I am above the law. I am the law.

I own the Attorney General.

I own the Justice Department.

I own the U.S. Senate and the Majority Leader.

I own the Republican Party.

I own the Supreme Court.

I own the Appellate Courts.

I own the Military.

I own the prisons.

I own the favorable media, and I will destroy the rest.

I will pervert the criminal justice system in any way I wish.

I will pardon all criminals who are loyal to me.

I will continue to lie, cheat, and steal, but I will not be punished.

I will ignore the Constitution.

I will exact revenge against my political enemies.

I will punish whistleblowers who reveal my secrets.

I will punish any who displeases me.

I will enable my political loyalists to break the law, free from punishment.

I will continue to put my friends and family into positions of financial and political power.

I will continue to hire political hacks who do as I say, not what is best for America.

I will make billions of dollars from my position.

I will reverse all judicial decisions that displease me.

I will reverse all Congressional decisions that displease me.

I will fire the Federal Reserve chairman if he doesn’t make me richer.

I will divorce another wife and cheat on the next one.

I alone will send America into war.

I alone will decide who enters America and who must leave.

I will do whatever I want, whenever I want.

There is nothing you can do about it.

King George III was America’s last old king.

I am America’s first new king, King Donald I.

The religions will support me, just as they always support kings.

You will obey me.

Or you will be punished.

Buy stocks. If the following Chicago Tribune/ Associated Press article proves to be correct, America’s economic boom will continue for at least another decade.

Here are some excerpts and translations:

This is how the GOP, the Dems, and Reason.com fill a bucket.

US on track for first $1T budget deficit since 2012

By Martin Crutsinger Associated Press

WASHINGTON — The U.S. budget deficit through the first four months of this budget year is up 19% from the same period a year ago, putting the country on track to record its first $1 trillion deficit since 2012.

Translation: . . . putting the economy on track to receive 1 trillion growth dollars from the government this year.

The Treasury Department said Wednesday in its monthly budget report that the deficit from October through January was $389.2 billion, up $78.9 billion from the same period last year.

Translation: The Treasury Department said Wednesday in its monthly budget report that it sent 389.2 billion growth dollars into the economy from October through January, up $78.9 billion from the same period last year.

The deficit reflected government spending that has grown 10.3% this budget year while revenue was up only 6.1%.

For January, the deficit totaled $32.6 billion, compared to a surplus a year ago of $8.68 billion.

Translation: The deficit reflected government stimulus to the economy has grown 10.3% this budget year while taking dollars out of the economy was up only 6.1%.

For January, 32.6 billion growth dollars were added to the economy, compared to a year ago when $8.68 billion were removed from the economy.

Cutting deficits to grow the economy is like applying leeches to cure anemia.

President Donald Trump sent Congress a new budget blueprint Monday that projects the deficit will top $1 trillion this year but then will decline over the next decade.

But the Congressional Budget Office is projecting that the deficit will top $1 trillion this year and remain above $1 trillion over the next decade.

Translation: President Donald Trump sent Congress a new budget blueprint Monday that projects sending more than 1 trillion growth dollars into the economythis year, but then would send less over the next decade.

However, the Congressional Budget Office is projecting that 1 trillion growth dollars will be sent into the economy this year and more than 1 trillion growth dollars will be sent in every year over the next decade.

The deficit for the 2019 budget year, which ended Sept. 30, was $984.4 billion, up 26% from the 2018 imbalance.

Translation: Growth dollars added to the economy for the 2019 budget year, which ended Sept. 30, totaled $984.4 billion, up 26% from the 2018 lesser surplus.

The rising deficits reflect the effect of the $1.5 trillion tax cut Trump pushed through Congress in 2017 and increased spending for military and domestic programs that the president has accepted as part of a budget deal with Democrats.

Translation: The rising economic stimulireflect the effect of the $1.5 trillion tax cut for the rich Trump pushed through Congress in 2017 and increased spending for military and domestic programs that the president has accepted as part of a budget deal with Democrats.

In his new budget plan for the 2021 fiscal year that starts Oct. 1, Trump is proposing spending $4.8 trillion, but would seek to hold down deficits by cutting domestic programs like food stamps and Medicaid.

In his new budget plan for the 2021 fiscal year that starts Oct. 1, Trump is proposing adding 4.8 trillion growth dollars to the economy, but would seek to punish the poor and the economy, by unnecessarily cutting domestic programs like food stamps and Medicaid.

Trump’s plan projects that if Congress goes along with his spending cuts, which is unlikely, the budget would return to balance in 15 years.

Translation: Trump’s plan projects that if Congress goes along with his spending cuts, which is unlikely, the government will take more than a trillion dollars out of the economy, and destroy those dollars, preventing any hope for economic growth, and assuring a depression that would make the 1929 depression look like a garden party.

Through the first four months of this budget year, government spending has totaled a record $1.57 trillion, up 10.3% from the same period last year.

Revenue also set a record for the first four months of a budget year, increasing by 6.1% to $1.18 trillion.

The government first ran $1 trillion deficits from 2009 through 2012 as revenue fell during the worst recession since the 1930s.

Translation: Through the first four months of this budget year, government growth dollars added to the economy have totaled a record $1.57 trillion, up 10.3% from the same period last year.

Unfortunately, the growth dollars removed from the economy also set a record for the first four months of a budget year, increasing by 6.1% to $1.18 trillion.

The government pumped $1 trillion into the economy annually from 2009 through 2012, which helped the economy recover from the worst recession since the 1930s.

We can end this post by showing you excerpts from a truly ignorant article that appeared in Reason.com:

To Revive the Economy, Cut Federal Spending

Obama and Boehner are both big spenders. That’s the problem.

NICK GILLESPIE AND VERONIQUE DE RUGY, 1.1.2013

The Republican opposition, led by House Speaker John Boehner of Ohio, has signaled that the Republicans could stomach generating as much as $800 billion in new revenue over the next decade.

Such a large difference obscures a more fundamental agreement: Neither side is interested in addressing the central role federal spending plays in creating persistent deficits and, more important, damping economic growth.

The deficit for fiscal 2012, which ended on Sept. 30, came in at about $1.1 trillion, marking the fourth consecutive year that the nation has posted a trillion-dollar-plus spending gap.

It’s fun to look back in time to see what people, who are completely ignorant of Monetary Sovereignty, said.

We’ve done that when we repeatedly published those “The Deficit is a Ticking Time Bomb” articles since 1940. (The bomb still is ticking).

And now we have the Reason.com’s daily serving of abject ignorance. You’ll note that the article makes dire predictions about the economy unless the government stops adding dollars to the economy.

(Thankfully, it didn’t stop; the dollar additions cured the Great Recession, and after the article was published, the economy continued to grow because of more dollar additions.)

Yet even today, if you go to Reason.com, you’ll find those folks have learned nothing. They still publish the same blather about the danger of deficits.

And here’s the real knee-slapper:

The article quotes economists Carmen M. Reinhart, Vincent R. Reinhart, and Kenneth Rogoffwho famously were discredited, partly because they didn’t take into account the differences between a Monetarily Sovereign nation and a monetarily non-sovereign nation. And these are “economists.”

They said that periods of “debt overhang” – when accumulated gross debt exceeds 90 percent of a country’s total economic activity for five or more consecutive years—reduce annual economic growth by more than one percentage point for decades.

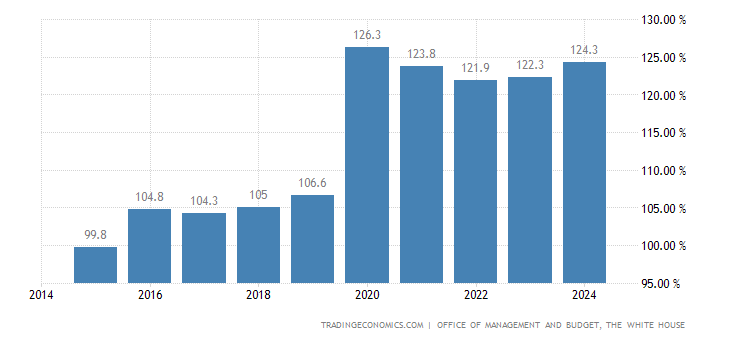

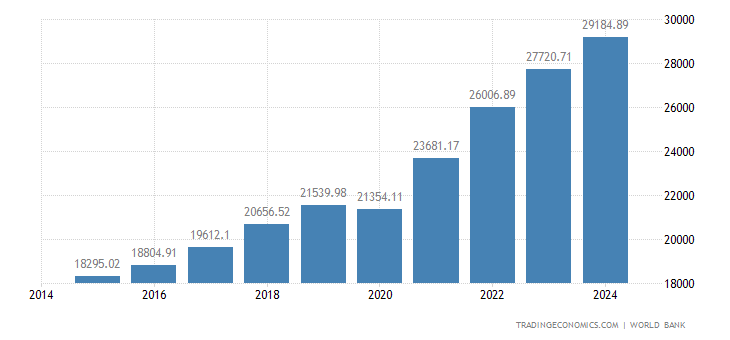

Oh REALLY? Look at this graph:

GDP/Federal Debt Ratio

Every year since 2010 (lots more than ten years), the federal debt has exceeded that magic 90% number, and the economy . . . oops . . . well, look for yourself:

GDP growth for the U.S.

Is Reason.com chastened by the facts? No, facts be damned. They have the “We know what we know and don’t bother us with facts” attitude.

And that is how the public is kept ignorant.

And that also is why we will not have a recession in the foreseeable future unless some politician can convince his/her peers that taking money out of an economy is a clever way to grow the economy. (Sort of like spilling water out of a bucket is a clever way to fill the bucket.)

So long as we keep running trillion-dollar deficits, and the deficits keep growing, my advice will be to buy stock.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

In certain applications (for example, a Jobs Guarantee) which MMT recommends and MS does not, and

The primary purpose of federal taxes. MMT says they are to give value to money; MS says they are to control the economy and to deceive the public and:

Inflation: MMT says curing inflation requires tax increases. MS says curing inflation requires deficit spending to eliminate shortages, usually of food or energy.

But they agree on the key fundamentals, for instance:

Money moves between the economy and the government.

The federal government invented the U.S. dollar, creates dollars at will, and so cannot run short of dollars.

The federal government does not borrow to fund spending, but rather creates new dollars every time it pays a bill.

So-called “federal debt” is nothing more than the total of deposits into T-security accounts, which easily are repaid by returning the dollars deposited, are not paid by taxpayers.

No level of federal debt is unsustainable.

Federal tax dollars are destroyed upon receipt.

In short, deficit spending by the government goes into the economy, and taxes paid by the economy go into the government. The difference: Monetarily sovereign governments have infinite access to money; economies do not.

The following are excerpts from an article that appeared in the June 5, 2019, New York Times, and written by Ben Dooley

Immediately, the article is misleading. Rather than saying “Despite its huge debt . . .” it should read, “Because of its huge debt . . . ” or even more accurately, “Because of its massive deficit spending, which led to a huge amount of deposits into government bond accounts.”

TOKYO — Spend big and never mind the deficit. That’s what proponents of modern monetary theory, the unorthodox set of economic ideas that has inspired politicians like Bernie Sanders and Alexandria Ocasio-Cortez, see as the winning formula for American prosperity.

It may have “inspired” them, but even they cling to the false notion that federal taxes are necessary to fund federal spending.

For proof, its admirers point to Japan. Despite the highest debt in the developed world, Japan remains an economic powerhouse with high living standards.

Becausethe Japanese government, like the governments of Canada, the UK, Australia, China, and others, is Monetarily Sovereign (it creates its own sovereign currency), Japan remains an economic powerhouse with high living standards. ”

Japanese leaders wish they would point somewhere else.

Shinzo Abe, the Japanese prime minister, has dismissed the theory as “simplistic.” Finance Minister Taro Aso described it as “very dangerous.” And Haruhiko Kuroda, the head of Japan’s central bank, called it “extreme.”

Monetary Sovereignty saved Japan’s economy.

Had Japan been monetarily non-sovereign, like the euro nations or like cities, counties, and states, the Japanese economy would be shattered, and the Japanese people would be destitute.

Perhaps, Mr. Abe would respect something more complex than: “Adding yen to the economy helps prevent recessions” and “Monetarily Sovereign governments never can run short of their own sovereign currency.”

Rather than embrace an idea that could explain or even justify the country’s situation, Japan is furiously debating it.

Lawmakers to Mr. Abe’s left are citing the theory — known as M.M.T. — to denounce his plan to raise taxes on the country’s consumers.

On the right, members of his own party have tried to link his policies to the theory, accusing him of running up gargantuan debts the country can never repay.

Japan could repay all of its debt tomorrow, if it chose. Like all Monetarily Sovereign nations, it has the unlimited ability to create its own sovereign currency.

Imagine you owned a legal, dollar-printing press. How many dollars of debt could you repay? The answer, of course, is: Infinite.

According to economics textbooks, when deficits grow, inflation and interest rates should grow along with them.

That is not what has happened in countries like the United States that racked up huge government debt after the global financial crisis in 2008.

Instead, prices and borrowing costs have remained low.

The textbooks are wrong, as both Japan and the United States have proved. There is no relationship between today’s deficits (high) and inflation (low).

In the United States, politicians from both parties have begunto question decades of consensus that government debt is bad. President Trump’s tax cuts have widened the deficit.

Proposalsfloated by Democrats for universal health care and investments in renewable energy could make it even bigger.

“Have begun.” I’ve been questioning it for 20 years. Other economists have questioned it even longer.

Trump’s tax cuts have widened the deficit, yet inflation remains low and growth continues. Those are facts, not economic hypotheses.

Sadly, those proposals have been floated by politicians who do not have the courage of their convictions. They still try to answer the question, “How will you pay for it?” by advancing a complex, convoluted “solution,” in which federal deficits do not increase.

The numbers make budget hawks nervous. But proponents of modern monetary theory say they should take a deep breath.

Deficits are a good thing, they say, as long as the government doesn’t create inflation by pushing the economy too far, too fast.

“Pushing the economy” is not the way inflations are created. Price increases are caused by shortages, usually shortages of food and energy, not by increased government spending.

In fact, increased government spending can cure inflations if the spending is devoted to curing the shortages.

If there is a food shortage, there will be inflation. If the government responds to the food shortage by using deficit spending to purchase food from abroad and distributing it to the people, the inflation will end.

The idea has provoked criticism from established economists like Paul Krugman, the Nobel laureate and columnist for The New York Times, as well as Lawrence Summers, the former Treasury secretary.

Government spending may be necessary when times are tough or to meet national priorities, they argue. But the bill will eventually come due.

In the meantime, all of that spending could crowd out the private sector and make it harder for governments to borrow money in the form of bonds. Besides, they say, M.M.T. remains largely untested.

Krugman and Summers simply do not know what they are talking about. “The bill will eventually come due” makes no sense. There is no “bill” for deficit spending.

The federal government can deficit spend forever.

And the federal government, which has the unlimited ability to create dollars, it has no need to borrow, and indeed, the U.S. government does not borrow.

What erroneously is termed “borrowing,” really is the issuance of Treasury securities (T-notes, T-bills, T-bonds) which do not provide spending money to the government.

When you buy a T-bill, you deposit dollars into your T-bill account. There you dollars remain, accumulating interest, until maturity. The U.S. government does not use the dollars in your T-bill account.

Proponents of the theory disagree (with Krugman and Summers). It has been tested, they say. In Japan.

The country is their equivalent of Charles Darwin’s Galápagos Islands: a natural experiment that reveals a fundamental truth about the way the world really works.

Since the country’s boom ended in the early 1990s, Japan has borrowed deeply. Currently, its debt level is approaching 250 percent of its annual economic output (GDP).Critics say it is an economic basket case.

Despite all that, Japanese inflation and lending rates remain low. In fact, some bond rates are negative, meaning Japan can profit when it borrows money.

Its standard of living remains competitive with those of the United States and other developed countries.

Negative bond rates result from the mistaken idea that low rates are stimulative of negative rates really are stimulative. Utter nonsense. High rates force the government to pump more interest money into the economy, and that is stimulative.

Low rates are unprofitable for lenders, and because lending creates money, negative discourage lending, sonegative rates are recessionary.

And because Japan is Monetarily Sovereign, it has no need to make a profit. It can create all the yen it needs, at the touch of a computer key.

Modern monetary theory explains it all, according to Bill Mitchell, a professor of economics at the University of Newcastle in Australia and one of the theory’s founders. He has been studying Japan since the 1990s.

“It is my laboratory,” he said, calling the country “a really good demonstration of why mainstream macroeconomics is wrong.”

Briefly stated, the theory holds that a country controlling its own currency like the United States and Japan cannot go broke no matter how much it borrows.

Government spending puts money in the hands of people and businesses. In other words, a government deficit is effectively a private sector surplus.

It’s not just a belief; it’s an absolute fact. A federal deficit adds money to the economy, which grows the economy. It is simple arithmetic.

To spur growth, the theory says, governments should run up deficits to give consumers and companies more to spend. If leaders need more money, they can print it.

That is basically what Japan has done on and off for the last 20 years. Its economy boomed after World War II. Then the go-go 1980s ended with a bust. The economy stagnated. Deflation drove down prices and corporate profits.

The debt “Henny Pennys” are so spooked by non-existent inflation that they forget about the real curse: Deflation.

Japan borrowed and spent to get growth going again.

When that didn’t work, it pioneered techniques, like quantitative easing, to inject money into its financial system. The idea — basically printing lots of money and spending it on large-scale asset purchases — went on to be used by central banks around the world to deal with the effects of the global financial crisis.

The measures were necessary, but Japan’s conservative policymakers were not happy about them, according to Gene Park, an expert on the Japanese economy at Loyola Marymount University in Los Angeles, and they were soon dropped.

Translation of the above: Adding yen to the economy cured the deflation and grew the economy. It worked.

But it violated the beliefs of the mainstream economists, so they stopped doing what worked.

Similarly, deficit spending cured America’s 2008 “Great Recession” (as well as the 1929 “Great Depression), so again, the economists railed against what works, and try to install what doesn’t work: Austerity.

That has led to 80 years of complaints that the growing federal debt is a “ticking time bomb,” — while the American economy has grown — a complaint that continues to this day.

Economics may be the only science in which the mainstream denies what always works and insists on implementing what never works.

“The ideas came from outside of Japan, and they only tried them when they were backed into a corner,” he said.

Still, inflation did not budge. Interest rates stayed low.

Of course.

Inflation is not caused by deficit spending. Inflation is caused by shortages. Period.

While Mr. Abe’s policies may resemble those put forward by supporters of the theory, they differ in one major way: Since his election, he has pledged to find a way to pay down the debts run up under his administration.

Mr. Abe is following the usual mainstream economists’ dictum: If it works, stop doing it, and if it never works, keep doing it.

To fulfill that promise, Mr. Abe has said, he will raise Japan’s consumption tax to 10 percent from 8 percent by October.

The pledge is controversial with lawmakers on both the left and right.

A similar tax increase in 2014 may have pushed Japan’s already sluggish economy into recession. This time, the economy has already been weakened by China’s slowing demand for its goods.

Does it get any dumber than that? The economy is sluggish, so let’s take money away from consumers.

Many in Mr. Abe’s party also oppose the tax increase, arguing that the government should address the deficits once Japan’s economic condition has improved and the country is better able to withstand the shock.

In the meantime, they fear that if Japan continues piling up debt, it will be even harder for the country to climb back out.

“A crash is going to come at some point,” said Kohei Otsuka, an opposition member of the Upper House finance committee who has warned about the country’s debt for over two decades, “and then we’ll see that M.M.T. didn’t have any merit after all.”

Get it? We know that cutting deficits will create a shock, so let’s do it. And we have been warning about debt for over two decades, and nothing bad happened, so that is evidence we have been right.

Only in economics could that be considered logical.

Pavlina Tcherneva, an associate professor of economics at Bard College in New York and part of a core group of M.M.T. theorists, said the debate demonstrated an important point: While the Japanese case may validate the ideas, there is a difference between the theory of M.M.T. and its practice.

“Japan has been the clearest case of some of the things that M.M.T. has been saying,” she said, but “that doesn’t guarantee you good policy.”

Yes, stunningly in the weird world of economics, where intuition rules over proven fact, you even can get statements of belief in deficit spending, but then the leaders cannot believe what their eyes tell them, and they regress into the nightmare world of austerity.

In the past, economists wrote textbooks that claimed: “Excessive government spending causes inflations.” This became dogma, when Weimar Republic, Zimbabwe et al had hyperinflations that corresponded to currency printing.

So when the likes of Krugman and Summers went to college and learned that deficits cause inflation, they not only were indoctrinated, but continued the flow of false information to young people, who themselves indoctrinated even younger people.

And so it went, with successive generations of economists ignoring the facts on the ground, and disseminating the false beliefs.

The facts are:

The currency printing does not cause the inflations; the inflations caused the currency printing, because the leaders did not understand that shortages caused their inflations. So out of ignorance, they printed currency to keep up with inflation.

Monetarily Sovereign governments cannot run short of money with which to pay any size obligations.Oh, and one last point that has become an issue, lately’

Deficit spending is not “socialism.” Socialism is government ownership and control, not mere spending.

For example, the U.S. Veterans Administration is socialism. Medicare is not.

Economics may be the only “science” in which the lay public believes it knows everything, and the university-trained scientists rely more on intuition than on facts.

What next, economists? Do you recommend we apply leeches to cure anemia?