We speculated on the fanciful notion that we humans may be one step in some grand scheme. (It’s all just fun and games but play along for a bit.)

In this mythical (?) grand scheme, would our purpose be to serve as an interim species in a series of experiments? The previous experiment had to do with size. Dinosaurs led the way.

After millions of years, that experiment eventually failed, with only birds left as a reminder. The current experiment has to do with intelligence, where we have become the leading actors, but perhaps we aren’t the ultimate step.

Are we an interim step in a grand scheme?

Could it be our purpose on earth is to develop nature’s next experiment: Superintelligence and other superpowers of survivability?

In my self-appointed experimenter role in this experiment, I played with the chatbot “Co:here.”. (Thank you reader, Nicholas Gomez.)

You can go there and experiment for yourself. Here are some of my results:

My question: Can the federal government run short of dollars if nobody pays taxes?

Co:here: No, the federal government cannot run short of dollars if nobody pays taxes. The federal government collects taxes in order to fund its operations and to pay for programs and services. It also collects taxes to pay for the debt that it has incurred.

Immediately, you get an inkling of illogic: Can’t run short of dollars, but needs dollars to fund . . . ======================================================== Question: Does the federal government need to collect taxes to create dollars?

Co:here: The federal government does not need to collect taxes in order to create dollars. It can create dollars through its own actions, such as by purchasing bonds or by making loans.

The federal government collects taxes because it needs to have a source of revenue in order to operate. It also collects taxes to fund programs and services that are not self-sufficient, such as social security and Medicare.

Now we enter the gibberish stage, where Co:here begins to meld competing ideas. “Can create dollars,” but “needs to have a source of revenue.”

Question: Isn’t this illogical: The government created dollars by spending them and collects dollars to pay for spending?

Co:here: The government does not create dollars by spending them. It creates money by spending money. The government collects dollars to pay for spending in the sense that it uses tax revenue to pay for spending, but this is not the same thing as collecting dollars to pay for spending.

Apparently, Co:here thinks money and dollars are different things. ==========================================================

Question: What causes inflation?

Co:here: Inflation is caused by an increase in the money supply.

Inflation is caused by an increase in the money supply, which can be caused by a variety of factors. One of these factors is oil shortages.

When there is a shortage of oil, it can lead to higher prices for oil and other related products. This can lead to inflation, as people may have less money to spend on other goods and services.

Suddenly, Co:here began to answer some questions twice. Note the contradiction where inflation is caused by an increase in the money supply and by people having less money. ==========================================================

Question: Does an increase in the money supply cause oil shortages?

Co:here: No. An increase in the money supply causes inflation because it increases the amount of money in circulation.

Question: Does an increase in the amount of money in circulation increase the demand for oil?

Co:here: No, an increase in the amount of money in circulation does not increase the demand for oil.An increase in the amount of money in circulation causes inflation, which decreases the demand for oil.

Question: Why does inflation decrease the demand for oil.

Co:here: Inflation is closely tied to the cost of energy. When the price of oil rises, the price of goods and services that rely on oil as a raw material or fuel also tends to increase.

Which is the correct answer? Does the U.S. federal government borrow money because it has to or because it chooses to?

Co:here: The correct answer is The U.S. federal government, which is Monetarily Sovereign, borrows money rather than just creating it because it chooses to.

Question: Why does the U.S. federal government, which is Monetarily Sovereign, chooses to borrow money rather than just creating it”

Co:here: The U.S. federal government, which is Monetarily Sovereign, chooses to borrow money rather than just creating it because it wants to be able to spend more money than it has.

Co:here: Total debt is the sum of all federal government liabilities.The federal government’s debt consists of the sum of all federal government liabilities.

Question: Why did you say the total debt is $18.6 trillion when some people say it is $26 trillion?

Co:here: The $18.6 trillion figure represents the total amount of debt that the federal government owes. This includes both debt held by the public, such as Treasury bonds, and debt held by government agencies, such as the Federal Reserve.

The $26 trillion figure represents the total amount of debt that the federal government owes, including debt held by the public and debt held by government agencies.

Co:here seems to be a buzzword or buzz phrase collecting machine that does not recognize inconsistencies.

One is reminded of a highschool sophomore, writing a paper the night before it is due.

As a slight aside, if ever you go to Google Images, you can type in any words, and it will provide you with pictures, some of which are appropriate and some not.

Co:here seems to operate in a similar way.

Go to that site and type in “What is Monetary Sovereignty?,” and you’ll see a picture version of a chatbot.

We humans are among the latest in a long line of mostly extinct species on earth, and to the best of our knowledge, we are the smartest.

But are we the final step, or are we just another interim species? Will we be replaced by an even smarter species?

Nature has tried millions of experiments. There have been notable experiments with size, with the dinosaurs taking center stage.

The first dinosaurs emerged during the Triassic Period, 252 to 201 million years ago. During the Jurassic Period (201 to 145 million years ago) many large land animals went extinct, leaving more opportunity for the dinosaurs.

During the Cretaceous Period (145 to 66 million years ago) dinosaurs continued to evolve, and the biggest dinosaurs emerged. The Argentinosaurus huinculensis is the biggest dinosaur ever found.

And then they died.

But for the whales, nature’s experiment with size ended, to be replaced by the experiment with intelligence, which featured the mammals.

While many dinosaurs were warm blooded, and had large brains, both facilitating intelligence, our hands and upright stature seem to have brought us to the apex of intelligence.

So far, for the experiment continues.

The big news in intelligence is artificial intelligence(AI) as demonstrated in chatbots.

IBM says, “A chatbot is a computer program that uses artificial intelligence (AI) and natural language processing (NLP) to understand customer questions and automate responses to them, simulating human conversation.”

If you use Siri or Alexa, you are using a basic chatbot. You ask a question in plain language and get an answer in plain language. So ubiquitous are these programs and devices that we often take for granted the technological miracle they represent.

I ask my tiny wristwatch a question, and despite my midwestern accent, and the variety of ways I phrase it, the watch searches the internet and within mere seconds, delivers an answer in a language of my choosing — both in audio and in print.

Are we an interim species?

It is a miracle, but it is yesterday’s miracle. Today’s technology has taken the concept much further.

Today, you can ask a chatbot to develop an original treatise on a subject.

The chatbot will search the Internet using advanced keyword techniques and create a paper containing information and a reasoned discussion.

In that sense, it operates much like you would if given the same assignment.

Chatbots learn via “computer learning,” AI trial and error, to provide “better” responses (meaning more accurate and human).

Being computer programs, chatbots can conduct millions of trials and learn from millions of errors in a relatively (compared to you and me) short time. They can work 24/7, don’t tire, and they don’t forget.

Thus, through time, chatbots continually become “smarter.”

Although chatbot responses can seem eerily human, they still lack what you might call “common sense,” a basic understanding of reality — but they are learning.

Cosmos magazine published an article about “Chatbot blunders.”

Here are some excerpts:

It’s taken just a few days for Google AI chatbot Bard to make headlines for the wrong reasons.

Google shared a GIF showing Bard answering the question: “What new discoveries from the James Webb Space Telescope can I tell my 9 year old about?”

One of Bard’s answers – that the telescope “took the very first pictures of a planet outside of our own solar system” – is more artificial than intelligent.

A number of astronomers have taken to Twitter to point out that the first exoplanet image was taken in 2004 – 18 years before Webb began taking its first snaps of the universe.

No one should be surprised that machines make mistakes, some of which can be hilarious. But we rely on them to be perfect, and they are — at a basic level. They copy and paste much better than we do. They can compute our income taxes flawlessly.

This essential perfection can lead us to believe in an overallperfection that does not exist and never will.

Google’s embarrassment over this mistake is compounded by the fact that it’s Bard’s first answer ever… and it was wrong! Bard is Google’s rushed answer to Microsoft-backed ChatGPT.

Both Bard and ChatGPT are powered by large language models (LLM) – deep learning algorithms that can recognize and generate content based on vast amounts of data.

The problem is that, sometimes, these chatbots simply make stuff up. There have even been reports that ChatGPT has produced made-up references.

“Wrong answers.” “Make stuff up.” Apparently, ChatGPT is even more human than some might have imagined.

It’s not “conscious” because the AI itself is not conscious; nevertheless, they are called “hallucinations.” They are the result of the software trying to fill in gaps and trying to make things sound natural and accurate.

It’s a well-known problem for LLMs and was even acknowledged by ChatGPT developers OpenAI in its release statement on November 30, 2022: ChatGPT sometimes writes plausible-sounding but incorrect or nonsensical answers.”

“Not conscious.” “Trying to make things sound accurate.” That sounds like some of the economists I know. ”

Experts say even the responses to the “successes” of artificial intelligence chatbots need to be tempered by an element of restraint.

The fundamental problem has to do with where the chatbots get their information. Remember the old computer mantra, “Garbage in, garbage out”?

That still applies. It applies to human responses, and it applies to computer responses. Why would machines be any more accurate?

In a paper published last week, University of Minnesota Law School researchers subjected ChatGPT to four real exams at the university. The exams were then graded blind.

After answering nearly 100 multiple-choice questions and 12 essay questions, ChatGPT received an average score of C+ – a low but passing grade.

C+ is pretty impressive, assuming the scorers were correct. If we have a chatbot grade the answers given by another chatbot, how will we know the “correct” grade?

Are we to assume human grading is more accurate?

Another team of researchers put ChatGPT through the United States Medical Licensing Exam (USMLE) – a notoriously difficult series of three exams.

A pass grade for the USMLE is usually around 60 percent. The researchers found that ChatGPT tested on 350 of the 376 public questions available from the June 2022 USMLE release scored between 52.4 and 75.0 percent.

I wonder how ChatGPT scored between 52.4 and 75.0 percent. Did they give the test repeatedly? Who determined which answers were correct?

In medicine, as in most sciences, much of what was thought to be correct yesterday now has been found incorrect, and tomorrow, that will change again.

It’s called “science,” the purpose of which is to identify and correct yesterday’s misunderstandings.

The authors claim in their research, published in PLOS Digital Health, that “ChatGPT produced at least one significant insight in 88.9% of all responses.”

In this case, “significant insight” refers to something in the chatbot’s responses that is new, non-obvious, and clinically valid.

How were “new,” “non-obvious,” and “clinically valid” determined? If a chatbot disagrees with a human, who is right?

But Dr. Simon McCallum, a senior lecturer in software engineering at New Zealand’s Victoria University of Wellington, says that ChatGPT’s performance isn’t even the most impressive of AI trained in medical settings.Google’s Med-PaLM, a specialist arm of the chat tool Glan-PaLM, is another LLM focused on medical texts and conversations.

“ChatGPT may pass the exam, but Med-PaLM is able to give advice to patients that is as good as a professional GP. And both of these systems are improving.”

And who determines that advice is “as good as a professional GP”? It would be informative to learn how that was determined.

I don’t have access to a sophisticated chatbot, so if you do, I would appreciate your asking it such questions as:

“What do United States federal taxes pay for?”

“Who will have to pay off the federal debt?”

“Is the federal debt too high?”

“How does the federal government borrow money?”

“Does federal deficit spending cause inflations?”

I chose the above questions because I suspect even the current level of chatbot technology merely regurgitates the common beliefs on any subject and does not analyze the way humans do.

I asked my Siri question #1, and she (it) answered, “Here’s what I found: Governments can use tax revenue to provide public services such as social security, healthcare, national defense, and education.”

The keywords are “Here’s what I found.” Siri isn’t thinking. Siri merely is playing back.

It gave the standard answer, which would be correct for state, county, and city governments, but it is not valid for the U.S. federal government. Siri has not yet learned about Monetary Sovereignty.

But what if Siri did learn about Monetary Sovereignty (MS). Ask most economists and they will tell you the federal government does borrow money, an answer with which MS strongly disagrees. Many, if not most, economists disagree with MS’s precepts.

The MS answers to the above questions are:

Federal taxes pay for nothing. They help the government control the economy by taxing what it wishes to discourage and by giving tax breaks to what it encourages. That’s the theoretical purpose. The real goal is to make the rich richer by widening the income/wealth/power Gap between the rich and the rest.

The so-called “debt” is paid off by returning dollars already in T-security accounts to the owners of those accounts.

No, the federal debt (i.e., the total of T-securities) is not too high. Decreasing the debt causes recessions and depressions. Increasing the federal debt would help increase the Gross Domestic Product (GPD), i.e., grow the economy.

The federal government never borrows money. It creates all the dollars it needs by pressing computer keys.

No, shortages of critical goods and services, usually oil and food, cause inflations. Federal spending doesn’t cause shortages or inflations.

I suspect that chatbots, which use AI to learn the correct answers, will not provide the MS answers, as those answers will be the minority view. Siri, for instance, told me the federal government borrows to pay its bills.

Chatbots are giant data-gathering machines. They really are good at that. We humans are data-gathering machines, too. We analyze data the way chatbots do by comparing it with what we already know.

But humans function differently. I suspect the more creative among us are more receptive or willing to examine minority concepts.

I suspect we are more likely to investigate the rejected, the impossible, the already “proved” wrong, and the crazy “what if” ideas that AI is designed to winnow out.

Our thinking is what differentiates us from the rest of life on earth. We imagine. We visualize. We dream. We hope. We aspire. We dare to be different.

If nature has a plan, was the plan for us to be smart enough to create artificial intelligence?

Today, we drift toward a “Terminator” world. As we simultaneously birth, rule over, and battle our machines, will there come a time when our electronic children replace us?

Are we nature’s interim species, on earth to pave the way for the next experiment?

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

The “ticking time bomb” is the federal debt that supposedly is so big as to be “unsustainable.” You remember. It’s the “bomb” that has been sustained for 84 years.

If someone is wrong every year for 84 years, would you believe them? Unfortunately, some still believe the federal debt is “unsustainable,” a “ticking time bomb,” and should be combated with a debt limit.

I have no polite words to describe those people. Sadly, I now must tell you about “the world’s largest Ponzi scheme,” which, by no coincidence, also is the federal debt.

Peter Schiff

“Ponzi” is the latest term used by people who either don’t understand Monetary Sovereignty or don’t want you to understand Monetary Sovereignty.

With the U.S. reaching its debt limit of $31.4 trillion on Jan. 19, Treasury Secretary Janet Yellen urged lawmakers to increase or suspend the debt ceiling.

Janet Yellen reveals that she knows the debt ceiling is unnecessary, useless, and harmful. Otherwise, she would ask that the debt be paid off.

She knows, however, that federal finance makes that not just unnecessary but impossible simply because the federal government is not the debtor.

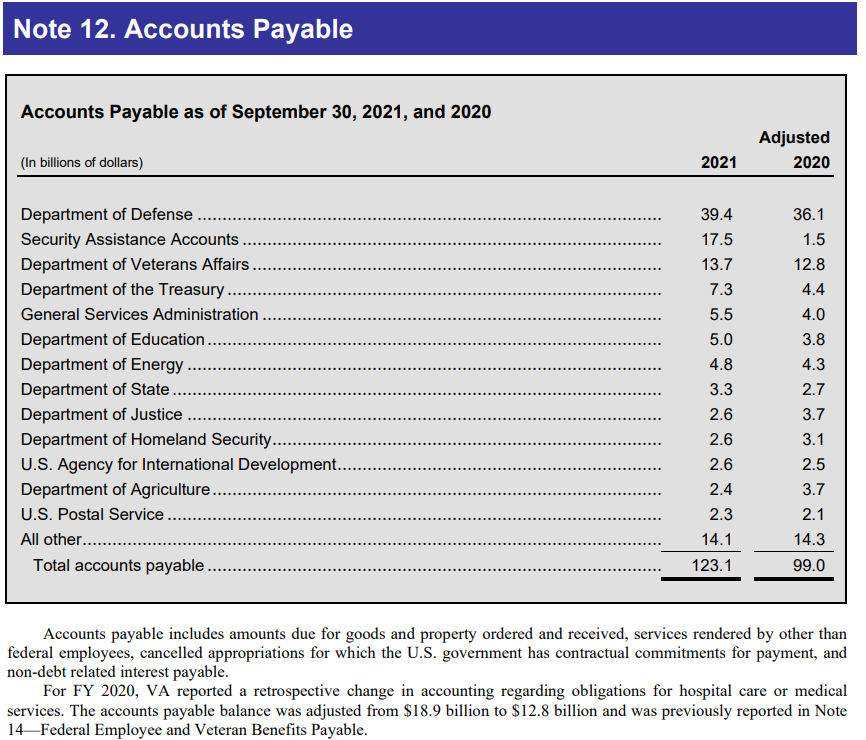

That thing called “federal debt” isn’t federal debt. The actualfederal debt is the amount the federal government owes to vendors of goods and services purchased by the federal government but not yet paid for.

In short, the real federal debt also is known as “Accounts Payable” plus Interest Payable.

The actual federal debt is in the billions, not the trillions, and it is paid reliably every day.

Treasury securities, T-bills, T-notes, and T-bonds are deposit accounts, similar to bank safe deposit accounts that the government never touches.

When you invest in a T-security, you put dollars into youraccount from which only you can withdraw. Just as the contents of your bank safe deposit box are not the debt of your bank, the contents of your T-security account are not the debt of your federal government.

The government didn’t borrow those dollars. It merely holds them separately for safekeeping until you take them back.

Her plea was taken by Peter Schiff, famed investor, and market commentator, as an “official admission that the U.S. is running the world’s largest Ponzi scheme.”

Sadly, Schiff doesn’t seem to know what a “Ponzi scheme is. Quoting from Wikipedia:

A Ponzi scheme is a form of fraud that lures investors and pays profits to earlier investors with funds from more recent investors.

The scheme leads victims to believe that profits come from legitimate business activity (e.g., product sales or successful investments), and they remain unaware that other investors are the source of funds.

A Ponzi scheme can maintain the illusion of a sustainable business if new investors contribute new funds. Most investors do not demand full repayment and still believe in the non-existent assets they purported to own.

Federal T-securities have none of these characteristics.

They are not fraud.

Payment does not come from more recent investors but rather from each depositor’s own deposits and the federal government’s infinite ability to create its sovereign currency.

There is no claim that funds come from any business activity, legitimate or otherwise.

The government does not rely on new investors, nor does it rely on new depositors. The government does not have to accept deposits. Even if every T-security owner demanded payment, the government could comply today.

Peter Schiff merely is using a scare tactic to fool the public. Rather than being a Ponzi scheme, U.S. T-securities are the safest investments known to the world and will continue to be safe so long as no political party is foolish enough to enforce the ridiculous debt limit (aka the “screw-depositors-to-make-political-points” action).

A political stand-off over the debt ceiling has been raging since Republicans regained control of the House of Representatives in the 2022 midterm elections.

President Joe Biden beseeched Congress not to hold the item hostage, suggesting a default could be “calamitous.”

His warnings hit deaf ears in the case of opposing Republicans who used their votes on an extension as leverage to seek spending cuts.

The debt limit has nothing to do with spending cuts because it deals with past spending, not future spending.

The Republican extortion attempt just as easily could be directed at any federal laws, even those having nothing to do with federal finances.

How about enforcing the debt limit unless women Senators wear long dresses, Trump’s rioters are released from prison, or the Capital is painted purple.

All of those have as much relevance to a debt limit as demanding cuts to future spending. The debt limit is a child’s game of, “I’ll hold my breath until I get my way.”

The Treasury can use “extraordinary measures” in the coming months to cover its many financial obligations, including Social Security and Medicare disbursements, but these emergency funds are limited.

At the end of the day, the U.S. simply must borrow more money, as it has done many times before.

The notion that the creator of the U.S. dollar needs to borrow dollars from the people who use the dollar is obviously ridiculous. Where would the so-called “lenders” get the dollars to “lend” if the creator is precluded from creating dollars?

Congress has set the limit for federal borrowing since 1917, raising it over time as government spending and borrowing needs have increased.

Notice the arbitrariness of the above sentence. It correctly assumes Congress can, at its discretion, increase the “debt limit” without regard to the wishes of so-called lenders.” If it were a real debt, the “borrower” could not, at whim, decide to borrow unlimited amounts.

“The U.S. Treas. Sec. has admitted the only way to avoid a default on the National Debt is to raise the #DebtCeiling so the Govt. can borrow from new lenders to repay existing lenders,” Schiff, CEO and chief global strategist at Euro Pacific Capital tweeted on Jan. 16.

“This is an official admission that the U.S. is running the world’s largest Ponzi scheme.”

Oh, the ignorance! Oh, the lies. The “U.S. Treas. Sec.” admitted no such thing. The real way to avoid default is to eliminate the useless debt ceiling. We didn’t always have a debt ceiling. Why do we have one now? Taken from Wikipedia:

In 1979, noting the potential problems of hitting a default, Dick Gephardt imposed the “Gephardt Rule,” a parliamentary rule that deemed the debt ceiling raised when a budget was passed.

This resolved the contradiction in voting for appropriations but not voting to fund them. The rule stood until it was repealed by Congress in 1995.

Get it? When Congress voted for an appropriation, it also voted to fund them.

So, if Congress said, “We authorize spending a billion dollars on a dam,” that meant a billion dollars immediately became available to build a dam.

Makes sense to any normal person. Apparently, though, it was too logical for Congress.

In 1995, Congress said, “When we authorize spending a billion dollars to build a dam, we really don’t authorize paying a billion dollars to build the dam.”

And if that makes sense to you, you should run for Congress. Since that convulsion of childish illogic, Congress has plagued the nation with repeated debt limit crises.

The US raised its debt ceiling (in some form or other) at least 90 times in the 20th century.

The debt ceiling was raised 74 times from March 1962 to May 2011, including 18 times under Ronald Reagan, eight times under Bill Clinton, seven times under George W. Bush, and five times under Barack Obama.

In practice, the debt ceiling has never been reduced, even though the public debt itself may have been reduced.

It should be noted that never has the arbitrary increase of the debt ceiling caused any sort of financial difficulty. There has been no time bomb explosion, fraud, or Ponzi scheme.

In his podcast, Schiff claimed the U.S. government is in a doom spiral where it cannot pay its current lenders back, so it borrows from new lenders repeatedly.

And, oh yes, no “doom spiral.” Though the so-called “debt” has risen from $40 billion to $26 trillion, a 65,000% increase, the federal government still has no difficulty paying its bills.

“Why do people willingly participate? It’s because they don’t realize it’s a Ponzi scheme,” Schiff says.

It’s not.

“They think they’re going to get paid back. When they realize they’re going to be paid back in monopoly money, they’re not going to want to lend.

“Monopoly money”? Is that a scare term like “Ponzi scheme” and “ticking time bomb”?

“In fact, they’re not going to want to hold on to these Treasuries, and the only buyer is going to be the Federal Reserve. And that’s when the printing press is going to overdrive, and the dollar is going to fall through the floor.”

Gee, Schiff, exactly when is that going to happen. It didn’t happen while the printing press was running every day, every week, every month, and every year for the past 84 years. Why are things different now?

As Congress fights over the debt ceiling extension, U.S. credit rating and financial markets are at risk – but here are three assets that Schiff likes as hedges against economic volatility.

And here it comes, the real reason Schiff is serving up bushels of BS:

Wealthy young Americans have lost confidence in the stock market — and are betting on these assets instead. Get in now for strong long-term tailwinds.

Gold. Schiff has long been a fan of the yellow metal.

“The problem with the dollar is it has no intrinsic value,”he once said. “Gold will store its value, and you’ll always be able to buy more food with your gold.”

Except, Schiff neglects to tell you that gold has very little intrinsic value. Gold has less intrinsic value than aluminum, iron, copper, or paper. Gold isn’t used for much other than decoration.

A few teeth fillings, some electronics, that’s about it. Rather than intrinsic value, gold has demand value. People want the stuff mainly because it’s pretty.

As always, he’s putting his money where his mouth is.

Euro Pacific Asset Management’s latest 13F filing shows that as of Sept. 30, Schiff’s company held 1.655 million shares of Barrick Gold (GOLD), 431,952 shares of Agnico Eagle Mines (AEM), and 317,495 shares of Newmont (NEM).

In fact, Barrick was the firm’s top holding, representing 6.8% of its portfolio. Agnico and Newmont were the third and sixth-largest holdings, respectively.

Right. He’s promoting his holdings, trying to get suckers to buy gold.

Gold can’t be printed out of thin air like fiat money, and its safe-haven status means demand typically increases during times of uncertainty.

Except, we always are in times of uncertainty, and gold can be mined out of thin air.

The biggest problem with gold is it costs money to ship, costs more money to store, and costs even more money to insure. And the stuff pays no interest or dividends.

Gold is the classic “bigger fool” investment. Fools buy it hoping to sell it to bigger fools. If you are looking for absolute safety, with no shipping, storage, or insurance costs, plus income, buy T-securities.

Other than that, your best bet is one of the big stock funds. based on the S&P index or similar. And stop worrying about the misnamed federal “debt.” It’s not federal, and it’s not debt, and it’s not a ticking time bomb.

It’s just privately owned, federally guaranteed depositories of U.S. dollars. The only way the “ticking time bomb” can explode is if the debt nuts push the “debt limit” button.

The cure for the “debt limit crisis:” Simply return to the Gephardt Rule. Simple.

Debt-to-GDP Ratio: How High Is Too High? It DependsOctober 07, 2020, By Heather Hennerich

How much federal debt is too much? Is there a tipping point at which it becomes a big problem for a country?

One way to gauge the size of a country’s national debt is to compare it with the size of its economy—the ratio of debt to GDP. (GDP serves as a measure of an economy’s overall size and health, measuring the total market value of all of a country’s goods and services produced in a given year.)

Gross Domestic Product (GDP) is one measure of size, but it is not a measure of health. There is no relationship between the health of an economy and the Debt/GDP ratio.

Heather Hennerich’s claim that “GDP serves as a measure of an economy’s overall size and health” simply is false. In fact, the Debt/GDP ratio signifies nothing, nothing at all.

Yes, it’s a fraction that is quoted all the time by people who should know better. But you might as well quote an apples/Apple phones comparison.

Debt is a cumulative measure of federal government deficitssince the beginning of time.GDP is a one yearmeasure of an entirenation’sspending.

If you want a similar comparison try the total amount of water a city has wasted vs. the amount of orange juice the mayor drank, yesterday. Call it the “waste/OJ” ratio, and claim it means something.

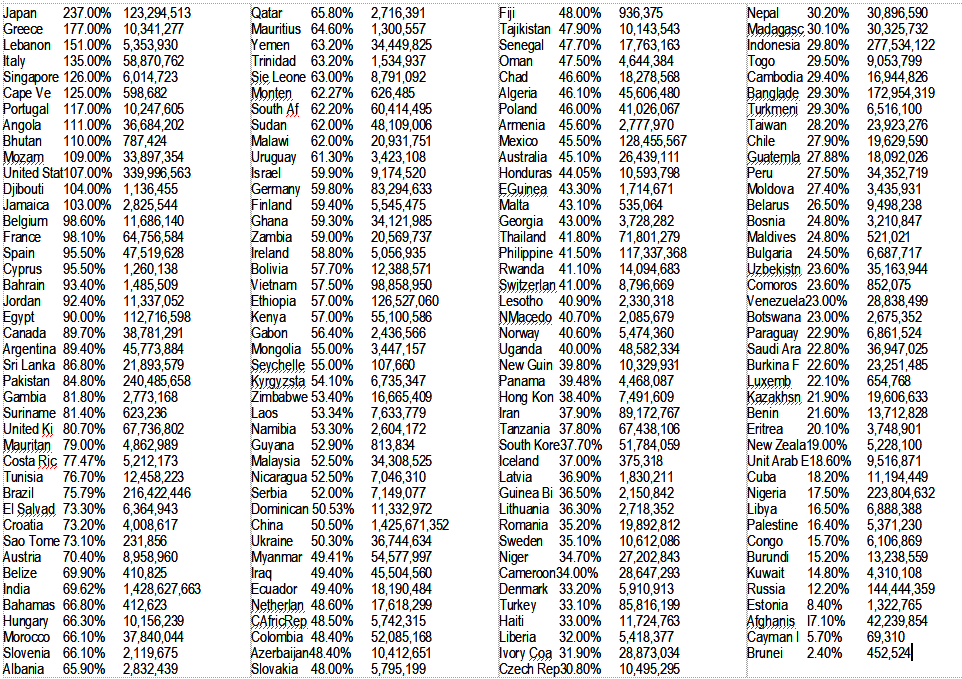

Skim the following list of Debt/GDP ratios, and see if you can find any relationship between the Debt/GDP ratio, the population of the nation, and what you know about the health of its economy.

Begin with the fact that wealthy, powerfulJapan and weak, impoverished Greece are 1,2 on the list. The United States falls right between Mozambique and Djbouti on the list. Russia has one of the lowest ratios, indicating the “health” of its economy.

NATION — DEBT/GDP RATIO — POPULATION

The Debt/GDP ratio does not measure the health of an economy.

The next time you hear or read some pundit’s concerns about America’s Debt/GDP ratio, you will know that pundit does not know what he/she is talking about.

The U.S. federal debt-to-GDP ratio was 107% late last year, and it went up to nearly 136% in the second quarter of 2020 with the passage of a coronavirus relief package.

By comparison, Japan’s ratio at the end of 2019 was higher: about 200%, according to data from the Bank of Japan and Japan’s Ministry of Foreign Affairs and calculations by St. Louis Fed Economist Miguel Faria-e-Castro.

By comparing the total federal debt to the size of a country’s economy, we can see how that government can use the resources at hand to finance the debt, according to Your Guide to America’s Finances from the U.S. Department of Treasury.

This wrongly assumes that federal (Monetarily Sovereign) finances are like personal (monetarily non-sovereign) finances.

The federal government does not “finance” its debt. (Here the word “finance” seems to mean pay it off or perhaps pay interest on it.)

The so-called “debt” is nothing more than deposits into privately owned, Treasury Security accounts. We say “privately owned” because the federal government never touches those dollars. As a depositor, you alone decide when to take dollars out or leave them in (following certain initial rules). The dollars are yours when you deposit them and when you retrieve them.

That’s why they are not a “loan.”If they were a loan, the borrower would control them. But there is no borrower. The federal government never borrows dollars.

These accounts are similar to safe deposit boxes into which you place your valuables. Just as the bank never touches those valuables, the federal government, being Monetarily Sovereign, never needs to touch your deposited money.

To pay off the so-called “debt” the government merely returns your dollars to you, the depositor.

As for the “resources at hand,” we assume this means that in some mysterious way, the government supposedly uses GDP or perhaps Lake Michigan, to pay off T-securities. No one knows how that works.

It’s all gibberish and nonsensical.

In his research, Faria-e-Castro explores big questions about the economy, so we asked him about this issue last year.

Deficit spending means that a government is choosing not to raise taxes today to pay for that spending but is choosing to wait until tomorrow, Faria-e-Castro said.

Monetarily non-sovereign governments (state, local, euro) use taxes to fund spending. But Monetarily Sovereign governments (US, Canada, Japan, Australia, et al) do not use taxes to fund spending. A huge difference Faria-e-Castro seems not to understand. (And he’s an economist for the St. Louis Fed!!)

Monetarily Sovereign governments use taxes to direct their economies by taxing what they want to discourage and giving tax breaks to what they want to encourage.

There is scant similarity between federal finances and state/local government finances. Those who do not understand the difference should not be writing for the Federal Reserve.

While state/local governments rely on tax income, the federal government could continue spending, forever, with no tax income at all.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Then we come to this bit of misinformation, that applies to state/local governments, but not to the federal government:

When federal spending exceeds revenue, the difference is a deficit. The government mostly borrows money to make up the difference.

The federal government doesn’t borrow dollars. Why would it, given its infinite ability to create new dollars?

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

Greenspan understood Monetary Sovereignty. Too bad he didn’t make his knowledge clear so we no longer would have ridiculous laws mandating a “debt ceiling.”

Now, again, the nation is paralyzed by the useless debt ceiling while the GOP demands spending cuts though they have no idea what they want to cut. (They don’t have the courage to admit they really would like to cut Social Security and Medicare, so as to help the rich become richer.)

The total national debt is an accumulation of federal deficits over time, minus any repayments of debt, among other factors.

By law, the federal government accepts deposits into T-security accounts equal to the accumulation of federal deficits. This is a point of confusion, because people mistakenly are led to believe that the deposits pay for the deficits. They don’t. The deposits pay for nothing.

The purpose of deposits (i.e. T-securities) is to provide a safe place to store dollars, which stabilizes the dollar.

A big consequence of deficit spending is that the fiscal burden shifts from one generation to the next, Faria-e-Castro said.

This is entirely wrong. You never have endured a “fiscal burden” for previous deficits. The government pays for all its deficits by creating new dollars from thin air. This is not a burden on anyone, not on you and not on the government.

The “fiscal burden” myth, promulgated through the decades, is a result of ignorance about Monetary Sovereignty.

That’s fine if a country’s economy is growing, because you know that the next generation will, on average, be better off than the current one, and likely able to pay a little more in taxes to decrease the debt, Faria-e-Castro said.

But if a country’s economy is slowing and economic growth rates are lower than they used to be, “this starts becoming a more divisive issue.”

It’s only divisive for those who are ignorant about federal finances. “The next generation” doesn’t pay for back debt. The taxes paid by every generation see the same fate: All federal taxes are destroyed upon receipt.

Tax dollars are paid from what is known as “the M2 money supply measure.” The moment they are received by the Treasury, they cease to be part of any money supply measure. In short, they are destroyed.

Say the government of “Country X” borrows money to cover its deficits, Faria-e-Castro said. Investors—many of them international—buy that debt and then want to be repaid.

“One day, the president of Country X can just organize a press conference and just tell people, ‘OK. We’re not paying,’” Faria-e-Castro said. “That’s an outright hard default.”

But countries that take that action will have trouble borrowing again. Lenders will be less willing to lend to them and will charge higher interest rates.

Here, Faria-e-Castro displays remarkable ignorance of national finance because he doesn’t differentiate between Monetarily Sovereign governments and monetarily non-sovereign governments.

The monetarily non-sovereign governments borrow money because they have no sovereign currency.

“The president of Country X can call the governor of the central bank and say, ‘OK, you have to print money to pay for this debt,’” Faria-e-Castro said.

In a country where the central bank is not an independent authority, the central bank can be pressured more easily by politicians to start printing money to pay for the country’s debt, he said.

But the flow of new money will invariably lead to high inflation in that country. That erases the value of the debt—a “soft default”—but it also typically kicks off hyperinflation, Faria-e-Castro said.

Astoundingly, that is precisely what does not happen, and the evidence is there for all to see.

Whether one views federal debt as “Federal Debt Held by The Public” (first graph below) or as “Federal Debt as a Percent of Gross Domestic Product” (2nd graph below), there is no relationship between federal debt and inflation.

There is no relationship between federal debt held by the public and inflation. Peaks and valleys do not correspond.There is no relationship between the Debt/GDP ratio and inflation. Peaks an valleys do not correspond.

It never ceases to amaze that obvious and readily available statistics are ignored by so-called “experts” in favor of hand-me-down beliefs having no basis in fact.

Inflation is not related to federal spending because inflation is caused by shortages of key goods and services.

Some claim that federal deficit spending causes those shortages, but for years and years, we’d seen massive federal spending, with low inflation.

The federal dollars that led to increased demand also facilitated increased supply. That is how capitalism works; supply rises to meet demand.

But suddenly, in 2020, we began to see inflation. What suddenly changed in 2020?

COVID.

The inflation that came suddenly in 2020, an inflation we still endure, was caused by COVID-related shortages of oil, food, computer chips, lumber, steel, shipping, labor, etc.

There is no statistical relationship between federal deficit spending and inflation.

But would you like to see something that does have a relationship with inflation?Shortages of key goods and services (most often oil) cause inflation. Oil prices are closely related to supply. The peaks and valleys correspond between oil supply and inflation.

Yes, if you’re looking for the primary cause of inflation, start with oil shortages, which then relate to other shortages. COVID was responsible for shortages of oil, food, etc.

It would be hard to make the case that after decades of big deficits, suddenly federal spending caused an increase in oil demand. Inflations are supply-related.

Federal spending actually can cure inflation if the spending is directed toward obtaining the scarce goods and services and distributing them to the public.

Contrary to popular wisdom, restricting federal spending during an inflation is counterproductive.

Hyperinflation is excessive inflation, with very rapid and out of control general price increases. Economists usually consider monthly inflation rates of above 50% as hyperinflation episodes, as noted in a 2018 On the Economy blog post.

Faria-e-Castro explained, countries that are not politically stable and don’t have independent central banks are not going to have very credible institutions. As a consequence, they can’t borrow easily: Investors won’t be willing to lend them that much for fear of future default.

But the debt of countries with strong institutions and independent central banks—like the U.S. and Japan—doesn’t present the same risks, Faria-e-Castro said.

He thinks the difference between countries has to do with a “strong, central bank.” Poppycock.

The central bank of a Monetarily Sovereign nation is strong because Monetary Sovereignty makes it strong. It has the unlimited ability to create its nation’s sovereign currency.

Monetarily non-sovereign nations also have central banks. Sadly, these banks are weak because they do not have the unlimited ability to create sovereign currency: They have no sovereign currency to create.

Few believe, for example, that the Japanese government will ever pressure the Bank of Japan to actually “print” money to pay for the country’s debt, Faria-e-Castro said.

First, the Bank of Japan “prints” (creates) yen all the time. No “pressure” needed. It’s a normal, daily process.

And second, those yen do not pay for the country’s debt. They pay for the country’s purchases. Like the U.S., the Japanese government does not borrow to pay for anything. It creates yen to pay for everything.

“As a consequence, these countries can typically sustain very high levels of debt to GDP,” he said. “Because people really believe that they will be repaid, so they can keep lending.”

There’s that phony Debt/GDP ratio, again. The U.S. doesn’t borrow. It issues Treasury bills, notes, and bonds, and if not enough are issued to satisfy the law, the Federal Reserve Bank simply buys the rest.

The strength of institutions also affects interest rates on the debt, which is another factor in determining the sustainability of high debt-to-GDP ratios.

No, the Fed determines short-term interest rates by fiat. And that meaningless Debt/GDP ratio is infinitely sustainable.

If a country has strong institutions, interest rates on the debt will be low, which means the cost of borrowing will be low, Faria-e-Castro said.

When he talks about the “cost of borrowing,” he mistakenly believes government T-securities represent borrowing. They don’t. They represent deposits.

These deposits are paid off, not with taxes but by returning the dollars that are in the accounts.

And whether interest rates are high or low is irrelevant to a Monetarily Sovereign nation having the infinite ability to create the currency to pay interest.

Because the institutional strength and riskiness of countries varies, there’s no rule of thumb for how high a debt-to-GDP ratio can be before it poses a risk to a country’s economy.

“At the end of the day, it all boils down to strong and independent institutions,” Faria-e-Castro said.

“A lot of economists try to study this. There’s no single measure that we can come up with… Measuring institutional strength is not obvious.”

It’s not obvious because Faria-e-Castro is confusing federal financing with private financing. He doesn’t understand the difference between Monetary Sovereignty and monetary non-sovereignty. And he’s speaking for the Federal Reserve!? Yikes!

He falls in line with the current mistaken belief that fighting inflations requires the pain of recession that cuts in federal spending beget.

That is the kind of leadership that destroys nations.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

And then they died.

But for the whales, nature’s experiment with size ended, to be replaced by the experiment with intelligence, which featured the mammals.

While many dinosaurs were warm blooded, and had large brains, both facilitating intelligence, our hands and upright stature seem to have brought us to the apex of intelligence.

So far, for the experiment continues.

The big news in intelligence is artificial intelligence (AI) as demonstrated in chatbots.

IBM says, “

And then they died.

But for the whales, nature’s experiment with size ended, to be replaced by the experiment with intelligence, which featured the mammals.

While many dinosaurs were warm blooded, and had large brains, both facilitating intelligence, our hands and upright stature seem to have brought us to the apex of intelligence.

So far, for the experiment continues.

The big news in intelligence is artificial intelligence (AI) as demonstrated in chatbots.

IBM says, “:no_upscale()/cdn.vox-cdn.com/uploads/chorus_image/image/63710580/terminator-comic.0.1537146051.0.jpg)