U.S. government now finds itself in, nobody would have taken that person seriously.

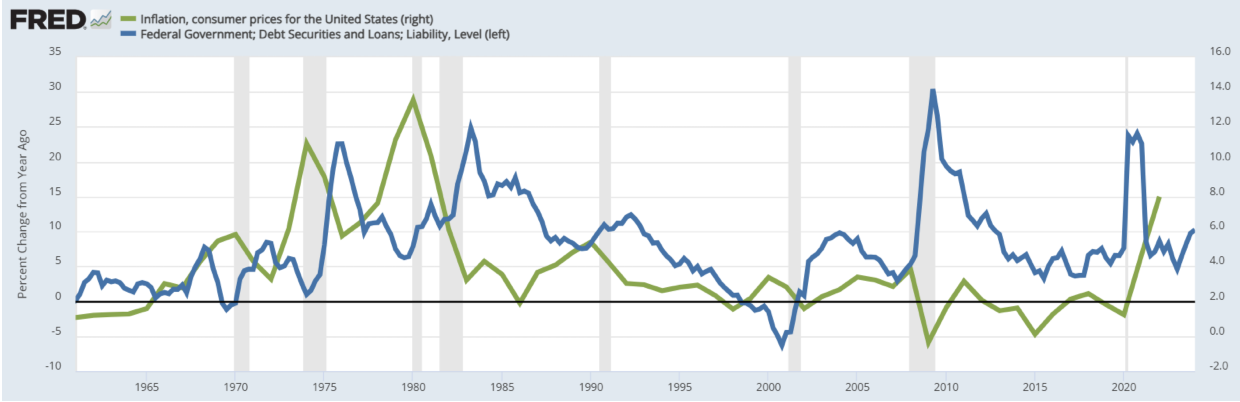

Translation: In 2023, the federal government pumped 1.7 trillion growth dollars into the economy. In the first eight months of the current fiscal year, it pumped another 1 trillion growth dollars into the economy and expects to pump 2 trillion growth dollars into the economy by the end of fiscal 2024. These are dollars that go into the pockets of Americans at no cost to anyone — not to you, not to your friends and family, not to your neighbors. Why? Because federal taxes don’t fund federal spending. Even if federal tax collections totaled $0, the federal government could continue spending forever. The Monetarily Sovereign U.S. federal government neither needs nor uses income. (It is different for state and local governments, businesses, and euro governments, all of which are monetarily non-sovereign, and they do need and use income to fund spending.) The U.S. federal government destroys all the income it receives. Paying creditors is the primary process by which the federal government creates dollars. To pay a creditor, the federal government first creates instructions (checks, wires, etc.) instructing the creditor’s bank to increase the balance in the creditor’s checking account. The instant the creditor’s bank obeys those instructions, new dollars are added to the creditor’s checking account and to the M2 money supply measure. Those dollars are not deducted from the M2 money supply. The bank clears those instructions through the Federal Reserve. Thus the federal government approves its own instructions, which is why it never can run short of dollars. By contrast, when a local government sends instructions, M2 dollars are deducted from the local government’s checking account in a bank and added to a creditor’s bank account. No net dollars are created. They merely are transferred. Not understanding the differences between Monetary Sovereignty and monetary non-sovereignty marks one as ignorant about economics.For most of American history, until the mid-1970s, annual federal spending and revenue were roughly in balance—the exceptions being in wartime.

Contrast that with the federal deficit in fiscal year 2023, which topped $1.7 trillion, an amount larger than Mexico’s total economy (the 12th largest in the world).

It exceeded $1 trillion again in the first eight months of the current fiscal year and, according to the Congressional Budget Office’s latest forecast, released on June 18, will approach $2 trillion by the end of fiscal 2024.

The debt/GDP ratio is meaningless. Those who quote it hope to scare you with irrelevant numbers. Federal debt is not a burden on the government or on taxpayers. It is nothing like private sector debt. Neither you nor anyone else pays for the federal debt—never has, never will. The so-called “debt” is nothing more than dollars deposited into T-security accounts. The contents of these accounts are wholly owned by the depositors and never used by the federal government. The purpose of T-accounts is not to provide spending money to the government. The purpose is to stabilize the dollar by:This has fueled a massive increase in the federal debt, which now totals $34 trillion, about $6 trillion more than America’s gross domestic product (GDP), the value of all the goods and services produced by America’s 330 million residents in a year.

If we count Social Security and Medicare liabilities, total debt is several times larger than GDP.

- Providing a storage place for unused dollars that is safer than any private bank account.

- To help the Fed control interest rates by providing a “floor” rate.

Government spending is more properly termed “investments,” not “debt. The economy doesn’t care where he investments come from. In fact, federal spending creates new growth dollars, while private investment only moves existing dollars. The “truth tellers” prefer the government to reduce its spending under the false narrative that this somehow will grow the economy. But:The consequences are sobering. Politicians like to use euphemisms to describe what they’re doing. Government spending, in the current vernacular, is referred to as “investment.”

Government spending, however, crowds out investment, which explains why private investment, the equivalent of 4.8% of GDP, is 30% lower than in 2000.

GDP = Federal Spending + Non-federal Spending + Net Exports.

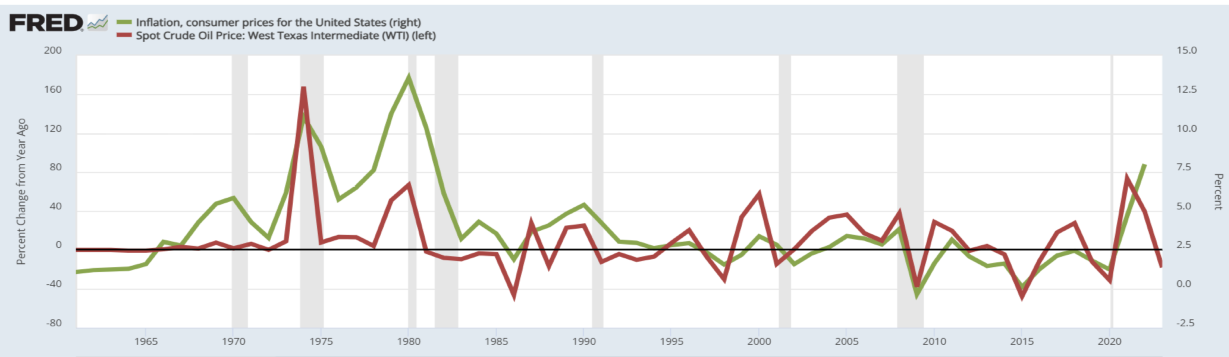

I have yet to communicate with a debt “truth-teller” who can explain the math of how cuts to federal spending will increase GDP.That’s called “inflation,” and as we have seen, the economy has enjoyed real (inflation-adjusted) growth.At the same time, the purchasing power of the U.S. dollar, a reflection of both the federal government’s finances and the Federal Reserve’s money printing, also is down: by more than 50% since 2000.

Translation: This year, at no cost to anyone, the government will pump 900 billion growth dollars into the economy in interest payments alone. In 2054, the government will pump 5.3 trillion growth dollars into the economy — also at no cost to anyone. Most of those dollars will go into the pockets of the American people.As a result of this economic mismanagement, the U.S. government will pay close to $900 billion this year just in interest payments on the national debt—and, according to Congressional Budget Office (CBO) projections, which assume an idyllic scenario of no major wars, no recessions, and no financial crises, debt service will steadily increase to some $5.3 trillion by 2054.

Oh, Mr. Vargas Llosa, I’ll bet you’re not even trying to use your imagination. The only difficulty in “sustaining” the debt came from being on a gold standard, which limited the government’s ability to create dollars. But Nixon took us off the gold standard in 1971 (Roosevelt did it for domestic us in 1933), and since then the federal government has had the infinite ability to “sustain” any level of deficit spending. It never can run short of dollars. Private savings and the debt/GDP ratio are irrelevant to the government’s ability to “sustain.” but one must assume Mr. Vargas Llosa tosses in those numbers for fear effect, not because they make any sense whatsoever.It was hard enough sustaining a debt that stood at 106% of GDP during WWII, when the country’s savings rate was 24%, but sustaining a much higher level of indebtedness with today’s 3% savings rate defies the imagination.

The U.S.’s real GDP was approximately $7.1 trillion in 1993. In 2023, it increased to approximately $21.6 trillion. And this is a “catastrophe”?? One hopes we continue to have “catastrophes” like that.This catastrophe has been a long time in the making. In 1993, for instance, the annual deficit amounted to 3.8% of GDP, and the debt, which seemed astronomically high at a “mere” $4.4 trillion, was Lilliputian by today’s standards.

During Eisenhower’s term, we suffered, not one, not two, but three recessions. One, called the “Eisenhower Recession,” occurred between 1957 and 1958. We had a sharp contraction in economic activity, high unemployment, and a decline in industrial production. Is that an example of “fiscal responsibility?”The trend goes back longer than that. The growth of the U.S. government in modern times is the story of post-WWII America.

President Dwight Eisenhower seems to have been the last guy in the post-WWII era who understood that the welfare state, the warfare state, and tax cuts not backed by tough spending cuts are incompatible with fiscally responsible government, or at least with reasonably-sized government.

This is another sleight-of-hand debt/GDP comparison that is meaningless. Nothing can be learned from comparing federal debt (i.e., the net cumulative total of deposits into Treasury Security accounts) vs. GDP (the total of all government and private spending in any given year). They are akin to comparing tons of butter eaten in the past 10 years with the number of butterflies born this year. Totally meaningless. If you don’t believe me, see Debt To GDP Ratio By Country. Scroll down to the middle of the page, where you will see every nation’s Debt/GDP ratio, from the highest (Japan) to tied for the lowest (Taiwan and several others). Look at those ratios, and you will see they tell you nothing about a nation’s ability to pay its bills.Between 1950 and 1970, total debt (including government, household, corporate, and financial) was stable at about 150% of GDP. After Nixon did away with what was left of the gold standard in 1971, it was off to the races. Since then, total debt has grown by nearly 5,600%, more than double the U.S. economic growth rate.

And there it is: The Libertarian belief in an “onerous legacy” of programs designed to aid middle and lower-income groups. That is the “onerous legacy” that gave us Social Security, Medicare, the War on Poverty, the Office of Economic Opportunity and the Economic Opportunity Act, a Job Corps for disadvantaged individuals, established work-study programs and community action initiatives, provided health insurance for elderly Americans, improving access to medical care, legislation addressing environmental concerns and conservation efforts, supported education, and Civil Rights Laws, focused on reducing racial injustice and promoting equality. Is it any wonder that a right-wing Libertarian should consider those “onerous?” After all, they cost dollars the government creates at the touch of a computer key, and much to Libertarian dismay, narrow the Gap between the rich and the rest.There was a time, even in the middle of the Cold War, when government leaders, despite their international responsibilities and the onerous legacy of the New Deal and Great Society that nobody dared reverse, understood the need for fiscal discipline and containing the growth of government.

Oh, yes, cut defense spending to weaken the military at a time when we are the last hope for democracy. And eliminate the “bread and butter” for the poor and disadvantaged. Perfect. And then there were the “unfunded tax cuts,” which is an oxymoron. Taxes need to be funded by the people. No one needs to fund tax cuts. They don’t need to be paid for, and the government doesn’t need or use taxes. In fact, it destroys all tax dollars it receives.The 12 years under Presidents Ronald Reagan and George H. W. Bush averaged a 4% deficit due to defense spending increases, abandonment of domestic restraint—a legacy of Johnson’s “bread and butter” years and the Nixon-Ford presidencies’ about-face on most of the economic principles they previously had espoused—and the unfunded tax cuts influenced by Arthur Laffer’s notion that tax cuts would pay for themselves.

And yet again he mentions the meaningless debt/GDP ratio. It never ends for the Libertarians.The new millennium distorted matters even further, with the annual deficit from 2002 to 2023 averaging 5% over the two decades, 20% higher than nominal economic growth, which averaged 4.2%.

And the economy grew massively.President Obama, under whom the deficit was double the Congressional Budget Office’s original projections, got the spending spree started, with Presidents Trump and Biden taking it to new levels.

The above is a perfect description of the effort to widen the Gap between the rich and the rest, while weakening our economy and our national defense.It’s now come down to this. Unless a new generation of leaders has the courage to cut such “untouchables” as the defense, education, justice, and homeland security budgets, and privatize the Social Security program (as more than 40 countries wisely have done), sooner or later, the current trajectory of federal finances will lead to an extremely ugly place.

If we ever elect a right-wing, Libertarian fool to be President, along with our current, right-wing SCOTUS, and right-wing governors, things can get much worse. Rodger Malcolm Mitchell Monetary Sovereignty Twitter: @rodgermitchell Search #monetarysovereignty Facebook: Rodger Malcolm Mitchell; MUCK RACK: https://muckrack.com/rodger-malcolm-mitchellIf you think things are bad now, just wait.

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

opposition to an obsession with contamination by genetic material from a perceived inferior bloodline.

opposition to an obsession with contamination by genetic material from a perceived inferior bloodline.

/cdn.vox-cdn.com/uploads/chorus_asset/file/13649459/1074706918.jpg.jpg)